- The Stock Market, the Theory of Rational Expectations, and the Efficient Markets Hypothesis

Содержание

- 2. © 2008 Pearson Education Canada 7. Ch 7: Stock Markets and Efficient Market Hypothesis. (*) Topics:

- 3. © 2008 Pearson Education Canada 7. The Markets for Stocks. (*) In Canada, stocks are traded

- 4. Common Stock Common stock is the principal way that corporations raise equity capital. Stockholders have the

- 5. Several Kinds of “Value” There are several types of value, of which we are concerned with

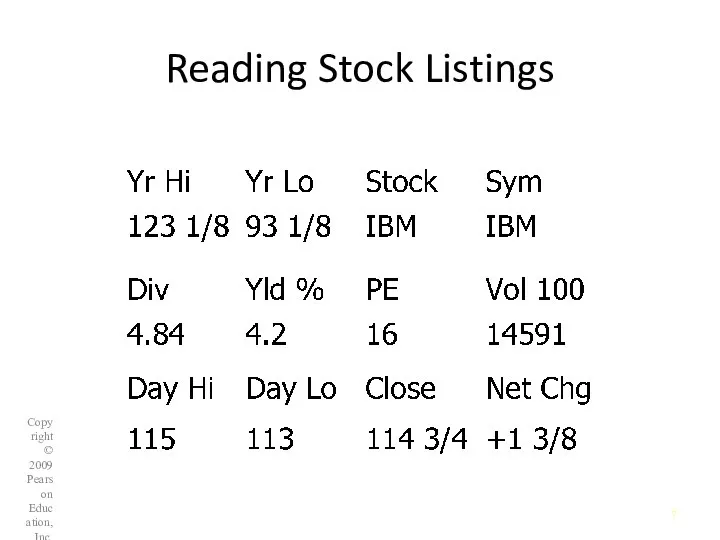

- 6. 9.1 Reading Stock Listings The following newspaper stock listing is usually printed as a horizontal string

- 7. Reading Stock Listings Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

- 8. Reading Stock Listings Hi = 123 1/8: The highest price the stock has traded at over

- 9. Reading Stock Listings Div = 4.84: The last quarterly dividend multiplied by 4 Yld % =

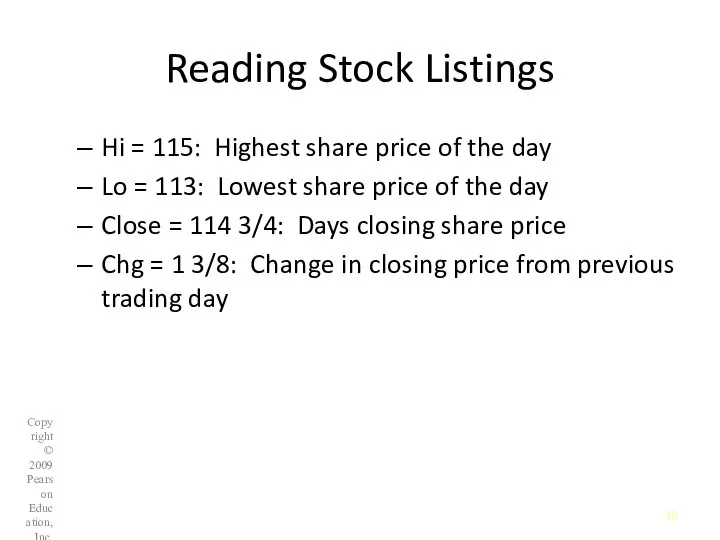

- 10. Reading Stock Listings Hi = 115: Highest share price of the day Lo = 113: Lowest

- 11. © 2008 Pearson Education Canada 7. The price of common stock. (*) Common stocks have two

- 12. Equation Total Return Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 9-

- 13. Rate of Total Return Copyright © 2008 Pearson Education Canada 10-

- 14. One-Period Valuation Model © 2008 Pearson Education Canada 7.

- 15. Generalized Dividend Valuation Model © 2008 Pearson Education Canada 7.

