- Options

Содержание

- 2. 22.1 Options Many corporate securities are similar to the stock options that are traded on organized

- 3. 22.1 Options Contracts: Preliminaries An option gives the holder the right, but not the obligation, to

- 4. 22.1 Options Contracts: Preliminaries Exercising the Option The act of buying or selling the underlying asset

- 5. Options Contracts: Preliminaries In-the-Money The exercise price is less than the spot price of the underlying

- 6. Options Contracts: Preliminaries Intrinsic Value The difference between the exercise price of the option and the

- 7. 22.2 Call Options Call options gives the holder the right, but not the obligation, to buy

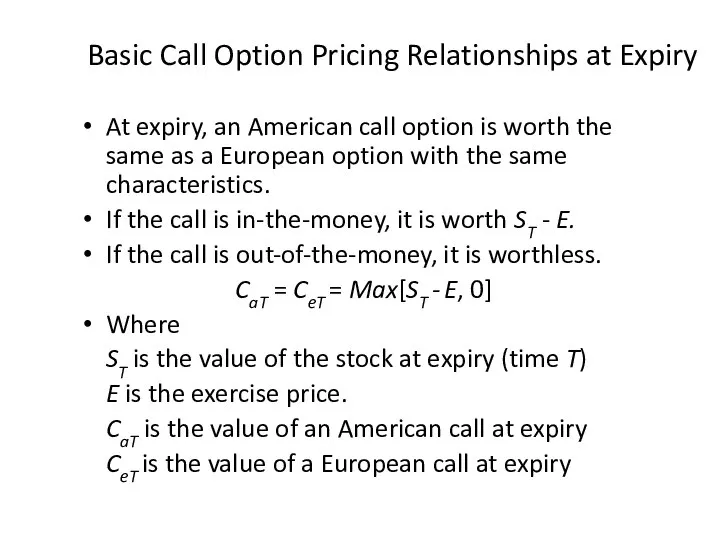

- 8. Basic Call Option Pricing Relationships at Expiry At expiry, an American call option is worth the

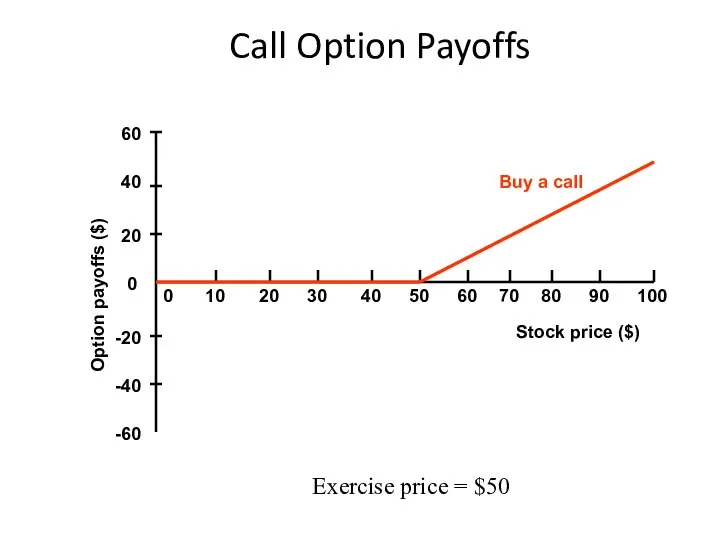

- 9. Call Option Payoffs -20 100 90 80 70 60 0 10 20 30 40 50 -40

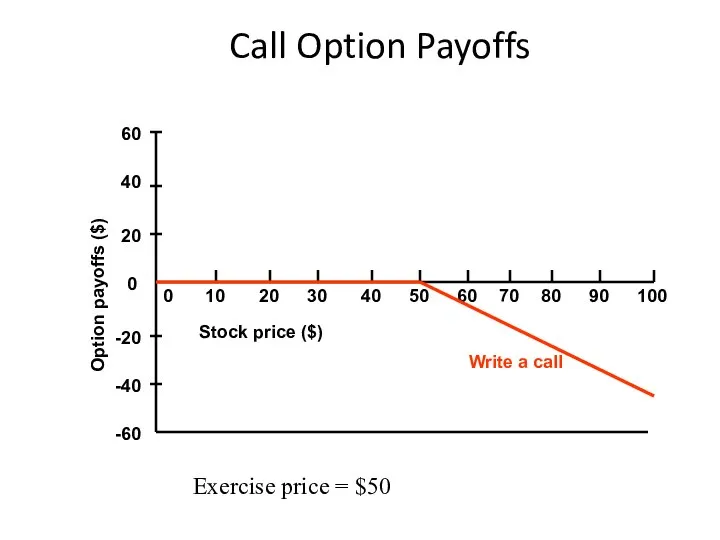

- 10. Call Option Payoffs Write a call Exercise price = $50

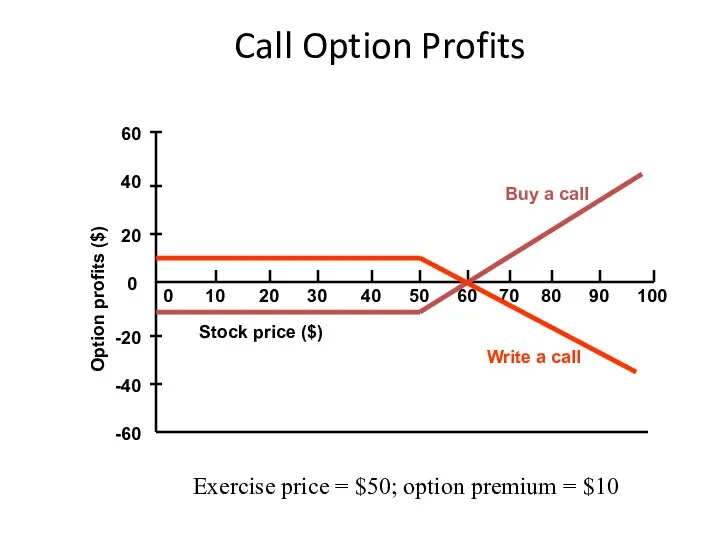

- 11. Call Option Profits Write a call Buy a call Exercise price = $50; option premium =

- 12. 22.3 Put Options Put options give the holder the right, but not the obligation, to sell

- 13. Basic Put Option Pricing Relationships at Expiry At expiry, an American put option is worth the

- 14. Put Option Payoffs -20 100 90 80 70 60 0 10 20 30 40 50 -40

- 15. Put Option Payoffs -20 100 90 80 70 60 0 10 20 30 40 50 -40

- 16. Put Option Profits -20 100 90 80 70 60 0 10 20 30 40 50 -40

- 17. 22.4 Selling Options The seller (or writer) of an option has an obligation. The purchaser of

- 18. 22.5 Stock Option Quotations

- 19. 22.5 Stock Option Quotations This option has a strike price of $8; A recent price for

- 20. 22.5 Stock Option Quotations This makes a call option with this exercise price in-the-money by $1.35

- 21. 22.5 Stock Option Quotations On this day, 15 call options with this exercise price were traded.

- 22. 22.5 Stock Option Quotations The holder of this CALL option can sell it for $1.95. Since

- 23. 22.5 Stock Option Quotations Buying this CALL option costs $2.10. Since the option is on 100

- 24. 22.5 Stock Option Quotations On this day, there were 660 call options with this exercise outstanding

- 25. 22.6 Combinations of Options Puts and calls can serve as the building blocks for more complex

- 26. Protective Put Strategy: Buy a Put and Buy the Underlying Stock: Payoffs at Expiry Buy a

- 27. Protective Put Strategy Profits Buy a put with exercise price of $50 for $10 Buy the

- 28. Covered Call Strategy Sell a call with exercise price of $50 for $10 Buy the stock

- 29. Long Straddle: Buy a Call and a Put Buy a put with an exercise price of

- 30. Short Straddle: Sell a Call and a Put Sell a put with exercise price of $50

- 31. Long Call Spread Sell a call with exercise price of $55 for $5 $55 long call

- 32. Put-Call Parity Sell a put with an exercise price of $40 Buy the stock at $40

- 33. 22.7 Valuing Options The last section concerned itself with the value of an option at expiry.

- 34. Option Value Determinants Call Put Stock price + – Exercise price – + Interest rate +

- 35. Market Value, Time Value, and Intrinsic Value for an American Call CaT > Max[ST - E,

- 36. 22.8 An Option‑Pricing Formula We will start with a binomial option pricing formula to build our

- 37. Binomial Option Pricing Model Suppose a stock is worth $25 today and in one period will

- 38. Binomial Option Pricing Model A call option on this stock with exercise price of $25 will

- 39. Binomial Option Pricing Model Borrow the present value of $21.25 today and buy one share. The

- 40. Binomial Option Pricing Model The levered equity portfolio value today is today’s value of one share

- 41. Binomial Option Pricing Model We can value the option today as half of the value of

- 42. The Binomial Option Pricing Model If the interest rate is 5%, the call is worth: $25

- 43. The Binomial Option Pricing Model If the interest rate is 5%, the call is worth: $25

- 44. Binomial Option Pricing Model the replicating portfolio intuition. Many derivative securities can be valued by valuing

- 45. The Risk-Neutral Approach to Valuation We could value V(0) as the value of the replicating portfolio.

