- Factor Models: Announcements, Surprises, and Expected Returns

Содержание

- 2. 11.1 Factor Models: Announcements, Surprises, and Expected Returns The return on any security consists of two

- 3. 11.1 Factor Models: Announcements, Surprises, and Expected Returns A way to write the return on a

- 4. 11.1 Factor Models: Announcements, Surprises, and Expected Returns Any announcement can be broken down into two

- 5. 11.2 Risk: Systematic and Unsystematic A systematic risk is any risk that affects a large number

- 6. 11.2 Risk: Systematic and Unsystematic Systematic Risk; m Nonsystematic Risk; ε n σ Total risk; U

- 7. 11.2 Risk: Systematic and Unsystematic Systematic risk is referred to as market risk. m influences all

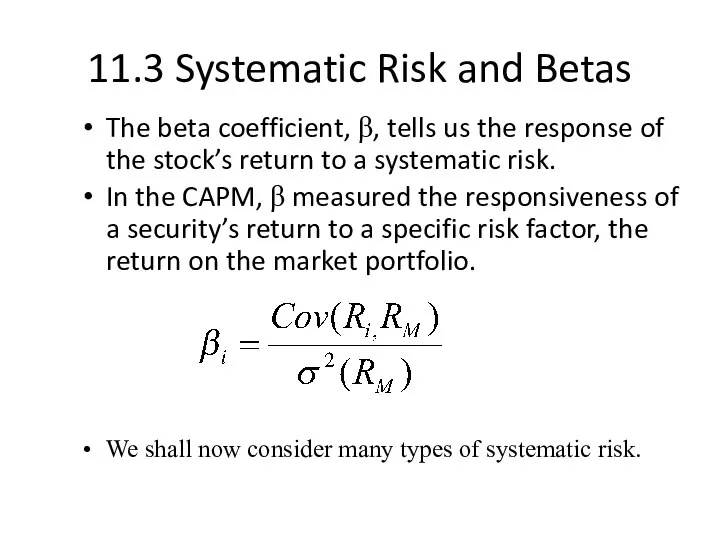

- 8. 11.3 Systematic Risk and Betas The beta coefficient, β, tells us the response of the stock’s

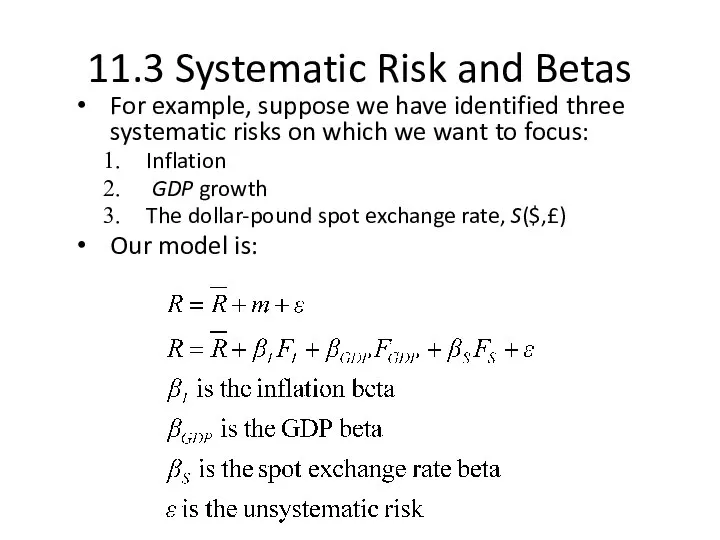

- 9. 11.3 Systematic Risk and Betas For example, suppose we have identified three systematic risks on which

