- Supply, Demand, and Prices

Содержание

- 2. Economics 1: Supply, Demand, and Prices meet the lecturers: semester 1 Simon Clark Supply, Demand, and

- 3. Economics 1: Supply, Demand, and Prices meet the lecturers: semester 2 Growth, Employment, Inflation, and Short-run

- 4. Economics 1: Supply, Demand, and Prices Before we start… Is Economics 1 the right course for

- 5. Economics 1: Supply, Demand, and Prices Which course? Economics 1 is for students who do an

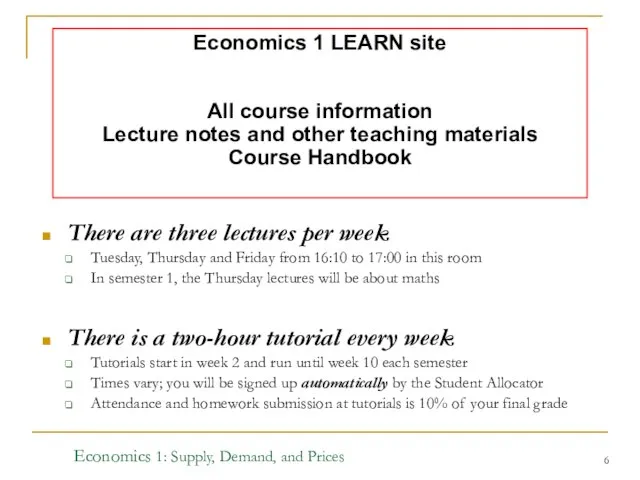

- 6. Economics 1: Supply, Demand, and Prices There are three lectures per week Tuesday, Thursday and Friday

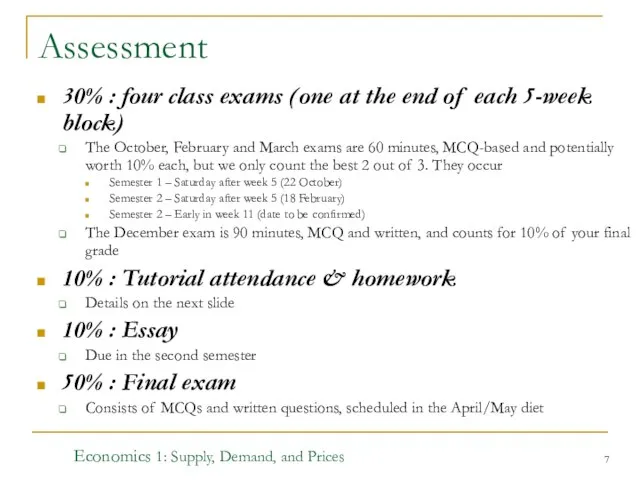

- 7. Assessment 30% : four class exams (one at the end of each 5-week block) The October,

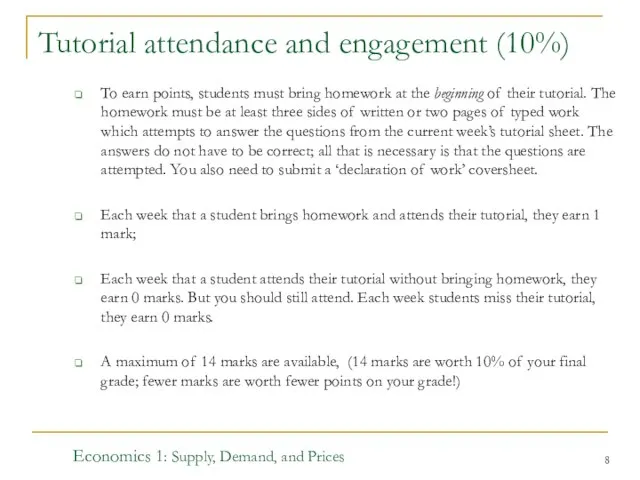

- 8. Tutorial attendance and engagement (10%) To earn points, students must bring homework at the beginning of

