- Modeling and forecasting. Volatility

Содержание

- 2. Outline Introduction: Why ARCH? ARCH Models Extensions: GARCH, T-GARCH, Q-GARCH, GARCH-M, Box-Cox GARCH Estimation Multivariate GARCH

- 3. 1. Introduction: Why ARCH?

- 4. Why ARCH? ARMA and VAR models are based on the conditional mean of the distribution where

- 5. Some example series: UST10Y

- 6. Dow Jones Symmetric Shocks? Homoskedastic?

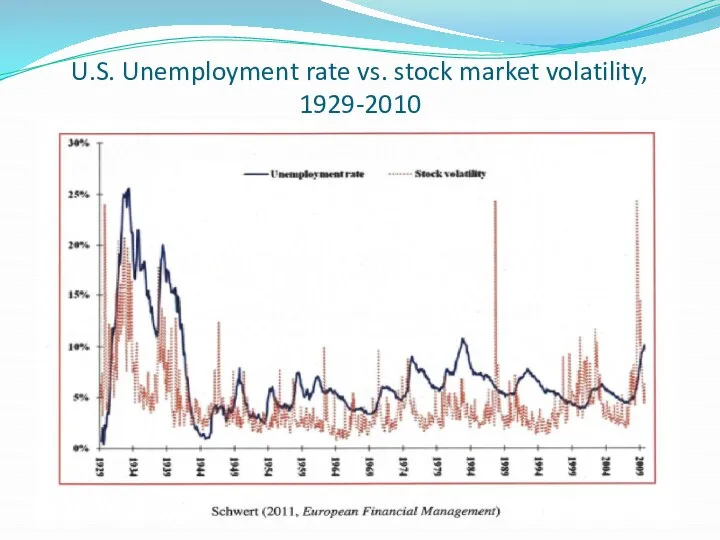

- 7. U.S. Unemployment rate vs. stock market volatility, 1929-2010

- 8. U.S. Realized Volatility (kernel based) 1997-2009

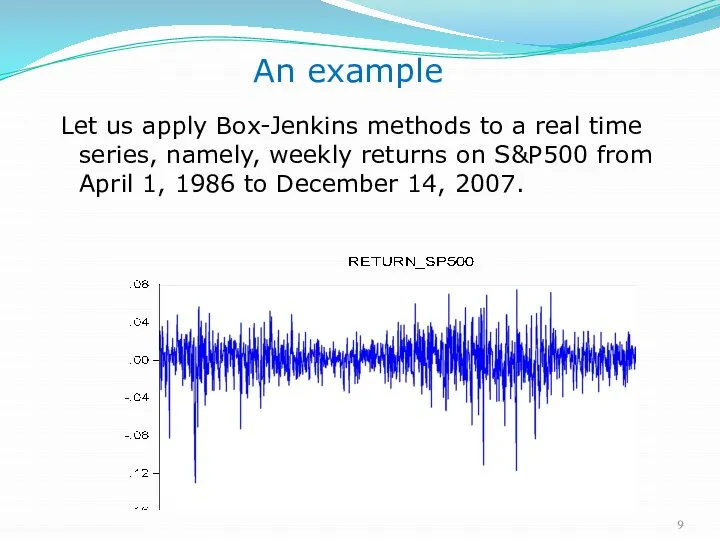

- 9. An example Let us apply Box-Jenkins methods to a real time series, namely, weekly returns on

- 10. Example (cont.) Note: Tranquil period Volatile period

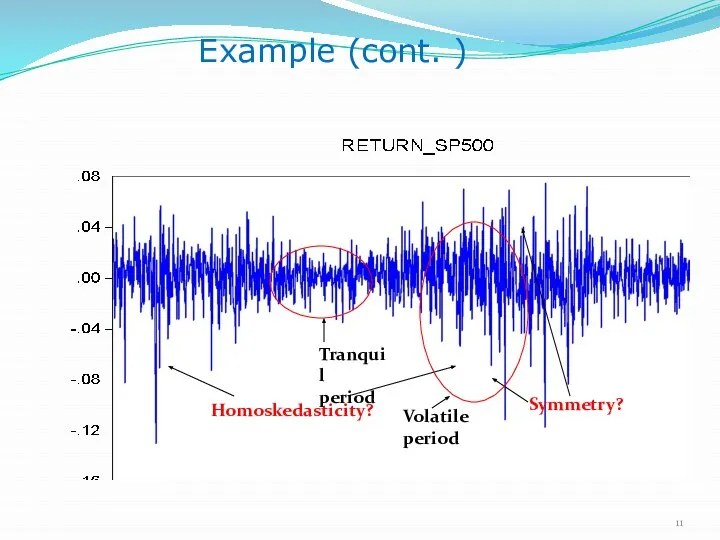

- 11. Example (cont. ) Homoskedasticity? Symmetry? Tranquil period Volatile period

- 12. Example (cont.) Both ACF and PACF are flat, suggesting p=0 and q=0 if we stay in

- 13. Example (cont. ) Look at the histogram and some summary statistics of the data: Asymmetry Fat