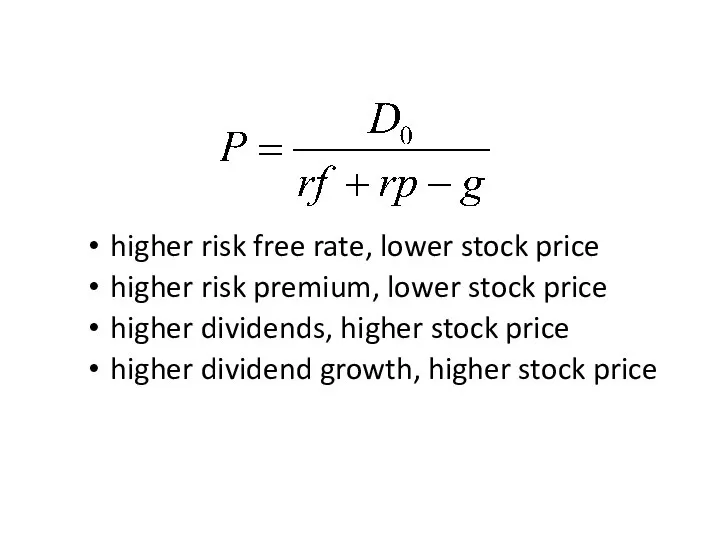

- 16. Gordon Growth Model © 2008 Pearson Education Canada 7.

- 17. © 2008 Pearson Education Canada 7. According to the above model, current stock prices depend on

- 18. Example 9.1 Stock Prices and Returns Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 9-

- 19. Example 9.1 Stock Prices and Returns Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 9-

- 20. Example Valuing a Firm with Constant Dividend Growth Copyright © 2007 Pearson Addison-Wesley. All rights reserved.

- 21. Example 9.2 Valuing a Firm with Constant Dividend Growth Copyright © 2007 Pearson Addison-Wesley. All rights

- 22. Factors Affecting Stock Prices Business cycles Interest rate changes Investor sentiment about Economy, Earnings And markets

- 23. interest rate = risk free rate + risk premium, ke = rf + rp then

- 24. higher risk free rate, lower stock price higher risk premium, lower stock price higher dividends, higher

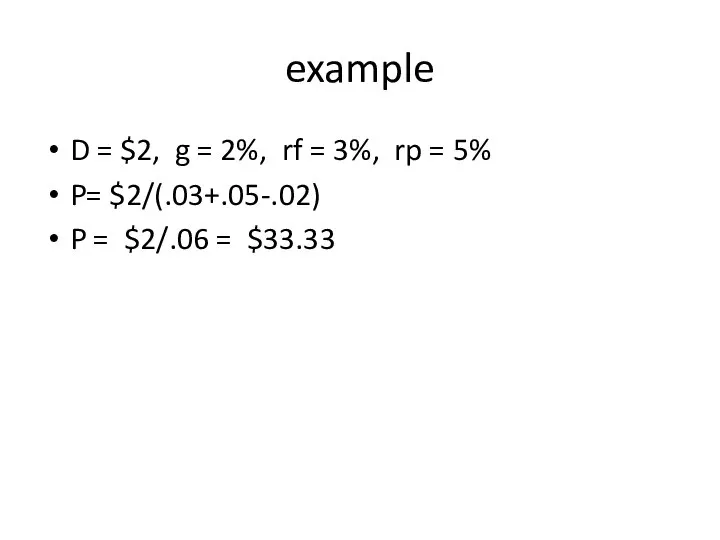

- 25. example D = $2, g = 2%, rf = 3%, rp = 5% P= $2/(.03+.05-.02) P

- 26. what if risk premium rises to 7%? P = $2/(.03+.07-.02) = $2/.08 = $12.50 what if

