- Cost-volume-profit (cvp) analysis

Содержание

- 2. COST-VOLUME-PROFIT (CVP) ANALYSIS CVP analysis examines the interaction of a firm’s sales volume, selling price, cost

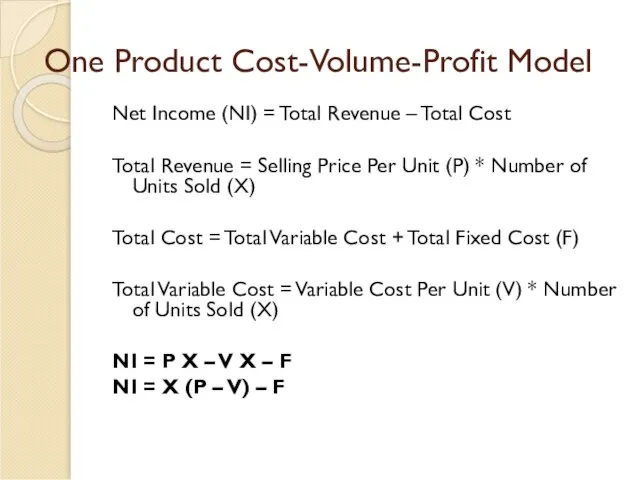

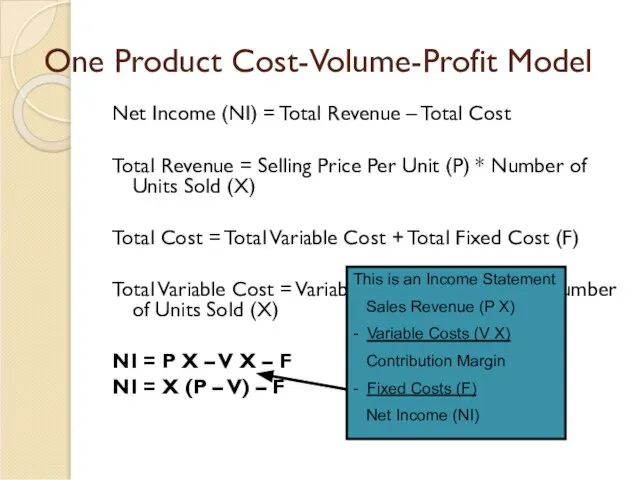

- 3. One Product Cost-Volume-Profit Model Net Income (NI) = Total Revenue – Total Cost Total Revenue =

- 4. One Product Cost-Volume-Profit Model Net Income (NI) = Total Revenue – Total Cost Total Revenue =

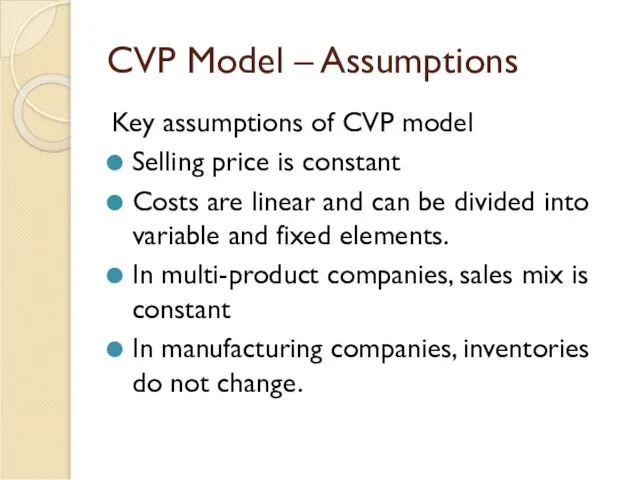

- 5. CVP Model – Assumptions Key assumptions of CVP model Selling price is constant Costs are linear

- 6. Contribution Margin Ratio Or, in terms of units, the contribution margin ratio is: For Racing Bicycle

- 7. Changes in Fixed Costs and Sales Volume What is the profit impact if Chocolate Co. can

- 8. Change in Variable Costs and Sales Volume What is the profit impact if Chocolate Co. can

- 9. Change in Fixed Cost, Sales Price and Volume What is the profit impact if Chocolate Co.

- 10. Break-Even Analysis Break-even analysis can be approached in two ways: Equation method Contribution margin method

- 11. Equation Method Profits = (Sales – Variable expenses) – Fixed expenses Sales = Variable expenses +

- 12. Equation Method $16Q = $12Q + $40,000 + $0 Where: Q = Number of chocolates sold

- 13. Equation Method We calculate the break-even point as follows: $500Q = $300Q + $80,000 + $0

- 14. Equation Method The equation can be modified to calculate the break-even point in sales dollars. Sales

- 15. Equation Method X = 0.75X + $40,000 + $0 0.25X = $40,000 X = $40,000 ÷

- 16. Contribution Margin Method The contribution margin method has two key equations.

- 17. Contribution Margin Method Let’s use the contribution margin method to calculate the break-even point in total

- 18. Target Profit Analysis The equation and contribution margin methods can be used to determine the sales

- 19. The CVP Equation Method Sales = Variable expenses + Fixed expenses + Profits $16Q = $12Q

- 20. The Contribution Margin Approach The contribution margin method can be used to determine that 900 bikes

- 21. The Margin of Safety The margin of safety is the excess of budgeted (or actual) sales

- 22. Multi-Product CVP Model

- 23. Multi-Product CVP Model - Example Example: Suppose FC = $200,000; P1 = $5; V1 = $2;

- 24. Multi-Product CVP Model - Example Any point on the line is a possible combination of X1

- 25. Multi-Product CVP Model - Example Suppose the firm produces and sells the same number of the