- 14. Skewness The shape of a uni-modal distribution can be symmetric or skewed to one side. If

- 15. Kurtosis Kurtosis measures the height and sharpness of the peak relative to the rest of the

- 16. Remarks Gaussian ARMA models are not able to generate asymmetric or fat-tailed behavior. The previous time

- 17. Example Variance of financial returns is often referred to as volatility. To understand the dynamics of

- 18. EViews Example – Daily S&P 500 Returns

- 19. When we learn about GARCH(1,1)…

- 20. We’ll be able to make squared residuals white noise

- 21. Quality of TGARCH predictions: 1% quantiles, VaR(0.01), from August 1, 2007

- 22. 2. ARCH Models

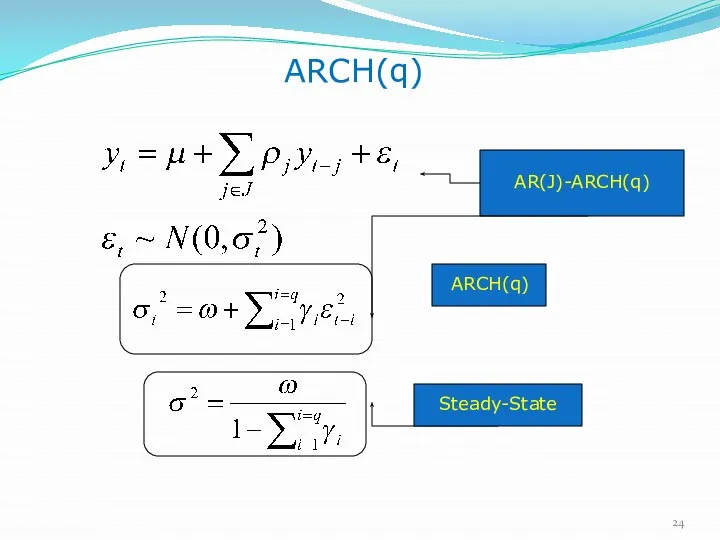

- 24. ARCH(q) AR(J)-ARCH(q) AR(J)-ARCH(q) ARCH(q) Steady-State

- 25. A special case: ARCH(1) Properties [It-1 = y1,..,yt-1] with the AR coefficient γ1 If , the

- 26. Testing for the ARCH effects Regress on . Calculate , which is an LM statistic. Under

- 27. 3. Extensions

- 28. GARCH(p,q) AR(J)-ARCH(q) AR(J)-GARCH(p,q) GARCH(p,q) Steady-State Additivity No negativity

- 29. GARCH(1,1) The most popular ARCH-type model Volatility ( ) VaR=1.645σ

- 30. Properties of GARCH(1,1) 1. follows an ARMA(1,1) with the AR coefficient , and the MA coefficient

- 31. I-GARCH If the coefficients of the GARCH model sum to 1, then the model has “integrated”

- 32. The speed of decrease in the IRFs is determined by Impulse response functions (IRFs) of GARCH(1,1)

- 33. NIC: as a function of holding other variables constant. The NIC of GARCH(1,1): It is symmetric.

- 34. Student t -- GARCH(1,1) where Compared to the Gaussian GARCH, the Student t-GARCH can generate fatter

- 35. T-GARCH (Asymmetry) NIC is asymmetric. If , bad news has a larger impact on the future

- 36. IRFs T-GARCH (Asymmetry)

- 37. NIC is asymmetric as long as Asymmetric Volatility Q(uadratic)-GARCH (Asymmetry)

- 38. NIC of Quadratic GARCH vs. Symmetric GARCH

- 39. GARCH-M An important application of the ARCH-type models is in modeling the trade-off between the mean

- 40. Box-Cox GARCH(1,1) We model the power transformation of volatility. As long as , NIC is asymmetric

- 41. Summary: NICs of Alternative ARCHs Inflation Volatility

- 42. Summing up (see Appendix for an expanded list) Asymmetric Models Non linear

- 43. 3. Estimation

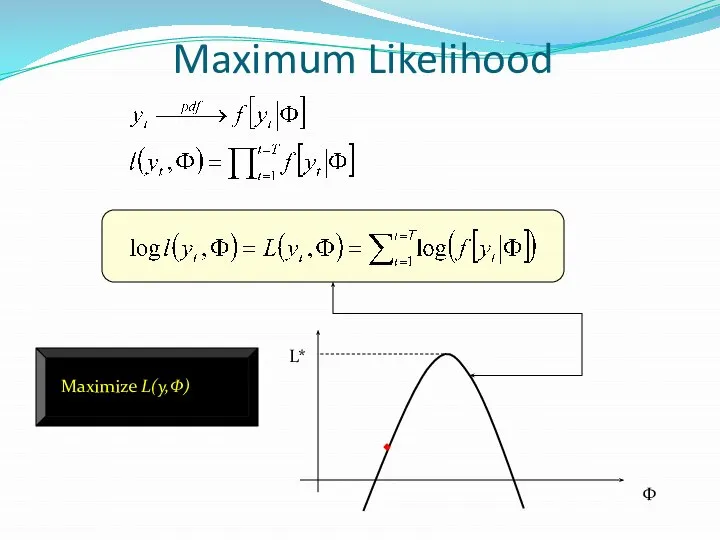

- 44. Maximum Likelihood Maximize L(y,Φ) Φ L*

- 45. Maximum Likelihood (continued) The maximum likelihood decomposes in a “mean” and a “variance” component. Estimation has