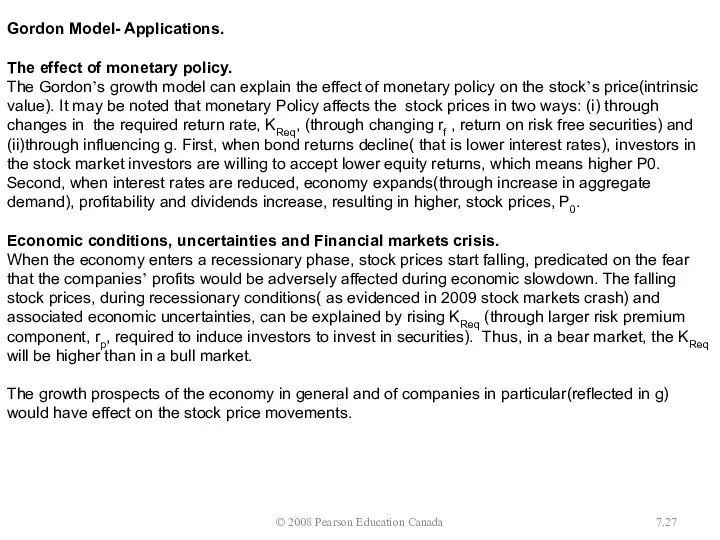

- 27. © 2008 Pearson Education Canada 7. Gordon Model- Applications. The effect of monetary policy. The Gordon’s

- 28. © 2008 Pearson Education Canada 7. Price-Earnings Ratio: The price/earnings ratio, which equals to the company’s

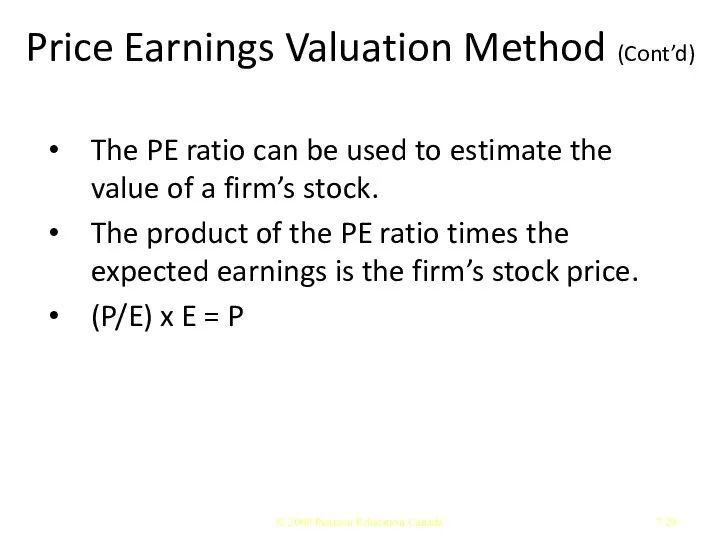

- 29. Price Earnings Valuation Method (Cont’d) The PE ratio can be used to estimate the value of

- 30. Stock Analysis Fundamental analysis Quantitative analysis Based on financial statements Qualitative analysis More subjective Examines management

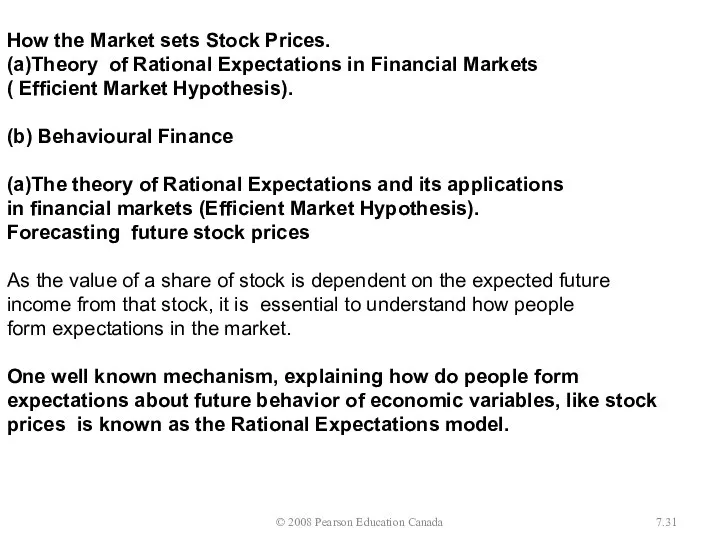

- 31. © 2008 Pearson Education Canada 7. How the Market sets Stock Prices. (a)Theory of Rational Expectations

- 32. © 2008 Pearson Education Canada 7. Rational Expectations Rational expectations theory views expectations as being identical