- 26. Multi-Product CVP Model

- 27. Multi-Product CVP Model - Example

- 28. Operating Leverage

- 29. Operating Leverage - Example Calculate Extreme’s degree of operating leverage DOL = $200,000 / $40,000 =

- 30. Operating Leverage - Example Sales $600,000 VC 360,000 CM 240,000 FC 160,000 NI $ 80,000

- 31. Operating Leverage - Example Calculate Extreme’s operating income, if Extreme experiences a drop of 30% in

- 32. Operating Leverage - Example Sales $350,000 VC 210,000 CM 140,000 FC 160,000 NI $ (20,000)

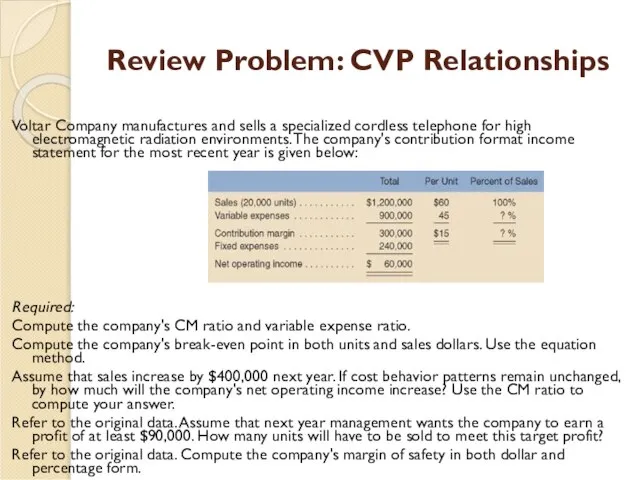

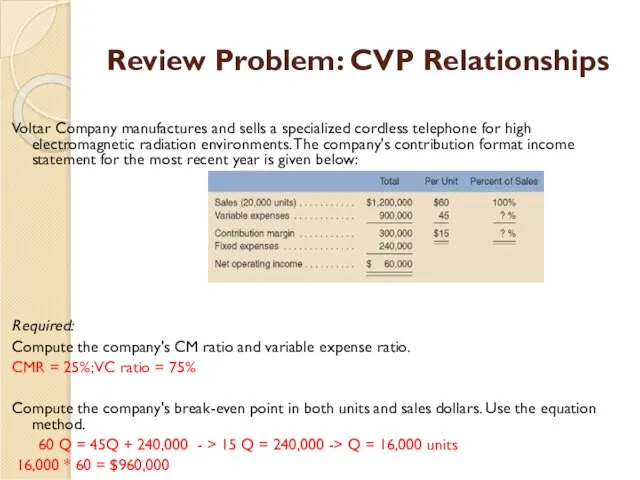

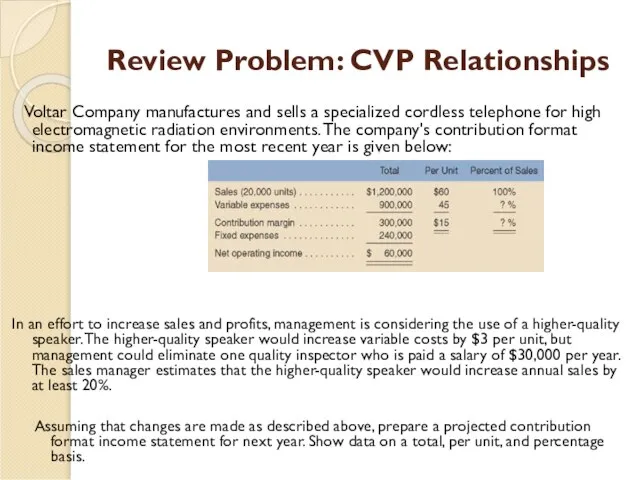

- 33. Review Problem: CVP Relationships Voltar Company manufactures and sells a specialized cordless telephone for high electromagnetic

- 34. Review Problem: CVP Relationships Voltar Company manufactures and sells a specialized cordless telephone for high electromagnetic

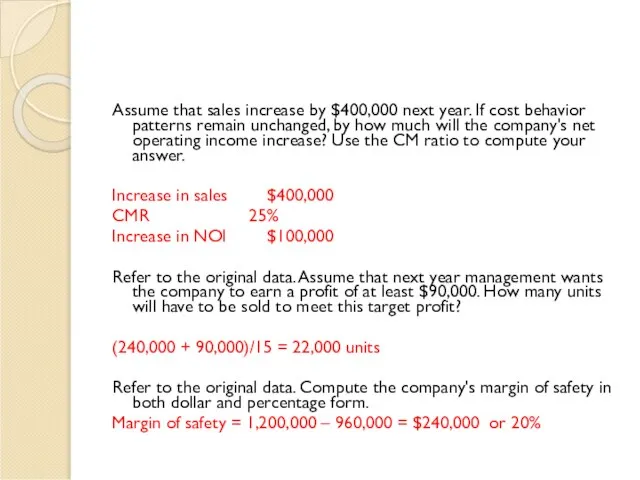

- 35. Assume that sales increase by $400,000 next year. If cost behavior patterns remain unchanged, by how

- 36. Review Problem: CVP Relationships Voltar Company manufactures and sells a specialized cordless telephone for high electromagnetic

- 37. Assume that through a more intense effort by the sales staff, the company's sales increase by