- 46. Optimization Newton’s Method Stochastic Newton Method Gradient and Hill Climbing Techniques

- 47. Multiple Solutions Monte Carlo Genetic Algorithms

- 48. 4. Multivariate models

- 49. Multivariate GARCH Models A natural extension of the time-varying variance models based on the univariate GARCH

- 50. Vech Model (2 variables) The conditional variance of each variable depends on its own lagged value,

- 51. BEKK Model C is a NxN lower triangular matrix of unknown parameters A and B are

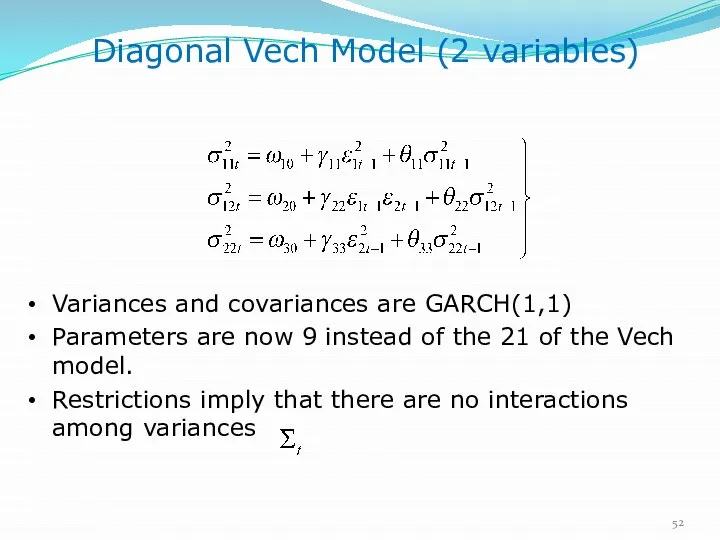

- 52. Diagonal Vech Model (2 variables) Variances and covariances are GARCH(1,1) Parameters are now 9 instead of

- 53. CCC (Constant Conditional Correlation) Model 3 variables The correlation coefficients are all time invariant

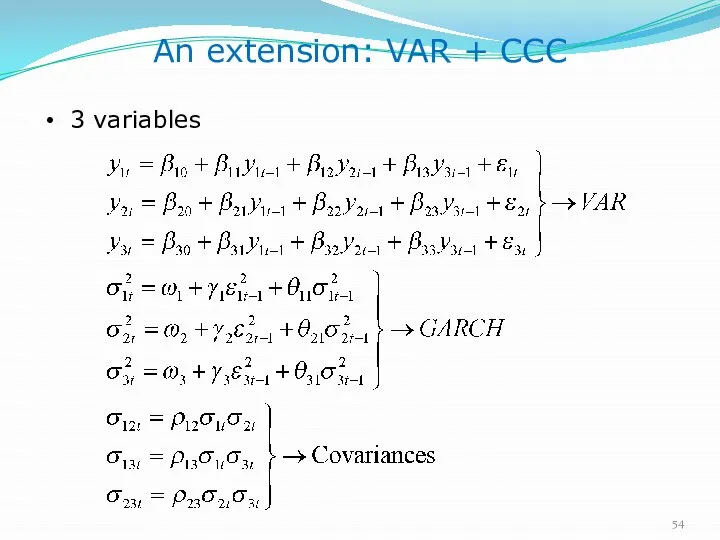

- 54. An extension: VAR + CCC 3 variables

- 55. A further extension: VAR + CCC+ GARCH-M Interactions between Markets Contagion

- 56. An example of volatility “contagion’’

- 57. 5. Application: Value-at-Risk (VaR)

- 58. VaR What is the most I can lose on an investment? VaR tries to provide an

- 59. Value-at-Risk (VaR) VaR summarizes the expected maximum loss over a time horizon within a given confidence

- 60. Value-at-Risk (VaR) - Continued The simplest assumption: daily gains/losses are normally distributed and independent. Calculate VaR

- 61. Measuring VaR with historical data 0 20 40 60 80 100 120 140 160 180 -15

- 62. Assuming a Normal distribution Mean Return (μ) Standard Deviation (σ) Assume that asset returns are normally

- 63. VaR with Normally Distributed Returns The probability of the return falling below a certain threshold depends

- 64. Portfolio VaR When we have more than one asset in our portfolio we can exploit the

- 65. An Example Let us consider the following investment US$200 million invested in 5-year zero coupon US

- 66. An Example (cont.) Suppose we want to compute the 95% VaR. The critical threshold is 1.65

- 67. An Example of Portfolio VaR Two securities 30-year zero-coupon U.S. Treasury bond 5-year zero-coupon U.S. Treasury

- 68. An Example of Portfolio VaR 95% confidence level 30 year zero VaR 1.65 * 0.01409 *

- 69. VaR of the Portfolio Suppose the correlation between the two bonds is ρ12=0.88 Remember that Portfolio

- 70. The problem with Normality: Kurtosis Extreme asset price changes occur more often than the normal distribution

- 71. Fat Tails and underestimation of VaR If we assume that returns are normally distributed when they

- 72. Backtesting Model backtesting involves systematic comparisons of the calculated VaRs with the subsequent realized profits and

- 73. Relevance: Basel VaR Guidelines VaR computed daily, holding period is 10 days. The confidence interval is

- 74. Summing up A host of research has examined a. how best to compute VaR with assumptions

- 75. Thank you!