- 33. The Efficient Market The efficient-market hypothesis (EMH) asserts that financial markets are "informationally efficient", or that

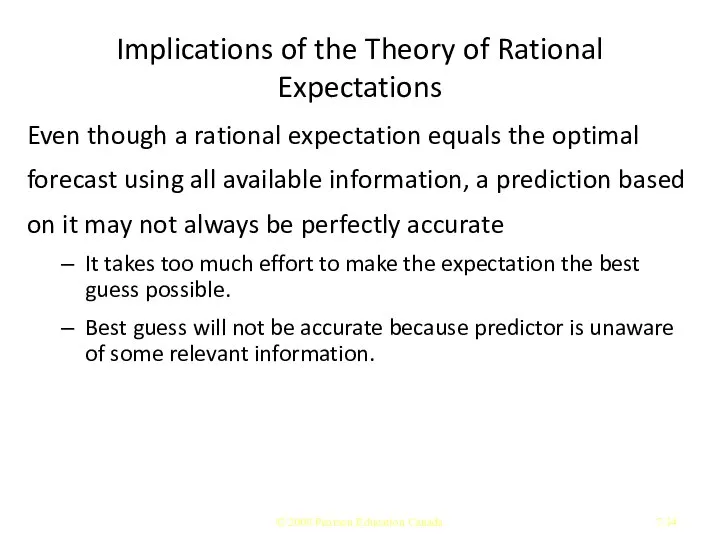

- 34. Implications of the Theory of Rational Expectations Even though a rational expectation equals the optimal forecast

- 35. Implications If there is a change in the way a variable moves, the way in which

- 36. Efficient Markets: An Application of Rational Expectations © 2008 Pearson Education Canada 7.

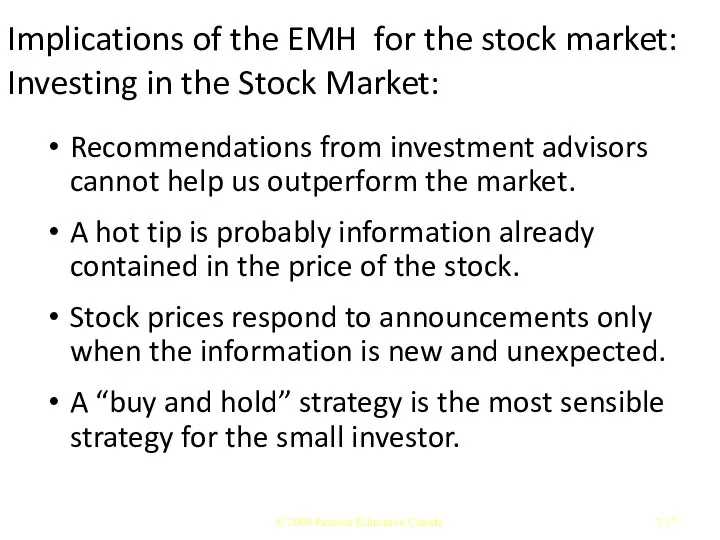

- 37. Implications of the EMH for the stock market: Investing in the Stock Market: Recommendations from investment

- 38. Evidence Against Market Efficiency Small-firm effect January Effect Market Overreaction Excessive Volatility Mean Reversion New information

- 39. (b)Behavioural Finance. The lack of short selling (causing over-priced stocks) may be explained by loss aversion.

- 40. (b) Behavioural Finance. Behavioral economists attribute the imperfections in financial markets to a combination of cognitive

- 41. Bubbles Large gaps between actual asset price and fundamental value Internet stock bubble of late 1990s

