- Financial Evaluation of an IT Project

Содержание

- 2. Contents 5В050700-Management

- 3. Plan of the practice As continue of the last lection we will try today to build

- 4. Sources of Return (1/4) 5В050700-Management Some projects are implemented to generate income, others to reduce costs,

- 5. Table 10.1 contains columns for different types of recoil, which may be for topics. If you

- 6. Sources of Return (3/4) 5В050700-Management Where do the numbers come from? Ideally - from a marketing

- 7. Sources of Return (4/4) 5В050700-Management Apart from the new income and income growth is the retained

- 8. New Income(1/2) 5В050700-Management We don't have reliable data. Sales Representative Terry says that based on current

- 9. New Income(2/2) 5В050700-Management

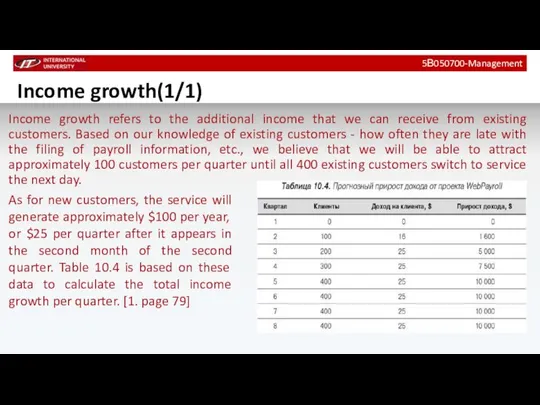

- 10. Income growth(1/1) 5В050700-Management Income growth refers to the additional income that we can receive from existing

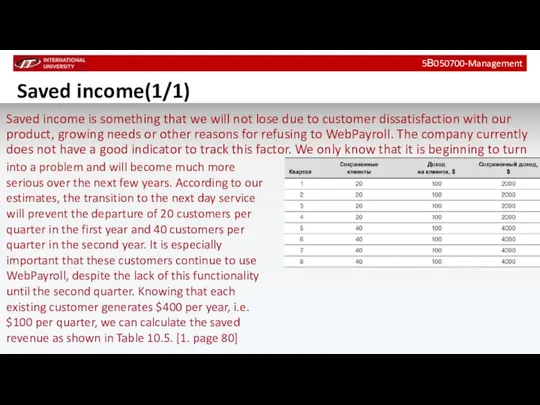

- 11. Saved income(1/1) 5В050700-Management Saved income is something that we will not lose due to customer dissatisfaction

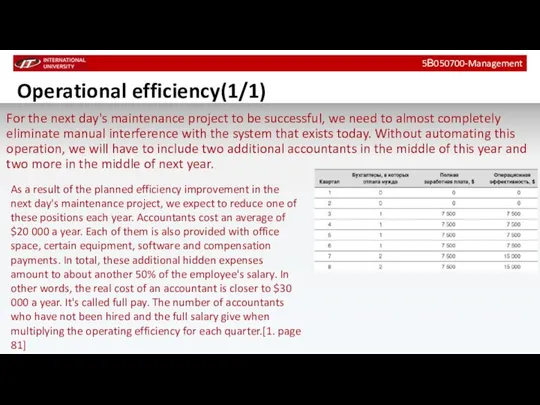

- 12. Operational efficiency(1/1) 5В050700-Management For the next day's maintenance project to be successful, we need to almost

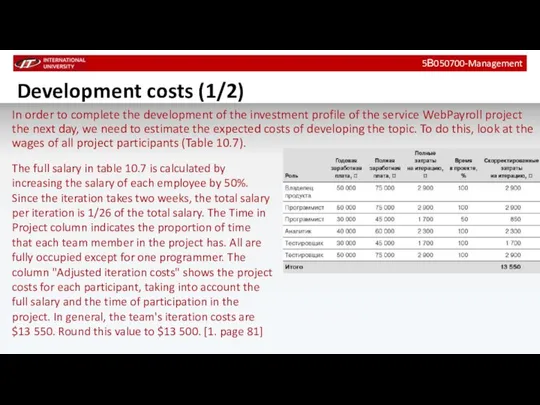

- 13. Development costs (1/2) 5В050700-Management In order to complete the development of the investment profile of the

- 14. Development costs (2/2) 5В050700-Management It is often useful to know the cost per item (or one

- 15. Profit Forecast (1/1) The results of the analysis of costs, new income, income growth and operational

- 16. Sprint Burnup Chart (1/2) B044-Management Analogous to how a release burnup chart is an alternative way

- 17. Sprint Burnup Chart (2/2) B044-Management Also, if we measure story points of completed product backlog items,

- 18. Home task By the next practice: to prepare Project Forecast Calculation table to prepare Burnup chart

- 19. Books B044-Management Mike Kohn – Agile estimating and planning. Alpina Publisher, 2018 Rubin K- Essential Scrum