- 76. Appendix – GARCH univariate families

- 77. Source: Bollerslev 2010, Engle Festschrift

- 79. APPENDIX II – Software

- 81. Скачать презентацию

Outline

Introduction: Why ARCH?

ARCH Models

Extensions: GARCH, T-GARCH, Q-GARCH, GARCH-M, Box-Cox GARCH

Estimation

Multivariate GARCH

Outline

Introduction: Why ARCH?

ARCH Models

Extensions: GARCH, T-GARCH, Q-GARCH, GARCH-M, Box-Cox GARCH

Estimation

Multivariate GARCH

1. Introduction:

Why ARCH?

1. Introduction:

Why ARCH?

Why ARCH?

ARMA and VAR models are based on the conditional mean

Why ARCH?

ARMA and VAR models are based on the conditional mean

Some example series: UST10Y

Some example series: UST10Y

Dow Jones

Symmetric Shocks?

Homoskedastic?

Dow Jones

Symmetric Shocks?

Homoskedastic?

U.S. Unemployment rate vs. stock market volatility, 1929-2010

U.S. Unemployment rate vs. stock market volatility, 1929-2010

U.S. Realized Volatility (kernel based)

1997-2009

U.S. Realized Volatility (kernel based)

1997-2009

An example

Let us apply Box-Jenkins methods to a real time series,

An example

Let us apply Box-Jenkins methods to a real time series,

Example (cont.)

Note:

Tranquil

period

Volatile period

Example (cont.)

Note:

Tranquil

period

Volatile period

Example (cont. )

Homoskedasticity?

Symmetry?

Tranquil

period

Volatile period

Example (cont. )

Homoskedasticity?

Symmetry?

Tranquil

period

Volatile period

Example (cont.)

Both ACF and PACF are flat, suggesting p=0 and q=0

Example (cont.)

Both ACF and PACF are flat, suggesting p=0 and q=0

Example (cont. )

Look at the histogram and some summary statistics of

Example (cont. )

Look at the histogram and some summary statistics of

Skewness

The shape of a uni-modal distribution can be symmetric or

Skewness

The shape of a uni-modal distribution can be symmetric or

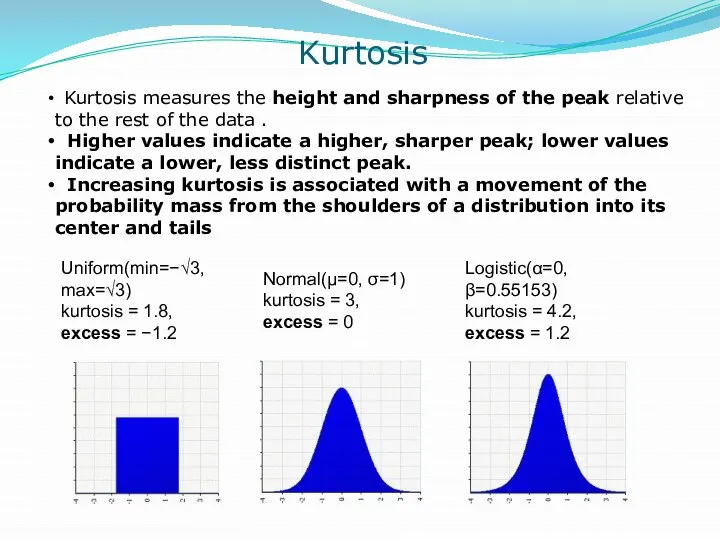

Kurtosis

Kurtosis measures the height and sharpness of the peak relative

Kurtosis

Kurtosis measures the height and sharpness of the peak relative

Remarks

Gaussian ARMA models are not able to generate asymmetric or fat-tailed

Remarks

Gaussian ARMA models are not able to generate asymmetric or fat-tailed

Example

Variance of financial returns is often referred to as volatility.

To understand

Example

Variance of financial returns is often referred to as volatility.