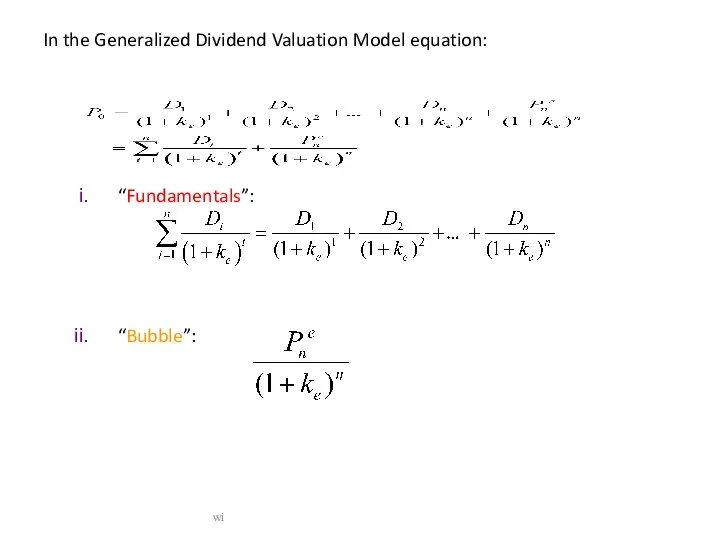

- 42. In the Generalized Dividend Valuation Model equation: “Fundamentals”: “Bubble”: wi

- 43. Implications of efficiency evidence very difficult for average person to beat the market trying to do

- 45. Скачать презентацию

© 2008 Pearson Education Canada

7.

Ch 7: Stock Markets and Efficient Market

7.

Ch 7: Stock Markets and Efficient Market

© 2008 Pearson Education Canada

7.

The Markets for Stocks. (*)

In Canada, stocks

7.

The Markets for Stocks. (*)

In Canada, stocks

Common Stock

Common stock is the principal way that corporations raise equity

Common Stock

Common stock is the principal way that corporations raise equity

Several Kinds of “Value”

There are several types of value, of which

Several Kinds of “Value”

There are several types of value, of which

9.1 Reading Stock Listings

The following newspaper stock listing is usually printed

9.1 Reading Stock Listings

The following newspaper stock listing is usually printed

Reading Stock Listings

Copyright © 2009 Pearson Education, Inc. Publishing as Prentice

Reading Stock Listings

Copyright © 2009 Pearson Education, Inc. Publishing as Prentice

Reading Stock Listings

Hi = 123 1/8: The highest price the stock

Reading Stock Listings

Hi = 123 1/8: The highest price the stock

Reading Stock Listings

Div = 4.84: The last quarterly dividend multiplied by

Reading Stock Listings

Div = 4.84: The last quarterly dividend multiplied by

Reading Stock Listings

Hi = 115: Highest share price of the day

Lo

Reading Stock Listings

Hi = 115: Highest share price of the day

Lo

© 2008 Pearson Education Canada

7.

The price of common stock. (*)

Common stocks

7.

The price of common stock. (*)

Common stocks

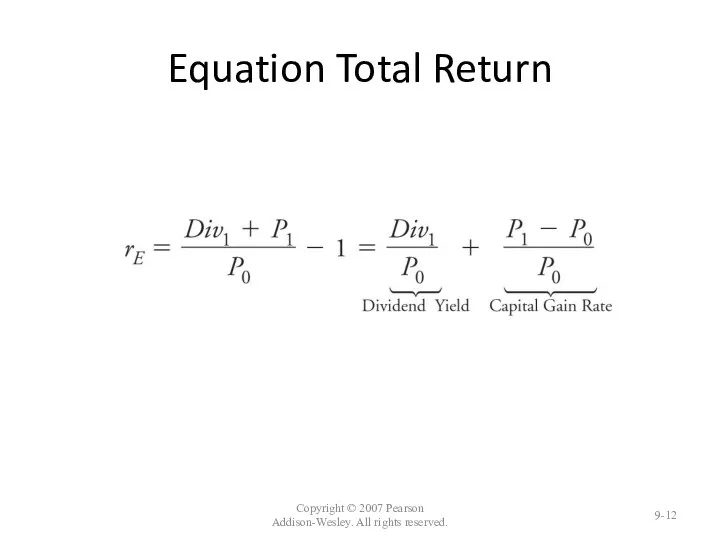

Equation Total Return

Copyright © 2007 Pearson Addison-Wesley. All rights reserved.

9-

Equation Total Return

Copyright © 2007 Pearson Addison-Wesley. All rights reserved.