- 46. The Risk-Neutral Approach to Valuation S(0) is the value of the underlying asset today. S(0), V(0)

- 47. The Risk-Neutral Approach to Valuation The key to finding q is to note that it is

- 48. Example of the Risk-Neutral Valuation of a Call: Suppose a stock is worth $25 today and

- 49. Example of the Risk-Neutral Valuation of a Call: The next step would be to compute the

- 50. Example of the Risk-Neutral Valuation of a Call: After that, find the value of the call

- 51. Example of the Risk-Neutral Valuation of a Call: Finally, find the value of the call at

- 52. Risk-Neutral Valuation and the Replicating Portfolio This risk-neutral result is consistent with valuing the call using

- 53. The Black-Scholes Model The Black-Scholes Model is Where C0 = the value of a European option

- 54. The Black-Scholes Model Find the value of a six-month call option on Microsoft with an exercise

- 55. The Black-Scholes Model Let’s try our hand at using the model. If you have a calculator

- 56. The Black-Scholes Model N(d1) = N(0.52815) = 0.7013 N(d2) = N(0.31602) = 0.62401

- 57. Assume S = $50, X = $45, T = 6 months, r = 10%, and σ

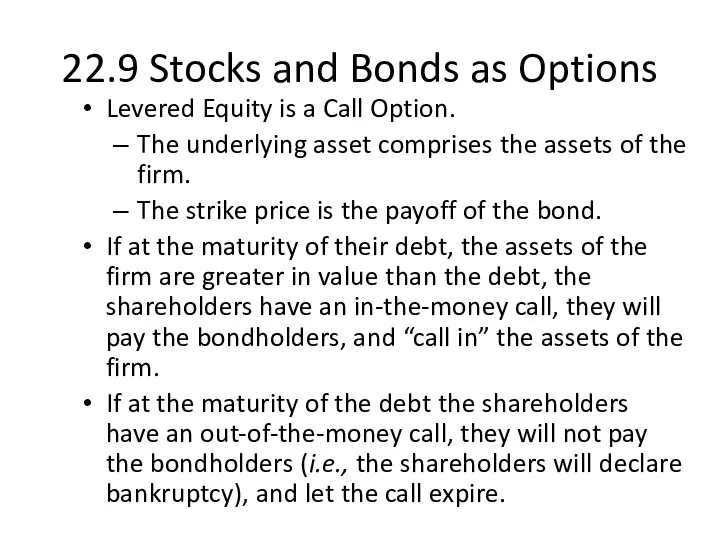

- 58. 22.9 Stocks and Bonds as Options Levered Equity is a Call Option. The underlying asset comprises

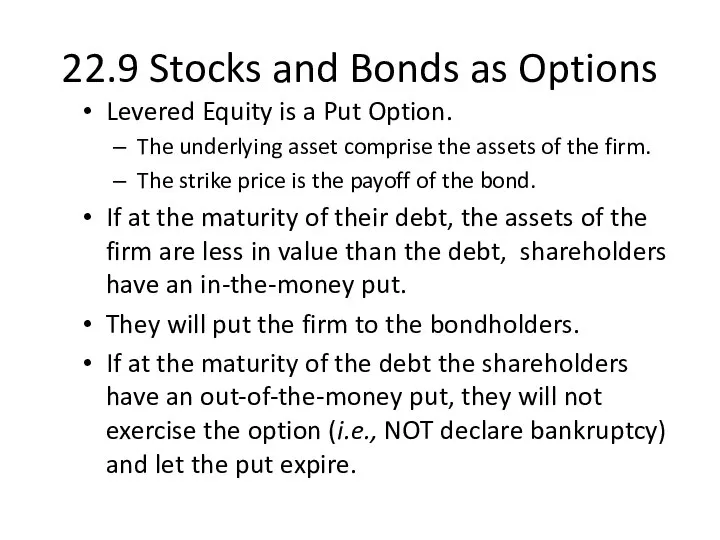

- 59. 22.9 Stocks and Bonds as Options Levered Equity is a Put Option. The underlying asset comprise

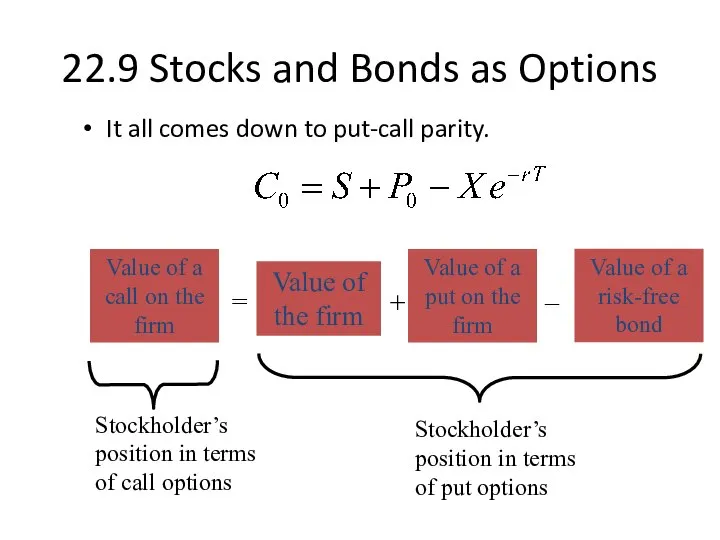

- 60. 22.9 Stocks and Bonds as Options It all comes down to put-call parity. Stockholder’s position in

- 61. 22.10 Capital-Structure Policy and Options Recall some of the agency costs of debt: they can all

- 62. Balance Sheet for a Company in Distress Assets BV MV Liabilities BV MV Cash $200 $200

- 63. Selfish Strategy 1: Take Large Risks (Think of a Call Option) The Gamble Probability Payoff Win

- 64. Selfish Stockholders Accept Negative NPV Project with Large Risks Expected cash flow from the Gamble To

- 65. 22.11 Mergers and Options This is an area rich with optionality, both in the structuring of

- 66. 22.12 Investment in Real Projects & Options Classic NPV calculations typically ignore the flexibility that real-world

- 67. 22.13 Summary and Conclusions The most familiar options are puts and calls. Put options give the

- 69. Скачать презентацию

22.1 Options

Many corporate securities are similar to the stock options that

22.1 Options

Many corporate securities are similar to the stock options that

22.1 Options Contracts: Preliminaries

An option gives the holder the right, but

22.1 Options Contracts: Preliminaries

An option gives the holder the right, but

22.1 Options Contracts: Preliminaries

Exercising the Option

The act of buying or selling

22.1 Options Contracts: Preliminaries

Exercising the Option

The act of buying or selling

Options Contracts: Preliminaries

In-the-Money

The exercise price is less than the spot price

Options Contracts: Preliminaries

In-the-Money

The exercise price is less than the spot price

Options Contracts: Preliminaries

Intrinsic Value

The difference between the exercise price of the

Options Contracts: Preliminaries

Intrinsic Value

The difference between the exercise price of the

22.2 Call Options

Call options gives the holder the right, but not

22.2 Call Options

Call options gives the holder the right, but not

Basic Call Option Pricing Relationships at Expiry

At expiry, an American call

Basic Call Option Pricing Relationships at Expiry

At expiry, an American call

Call Option Payoffs

-20

100

90

80

70

60

0

10

20

30

40

50

-40

20

0

-60

40

60

Stock price ($)

Option payoffs ($)

Buy a call

Exercise price =

Call Option Payoffs

-20

100

90

80

70

60

0

10

20

30

40

50

-40

20

0

-60

40

60

Stock price ($)

Option payoffs ($)

Buy a call

Exercise price =

Call Option Payoffs

Write a call

Exercise price = $50

Call Option Payoffs

Write a call

Exercise price = $50

Call Option Profits

Write a call

Buy a call

Exercise price = $50; option

Call Option Profits

Write a call

Buy a call

Exercise price = $50; option

22.3 Put Options

Put options give the holder the right, but not

22.3 Put Options

Put options give the holder the right, but not

Basic Put Option Pricing Relationships at Expiry

At expiry, an American put

Basic Put Option Pricing Relationships at Expiry

At expiry, an American put

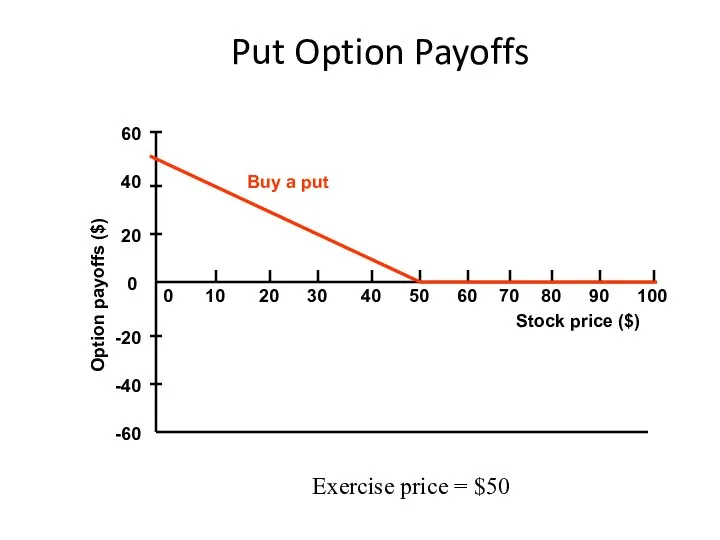

Put Option Payoffs

-20

100

90

80

70

60

0

10

20

30

40

50

-40

20

0

-60

40

60

Stock price ($)