To understand

EViews Example – Daily S&P 500 Returns

EViews Example – Daily S&P 500 Returns

When we learn about GARCH(1,1)…

When we learn about GARCH(1,1)…

We’ll be able to make squared residuals white noise

We’ll be able to make squared residuals white noise

Quality of TGARCH predictions: 1% quantiles, VaR(0.01), from August 1, 2007

Quality of TGARCH predictions: 1% quantiles, VaR(0.01), from August 1, 2007

2. ARCH Models

2. ARCH Models

ARCH(q)

AR(J)-ARCH(q)

AR(J)-ARCH(q)

ARCH(q)

Steady-State

ARCH(q)

AR(J)-ARCH(q)

AR(J)-ARCH(q)

ARCH(q)

Steady-State

![A special case: ARCH(1) Properties [It-1 = y1,..,yt-1] with the AR](/_ipx/f_webp&q_80&fit_contain&s_1440x1080/imagesDir/jpg/1434015/slide-24.jpg)

A special case: ARCH(1)

Properties [It-1 = y1,..,yt-1]

with the AR coefficient

A special case: ARCH(1)

Properties [It-1 = y1,..,yt-1]

with the AR coefficient

Testing for the ARCH effects

Regress on .

Calculate , which is

Testing for the ARCH effects

Regress on .

Calculate , which is

3. Extensions

3. Extensions

GARCH(p,q)

AR(J)-ARCH(q)

AR(J)-GARCH(p,q)

GARCH(p,q)

Steady-State

Additivity

No negativity

GARCH(p,q)

AR(J)-ARCH(q)

AR(J)-GARCH(p,q)

GARCH(p,q)

Steady-State

Additivity

No negativity

GARCH(1,1)

The most popular ARCH-type model

Volatility ( )

VaR=1.645σ

GARCH(1,1)

The most popular ARCH-type model

Volatility ( )

VaR=1.645σ

Properties of GARCH(1,1)

1. follows an ARMA(1,1) with the AR coefficient ,

Properties of GARCH(1,1)

1. follows an ARMA(1,1) with the AR coefficient ,

I-GARCH

If the coefficients of the GARCH model sum to 1, then

I-GARCH

If the coefficients of the GARCH model sum to 1, then

The speed of decrease in the IRFs is determined by

Impulse

The speed of decrease in the IRFs is determined by

Impulse

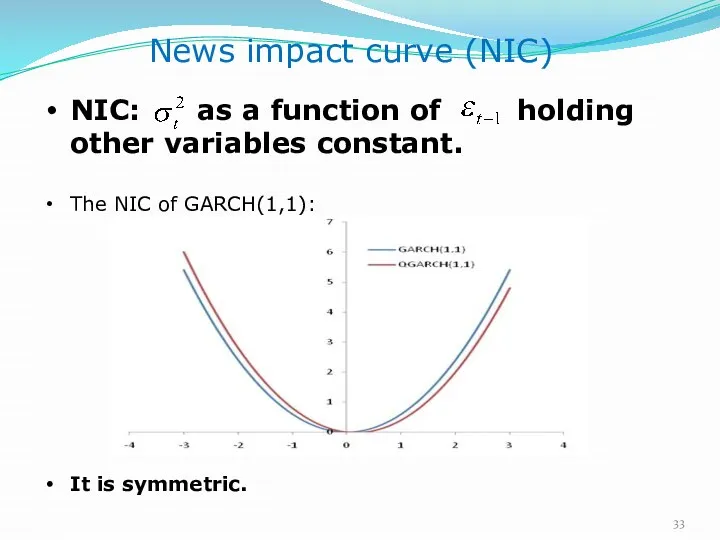

NIC: as a function of holding other variables constant.

The NIC

NIC: as a function of holding other variables constant.

The NIC

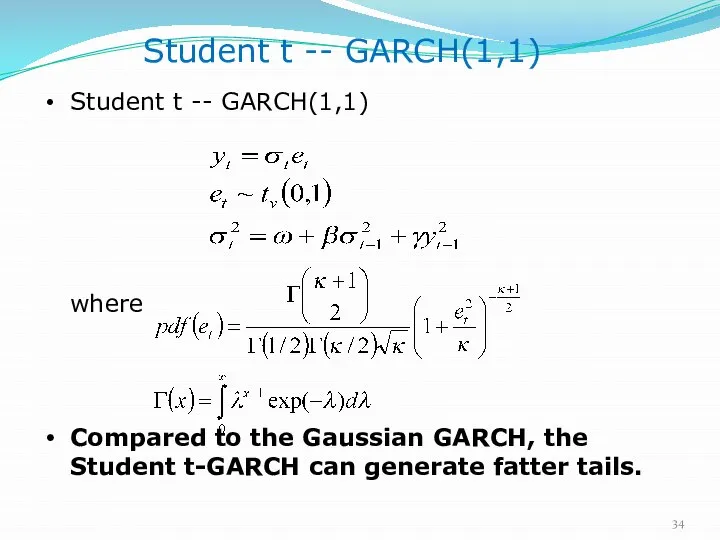

Student t -- GARCH(1,1)

where

Compared to the Gaussian GARCH, the Student t-GARCH

Student t -- GARCH(1,1)