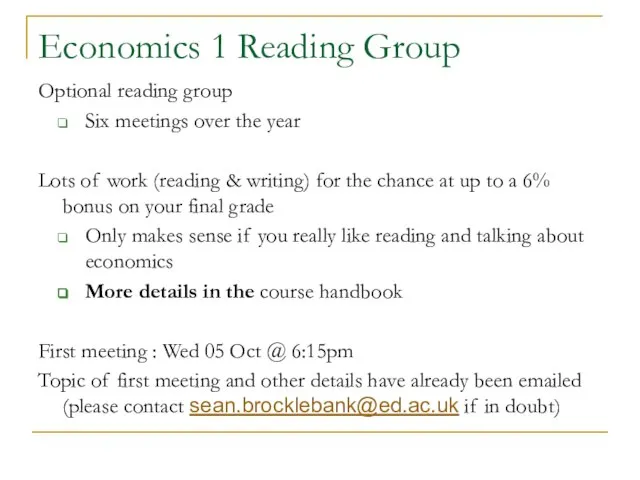

- 9. Economics 1 Reading Group Optional reading group Six meetings over the year Lots of work (reading

- 10. Economics 1: Supply, Demand, and Prices Textbooks There are two core textbooks One for micro in

- 11. Economics 1: Supply, Demand, and Prices Math textbook There is a suggested math text Most of

- 12. Economics 1: Supply, Demand, and Prices Helpdesks Twice-weekly Economics 1-only helpdesk staffed by some of the

- 13. Economics 1: Supply, Demand, and Prices maths in economics: why? Many economic magnitudes are inherently numerical

- 14. Economics 1: Supply, Demand, and Prices what maths do we use in Economics 1? basic algebra

- 15. Economics 1: Supply, Demand, and Prices Outline of weeks 1 - 5 Frank & Cartwright Thinking

- 16. Economics 1: Supply, Demand, and Prices some things to note these lectures will not be repeating

- 17. Economics 1: Supply, Demand, and Prices to illustrate the economic approach, consider some interesting problems: the

- 18. Economics 1: Supply, Demand, and Prices the market for lemons a seller has a car that

- 19. Economics 1: Supply, Demand, and Prices what if the quality of the car is private information

- 20. Economics 1: Supply, Demand, and Prices if the proportion of plums and lemons offered for sale

- 21. Economics 1: Supply, Demand, and Prices Suppose the proportion of plums and lemons offered for sale

- 22. if the proportion of plums and lemons offered for sale is ¾ and ¼ , then

- 23. Economics 1: Supply, Demand, and Prices market failure if the maximum price a buyer is willing

- 24. Economics 1: Supply, Demand, and Prices the ubiquity of (possible) adverse selection insurance markets careful/reckless drivers

- 25. Economics 1: Supply, Demand, and Prices adverse selection and liquidity banks selling bundles of debt (CDOs)

- 26. Economics 1: Supply, Demand, and Prices signalling: one way to overcome adverse selection an informative signal

- 27. Economics 1: Supply, Demand, and Prices the prisoners’ dilemma deny -10, -10 0, -25 confess -25,

- 28. Economics 1: Supply, Demand, and Prices Question : what happens? deny -10, -10 0, -25 confess

- 29. the prisoners’ dilemma: the economist’s answer deny -10, -10 0, -25 confess -25, 0 -20, -20

- 30. Economics 1: Supply, Demand, and Prices the payoffs in the prisoners dilemma have a very particular

- 31. Economics 1: Supply, Demand, and Prices the Prisoner’s dilemma is a metaphor for a wide range

- 32. Economics 1: Supply, Demand, and Prices What if the situation is repeated? Does cooperation emerge? How

- 33. Economics 1: Supply, Demand, and Prices ice cream wars 2 ice-cream sellers simultaneously choose a location

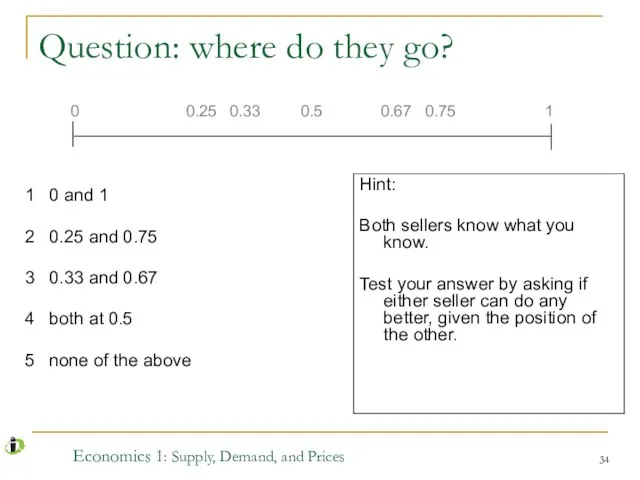

- 34. Economics 1: Supply, Demand, and Prices Question: where do they go? 1 0 and 1 2