Option payoffs ($)

Buy a put

Exercise price =

Put Option Payoffs

-20

100

90

80

70

60

0

10

20

30

40

50

-40

20

0

-60

40

60

Stock price ($)

Option payoffs ($)

Buy a put

Exercise price =

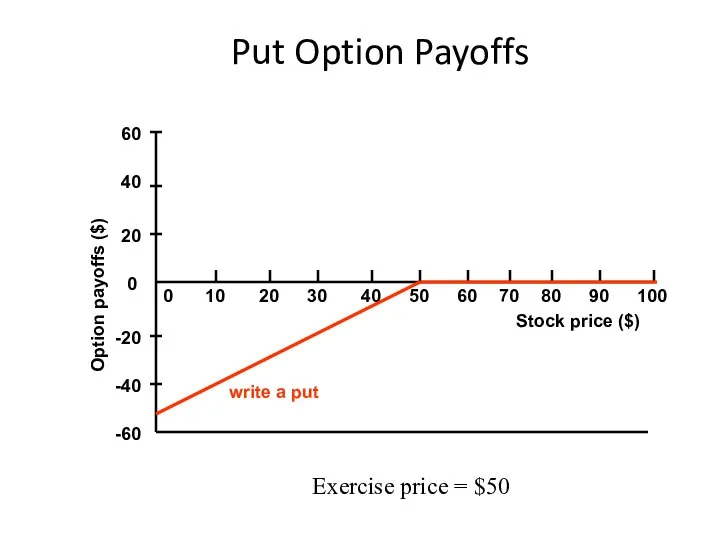

Put Option Payoffs

-20

100

90

80

70

60

0

10

20

30

40

50

-40

20

0

-60

40

60

Option payoffs ($)

write a put

Exercise price = $50

Stock price

Put Option Payoffs

-20

100

90

80

70

60

0

10

20

30

40

50

-40

20

0

-60

40

60

Option payoffs ($)

write a put

Exercise price = $50

Stock price

Put Option Profits

-20

100

90

80

70

60

0

10

20

30

40

50

-40

20

0

-60

40

60

Stock price ($)

Option profits ($)

Buy a put

Write a put

Exercise

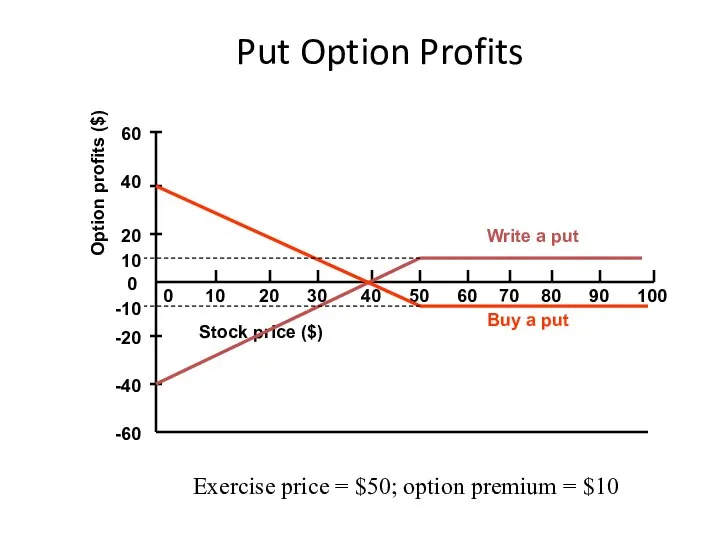

Put Option Profits

-20

100

90

80

70

60

0

10

20

30

40

50

-40

20

0

-60

40

60

Stock price ($)

Option profits ($)