where

Compared to the Gaussian GARCH, the Student t-GARCH

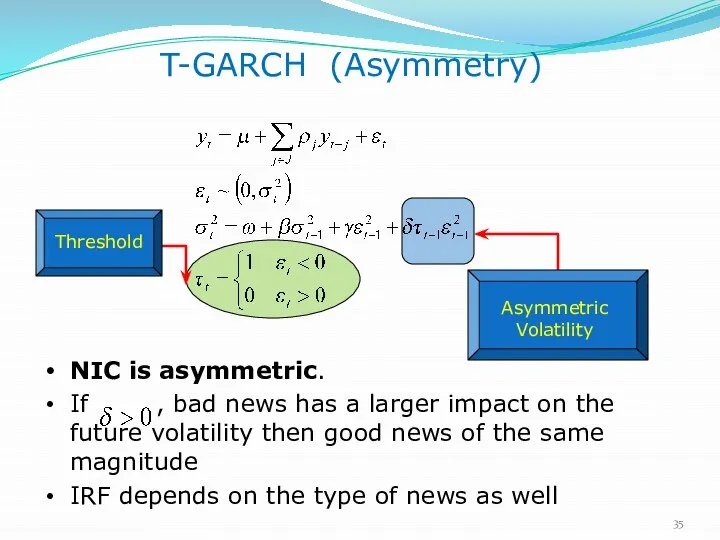

T-GARCH (Asymmetry)

NIC is asymmetric.

If , bad news has a larger

T-GARCH (Asymmetry)

NIC is asymmetric.

If , bad news has a larger

IRFs

T-GARCH (Asymmetry)

IRFs

T-GARCH (Asymmetry)

NIC is asymmetric as long as

Asymmetric Volatility

Q(uadratic)-GARCH (Asymmetry)

NIC is asymmetric as long as

Asymmetric Volatility

Q(uadratic)-GARCH (Asymmetry)

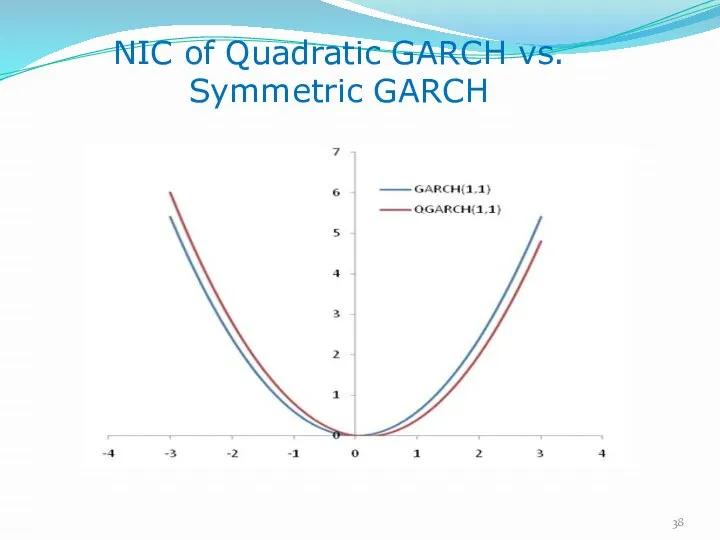

NIC of Quadratic GARCH vs.

Symmetric GARCH

NIC of Quadratic GARCH vs.

Symmetric GARCH

GARCH-M

An important application of the ARCH-type models is in modeling

GARCH-M

An important application of the ARCH-type models is in modeling

Box-Cox GARCH(1,1)

We model the power transformation of volatility.

As long

Box-Cox GARCH(1,1)

We model the power transformation of volatility.

As long

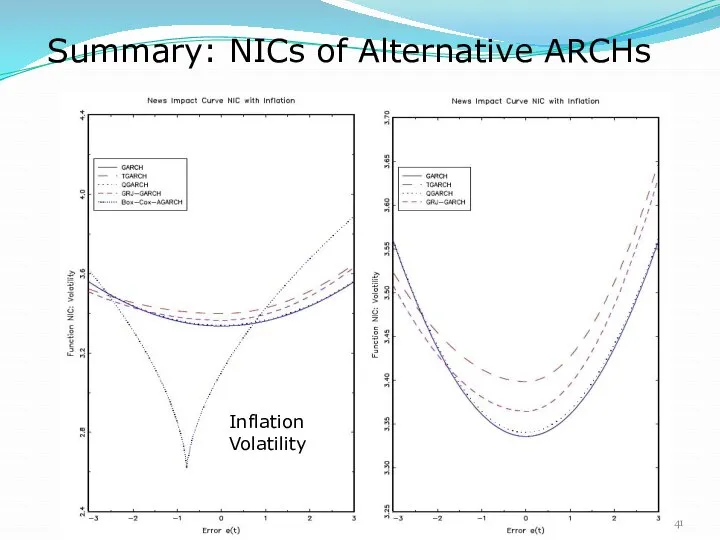

Summary: NICs of Alternative ARCHs

Inflation Volatility

Summary: NICs of Alternative ARCHs

Inflation Volatility

Summing up (see Appendix for an expanded list)

Asymmetric Models

Non linear

Summing up (see Appendix for an expanded list)

Asymmetric Models

Non linear

3. Estimation

3. Estimation

Maximum Likelihood

Maximize L(y,Φ)

Φ

L*

Maximum Likelihood

Maximize L(y,Φ)