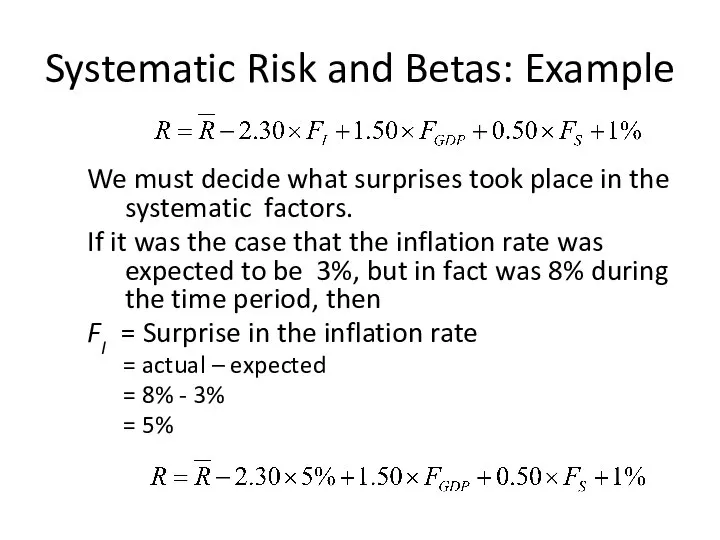

- 10. Systematic Risk and Betas: Example Suppose we have made the following estimates: βI = -2.30 βGDP

- 11. Systematic Risk and Betas: Example We must decide what surprises took place in the systematic factors.

- 12. Systematic Risk and Betas: Example If it was the case that the rate of GDP growth

- 13. Systematic Risk and Betas: Example If it was the case that dollar-pound spot exchange rate, S($,£),

- 14. Systematic Risk and Betas: Example Finally, if it was the case that the expected return on

- 15. 11.4 Portfolios and Factor Models Now let us consider what happens to portfolios of stocks when

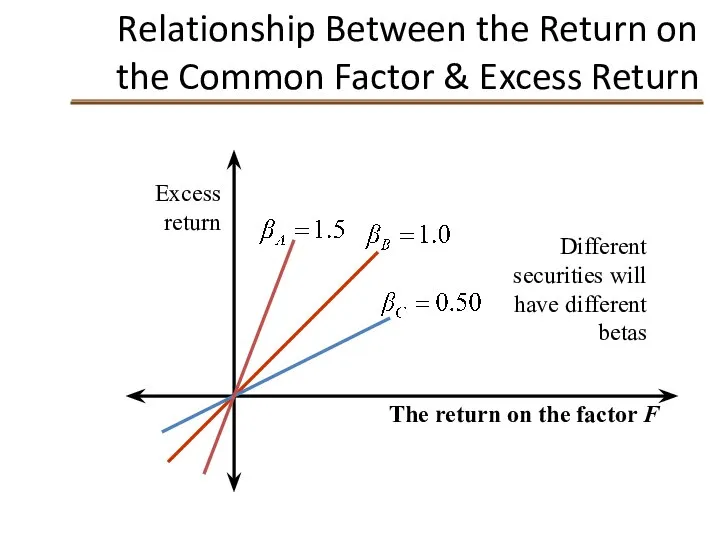

- 16. Relationship Between the Return on the Common Factor & Excess Return Excess return The return on

- 17. Relationship Between the Return on the Common Factor & Excess Return Excess return The return on

- 18. Relationship Between the Return on the Common Factor & Excess Return Excess return The return on