- 35. Economics 1: Supply, Demand, and Prices where do they go? 1 0 and 1 2 0.25

- 36. Economics 1: Supply, Demand, and Prices again, this can be seen as a metaphor for many

- 37. Economics 1: Supply, Demand, and Prices some interesting extensions to consider what if there are 3

- 38. Economics 1: Supply, Demand, and Prices the demand for things without a market a common problem

- 39. Economics 1: Supply, Demand, and Prices hedonic pricing people are prepared to pay more for goods

- 40. Economics 1: Supply, Demand, and Prices using house prices a house: price reflects size, style, number

- 41. Economics 1: Supply, Demand, and Prices house prices and school quality Cheshire and Sheppard, (Economic Journal

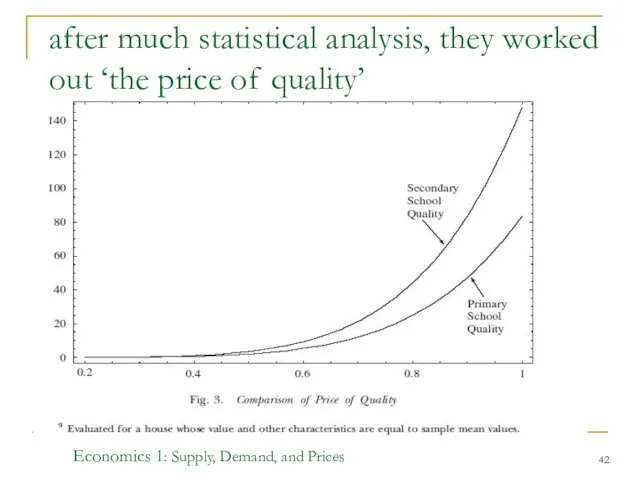

- 42. Economics 1: Supply, Demand, and Prices after much statistical analysis, they worked out ‘the price of

- 43. Economics 1: Supply, Demand, and Prices conclusions from the study For the average house the difference

- 44. Economics 1: Supply, Demand, and Prices conclusions from these problems simple numerical examples can be very

- 46. Скачать презентацию

Economics 1: Supply, Demand, and Prices

meet the lecturers: semester 1

Simon

Clark

Supply,

Demand,

and

Economics 1: Supply, Demand, and Prices

meet the lecturers: semester 1

Simon

Clark

Supply,

Demand,

and

Economics 1: Supply, Demand, and Prices

meet the lecturers: semester 2

Growth, Employment,

Economics 1: Supply, Demand, and Prices

meet the lecturers: semester 2

Growth, Employment,

Economics 1: Supply, Demand, and Prices

Before we start…

Is Economics 1

Economics 1: Supply, Demand, and Prices

Before we start…

Is Economics 1

Economics 1: Supply, Demand, and Prices

Which course?

Economics 1 is for students

Economics 1: Supply, Demand, and Prices

Which course?

Economics 1 is for students

Economics 1: Supply, Demand, and Prices

There are three lectures per week

Tuesday,

Economics 1: Supply, Demand, and Prices

There are three lectures per week

Tuesday,

Assessment

30% : four class exams (one at the end of each

Assessment

30% : four class exams (one at the end of each

Tutorial attendance and engagement (10%)

To earn points, students must bring homework

Tutorial attendance and engagement (10%)

To earn points, students must bring homework

Economics 1 Reading Group

Optional reading group

Six meetings over the year

Lots of

Economics 1 Reading Group

Optional reading group

Six meetings over the year

Lots of

Economics 1: Supply, Demand, and Prices

Textbooks

There are two core textbooks

One for

Economics 1: Supply, Demand, and Prices

Textbooks

There are two core textbooks

One for

Economics 1: Supply, Demand, and Prices

Math textbook

There is a suggested math

Economics 1: Supply, Demand, and Prices

Math textbook

There is a suggested math

Economics 1: Supply, Demand, and Prices

Helpdesks

Twice-weekly Economics 1-only helpdesk staffed by

Economics 1: Supply, Demand, and Prices

Helpdesks

Twice-weekly Economics 1-only helpdesk staffed by

Economics 1: Supply, Demand, and Prices

maths in economics: why?