- 21. Скачать презентацию

Contents

5В050700-Management

Contents

5В050700-Management

Plan of the practice

As continue of the last lection we will

Plan of the practice

As continue of the last lection we will

Sources of Return (1/4)

5В050700-Management

Some projects are implemented to generate income, others

Sources of Return (1/4)

5В050700-Management

Some projects are implemented to generate income, others

Table 10.1 contains columns for different types of recoil, which may

Table 10.1 contains columns for different types of recoil, which may

Sources of Return (3/4)

5В050700-Management

Where do the numbers come from? Ideally -

Sources of Return (3/4)

5В050700-Management

Where do the numbers come from? Ideally -

Sources of Return (4/4)

5В050700-Management

Apart from the new income and income growth

Sources of Return (4/4)

5В050700-Management

Apart from the new income and income growth

New Income(1/2)

5В050700-Management

We don't have reliable data. Sales Representative Terry says that

New Income(1/2)

5В050700-Management

We don't have reliable data. Sales Representative Terry says that

New Income(2/2)

5В050700-Management

New Income(2/2)

5В050700-Management

Income growth(1/1)

5В050700-Management

Income growth refers to the additional income that we can

Income growth(1/1)

5В050700-Management

Income growth refers to the additional income that we can

Saved income(1/1)

5В050700-Management

Saved income is something that we will not lose due

Saved income(1/1)

5В050700-Management

Saved income is something that we will not lose due

Operational efficiency(1/1)

5В050700-Management

For the next day's maintenance project to be successful, we

Operational efficiency(1/1)

5В050700-Management

For the next day's maintenance project to be successful, we

Development costs (1/2)

5В050700-Management

In order to complete the development of the investment

Development costs (1/2)

5В050700-Management

In order to complete the development of the investment

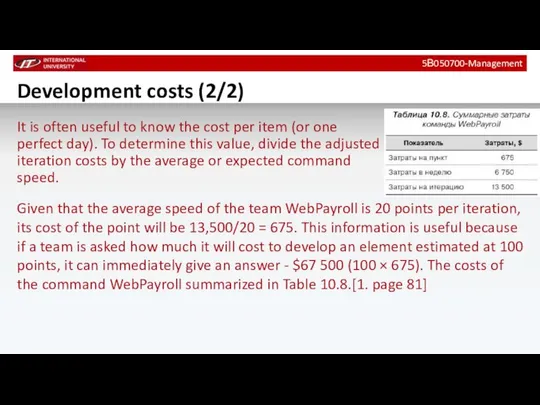

Development costs (2/2)

5В050700-Management

It is often useful to know the cost per

Development costs (2/2)

5В050700-Management

It is often useful to know the cost per

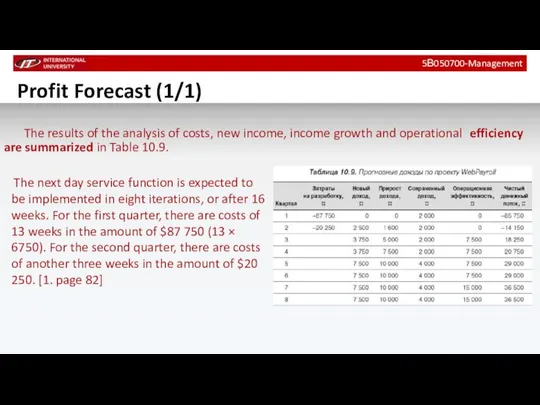

Profit Forecast (1/1)

The results of the analysis of costs, new

Profit Forecast (1/1)

The results of the analysis of costs, new

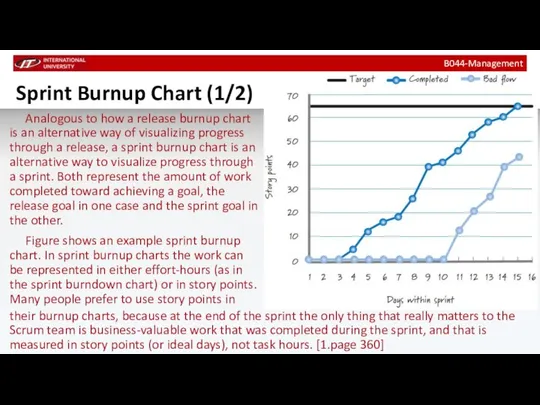

Sprint Burnup Chart (1/2)

B044-Management

Analogous to how a release burnup chart is

Sprint Burnup Chart (1/2)

B044-Management

Analogous to how a release burnup chart is

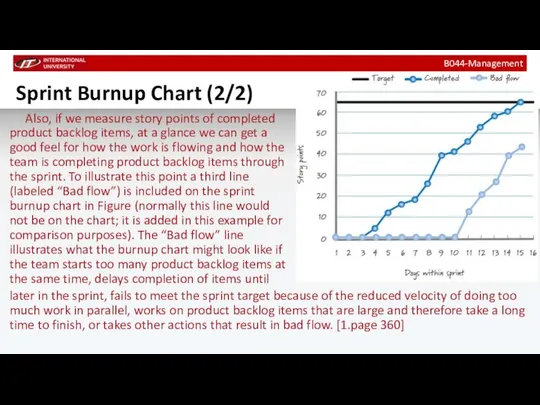

Sprint Burnup Chart (2/2)