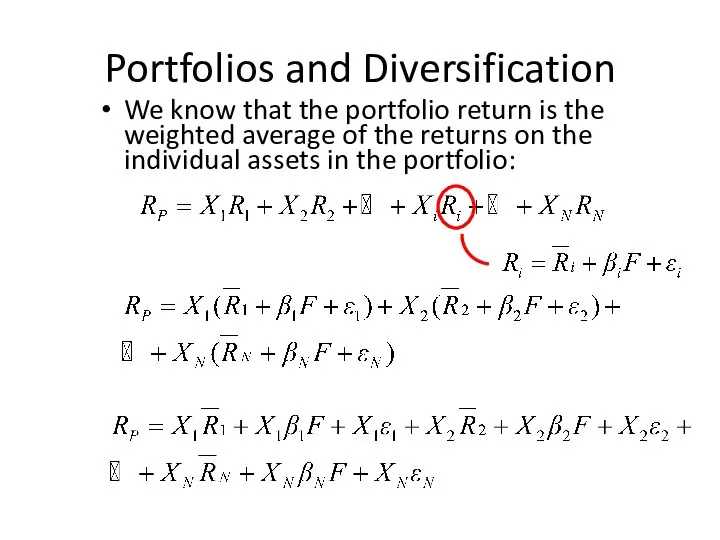

- 19. Portfolios and Diversification We know that the portfolio return is the weighted average of the returns

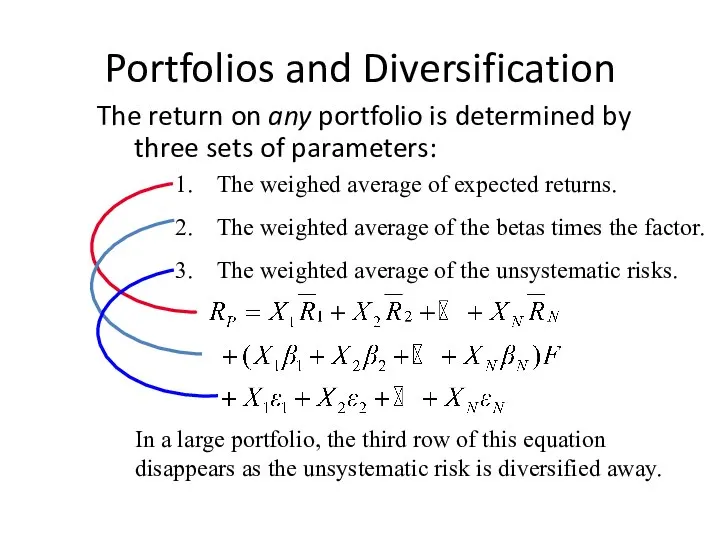

- 20. Portfolios and Diversification The return on any portfolio is determined by three sets of parameters: In

- 21. Portfolios and Diversification So the return on a diversified portfolio is determined by two sets of

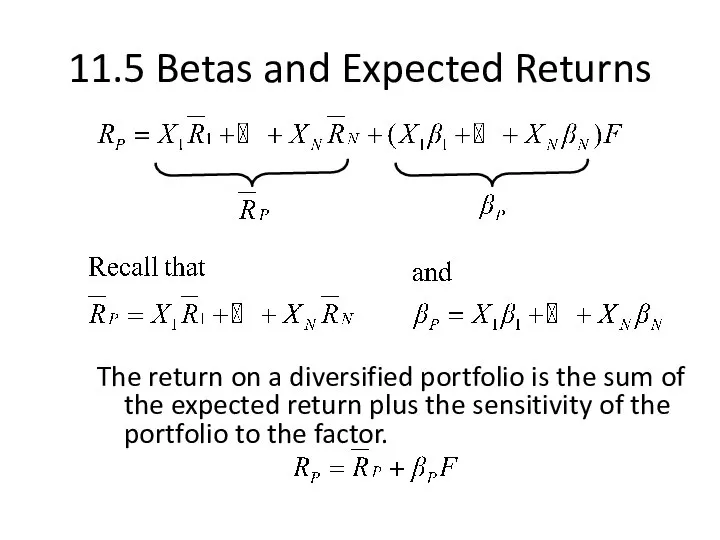

- 22. 11.5 Betas and Expected Returns The return on a diversified portfolio is the sum of the

- 23. Relationship Between β & Expected Return The relevant risk in large and well-diversified portfolios is all

- 24. Relationship Between β & Expected Return Expected return β A B C D SML

- 25. 11.6 The Capital Asset Pricing Model and the Arbitrage Pricing Theory APT applies to well diversified