Many economic magnitudes

Economics 1: Supply, Demand, and Prices

maths in economics: why?

Many economic magnitudes

Economics 1: Supply, Demand, and Prices

what maths do we use in

Economics 1: Supply, Demand, and Prices

what maths do we use in

Economics 1: Supply, Demand, and Prices

Outline of weeks 1 - 5

Economics 1: Supply, Demand, and Prices

Outline of weeks 1 - 5

Economics 1: Supply, Demand, and Prices

some things to note

these lectures will

Economics 1: Supply, Demand, and Prices

some things to note

these lectures will

Economics 1: Supply, Demand, and Prices

to illustrate the economic approach, consider

Economics 1: Supply, Demand, and Prices

to illustrate the economic approach, consider

Economics 1: Supply, Demand, and Prices

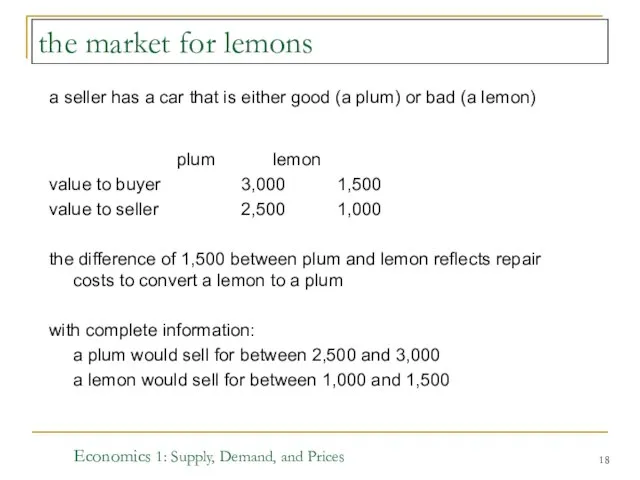

the market for lemons

a seller

Economics 1: Supply, Demand, and Prices

the market for lemons

a seller

Economics 1: Supply, Demand, and Prices