B044-Management

Also, if we measure story points of completed

Sprint Burnup Chart (2/2)

B044-Management

Also, if we measure story points of completed

Home task

By the next practice:

to prepare Project Forecast Calculation table

to

Home task

By the next practice:

to prepare Project Forecast Calculation table

to

Books

B044-Management

Mike Kohn – Agile estimating and planning. Alpina Publisher, 2018

Rubin K-

Books

B044-Management

Mike Kohn – Agile estimating and planning. Alpina Publisher, 2018

Rubin K-

Презентация Ответственность за нарушение законодательства о недрах

Презентация Ответственность за нарушение законодательства о недрах Занятость населения

Занятость населения Международная торговля услугами

Международная торговля услугами Федеральные округа Российской Федерации

Федеральные округа Российской Федерации Теоретические основы экономики труда

Теоретические основы экономики труда Хозяйство Европейского Юга

Хозяйство Европейского Юга Милтон Фридман (1912-2006)

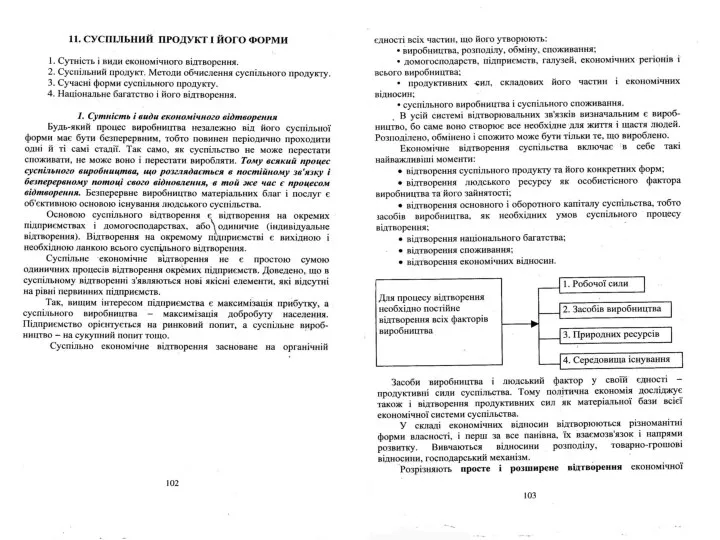

Милтон Фридман (1912-2006) Суспільний продукт і його форми

Суспільний продукт і його форми Региональная экономика

Региональная экономика Венчурный бизнес и его роль в современной экономике. Инновации и венчурный бизнес

Венчурный бизнес и его роль в современной экономике. Инновации и венчурный бизнес Статистика научно-технического прогресса

Статистика научно-технического прогресса Условия и механизм применения антидемпинговых пошлин Выполнили студентки группы Ю 101 Дамаева Кристина, Мукебенова Людмила _

Условия и механизм применения антидемпинговых пошлин Выполнили студентки группы Ю 101 Дамаева Кристина, Мукебенова Людмила _ Модель оптового рынка электроэнергии и мощности (ОРЭМ)

Модель оптового рынка электроэнергии и мощности (ОРЭМ) Управление природопользованием и его инструменты

Управление природопользованием и его инструменты Новая экономическая политика (НЭП)

Новая экономическая политика (НЭП) Предметные области и особенности основных направлений институциональной экономики

Предметные области и особенности основных направлений институциональной экономики О практике оценки эффективности деятельности ТК в Российской Федерации

О практике оценки эффективности деятельности ТК в Российской Федерации Колледж ОмГТУ. Экономика и бухгалтерский учёт

Колледж ОмГТУ. Экономика и бухгалтерский учёт Контроллинг как интегративная функция и инструментальная среда управления. Специфика контроллинга в таможенных органах

Контроллинг как интегративная функция и инструментальная среда управления. Специфика контроллинга в таможенных органах закон спроса и предложения

закон спроса и предложения Экономический рост России и его проблемы

Экономический рост России и его проблемы Механизм рынка труда: спрос и предложение, равновесие на рынке труда

Механизм рынка труда: спрос и предложение, равновесие на рынке труда Что такое предпринимательство

Что такое предпринимательство Базовые категории институционализма. Тема 6

Базовые категории институционализма. Тема 6 Бухгалтерские издержки. Экономические издержки

Бухгалтерские издержки. Экономические издержки Неоклассическая теория: общая характеристика

Неоклассическая теория: общая характеристика Деловой туризм

Деловой туризм Рыночные отношения в экономике

Рыночные отношения в экономике