- 26. Multi-factor APT Example: A Canadian study (Otuteye, CIR 1991) with five factors: the rate of growth

- 27. 11.7 Empirical Approaches to Asset Pricing Both the CAPM and APT are risk-based models. There are

- 29. Скачать презентацию

11.1 Factor Models: Announcements, Surprises, and Expected Returns

The return on any

11.1 Factor Models: Announcements, Surprises, and Expected Returns

The return on any

11.1 Factor Models: Announcements, Surprises, and Expected Returns

A way to write

11.1 Factor Models: Announcements, Surprises, and Expected Returns

A way to write

11.1 Factor Models: Announcements, Surprises, and Expected Returns

Any announcement can be

11.1 Factor Models: Announcements, Surprises, and Expected Returns

Any announcement can be

11.2 Risk: Systematic and Unsystematic

A systematic risk is any risk that

11.2 Risk: Systematic and Unsystematic

A systematic risk is any risk that

11.2 Risk: Systematic and Unsystematic

Systematic Risk; m

Nonsystematic Risk; ε

n

σ

Total risk;

11.2 Risk: Systematic and Unsystematic

Systematic Risk; m

Nonsystematic Risk; ε

n

σ

Total risk;

11.2 Risk: Systematic and Unsystematic

Systematic risk is referred to as market

11.2 Risk: Systematic and Unsystematic

Systematic risk is referred to as market

11.3 Systematic Risk and Betas

The beta coefficient, β, tells us the

11.3 Systematic Risk and Betas

The beta coefficient, β, tells us the

11.3 Systematic Risk and Betas

For example, suppose we have identified three

11.3 Systematic Risk and Betas

For example, suppose we have identified three

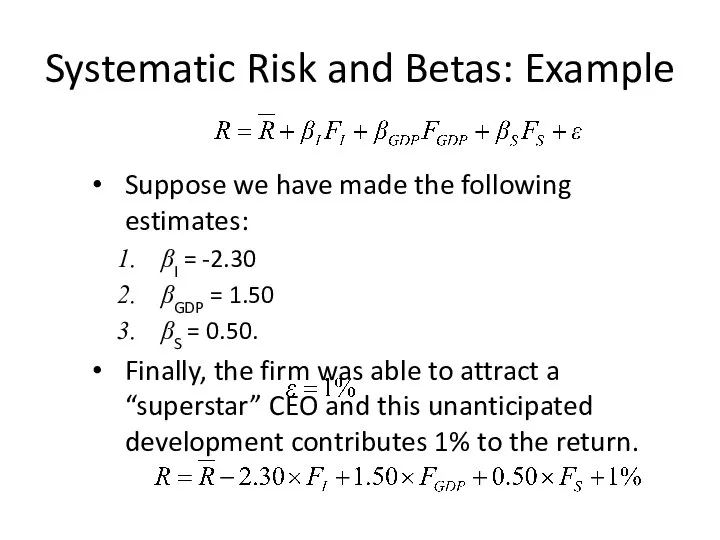

Systematic Risk and Betas: Example

Suppose we have made the following estimates:

βI

Systematic Risk and Betas: Example

Suppose we have made the following estimates:

βI

Systematic Risk and Betas: Example

We must decide what surprises took place

Systematic Risk and Betas: Example

We must decide what surprises took place

Systematic Risk and Betas: Example

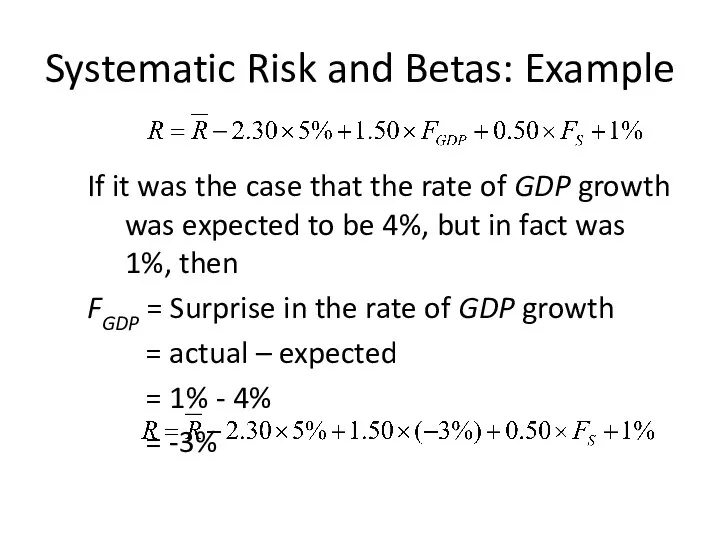

If it was the case that the

Systematic Risk and Betas: Example

If it was the case that the

Systematic Risk and Betas: Example

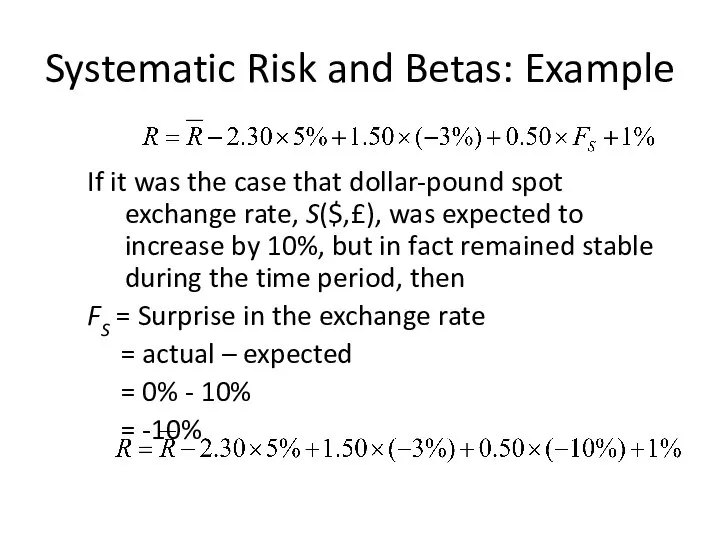

If it was the case that dollar-pound

Systematic Risk and Betas: Example

If it was the case that dollar-pound

Systematic Risk and Betas: Example

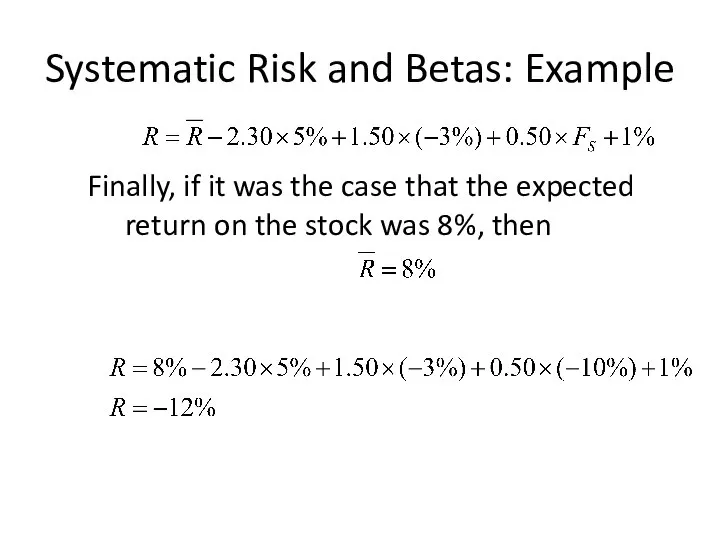

Finally, if it was the case that

Systematic Risk and Betas: Example

Finally, if it was the case that

11.4 Portfolios and Factor Models

Now let us consider what happens to

11.4 Portfolios and Factor Models

Now let us consider what happens to

Relationship Between the Return on the Common Factor & Excess Return

Excess

Relationship Between the Return on the Common Factor & Excess Return

Excess

Relationship Between the Return on the Common Factor & Excess Return

Excess

Relationship Between the Return on the Common Factor & Excess Return

Excess

Relationship Between the Return on the Common Factor & Excess Return

Excess

Relationship Between the Return on the Common Factor & Excess Return