Φ

L*

Maximum Likelihood (continued)

The maximum likelihood decomposes in a “mean” and

Maximum Likelihood (continued)

The maximum likelihood decomposes in a “mean” and

Optimization

Newton’s Method

Stochastic Newton Method

Gradient and Hill Climbing Techniques

Optimization

Newton’s Method

Stochastic Newton Method

Gradient and Hill Climbing Techniques

Multiple Solutions

Monte Carlo

Genetic Algorithms

Multiple Solutions

Monte Carlo

Genetic Algorithms

4. Multivariate models

4. Multivariate models

Multivariate GARCH Models

A natural extension of the time-varying variance models based

Multivariate GARCH Models

A natural extension of the time-varying variance models based

Vech Model (2 variables)

The conditional variance of each variable depends on

Vech Model (2 variables)

The conditional variance of each variable depends on

BEKK Model

C is a NxN lower triangular matrix of unknown parameters

BEKK Model

C is a NxN lower triangular matrix of unknown parameters

Diagonal Vech Model (2 variables)

Variances and covariances are GARCH(1,1)

Parameters are now

Diagonal Vech Model (2 variables)

Variances and covariances are GARCH(1,1)

Parameters are now

CCC

(Constant Conditional Correlation) Model

3 variables

The correlation coefficients are all time

CCC

(Constant Conditional Correlation) Model

3 variables

The correlation coefficients are all time

An extension: VAR + CCC

3 variables

An extension: VAR + CCC

3 variables

A further extension:

VAR + CCC+ GARCH-M

Interactions between Markets

Contagion

A further extension:

VAR + CCC+ GARCH-M

Interactions between Markets

Contagion

An example of volatility “contagion’’

An example of volatility “contagion’’

5. Application:

Value-at-Risk (VaR)

5. Application:

Value-at-Risk (VaR)

VaR

What is the most I can lose on an investment?

VaR

VaR

What is the most I can lose on an investment?

VaR

Value-at-Risk (VaR)

VaR summarizes the expected maximum loss over a time horizon

Value-at-Risk (VaR)

VaR summarizes the expected maximum loss over a time horizon

Value-at-Risk (VaR) - Continued

The simplest assumption: daily gains/losses are normally distributed

Value-at-Risk (VaR) - Continued

The simplest assumption: daily gains/losses are normally distributed

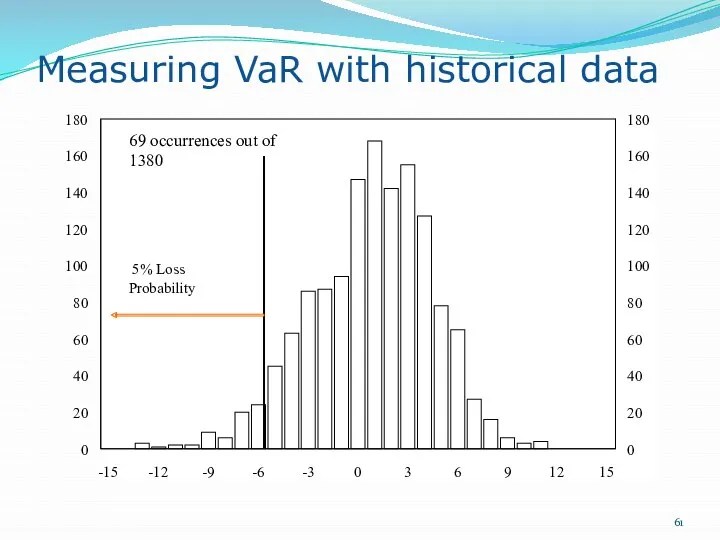

Measuring VaR with historical data

0

20

40

60

80

100

120

140

160

180

-15

-12

-9

-6

-3

0

3

6

9

12

15

0

20

40

60

80

100

120

140

160

180

Probability

Measuring VaR with historical data

0

20

40

60

80

100

120

140

160

180

-15

-12

-9

-6

-3

0

3

6

9

12

15

0

20

40

60

80

100

120

140

160

180

Probability

Assuming a Normal distribution

Mean Return (μ)

Standard Deviation (σ)

Assume that asset returns

Assuming a Normal distribution

Mean Return (μ)

Standard Deviation (σ)

Assume that asset returns

VaR with Normally

Distributed Returns

The probability of the return falling below

VaR with Normally

Distributed Returns

The probability of the return falling below

Portfolio VaR

When we have more than one asset in our portfolio

Portfolio VaR

When we have more than one asset in our portfolio

An Example

Let us consider the following investment

US$200 million invested in 5-year

An Example

Let us consider the following investment

US$200 million invested in 5-year

An Example (cont.)

Suppose we want to compute the 95% VaR.

The

An Example (cont.)

Suppose we want to compute the 95% VaR.