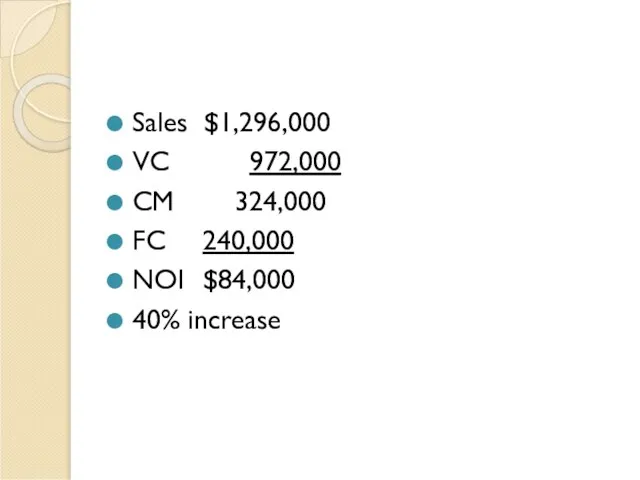

- 38. Sales $1,296,000 VC 972,000 CM 324,000 FC 240,000 NOI $84,000 40% increase

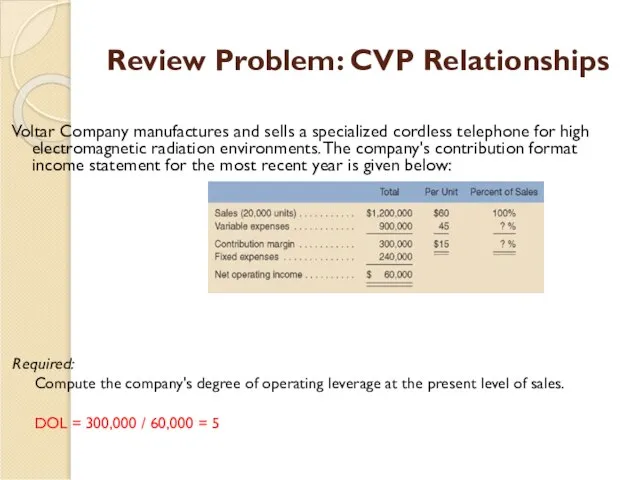

- 39. Review Problem: CVP Relationships Voltar Company manufactures and sells a specialized cordless telephone for high electromagnetic