Excess

Portfolios and Diversification

We know that the portfolio return is the weighted

Portfolios and Diversification

We know that the portfolio return is the weighted

Portfolios and Diversification

The return on any portfolio is determined by three

Portfolios and Diversification

The return on any portfolio is determined by three

Portfolios and Diversification

So the return on a diversified portfolio is determined

Portfolios and Diversification

So the return on a diversified portfolio is determined

11.5 Betas and Expected Returns

The return on a diversified portfolio is

11.5 Betas and Expected Returns

The return on a diversified portfolio is

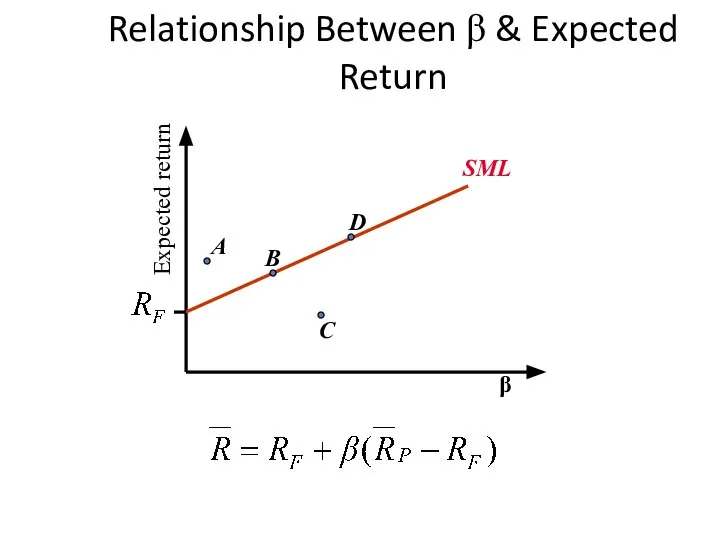

Relationship Between β & Expected Return

The relevant risk in large and

Relationship Between β & Expected Return

The relevant risk in large and

Relationship Between β & Expected Return

Expected return

β

A

B

C

D

SML

Relationship Between β & Expected Return

Expected return

β

A

B

C

D

SML

11.6 The Capital Asset Pricing Model and the Arbitrage Pricing Theory

APT

11.6 The Capital Asset Pricing Model and the Arbitrage Pricing Theory

APT

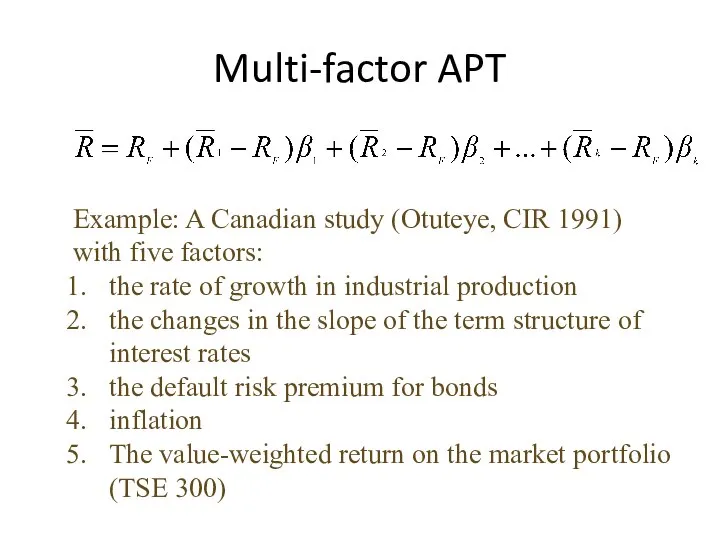

Multi-factor APT

Example: A Canadian study (Otuteye, CIR 1991)