Buy a put

Write a put

Exercise

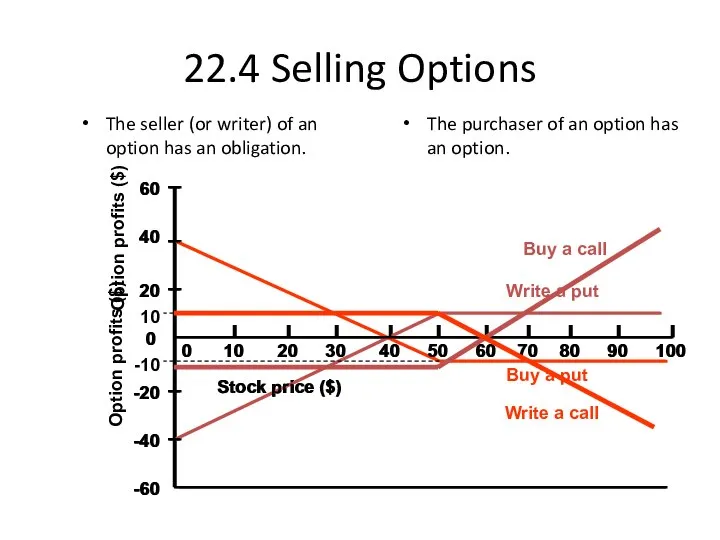

22.4 Selling Options

The seller (or writer) of an option has an

22.4 Selling Options

The seller (or writer) of an option has an

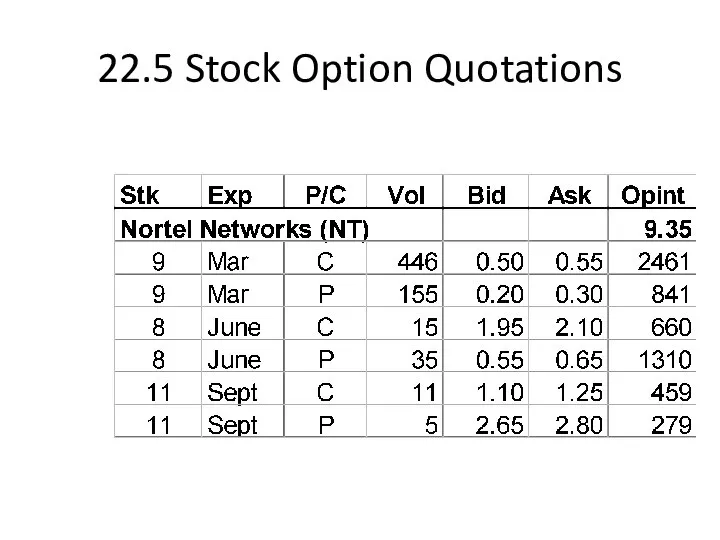

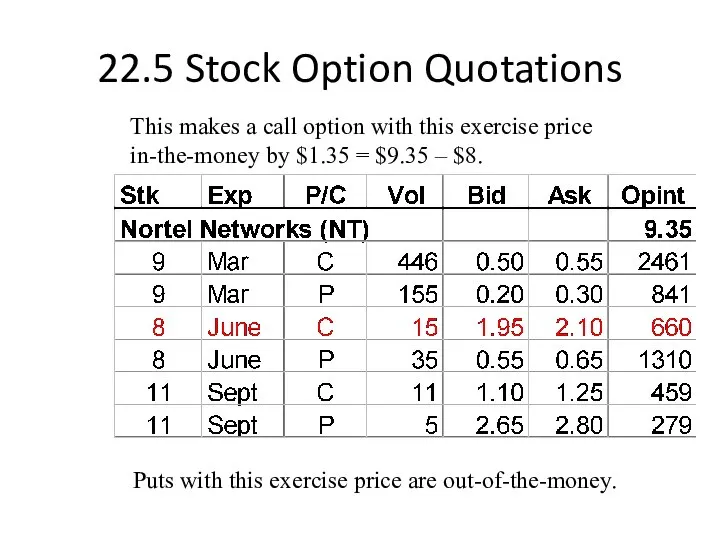

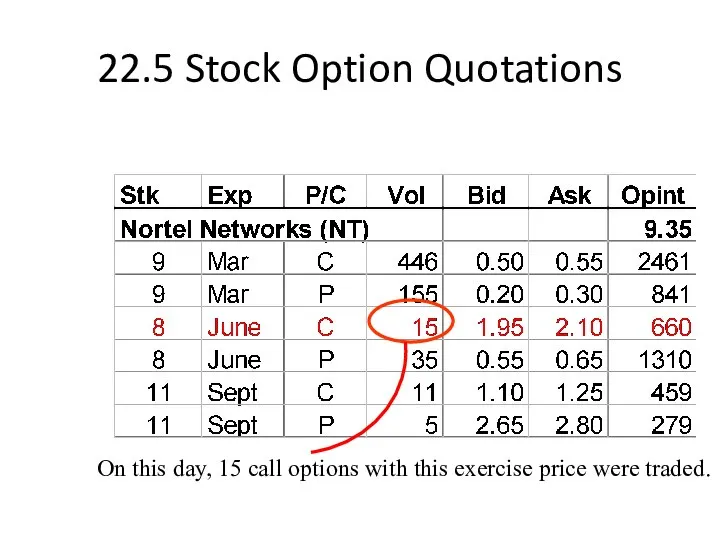

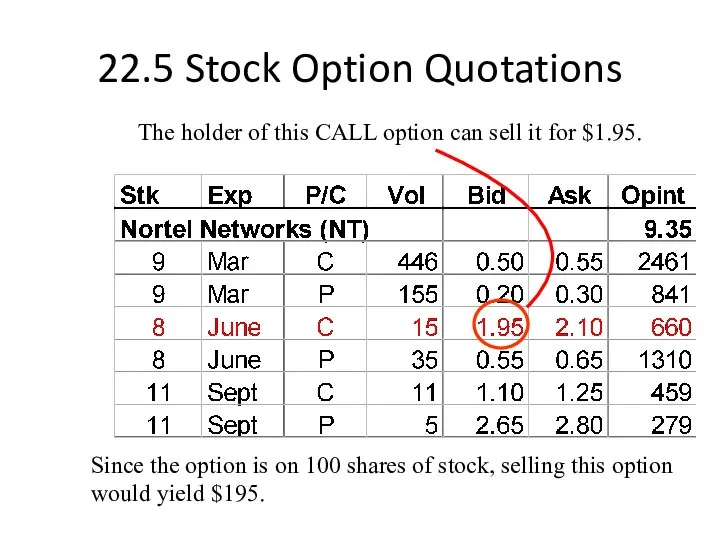

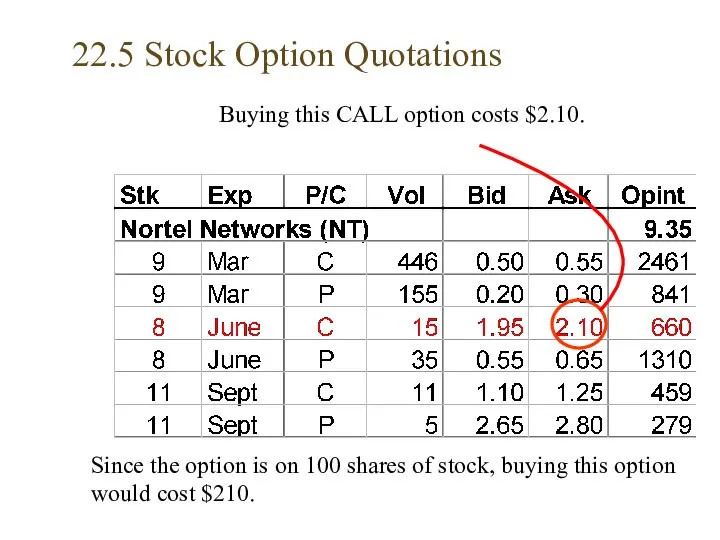

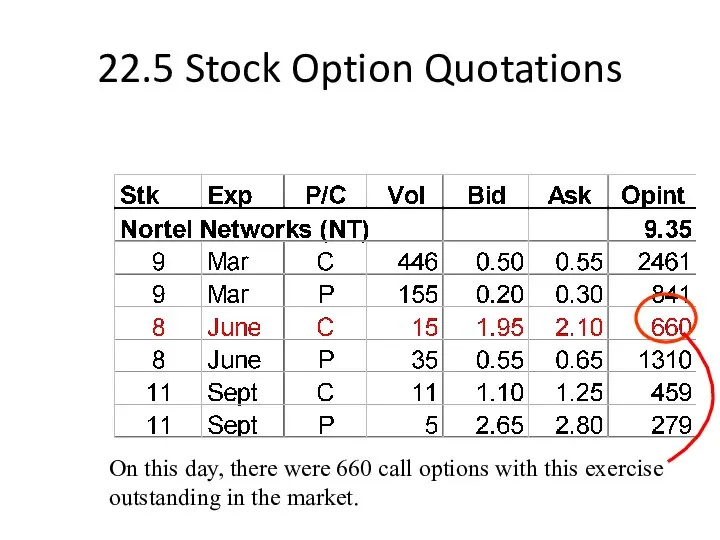

22.5 Stock Option Quotations

22.5 Stock Option Quotations

22.5 Stock Option Quotations

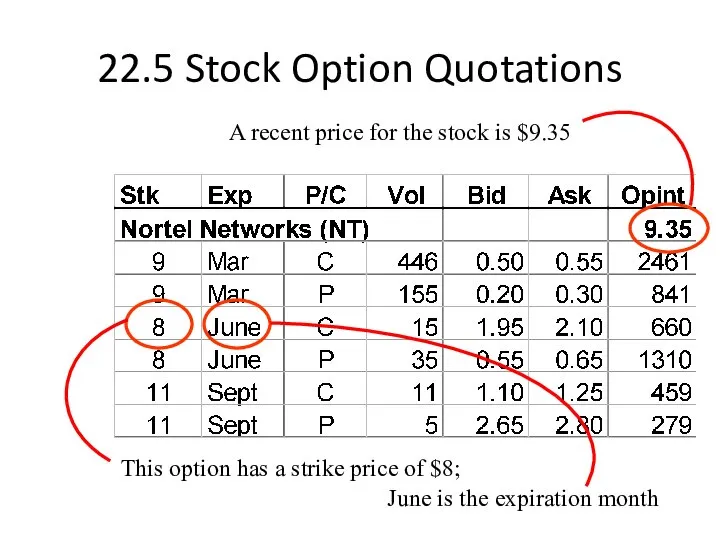

This option has a strike price of $8;

A

22.5 Stock Option Quotations

This option has a strike price of $8;

A

22.5 Stock Option Quotations

This makes a call option with this exercise

22.5 Stock Option Quotations

This makes a call option with this exercise

22.5 Stock Option Quotations

On this day, 15 call options with this

22.5 Stock Option Quotations

On this day, 15 call options with this

22.5 Stock Option Quotations

The holder of this CALL option can sell

22.5 Stock Option Quotations

The holder of this CALL option can sell

22.5 Stock Option Quotations

Buying this CALL option costs $2.10.

Since the option

22.5 Stock Option Quotations

Buying this CALL option costs $2.10.

Since the option

22.5 Stock Option Quotations

On this day, there were 660 call options

22.5 Stock Option Quotations

On this day, there were 660 call options

22.6 Combinations of Options

Puts and calls can serve as the building

22.6 Combinations of Options

Puts and calls can serve as the building

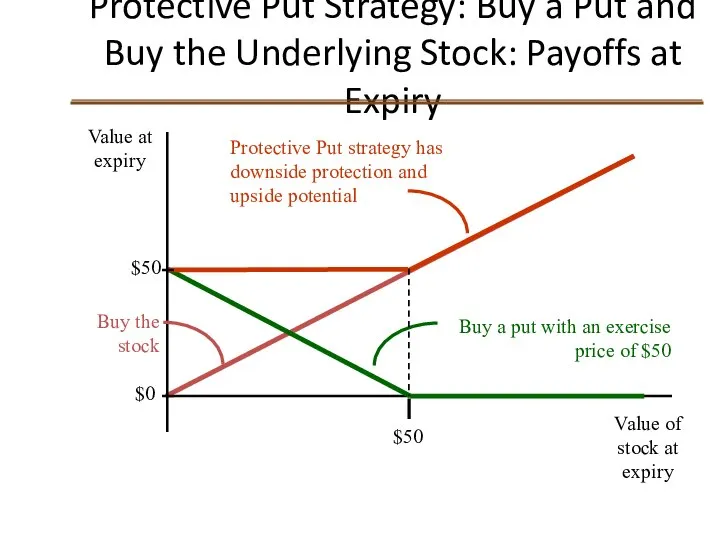

Protective Put Strategy: Buy a Put and Buy the Underlying Stock:

Protective Put Strategy: Buy a Put and Buy the Underlying Stock:

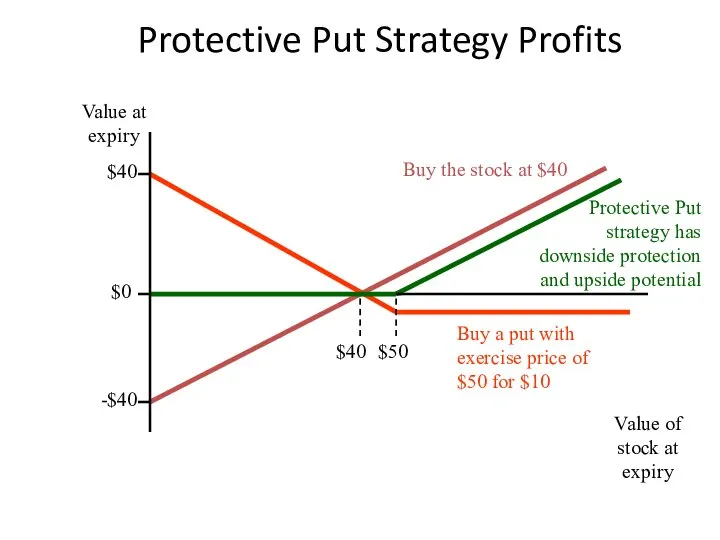

Protective Put Strategy Profits

Buy a put with exercise price of $50

Protective Put Strategy Profits

Buy a put with exercise price of $50

Covered Call Strategy

Sell a call with exercise price of $50 for

Covered Call Strategy

Sell a call with exercise price of $50 for

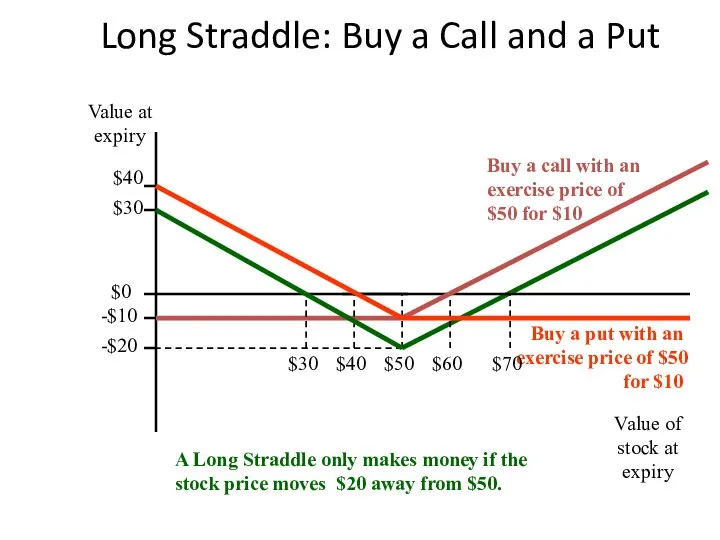

Long Straddle: Buy a Call and a Put

Buy a put with

Long Straddle: Buy a Call and a Put

Buy a put with

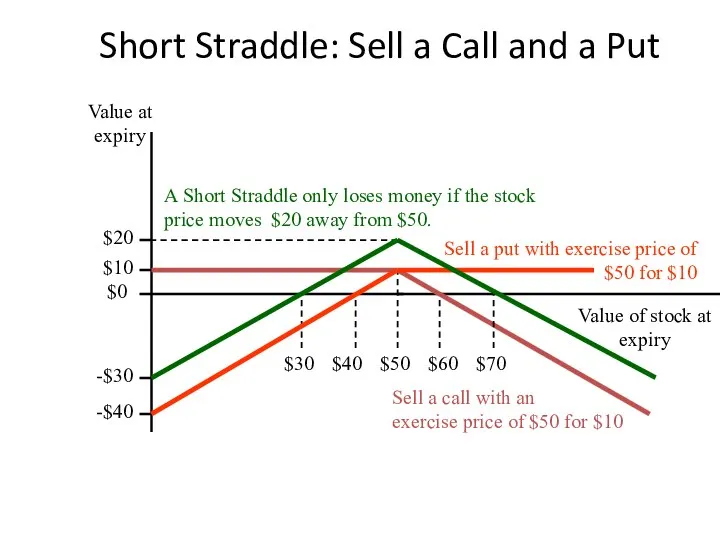

Short Straddle: Sell a Call and a Put

Sell a put with

Short Straddle: Sell a Call and a Put

Sell a put with

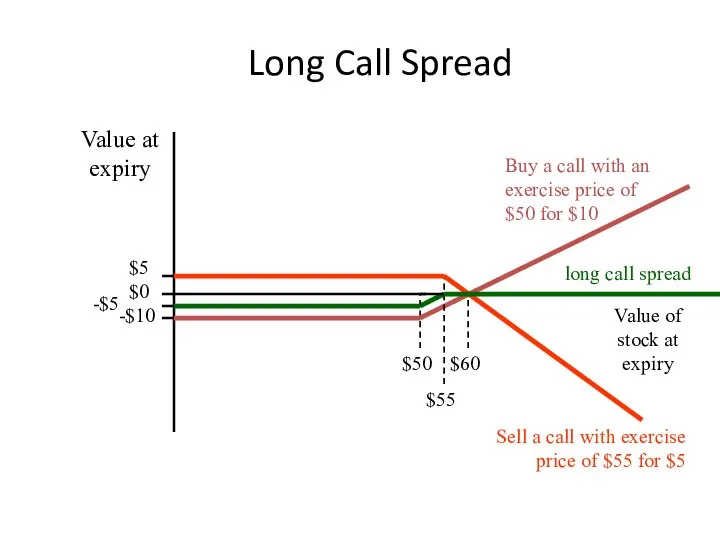

Long Call Spread

Sell a call with exercise price of $55 for

Long Call Spread

Sell a call with exercise price of $55 for

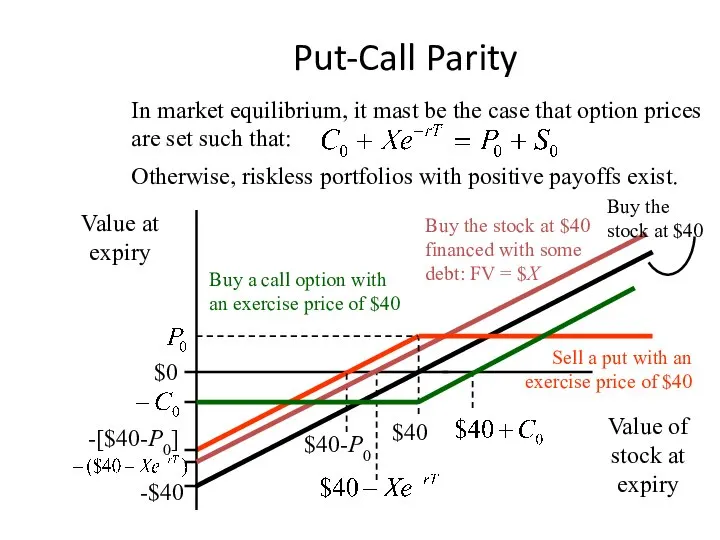

Put-Call Parity

Sell a put with an exercise price of $40

Buy the

Put-Call Parity

Sell a put with an exercise price of $40

Buy the

22.7 Valuing Options

The last section concerned itself with the value of

22.7 Valuing Options

The last section concerned itself with the value of

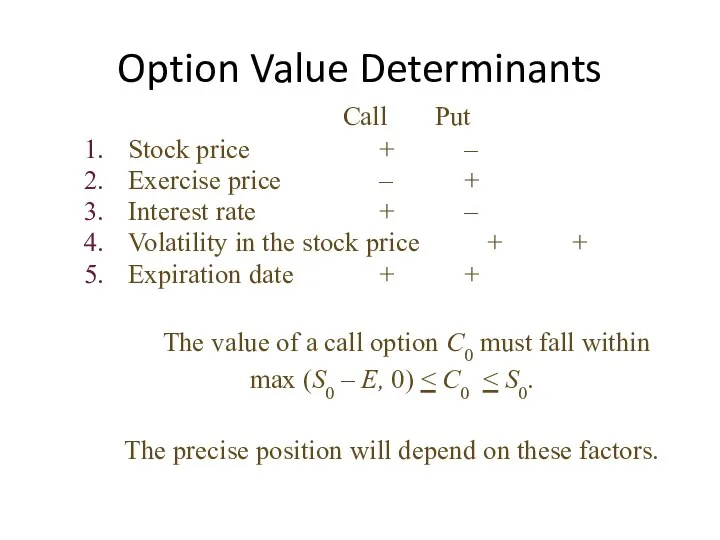

Option Value Determinants

Call Put

Stock price + –

Exercise price – +

Interest rate + –

Volatility

Option Value Determinants

Call Put

Stock price + –

Exercise price – +

Interest rate + –

Volatility

Market Value, Time Value, and Intrinsic Value for an American Call

CaT

Market Value, Time Value, and Intrinsic Value for an American Call

CaT

22.8 An Option‑Pricing Formula

We will start with a binomial option pricing

22.8 An Option‑Pricing Formula

We will start with a binomial option pricing

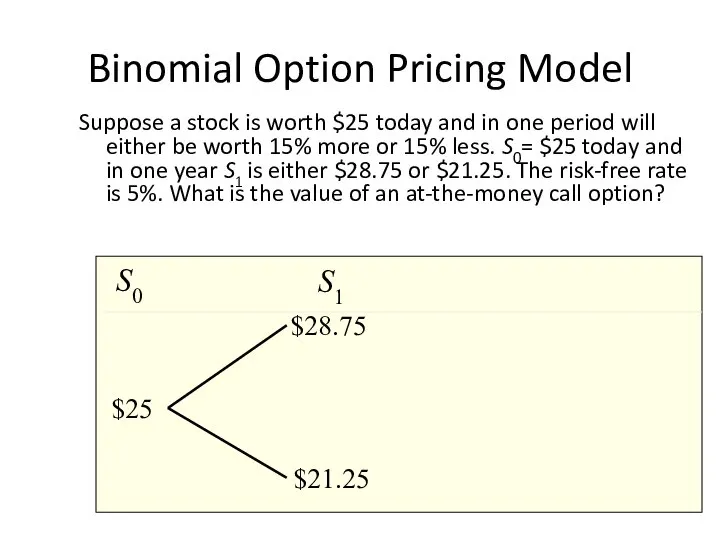

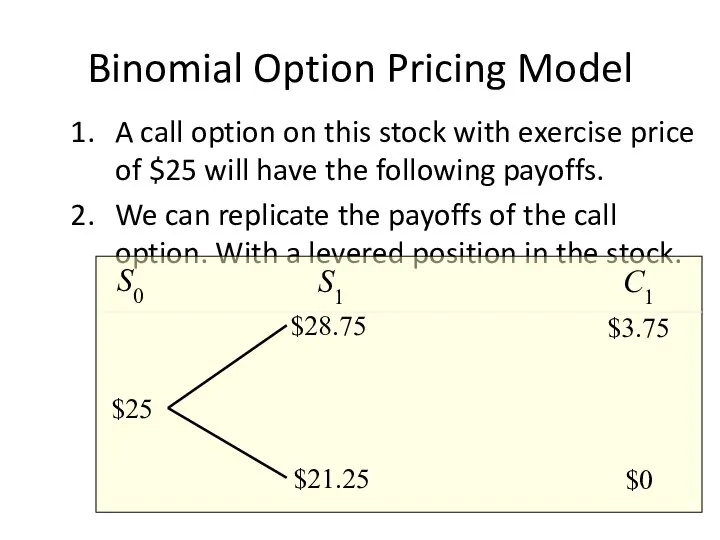

Binomial Option Pricing Model

Suppose a stock is worth $25 today and