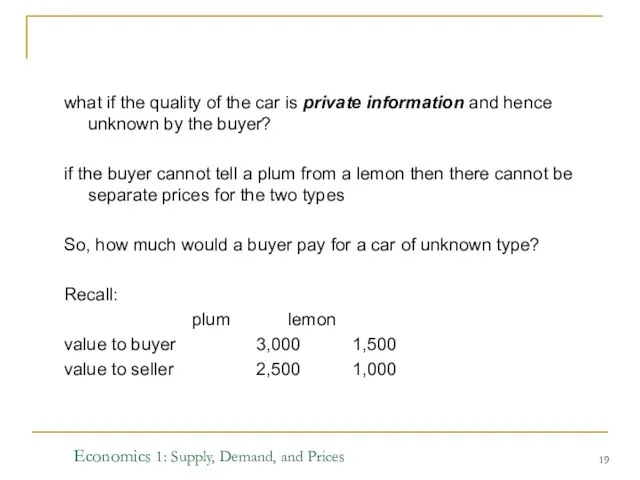

what if the quality of the

Economics 1: Supply, Demand, and Prices

what if the quality of the

Economics 1: Supply, Demand, and Prices

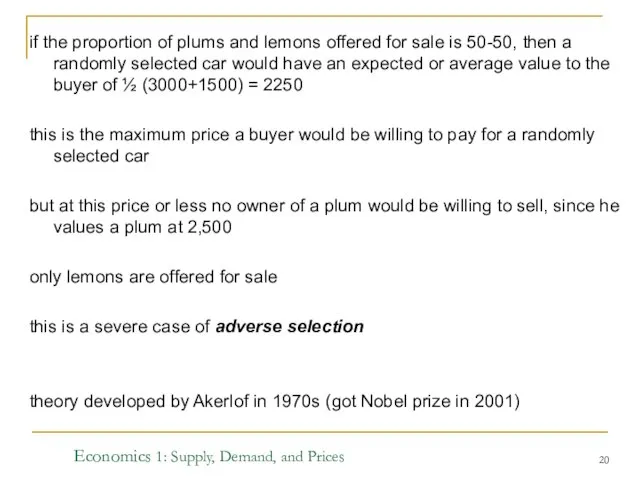

if the proportion of plums and

Economics 1: Supply, Demand, and Prices

if the proportion of plums and

Economics 1: Supply, Demand, and Prices

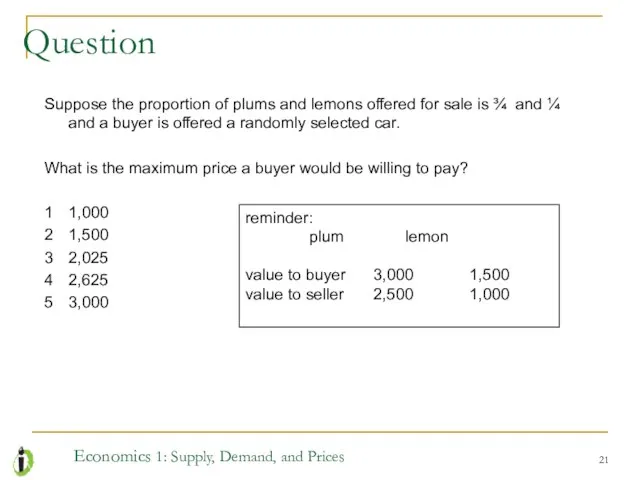

Suppose the proportion of plums and

Economics 1: Supply, Demand, and Prices

Suppose the proportion of plums and

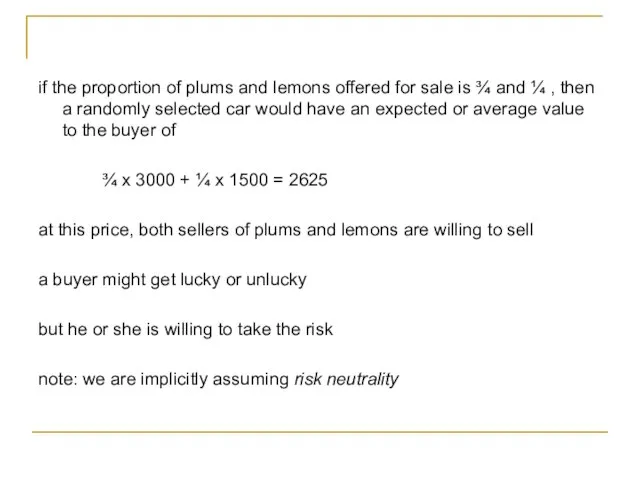

if the proportion of plums and lemons offered for sale is

if the proportion of plums and lemons offered for sale is

Economics 1: Supply, Demand, and Prices

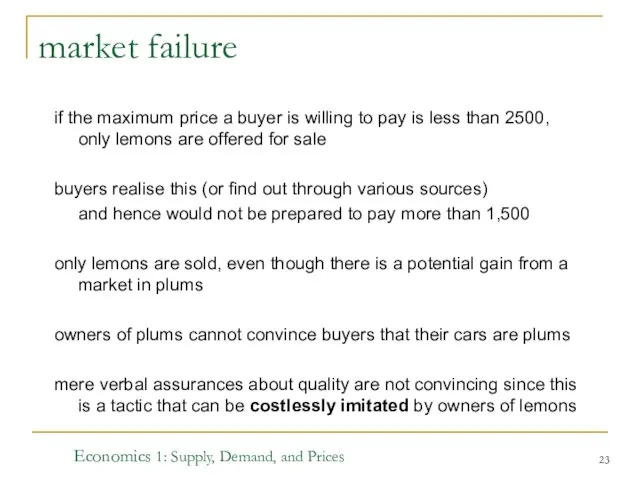

market failure

if the maximum price a

Economics 1: Supply, Demand, and Prices

market failure

if the maximum price a

Economics 1: Supply, Demand, and Prices

