- Financial planning

Содержание

- 2. Plan of the day Today we will see financial planning and the time value of money.

- 3. Financial Planning The class on financial statements served to understand how a firm is working from

- 4. The Financial Planning Process Financial planning is a dynamic process that follows a cycle of making

- 5. The Financial Planning Process A key factor in setting the strategy and the financial play is

- 6. The Financial Planning Process The financial planning horizon may be broken down into several steps: There

- 7. The Financial Planning Process – Remarks Some variables must be forecast well in advance because exploitation

- 8. The Financial Planning Process – Remarks A plan should always lead to decisions that justify the

- 9. Financial planning – an example Consider the following example of a fictional company called GPC. Let

- 10. Financial planning – Example: Income statement Financial Planning (Nearest $ Million) Year xxx0 xxx1 xxx2 xxx3

- 11. Financial planning – Example: balance sheet Financial Planning

- 12. Financial planning – Steps How can we prepare the financial plan for the next year? The

- 13. Financial planning – First step Which items in the income statement / balance sheet have maintained

- 14. Financial planning – First step Financial Planning

- 15. Financial planning – First step: combining tables Financial Planning GPC Financial Statements, Years xxx1 - xxx3

- 16. Financial planning – First step We compare everything to sales since sales represents the outcome of

- 17. Financial planning – Second and third step The second step is to forecast sales itself. We

- 18. Financial planning – Second and third step Note that there are still some numbers missing. Financial

- 19. Financial planning – Second and third step Note that there are still some numbers missing. Financial

- 20. Financial planning – Fourth step: completing the income statement We need to fill in the missing

- 21. Financial planning – Fourth step: completed income statement Financial Planning

- 22. Financial planning – Fourth step: completing the balance sheet We have obtained the change in the

- 23. Financial planning – Fourth step: completed the balance sheet Financial Planning

- 24. Can we do the same exercise with a real firm? Here are some relevant numbers of

- 25. Can we do the same exercise with a real firm? First step: we compare all items

- 26. Can we do the same exercise with a real firm? Obviously, here the number are not

- 27. Can we do the same exercise with a real firm? Fixed ratios? Financial Planning

- 28. Can we do the same exercise with a real firm? Fixed ratios? As commented before, total

- 29. Can we do the same exercise with a real firm? Financial Planning

- 30. Can we do the same exercise with a real firm? The next step is about finding

- 31. Can we do the same exercise with a real firm? Financial Planning

- 32. Can we do the same exercise with a real firm? What about the balance sheet? We

- 33. Can we do the same exercise with a real firm? Hence, it seems that before liabilities

- 34. Can we do the same exercise with a real firm? Financial Planning

- 35. Assignment 2 Choose any company that has on its website the data (balance sheet and income

- 36. Assignment 2 Choose wisely the company as you may need to come up with assumptions as

- 37. Growth and need for external finance In the previous example we have seen that if the

- 38. Growth and need for external finance Then, EBIT refers to earnings before interest and taxes and

- 39. Growth and need for external finance Using this formula we can calculate the external funding rate

- 40. Growth and need for external finance Hence, the more the firm wants to grow, the more

- 41. Sustainable rate of growth The sustainable growth rate is a measure of how much a firm

- 42. Sustainable rate of growth There is an easy formula to calculate sustainable growth: Sustainable Rate of

- 43. Working Capital Management An important part of financial planning and management is working capital management. In

- 44. Working Capital Management There is a problem if you have to pay a lot and for

- 45. Efficient Management of Working Capital Principle: Minimize the investment in non-earning assets such as receivables and

- 46. Working Capital Management The longer the working capital cycle is, the longer a business is tying

- 47. Working Capital Management: Cash cycle One way to consider if working capital management is efficient is

- 48. Working Capital Management – Real Madrid FC Proper working capital management is important for sport clubs

- 49. Cash budgeting (This section builds heavily on the chapter about working capital in Brealey – Myers:

- 50. Cash budgeting The financial plan sets out a strategy for investing cash surpluses or financing any

- 51. Cash budgeting This proportion depends on the lags with which customers pay their bills. For example,

- 52. Cash budgeting – Sources of cash The general formula is Ending accounts receivable = beginning accounts

- 53. Cash budgeting The second section of the table shows how Dynamic expects to use cash. We