with five factors:

the rate

Multi-factor APT

Example: A Canadian study (Otuteye, CIR 1991)

with five factors:

the rate

11.7 Empirical Approaches to Asset Pricing

Both the CAPM and APT are

11.7 Empirical Approaches to Asset Pricing

Both the CAPM and APT are

Ընդհանուր պատկերացումներ տնտեսության մասին

Ընդհանուր պատկերացումներ տնտեսության մասին Елдердің экономикалық көшбасшылары. Елдер түрлері: орталық, жартылай перифериялы, перифериялы. Географиялық орталықтар

Елдердің экономикалық көшбасшылары. Елдер түрлері: орталық, жартылай перифериялы, перифериялы. Географиялық орталықтар Актуальные вопросы туризма в России

Актуальные вопросы туризма в России Квалиметрия. Техника применения экспертного метода измерения качества продукции

Квалиметрия. Техника применения экспертного метода измерения качества продукции Политические институты и экономические результаты

Политические институты и экономические результаты Безработица. Типы и формы безработицы

Безработица. Типы и формы безработицы Экономикалық теорияның пәні және әдістері

Экономикалық теорияның пәні және әдістері История становления предпринимательства в России

История становления предпринимательства в России Пятиэтапная модель Роберта Гранта. GAP-анализ

Пятиэтапная модель Роберта Гранта. GAP-анализ Малиновский район міста Одеси. Слайды

Малиновский район міста Одеси. Слайды Содержание дисциплины Экономика и ее задачи

Содержание дисциплины Экономика и ее задачи Роль иностранного капитала в экономике России XIX-XX веков

Роль иностранного капитала в экономике России XIX-XX веков Мировое хозяйство и международная торговля

Мировое хозяйство и международная торговля Экономика - искусство ведения хозяйства

Экономика - искусство ведения хозяйства Типы экономических систем

Типы экономических систем Внешнеэкономическая деятельность Торгово-промышленной палаты Российской Федерации

Внешнеэкономическая деятельность Торгово-промышленной палаты Российской Федерации Основи аналізу попиту

Основи аналізу попиту Customer behavior specifics in the access economy: comparison of Russian and Italian carsharing customers

Customer behavior specifics in the access economy: comparison of Russian and Italian carsharing customers Презентация Таможенная политика в период складывания единого централизованного государства.

Презентация Таможенная политика в период складывания единого централизованного государства. Планирование производственных процессов и определение состава машинно-тракторного парка в ООО «Милославский ячмень»

Планирование производственных процессов и определение состава машинно-тракторного парка в ООО «Милославский ячмень» Еколого-економічне обґрунтування структури угідь та організації сівозмін фермерського господарства

Еколого-економічне обґрунтування структури угідь та організації сівозмін фермерського господарства Поддорское сельское поселение. Проект поддержки местных инициатив

Поддорское сельское поселение. Проект поддержки местных инициатив Организационная структура отрасли «торговля»

Организационная структура отрасли «торговля» Рынки факторов производства Цель: изучить специфику факторных рынков

Рынки факторов производства Цель: изучить специфику факторных рынков ВТО

ВТО Процедура взаимодействия СК с поставщиками по сервису (Мониторинг KPI и производственный аудит)

Процедура взаимодействия СК с поставщиками по сервису (Мониторинг KPI и производственный аудит) Нарықтық экономикалық жүйе және нарықтық механизм

Нарықтық экономикалық жүйе және нарықтық механизм Анализ региона: Юго-Восточная Азия

Анализ региона: Юго-Восточная Азия