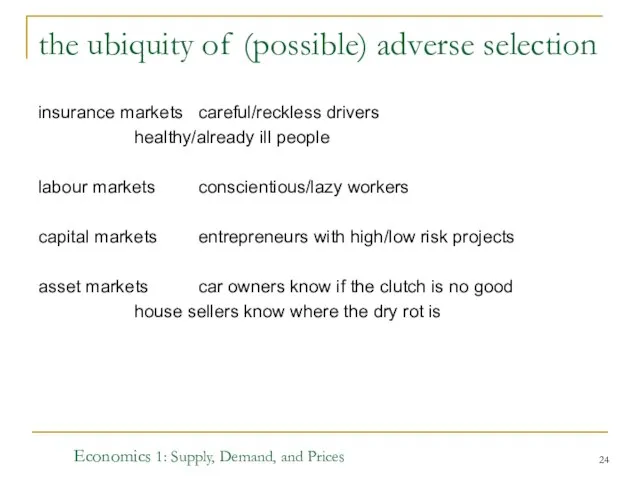

the ubiquity of (possible) adverse selection

insurance

Economics 1: Supply, Demand, and Prices

the ubiquity of (possible) adverse selection

insurance

Economics 1: Supply, Demand, and Prices

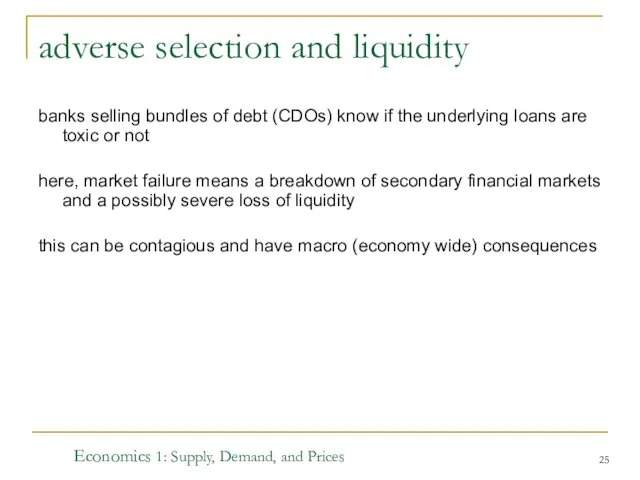

adverse selection and liquidity

banks selling bundles

Economics 1: Supply, Demand, and Prices

adverse selection and liquidity

banks selling bundles

Economics 1: Supply, Demand, and Prices

signalling: one way to overcome adverse

Economics 1: Supply, Demand, and Prices

signalling: one way to overcome adverse

Economics 1: Supply, Demand, and Prices

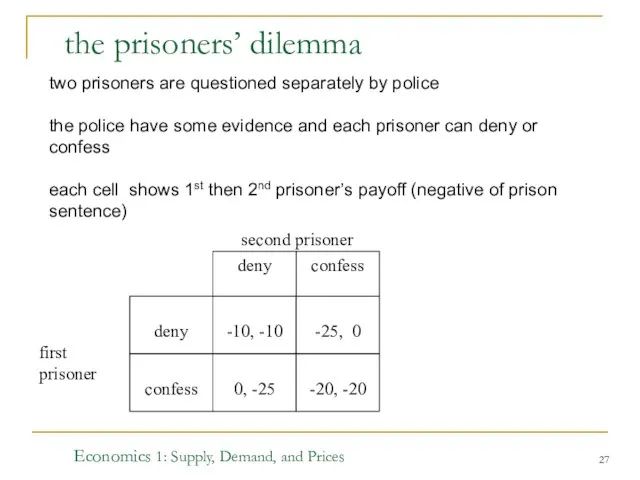

the prisoners’ dilemma

deny

-10, -10

0, -25

confess

-25, 0

-20,

Economics 1: Supply, Demand, and Prices

the prisoners’ dilemma

deny

-10, -10

0, -25

confess

-25, 0

-20,

Economics 1: Supply, Demand, and Prices

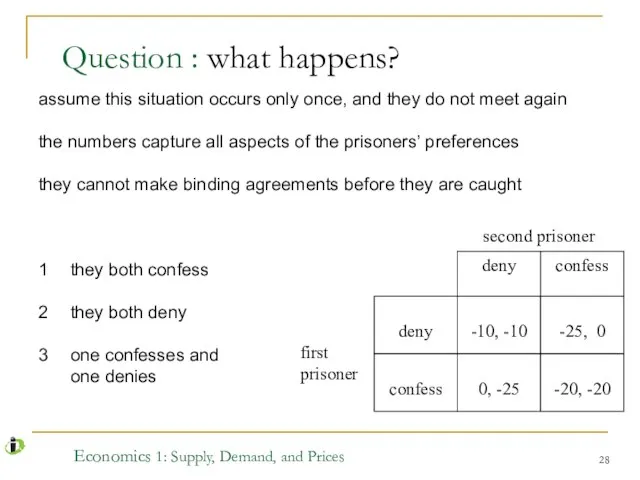

Question : what happens?