9-

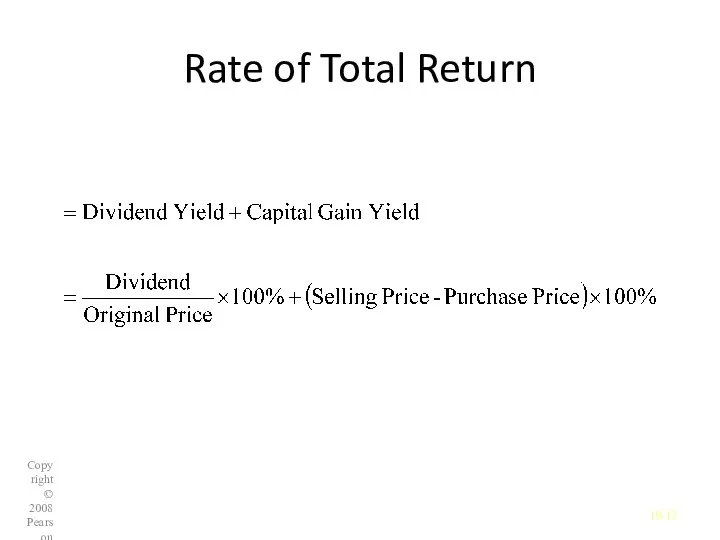

Rate of Total Return

Copyright © 2008 Pearson Education Canada

10-

Rate of Total Return

Copyright © 2008 Pearson Education Canada

10-

One-Period Valuation Model

© 2008 Pearson Education Canada

7.

One-Period Valuation Model

© 2008 Pearson Education Canada

7.

Generalized Dividend

Valuation Model

© 2008 Pearson Education Canada

7.

Generalized Dividend

Valuation Model

© 2008 Pearson Education Canada

7.

Gordon Growth Model

© 2008 Pearson Education Canada

7.

Gordon Growth Model

© 2008 Pearson Education Canada

7.

© 2008 Pearson Education Canada

7.

According to the above model, current stock

7.