Binomial Option Pricing Model

Suppose a stock is worth $25 today and

Binomial Option Pricing Model

A call option on this stock with exercise

Binomial Option Pricing Model

A call option on this stock with exercise

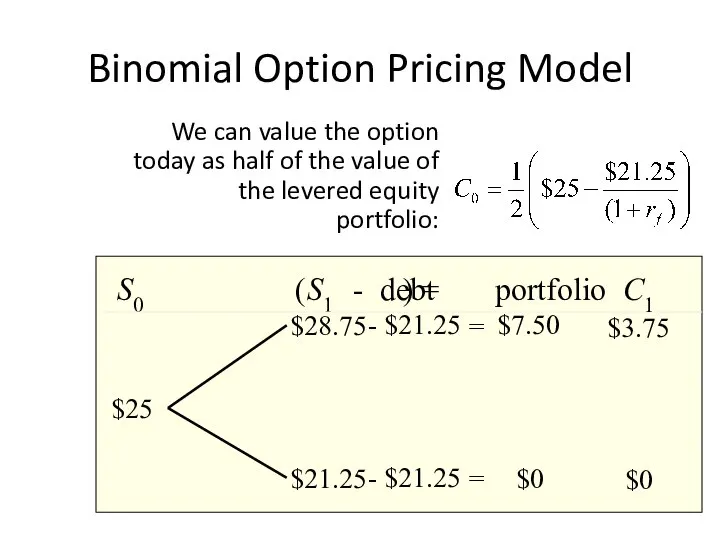

Binomial Option Pricing Model

Borrow the present value of $21.25 today and

Binomial Option Pricing Model

Borrow the present value of $21.25 today and

Binomial Option Pricing Model

The levered equity portfolio value today is

Binomial Option Pricing Model

The levered equity portfolio value today is

Binomial Option Pricing Model

We can value the option today as half

Binomial Option Pricing Model

We can value the option today as half

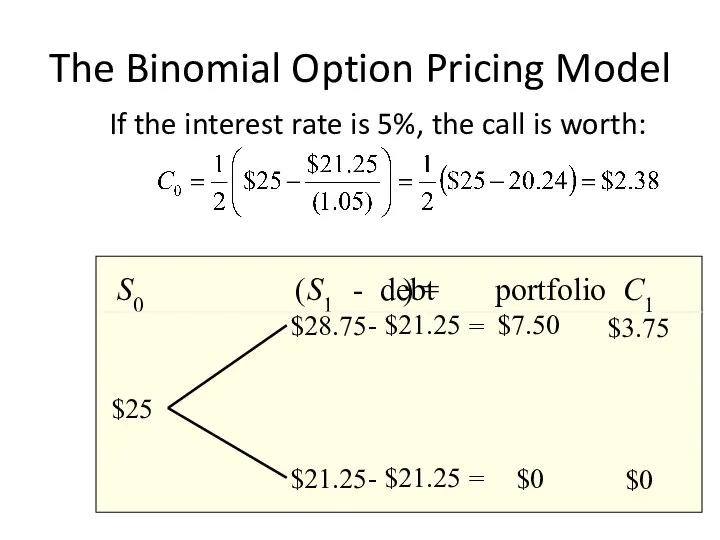

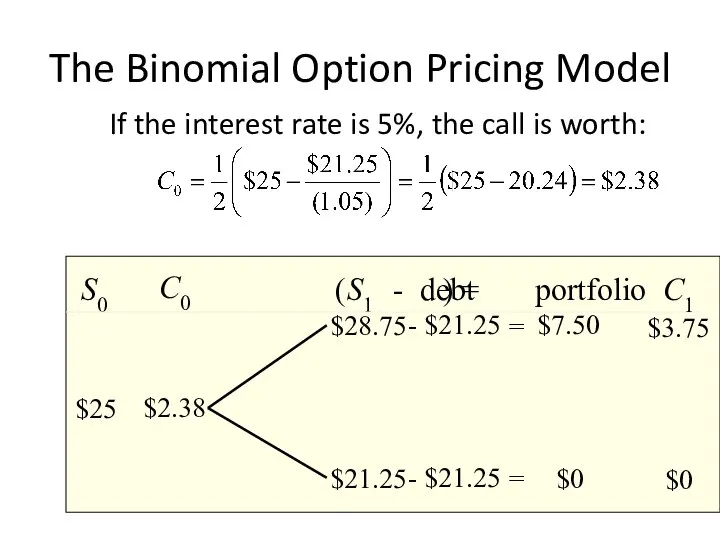

The Binomial Option Pricing Model

If the interest rate is 5%, the

The Binomial Option Pricing Model

If the interest rate is 5%, the

The Binomial Option Pricing Model

If the interest rate is 5%, the

The Binomial Option Pricing Model

If the interest rate is 5%, the

Binomial Option Pricing Model

the replicating portfolio intuition.

Many derivative securities can be

Binomial Option Pricing Model

the replicating portfolio intuition.

Many derivative securities can be

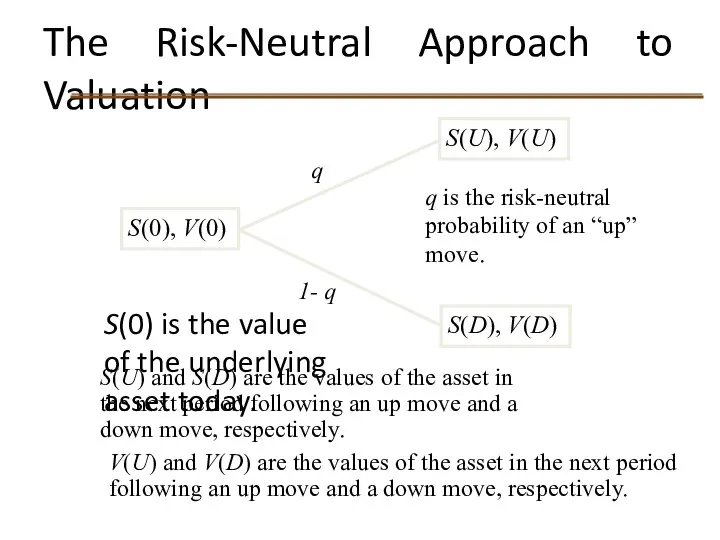

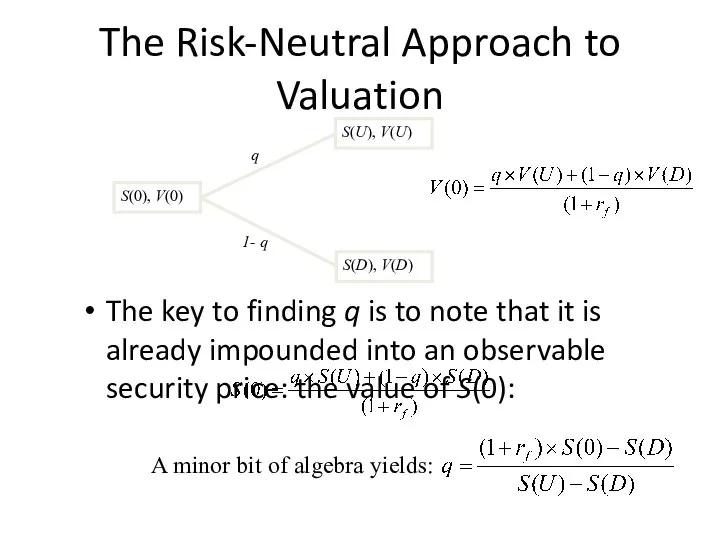

The Risk-Neutral Approach to Valuation

We could value V(0) as the value

The Risk-Neutral Approach to Valuation

We could value V(0) as the value

The Risk-Neutral Approach to Valuation

S(0) is the value of the underlying

The Risk-Neutral Approach to Valuation

S(0) is the value of the underlying

The Risk-Neutral Approach to Valuation

The key to finding q is to

The Risk-Neutral Approach to Valuation

The key to finding q is to

Example of the Risk-Neutral Valuation of a Call:

Suppose a stock is

Example of the Risk-Neutral Valuation of a Call:

Suppose a stock is

Example of the Risk-Neutral Valuation of a Call:

The next step would

Example of the Risk-Neutral Valuation of a Call:

The next step would

Example of the Risk-Neutral Valuation of a Call:

After that, find the

Example of the Risk-Neutral Valuation of a Call:

After that, find the

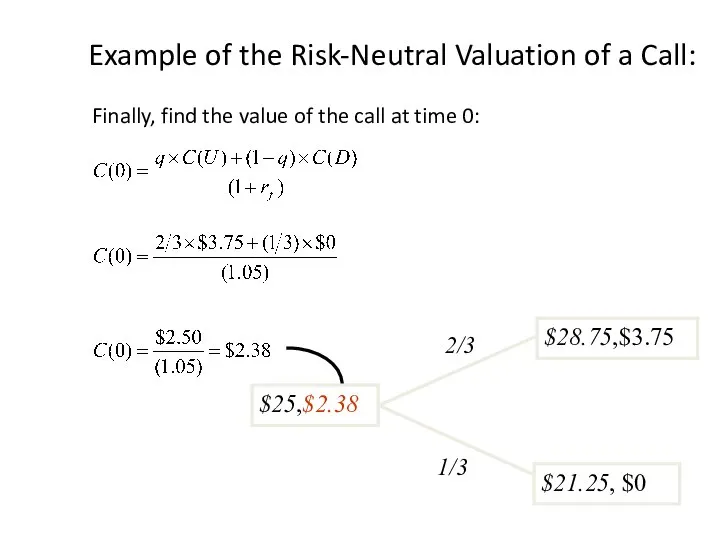

Example of the Risk-Neutral Valuation of a Call:

Finally, find the value

Example of the Risk-Neutral Valuation of a Call:

Finally, find the value

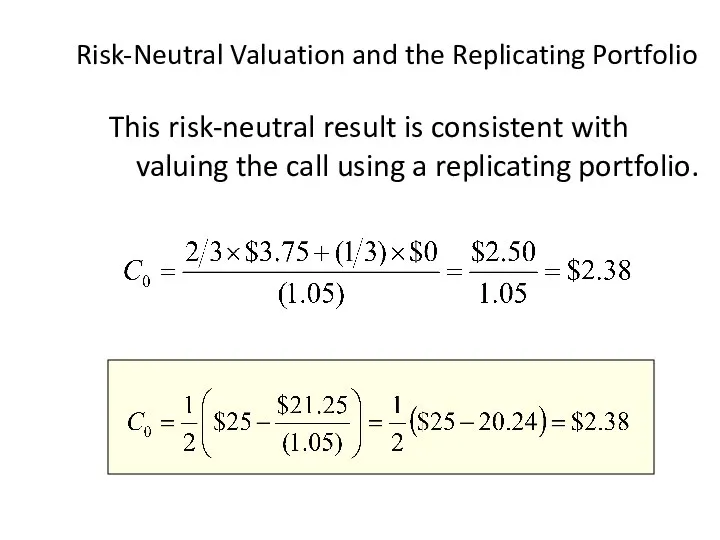

Risk-Neutral Valuation and the Replicating Portfolio

This risk-neutral result is consistent with

Risk-Neutral Valuation and the Replicating Portfolio

This risk-neutral result is consistent with

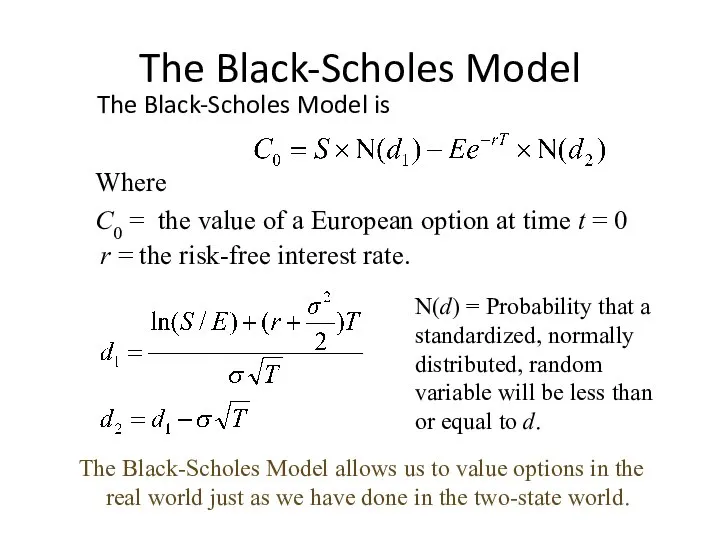

The Black-Scholes Model

The Black-Scholes Model is

Where

C0 = the value of a

The Black-Scholes Model

The Black-Scholes Model is

Where

C0 = the value of a

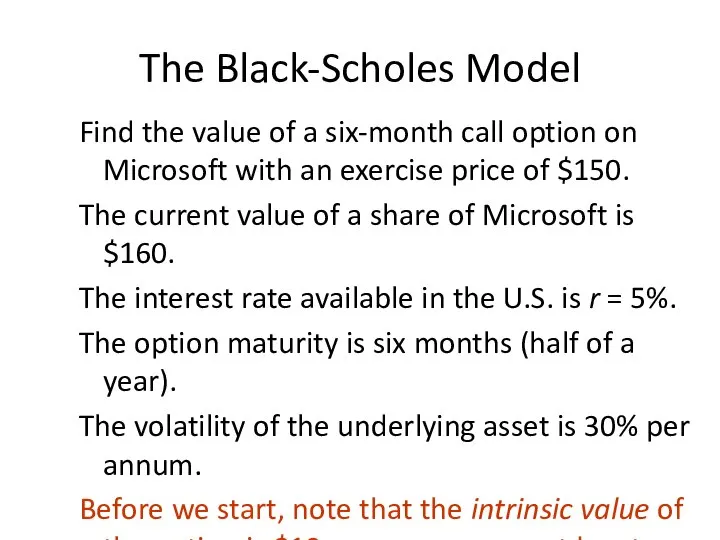

The Black-Scholes Model

Find the value of a six-month call option on

The Black-Scholes Model

Find the value of a six-month call option on

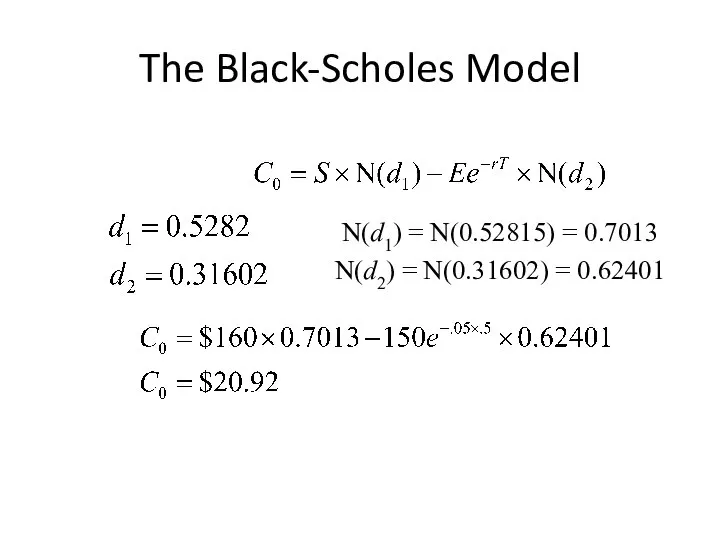

The Black-Scholes Model

Let’s try our hand at using the model. If

The Black-Scholes Model

Let’s try our hand at using the model. If

The Black-Scholes Model

N(d1) = N(0.52815) = 0.7013

N(d2) = N(0.31602) = 0.62401

The Black-Scholes Model

N(d1) = N(0.52815) = 0.7013

N(d2) = N(0.31602) = 0.62401

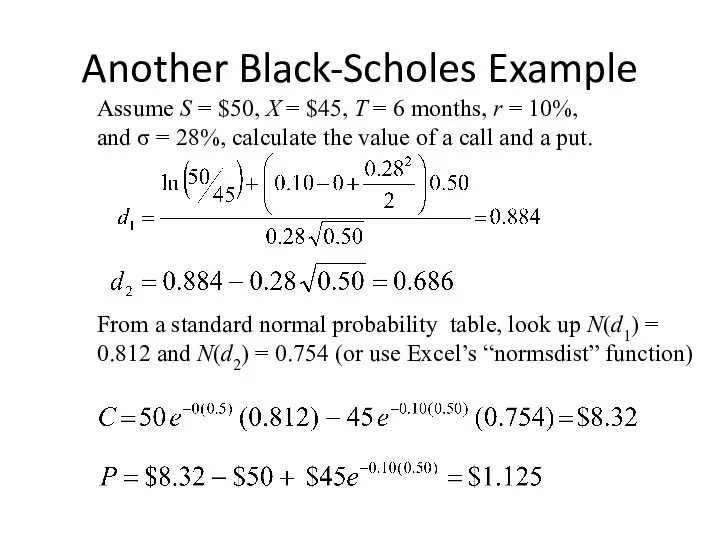

Assume S = $50, X = $45, T = 6 months,

Assume S = $50, X = $45, T = 6 months,

22.9 Stocks and Bonds as Options

Levered Equity is a Call Option.