- 41. Скачать презентацию

COST-VOLUME-PROFIT (CVP) ANALYSIS

CVP analysis examines the interaction of a firm’s sales

COST-VOLUME-PROFIT (CVP) ANALYSIS

CVP analysis examines the interaction of a firm’s sales

One Product Cost-Volume-Profit Model

Net Income (NI) = Total Revenue – Total

One Product Cost-Volume-Profit Model

Net Income (NI) = Total Revenue – Total

One Product Cost-Volume-Profit Model

Net Income (NI) = Total Revenue – Total

One Product Cost-Volume-Profit Model

Net Income (NI) = Total Revenue – Total

CVP Model – Assumptions

Key assumptions of CVP model

Selling price is

CVP Model – Assumptions

Key assumptions of CVP model

Selling price is

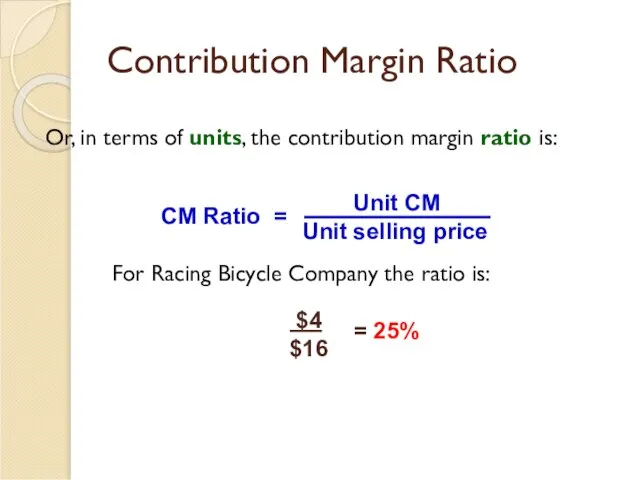

Contribution Margin Ratio

Or, in terms of units, the contribution margin ratio

Contribution Margin Ratio

Or, in terms of units, the contribution margin ratio

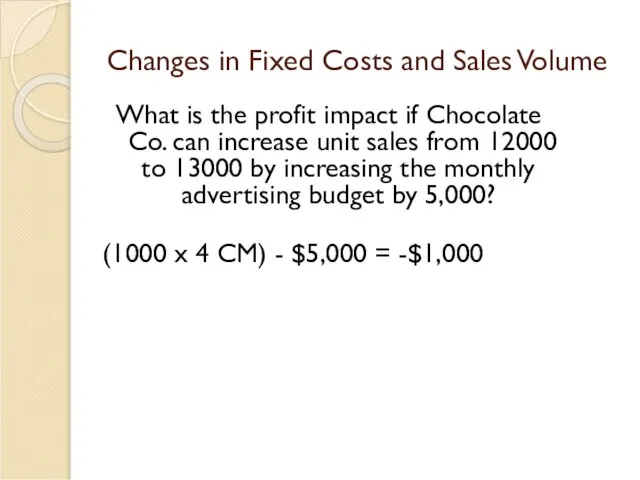

Changes in Fixed Costs and Sales Volume

What is the profit impact

Changes in Fixed Costs and Sales Volume

What is the profit impact

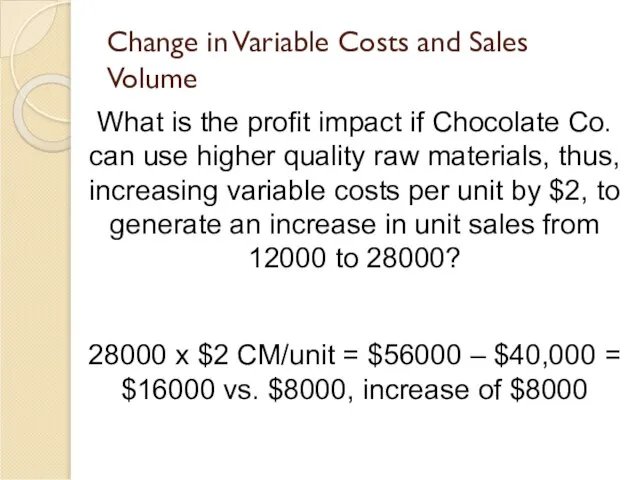

Change in Variable Costs and Sales Volume

What is the profit impact

Change in Variable Costs and Sales Volume

What is the profit impact

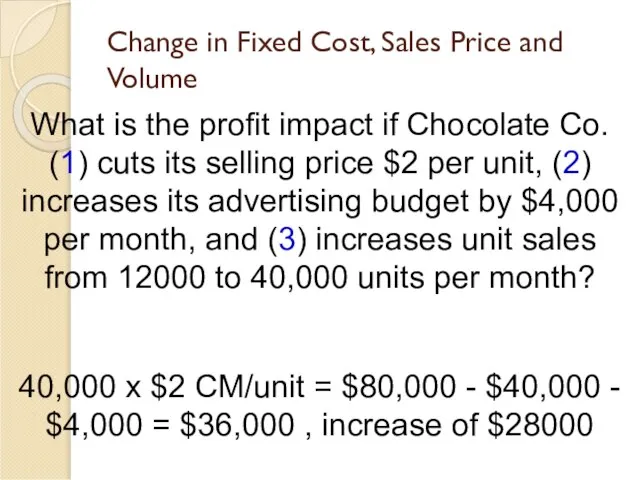

Change in Fixed Cost, Sales Price and Volume

What is the profit

Change in Fixed Cost, Sales Price and Volume

What is the profit

Break-Even Analysis

Break-even analysis can be approached in two ways:

Equation method

Contribution

Break-Even Analysis

Break-even analysis can be approached in two ways:

Equation method

Contribution

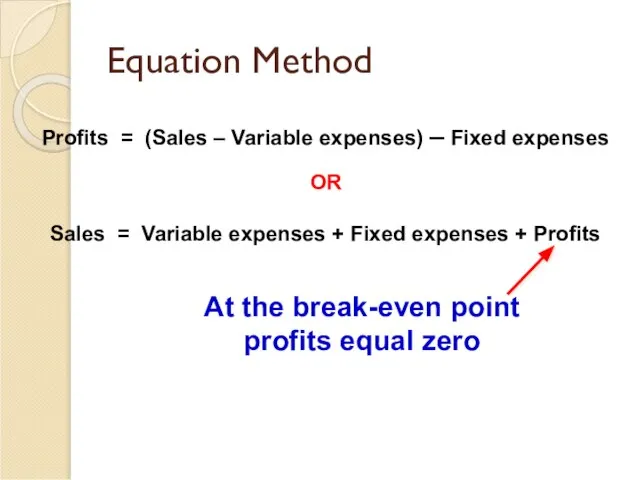

Equation Method

Profits = (Sales – Variable expenses) – Fixed expenses

Sales =

Equation Method

Profits = (Sales – Variable expenses) – Fixed expenses

Sales =

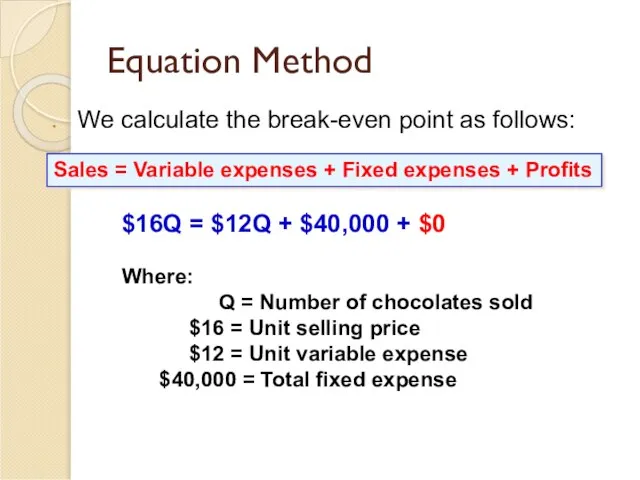

Equation Method

$16Q = $12Q + $40,000 + $0

Where:

Q = Number

Equation Method

$16Q = $12Q + $40,000 + $0

Where:

Q = Number

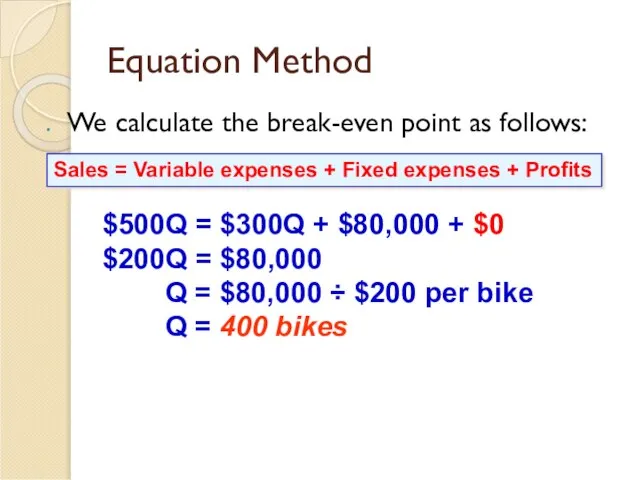

Equation Method

We calculate the break-even point as follows:

$500Q = $300Q +

Equation Method

We calculate the break-even point as follows:

$500Q = $300Q +

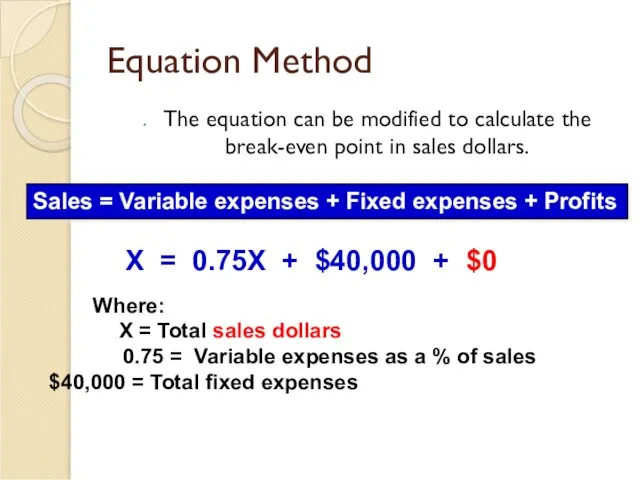

Equation Method

The equation can be modified to calculate the break-even point

Equation Method

The equation can be modified to calculate the break-even point

Equation Method

X = 0.75X + $40,000 + $0

0.25X =

Equation Method

X = 0.75X + $40,000 + $0

0.25X =

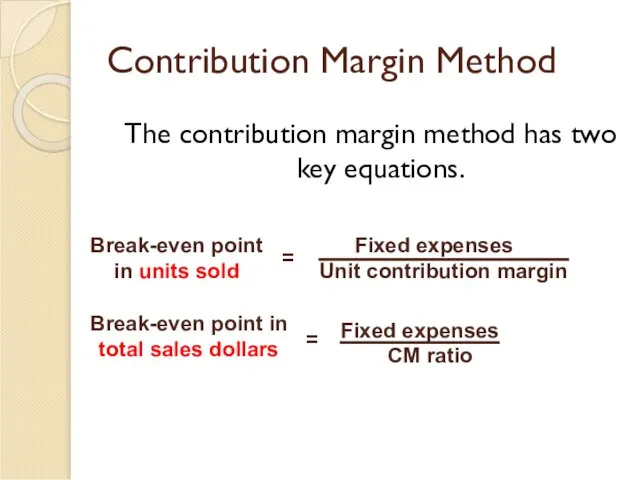

Contribution Margin Method

The contribution margin method has two key equations.

Contribution Margin Method

The contribution margin method has two key equations.