According to the above model, current stock

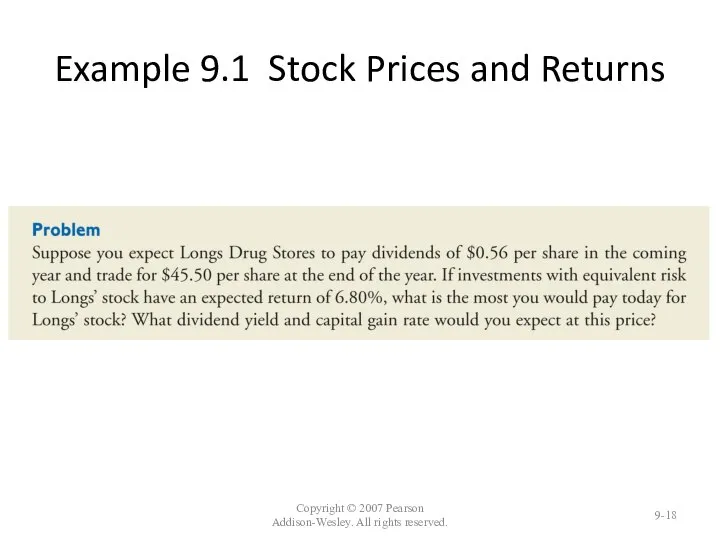

Example 9.1 Stock Prices and Returns

Copyright © 2007 Pearson Addison-Wesley. All

Example 9.1 Stock Prices and Returns

Copyright © 2007 Pearson Addison-Wesley. All

Example 9.1 Stock Prices and Returns

Copyright © 2007 Pearson Addison-Wesley. All

Example 9.1 Stock Prices and Returns

Copyright © 2007 Pearson Addison-Wesley. All

Example Valuing a Firm with Constant Dividend Growth

Copyright © 2007 Pearson

Example Valuing a Firm with Constant Dividend Growth

Copyright © 2007 Pearson

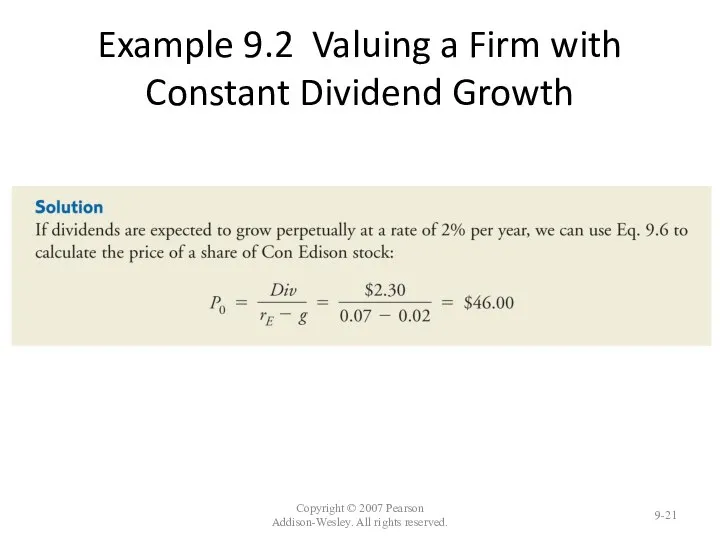

Example 9.2 Valuing a Firm with Constant Dividend Growth

Copyright © 2007

Example 9.2 Valuing a Firm with Constant Dividend Growth

Copyright © 2007

Factors Affecting Stock Prices

Business cycles

Interest rate changes

Investor sentiment about

Economy,

Earnings

And markets

Copyright ©

Factors Affecting Stock Prices

Business cycles

Interest rate changes

Investor sentiment about

Economy,

Earnings

And markets

Copyright ©

interest rate = risk free rate + risk premium, ke =

interest rate = risk free rate + risk premium, ke =

higher risk free rate, lower stock price

higher risk premium, lower stock

higher risk free rate, lower stock price

higher risk premium, lower stock

example

D = $2, g = 2%, rf = 3%, rp =

example

D = $2, g = 2%, rf = 3%, rp =

what if risk premium rises to 7%?

P = $2/(.03+.07-.02) = $2/.08

what if risk premium rises to 7%?

P = $2/(.03+.07-.02) = $2/.08

© 2008 Pearson Education Canada

7.

Gordon Model- Applications.

The effect of monetary policy.

The

7.

Gordon Model- Applications.

The effect of monetary policy.

The

© 2008 Pearson Education Canada

7.

Price-Earnings Ratio: The price/earnings ratio, which equals

7.

Price-Earnings Ratio: The price/earnings ratio, which equals

Price Earnings Valuation Method (Cont’d)

The PE ratio can be used to

Price Earnings Valuation Method (Cont’d)

The PE ratio can be used to

Stock Analysis

Fundamental analysis

Quantitative analysis

Based on financial statements

Qualitative analysis

More subjective

Examines management skill

Technical

Stock Analysis

Fundamental analysis

Quantitative analysis

Based on financial statements

Qualitative analysis

More subjective

Examines management skill

Technical

© 2008 Pearson Education Canada

7.

How the Market sets Stock Prices.

(a)Theory of

7.

How the Market sets Stock Prices.

(a)Theory of

© 2008 Pearson Education Canada

7.

Rational Expectations

Rational expectations theory views expectations as

7.

Rational Expectations

Rational expectations theory views expectations as

The Efficient Market

The efficient-market hypothesis (EMH) asserts that financial markets are

"informationally efficient", or that

The efficient-market hypothesis (EMH) asserts that financial markets are

"informationally efficient", or that

Implications of the Theory of Rational Expectations

Even though a rational expectation

Implications of the Theory of Rational Expectations

Even though a rational expectation

Implications

If there is a change in the way a variable moves,

Implications

If there is a change in the way a variable moves,

Efficient Markets: An Application of Rational Expectations

© 2008 Pearson Education

Efficient Markets: An Application of Rational Expectations

© 2008 Pearson Education

Implications of the EMH for the stock market: Investing in the

Implications of the EMH for the stock market: Investing in the

Evidence Against Market Efficiency

Small-firm effect

January Effect

Market Overreaction

Excessive Volatility

Mean Reversion

New information is

Evidence Against Market Efficiency

Small-firm effect

January Effect

Market Overreaction

Excessive Volatility

Mean Reversion

New information is

(b)Behavioural Finance.