The

22.9 Stocks and Bonds as Options

Levered Equity is a Call Option.

The

22.9 Stocks and Bonds as Options

Levered Equity is a Put Option.

The

22.9 Stocks and Bonds as Options

Levered Equity is a Put Option.

The

22.9 Stocks and Bonds as Options

It all comes down to put-call

22.9 Stocks and Bonds as Options

It all comes down to put-call

22.10 Capital-Structure Policy and Options

Recall some of the agency costs of

22.10 Capital-Structure Policy and Options

Recall some of the agency costs of

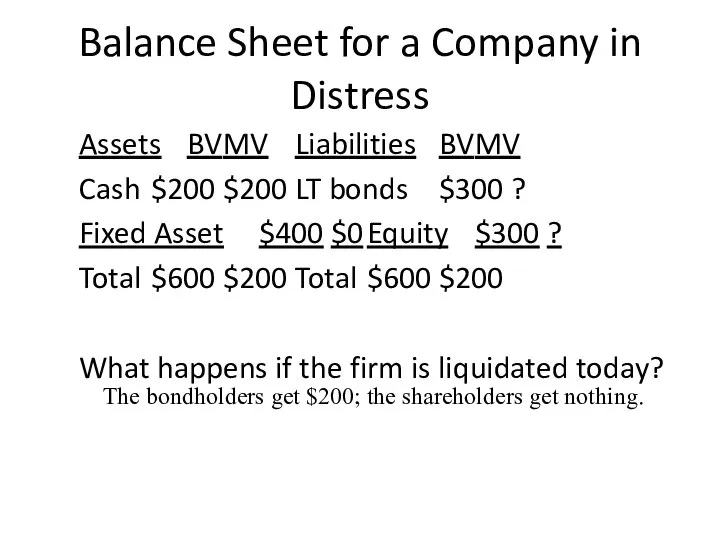

Balance Sheet for a Company in Distress

Assets BV MV Liabilities BV MV

Cash $200 $200 LT bonds $300 ?

Fixed Asset $400 $0 Equity $300 ?

Total $600 $200 Total $600 $200

What happens if

Balance Sheet for a Company in Distress

Assets BV MV Liabilities BV MV

Cash $200 $200 LT bonds $300 ?

Fixed Asset $400 $0 Equity $300 ?

Total $600 $200 Total $600 $200

What happens if

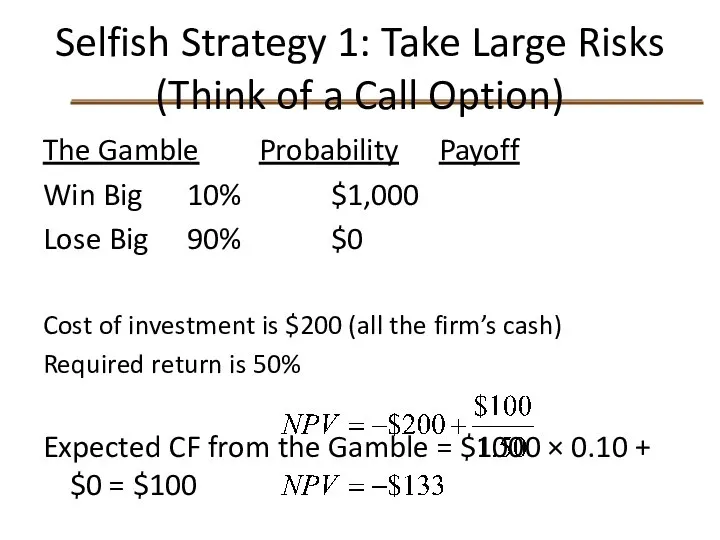

Selfish Strategy 1: Take Large Risks

(Think of a Call Option)

The

Selfish Strategy 1: Take Large Risks

(Think of a Call Option)

The

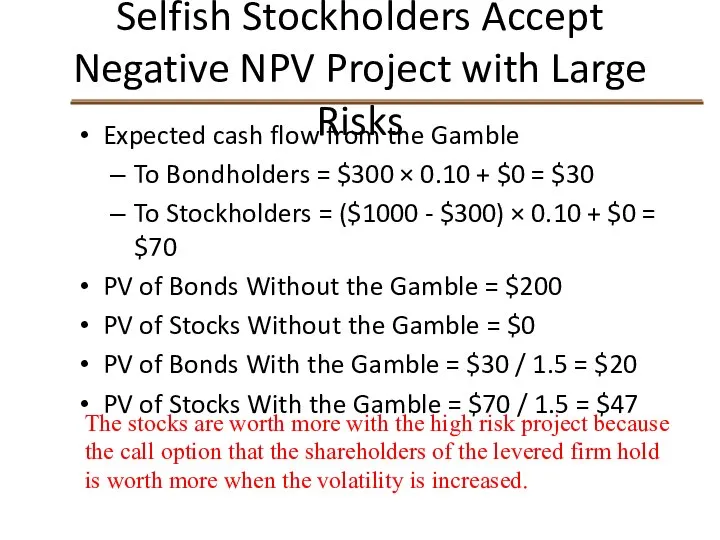

Selfish Stockholders Accept Negative NPV Project with Large Risks

Expected cash flow

Selfish Stockholders Accept Negative NPV Project with Large Risks

Expected cash flow

22.11 Mergers and Options

This is an area rich with optionality, both

22.11 Mergers and Options

This is an area rich with optionality, both

22.12 Investment in Real Projects & Options

Classic NPV calculations typically ignore

22.12 Investment in Real Projects & Options

Classic NPV calculations typically ignore

22.13 Summary and Conclusions

The most familiar options are puts and calls.

Put

22.13 Summary and Conclusions

The most familiar options are puts and calls.

Put

Типы экономических систем

Типы экономических систем Экономические аспекты

Экономические аспекты Производный спрос. Спрос на труд. Предложение труда для отдельной фирмы

Производный спрос. Спрос на труд. Предложение труда для отдельной фирмы Курс Экономика. Лекция № 1. Что и как изучает экономическая наука

Курс Экономика. Лекция № 1. Что и как изучает экономическая наука Глобальні пріоритети міжнародних стратегій економічного розвитку: сталість, конкурентоспроможність, макроекономічна стійкість

Глобальні пріоритети міжнародних стратегій економічного розвитку: сталість, конкурентоспроможність, макроекономічна стійкість Структура предприятия и организация производственного процесса

Структура предприятия и организация производственного процесса Общее макроэкономическое равновесие: модель AD – АS

Общее макроэкономическое равновесие: модель AD – АS Китай и глобальный финансовый кризис

Китай и глобальный финансовый кризис Якість як об’єкт управління

Якість як об’єкт управління Инвестиционные проекты Группы компаний «Сигма» в Республике Башкортостан

Инвестиционные проекты Группы компаний «Сигма» в Республике Башкортостан Животноводство-России

Животноводство-России Разработка организационных схем и адаптивной стратегии комплексного развития региональной ипотеки

Разработка организационных схем и адаптивной стратегии комплексного развития региональной ипотеки Сущность и экономические эффекты прямых инвестиций

Сущность и экономические эффекты прямых инвестиций Микроэкономика. Происхождение и развитие системы экономических знаний. Выделение экономической теории в самостоятельную науку

Микроэкономика. Происхождение и развитие системы экономических знаний. Выделение экономической теории в самостоятельную науку Цена земли и арендная плата

Цена земли и арендная плата Финансы, как экономическая категория

Финансы, как экономическая категория Резервный фонд и фонд национального благосостояния, особенности управления

Резервный фонд и фонд национального благосостояния, особенности управления Экономическая теория прав собственности

Экономическая теория прав собственности Государство и экономика

Государство и экономика Экономика 21 века: почему политэкономия и есть ли альтернатива?

Экономика 21 века: почему политэкономия и есть ли альтернатива? Прогноз развития крупнейшего города: конструирование будущего

Прогноз развития крупнейшего города: конструирование будущего Социальная политика и распределение доходов

Социальная политика и распределение доходов Культура потребления

Культура потребления Понятие и правовой статус органов исполнительной власти Выполнил:Студент II-го курса Группы: ЮБ 02/1403 Благодатнов Александр

Понятие и правовой статус органов исполнительной власти Выполнил:Студент II-го курса Группы: ЮБ 02/1403 Благодатнов Александр  Презентация Понятие и особенности функционирования валютного рынка

Презентация Понятие и особенности функционирования валютного рынка  Рынок, его механизмы и функции

Рынок, его механизмы и функции Неравенство в Европе в 1990-2016 годах

Неравенство в Европе в 1990-2016 годах Концессии в ЖКХ: экономико-социальный аспект

Концессии в ЖКХ: экономико-социальный аспект