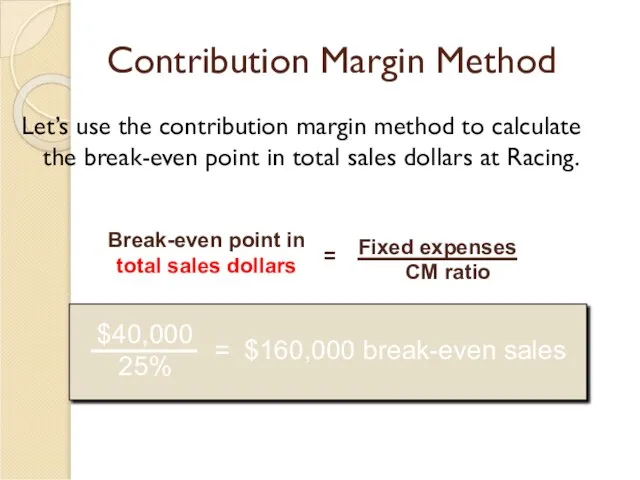

Contribution Margin Method

Let’s use the contribution margin method to calculate the

Contribution Margin Method

Let’s use the contribution margin method to calculate the

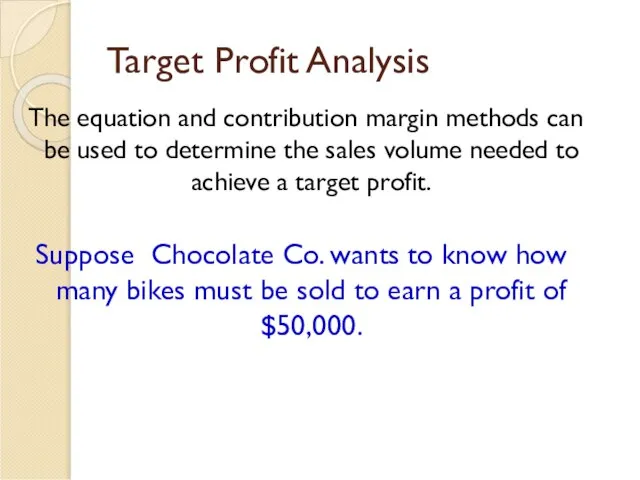

Target Profit Analysis

The equation and contribution margin methods can be

Target Profit Analysis

The equation and contribution margin methods can be

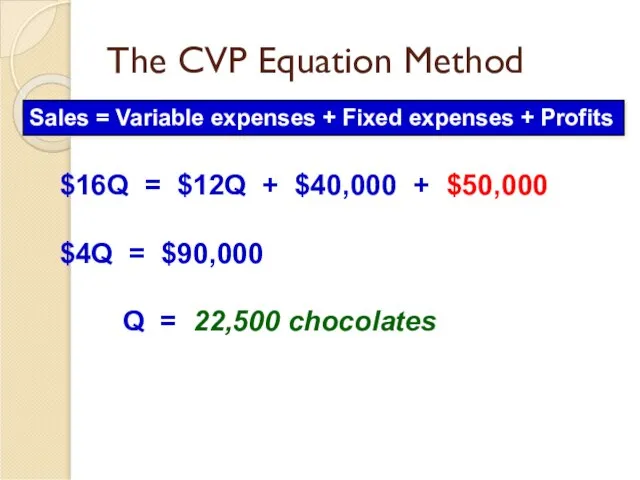

The CVP Equation Method

Sales = Variable expenses + Fixed expenses +

The CVP Equation Method

Sales = Variable expenses + Fixed expenses +

The Contribution Margin Approach

The contribution margin method can be used

The Contribution Margin Approach

The contribution margin method can be used

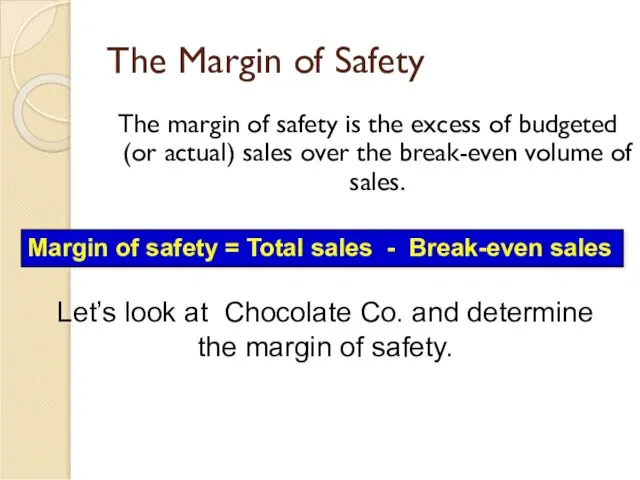

The Margin of Safety

The margin of safety is the excess of

The Margin of Safety

The margin of safety is the excess of

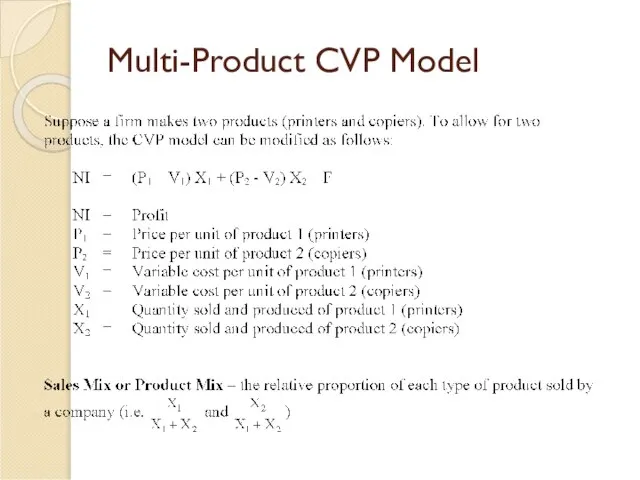

Multi-Product CVP Model

Multi-Product CVP Model

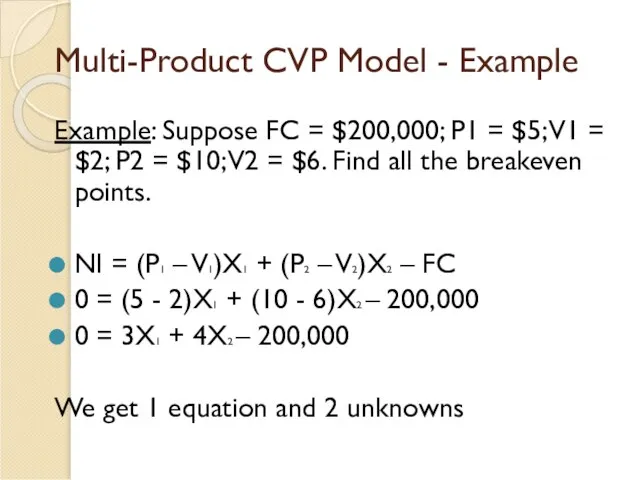

Multi-Product CVP Model - Example

Example: Suppose FC = $200,000; P1 =

Multi-Product CVP Model - Example

Example: Suppose FC = $200,000; P1 =

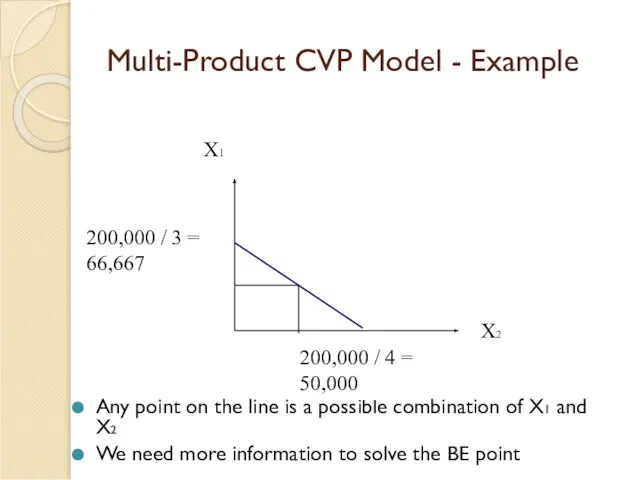

Multi-Product CVP Model - Example

Any point on the line is a

Multi-Product CVP Model - Example

Any point on the line is a

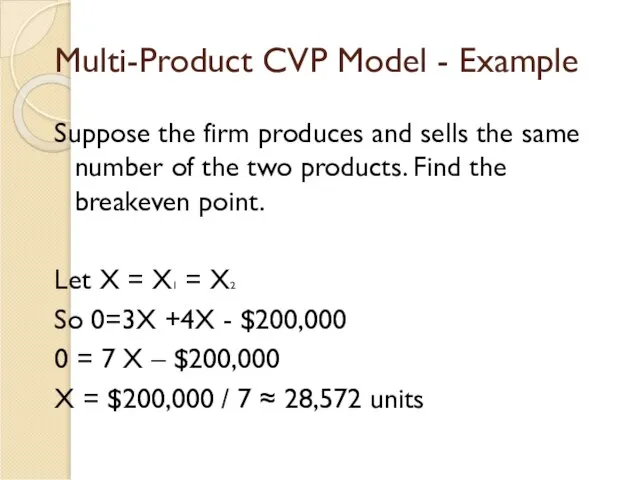

Multi-Product CVP Model - Example

Suppose the firm produces and sells the

Multi-Product CVP Model - Example

Suppose the firm produces and sells the

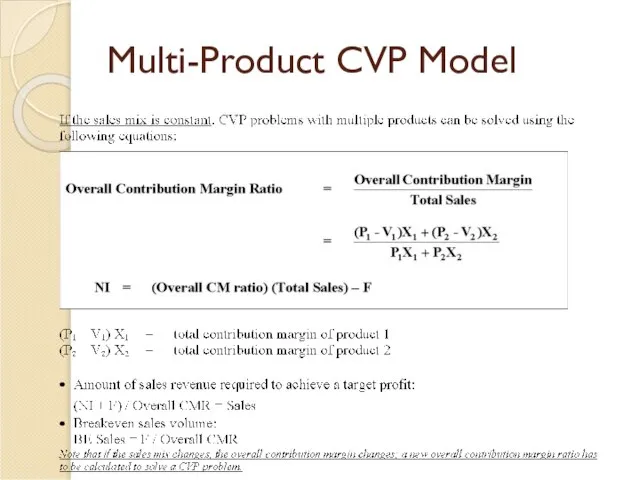

Multi-Product CVP Model

Multi-Product CVP Model

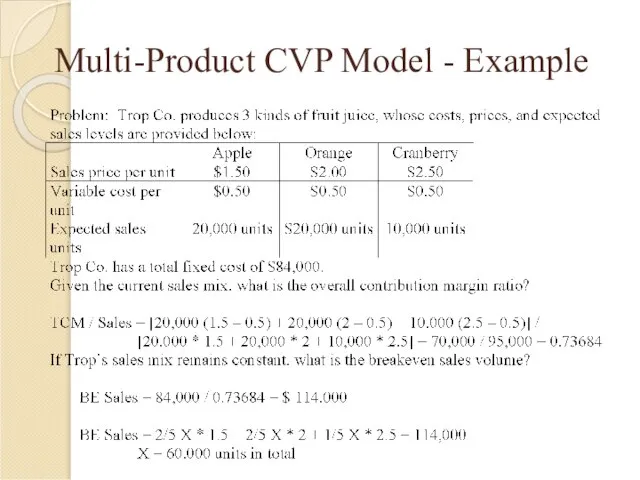

Multi-Product CVP Model - Example

Multi-Product CVP Model - Example

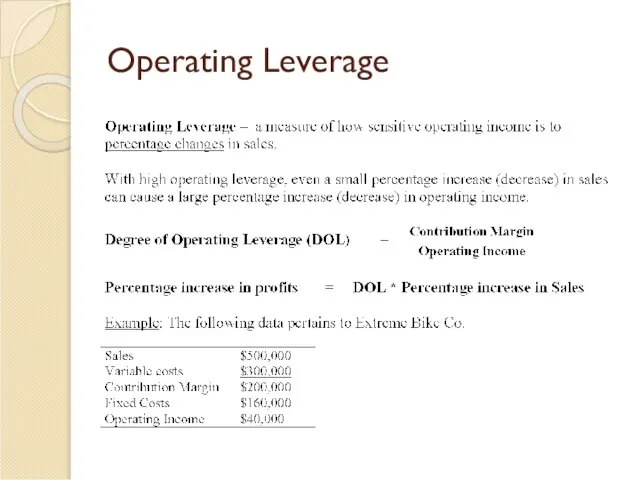

Operating Leverage

Operating Leverage

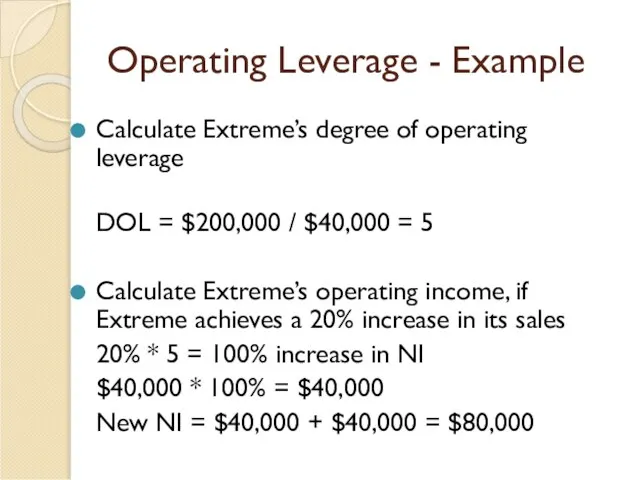

Operating Leverage - Example

Calculate Extreme’s degree of operating leverage

DOL = $200,000

Operating Leverage - Example

Calculate Extreme’s degree of operating leverage

DOL = $200,000

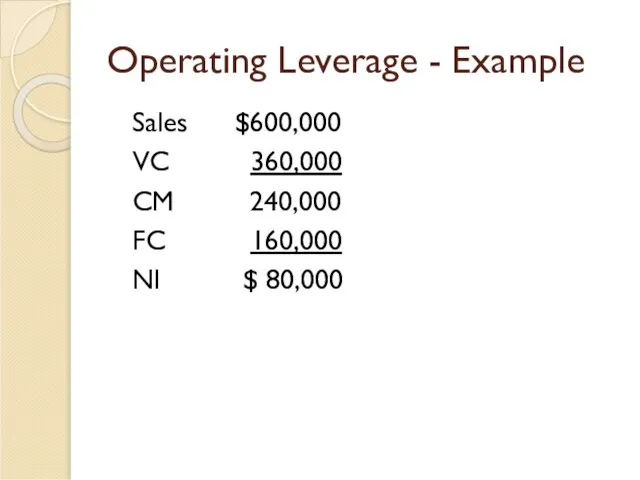

Operating Leverage - Example

Sales $600,000

VC 360,000

CM 240,000

FC 160,000

NI $ 80,000

Operating Leverage - Example

Sales $600,000