The lack of short selling (causing

over-priced stocks) may be

(b)Behavioural Finance.

The lack of short selling (causing over-priced stocks) may be

(b) Behavioural Finance.

Behavioral economists attribute the imperfections in financial markets

to a

(b) Behavioural Finance.

Behavioral economists attribute the imperfections in financial markets

to a

Bubbles

Large gaps between actual asset price and fundamental value

Internet stock bubble

Bubbles

Large gaps between actual asset price and fundamental value

Internet stock bubble

In the Generalized Dividend Valuation Model equation:

“Fundamentals”:

“Bubble”:

wi

In the Generalized Dividend Valuation Model equation:

“Fundamentals”:

“Bubble”:

wi

Implications of efficiency evidence

very difficult for average person to beat the

Implications of efficiency evidence

very difficult for average person to beat the

Ընդհանուր պատկերացումներ տնտեսության մասին

Ընդհանուր պատկերացումներ տնտեսության մասին Елдердің экономикалық көшбасшылары. Елдер түрлері: орталық, жартылай перифериялы, перифериялы. Географиялық орталықтар

Елдердің экономикалық көшбасшылары. Елдер түрлері: орталық, жартылай перифериялы, перифериялы. Географиялық орталықтар Актуальные вопросы туризма в России

Актуальные вопросы туризма в России Квалиметрия. Техника применения экспертного метода измерения качества продукции

Квалиметрия. Техника применения экспертного метода измерения качества продукции Политические институты и экономические результаты

Политические институты и экономические результаты Безработица. Типы и формы безработицы

Безработица. Типы и формы безработицы Экономикалық теорияның пәні және әдістері

Экономикалық теорияның пәні және әдістері История становления предпринимательства в России

История становления предпринимательства в России Пятиэтапная модель Роберта Гранта. GAP-анализ

Пятиэтапная модель Роберта Гранта. GAP-анализ Малиновский район міста Одеси. Слайды

Малиновский район міста Одеси. Слайды Содержание дисциплины Экономика и ее задачи

Содержание дисциплины Экономика и ее задачи Роль иностранного капитала в экономике России XIX-XX веков

Роль иностранного капитала в экономике России XIX-XX веков Мировое хозяйство и международная торговля

Мировое хозяйство и международная торговля Экономика - искусство ведения хозяйства

Экономика - искусство ведения хозяйства Типы экономических систем

Типы экономических систем Внешнеэкономическая деятельность Торгово-промышленной палаты Российской Федерации

Внешнеэкономическая деятельность Торгово-промышленной палаты Российской Федерации Основи аналізу попиту

Основи аналізу попиту Customer behavior specifics in the access economy: comparison of Russian and Italian carsharing customers

Customer behavior specifics in the access economy: comparison of Russian and Italian carsharing customers Презентация Таможенная политика в период складывания единого централизованного государства.

Презентация Таможенная политика в период складывания единого централизованного государства. Планирование производственных процессов и определение состава машинно-тракторного парка в ООО «Милославский ячмень»

Планирование производственных процессов и определение состава машинно-тракторного парка в ООО «Милославский ячмень» Еколого-економічне обґрунтування структури угідь та організації сівозмін фермерського господарства

Еколого-економічне обґрунтування структури угідь та організації сівозмін фермерського господарства Поддорское сельское поселение. Проект поддержки местных инициатив

Поддорское сельское поселение. Проект поддержки местных инициатив Организационная структура отрасли «торговля»

Организационная структура отрасли «торговля» Рынки факторов производства Цель: изучить специфику факторных рынков

Рынки факторов производства Цель: изучить специфику факторных рынков ВТО

ВТО Процедура взаимодействия СК с поставщиками по сервису (Мониторинг KPI и производственный аудит)

Процедура взаимодействия СК с поставщиками по сервису (Мониторинг KPI и производственный аудит) Нарықтық экономикалық жүйе және нарықтық механизм

Нарықтық экономикалық жүйе және нарықтық механизм Анализ региона: Юго-Восточная Азия

Анализ региона: Юго-Восточная Азия