deny

-10, -10

0, -25

confess

-25,

Economics 1: Supply, Demand, and Prices

Question : what happens?

deny

-10, -10

0, -25

confess

-25,

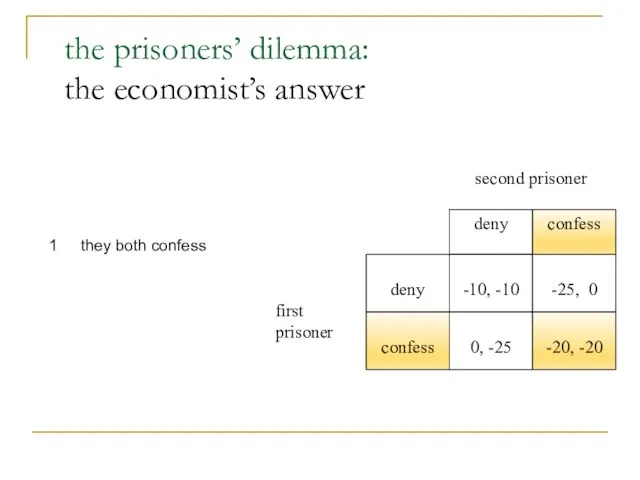

the prisoners’ dilemma:

the economist’s answer

deny

-10, -10

0, -25

confess

-25, 0

-20, -20

confess

deny

first prisoner

second prisoner

1 they

the prisoners’ dilemma:

the economist’s answer

deny

-10, -10

0, -25

confess

-25, 0

-20, -20

confess

deny

first prisoner

second prisoner

1 they

Economics 1: Supply, Demand, and Prices

the payoffs in the prisoners dilemma

Economics 1: Supply, Demand, and Prices

the payoffs in the prisoners dilemma

Economics 1: Supply, Demand, and Prices

the Prisoner’s dilemma is a metaphor

Economics 1: Supply, Demand, and Prices

the Prisoner’s dilemma is a metaphor

Economics 1: Supply, Demand, and Prices

What if the situation is repeated?

Economics 1: Supply, Demand, and Prices

What if the situation is repeated?

Economics 1: Supply, Demand, and Prices

ice cream wars

2 ice-cream sellers simultaneously

Economics 1: Supply, Demand, and Prices

ice cream wars

2 ice-cream sellers simultaneously

Economics 1: Supply, Demand, and Prices

Question: where do they go?

1 0 and

Economics 1: Supply, Demand, and Prices

Question: where do they go?

1 0 and

Economics 1: Supply, Demand, and Prices

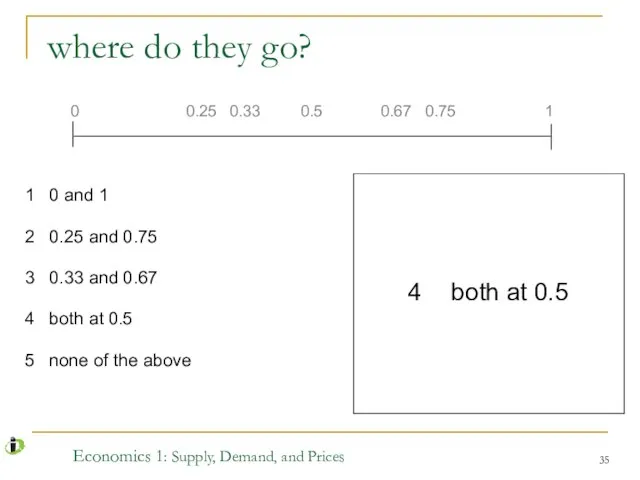

where do they go?

1 0 and

Economics 1: Supply, Demand, and Prices

where do they go?