VC 360,000

CM 240,000

FC 160,000

NI $ 80,000

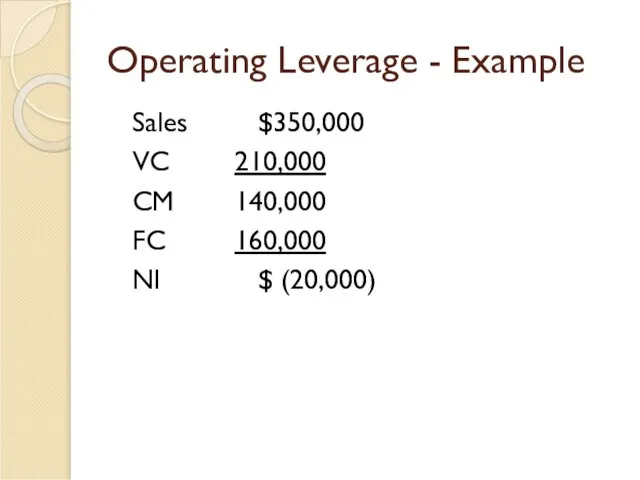

Operating Leverage - Example

Calculate Extreme’s operating income, if Extreme experiences a

Operating Leverage - Example

Calculate Extreme’s operating income, if Extreme experiences a

Operating Leverage - Example

Sales $350,000

VC 210,000

CM 140,000

FC 160,000

NI $ (20,000)

Operating Leverage - Example

Sales $350,000

VC 210,000

CM 140,000

FC 160,000

NI $ (20,000)

Review Problem: CVP Relationships

Voltar Company manufactures and sells a specialized

Review Problem: CVP Relationships

Voltar Company manufactures and sells a specialized

Review Problem: CVP Relationships

Voltar Company manufactures and sells a specialized

Review Problem: CVP Relationships

Voltar Company manufactures and sells a specialized

Assume that sales increase by $400,000 next year. If cost behavior

Assume that sales increase by $400,000 next year. If cost behavior

Review Problem: CVP Relationships

Voltar Company manufactures and sells a specialized

Review Problem: CVP Relationships

Voltar Company manufactures and sells a specialized

Assume that through a more intense effort by the sales staff,

Assume that through a more intense effort by the sales staff,

Sales $1,296,000

VC 972,000

CM 324,000

FC 240,000

NOI $84,000

40% increase

Sales $1,296,000

VC 972,000

CM 324,000

FC 240,000

NOI $84,000

40% increase

Review Problem: CVP Relationships

Voltar Company manufactures and sells a specialized

Review Problem: CVP Relationships

Voltar Company manufactures and sells a specialized

Предприятия в экономике

Предприятия в экономике Понятие о мировом рынке. Международное экономическое сотрудничество

Понятие о мировом рынке. Международное экономическое сотрудничество Инвестиционный паспорт муниципального образования «Медвежьегорский муниципальный район»

Инвестиционный паспорт муниципального образования «Медвежьегорский муниципальный район» Имитационно-ролевая игра

Имитационно-ролевая игра Экономические системы. Виды, механизм функционирования

Экономические системы. Виды, механизм функционирования Анализ рынка и оффер

Анализ рынка и оффер Мировая экономика и международные экономические отношения в начале XXI века. (Тема 1)