The

An Example of Portfolio VaR

Two securities

30-year zero-coupon U.S. Treasury bond

5-year zero-coupon

An Example of Portfolio VaR

Two securities

30-year zero-coupon U.S. Treasury bond

5-year zero-coupon

An Example of Portfolio VaR

95% confidence level

30 year zero VaR

1.65

An Example of Portfolio VaR

95% confidence level

30 year zero VaR

1.65

VaR of the Portfolio

Suppose the correlation between the two bonds is

VaR of the Portfolio

Suppose the correlation between the two bonds is

The problem with Normality: Kurtosis

Extreme asset price changes occur more often

The problem with Normality: Kurtosis

Extreme asset price changes occur more often

Fat Tails and underestimation of VaR

If we assume that returns are

Fat Tails and underestimation of VaR

If we assume that returns are

Backtesting

Model backtesting involves systematic comparisons of the calculated VaRs with the

Backtesting

Model backtesting involves systematic comparisons of the calculated VaRs with the

Relevance: Basel VaR Guidelines

VaR computed daily, holding period is 10 days.

The

Relevance: Basel VaR Guidelines

VaR computed daily, holding period is 10 days.

The

Summing up

A host of research has examined

a. how best to

Summing up

A host of research has examined

a. how best to

Thank you!

Thank you!

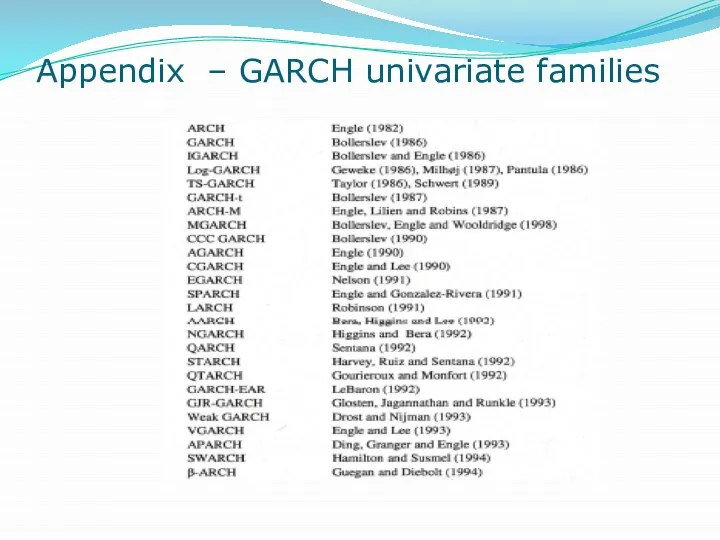

Appendix – GARCH univariate families

Appendix – GARCH univariate families

Source: Bollerslev 2010, Engle Festschrift

Source: Bollerslev 2010, Engle Festschrift

APPENDIX II – Software

APPENDIX II – Software

Современное состояние и перспективы развития инновационной составляющей экономики Украины

Современное состояние и перспективы развития инновационной составляющей экономики Украины Предпочтения и выбор

Предпочтения и выбор Борьба с безработицей

Борьба с безработицей Концептуальные основы регионального развития в России

Концептуальные основы регионального развития в России Приоритетные направления инновационного развития

Приоритетные направления инновационного развития Роль государства в рыночной экономике

Роль государства в рыночной экономике Возникновение экономики и её роль в государстве

Возникновение экономики и её роль в государстве Типы рыночных структур

Типы рыночных структур Глобализация, её проявления и последствия

Глобализация, её проявления и последствия Рынок. Модели. Спрос. Предложение. Равновесие

Рынок. Модели. Спрос. Предложение. Равновесие Товарная политика. Лекция 3

Товарная политика. Лекция 3 Модель кейнсианского креста

Модель кейнсианского креста Экономическое взаимодействие России и Китая

Экономическое взаимодействие России и Китая Проект Комфортная городская среда в Великоустюгском муниципальном районе

Проект Комфортная городская среда в Великоустюгском муниципальном районе Планирование и прогнозирование в условиях рынка

Планирование и прогнозирование в условиях рынка Методы экономического анализа

Методы экономического анализа Компанияның қаржы жағдайына жалпы баға беру

Компанияның қаржы жағдайына жалпы баға беру Обмен. Торговля. Реклама (7 класс)

Обмен. Торговля. Реклама (7 класс) Рыночные отношения в экономике

Рыночные отношения в экономике Ключевые этапы реализации стратегии по двигателестроению

Ключевые этапы реализации стратегии по двигателестроению Identification de marché. Identification des clients. Verifier auprés des clients l’attent des produits et services

Identification de marché. Identification des clients. Verifier auprés des clients l’attent des produits et services Потребности в перемещении людей и товаров,

Потребности в перемещении людей и товаров, Стратегии социального развития России в 21 веке

Стратегии социального развития России в 21 веке Рынок ресурсов

Рынок ресурсов Презентация Анализ конкурентоспособности экономики

Презентация Анализ конкурентоспособности экономики Поточні витрати торговельного підприємства. (Лекція 12)

Поточні витрати торговельного підприємства. (Лекція 12) Контрольные цифры проекта бюджета Санкт-Петербурга

Контрольные цифры проекта бюджета Санкт-Петербурга Курсовая работа по методике обучения экономике

Курсовая работа по методике обучения экономике