1 0 and

Economics 1: Supply, Demand, and Prices

again, this can be seen as

Economics 1: Supply, Demand, and Prices

again, this can be seen as

Economics 1: Supply, Demand, and Prices

some interesting extensions to consider

what if

Economics 1: Supply, Demand, and Prices

some interesting extensions to consider

what if

Economics 1: Supply, Demand, and Prices

the demand for things without a

Economics 1: Supply, Demand, and Prices

the demand for things without a

Economics 1: Supply, Demand, and Prices

hedonic pricing

people are prepared to pay

Economics 1: Supply, Demand, and Prices

hedonic pricing

people are prepared to pay

Economics 1: Supply, Demand, and Prices

using house prices

a house: price reflects

size,

Economics 1: Supply, Demand, and Prices

using house prices

a house: price reflects

size,

Economics 1: Supply, Demand, and Prices

house prices and school quality

Cheshire and

Economics 1: Supply, Demand, and Prices

house prices and school quality

Cheshire and

Economics 1: Supply, Demand, and Prices

after much statistical analysis, they worked

Economics 1: Supply, Demand, and Prices

after much statistical analysis, they worked

Economics 1: Supply, Demand, and Prices

conclusions from the study

For the average

Economics 1: Supply, Demand, and Prices

conclusions from the study

For the average

Economics 1: Supply, Demand, and Prices

conclusions from these problems

simple numerical examples

Economics 1: Supply, Demand, and Prices

conclusions from these problems

simple numerical examples

Бережливое предприятие. Чем является Бережливое предприятие

Бережливое предприятие. Чем является Бережливое предприятие Три модели экономики. 9 класс

Три модели экономики. 9 класс Презентация Экспортоориентированный сектор экономики с позиций обеспечения экономической безопасности

Презентация Экспортоориентированный сектор экономики с позиций обеспечения экономической безопасности  Рыночные отношения в экономике

Рыночные отношения в экономике Глобализация и глобальные вызовы человеческой цивилизации, мировая политика

Глобализация и глобальные вызовы человеческой цивилизации, мировая политика История экономических учений. Этапы становления экономической науки

История экономических учений. Этапы становления экономической науки Міжнародна конкурентоспроможність підприємства

Міжнародна конкурентоспроможність підприємства Analiza PEST

Analiza PEST Рынок и рыночный механизм

Рынок и рыночный механизм Производство экономических благ. Издержки производства. (Тема 4)

Производство экономических благ. Издержки производства. (Тема 4) «Великая трансформация» Карла Поланьи: прошлое, настоящее, будущее

«Великая трансформация» Карла Поланьи: прошлое, настоящее, будущее Общественное производство. Блага и их классификация

Общественное производство. Блага и их классификация Барьеры входа на отраслевые рынки. (Лекция 3)

Барьеры входа на отраслевые рынки. (Лекция 3) Акция Поезд будущего: вклад представителей разных национальностей в социально-экономическое развитие и культурное наследие Дона

Акция Поезд будущего: вклад представителей разных национальностей в социально-экономическое развитие и культурное наследие Дона Управление повышением производительности труда

Управление повышением производительности труда Предмет и метод экономической теории. Понятие общественного производства

Предмет и метод экономической теории. Понятие общественного производства Соглашение о единых правилах определения страны происхождения товаров

Соглашение о единых правилах определения страны происхождения товаров Решение задач

Решение задач Экономическая социология

Экономическая социология Экономические идеи монетаризма

Экономические идеи монетаризма Префектура Канагава

Префектура Канагава Анализ безубыточности предприятия

Анализ безубыточности предприятия Профессия экономиста и как открыть свое дело. (Раздел 6)

Профессия экономиста и как открыть свое дело. (Раздел 6) Анализ и оценка инновационного развития Республики Башкортостан

Анализ и оценка инновационного развития Республики Башкортостан Механизм образования и развития кластера хозяйствующих субъектов за счет hi-tech маркетинга

Механизм образования и развития кластера хозяйствующих субъектов за счет hi-tech маркетинга Матрицы. Матричные модели в экономике,

Матрицы. Матричные модели в экономике, Фирмы в экономике

Фирмы в экономике История экономической мысли. Феномен Карла Маркса. (Лекция 3)

История экономической мысли. Феномен Карла Маркса. (Лекция 3)