Мировая экономика и международные экономические отношения в начале XXI века. (Тема 1) Рыночные операции: исходный анализ спроса и предложения и его применение

Рыночные операции: исходный анализ спроса и предложения и его применение Человек и техника. Проблемы и перспективы взаимодействия

Человек и техника. Проблемы и перспективы взаимодействия Финансы коммерческих организаций. (Тема 4)

Финансы коммерческих организаций. (Тема 4) Слияния и поглощения и стратегические альянсы

Слияния и поглощения и стратегические альянсы Анализ обеспеченности предприятия трудовыми ресурсами и их использования

Анализ обеспеченности предприятия трудовыми ресурсами и их использования История развития экономико-географических теорий и концепций: научно-практические труды выдающихся географов

История развития экономико-географических теорий и концепций: научно-практические труды выдающихся географов Инфляция и ее виды

Инфляция и ее виды Економічна розвідка як фактор у конкурентній боротьбі

Економічна розвідка як фактор у конкурентній боротьбі Риски ВЭД

Риски ВЭД Поддержка малого и среднего предпринимательства в Саратовской области

Поддержка малого и среднего предпринимательства в Саратовской области Проектирование урока экономики. Лекция 3

Проектирование урока экономики. Лекция 3 Теоретические основы современных технологий

Теоретические основы современных технологий Рост производительности труда. (Задача 12)

Рост производительности труда. (Задача 12) Потребности, блага, экономический выбор

Потребности, блага, экономический выбор Предмет изучения институциональной экономики и ее место в современной экономической теории

Предмет изучения институциональной экономики и ее место в современной экономической теории Модели эндогенного роста

Модели эндогенного роста Региональная экономическая диагностика

Региональная экономическая диагностика Продукция организации (предприятия)

Продукция организации (предприятия) Развитие супермаркетов на розничном рынке: зарубежная практика

Развитие супермаркетов на розничном рынке: зарубежная практика Рынки факторов производства и спрос на экономические ресурсы

Рынки факторов производства и спрос на экономические ресурсы Экономико-правовое содержание собственности

Экономико-правовое содержание собственности