- 54. Cash budgeting – Uses of cash Some details. 1. Payments of accounts payable. Dynamic has to

- 55. Cash budgeting – Cash balance The forecast net inflow of cash (sources minus uses) is shown

- 56. Cash budgeting – Cash balance Dynamic starts the year with $5 million in cash. There is

- 57. Cash budgeting – Cash balance Some remarks. The large cash outflows in the first two quarters

- 58. Cash budgeting – Short-term financing plan Our next step will be to develop a short-term financing

- 59. Cash budgeting – Short-term financing plan Alternatively, Dynamic can borrow up to $40 million from the

- 60. Cash budgeting – Short-term financing plan Financial Planning

- 61. Cash budgeting – Short-term financing plan In the first quarter the plan calls for borrowing the

- 62. Cash budgeting – Evaluation of the plan Does the plan solve Dynamic’s short-term financing problem? The

- 63. Cash budgeting – Evaluation of the plan 4. Should Dynamic try to arrange long-term financing for

- 64. Cash budgeting – Evaluation of the plan 4. Should Dynamic try to arrange long-term financing for

- 65. Cash budgeting – Sources of Short-Term Financing: Bank loans Let us briefly consider alternative ways of

- 66. Cash budgeting – Sources of Short-Term Financing: Bank loans However, banks also make term loans, which

- 67. Cash budgeting – Sources of Short-Term Financing: Commercial Papers Commercial papers When banks lend money, they

- 68. Cash budgeting – Sources of Short-Term Financing: Secured loans Secured loans Many short-term loans are unsecured,

- 69. Conclusion – Financial planning Hopefully, after this lesson you are convinced about the importance of financial

- 70. Introduction – The time value of money $20 today is worth more than the expectation of

- 71. Look how $100 grows over time at different interest rates. Small differences in the interest rate

- 72. Here I decompose the earned interests. The Time Value of Money

- 73. The Time Value of Money The sale of Manhattan Island According to a myth in American

- 74. Compounding has a very important consequence. 1/(1+i)n is called the discount factor. If you have any

- 75. The Time Value of Money

- 76. In 1995 Coca-Cola Enterprises needed to borrow about a quarter of a billion dollars for 25

- 77. Similarly, if you know FV and PV, then you can calculate the interest rate. Example: If

- 78. Cash flows Generally, not only one payment is made, but a stream of cash flows. We

- 79. Cash flows – an example Suppose that the interest rate is 8%. An auto dealer gives

- 80. Level cash flows There are cash flows that feature very regular payments. For example, a home

- 81. Annuity Annuity is a sequence of equally spaced identical cash flows. We will use the following

- 82. The present value of an annuity How much would you pay for a cash flow that

- 83. Substract from line 4 line 2 1-1/(1+i)n is called the annuity factor. Annuity

- 84. Annuities example 1: Suppose that you want to buy a house and know that you will

- 85. Annuities example 2: Suppose that you want to buy a house and need $450000. You want

- 86. How much of the monthly payments is used to pay interest on the loan and how

- 87. The retirement example Let’s see how we can use knowing how „famous” cash flows are calculated

- 88. Target replacement rate of pre-retirement income First compute the retirement income. Many experts recommend a rate

- 89. Target replacement rate of pre-retirement income Next compute how much you need to save each year.

- 90. Target replacement rate of pre-retirement income Thus, we have To obtain a real $22,500 for the

- 91. Maintain the same level of consumption spending Assume that your level of real consumption is c.

- 92. Taking care of inflation Generally, prices and rates are nominal, that is they are expressed in

- 93. Taking care of inflation What is the real rate of interest if the nominal rate is

- 94. Evaluating investment opportunities We can use discounted cash flow analysis to make decisions such as: Whether

- 95. Example: NPV of a project when discount rate is 10% This project should be carried out.

- 96. Example: NPV of a project when discount rate is 15% We consider the same project, but

- 97. Example: NPV of a project and the internal rate of return The higher the discount rate,

- 98. NPV and the internal rate of return From the previous example we can conclude the following:

- 99. Example (taken from Brealey-Myers): Obsolete Technologies is considering the purchase of a new computer system to

- 100. Example (taken from Brealey-Myers): Therefore, the net present value is -$50000+$69740=$19740. It has a positive NPV,

- 101. Mutually exclusive projects We speak about mutually exclusive projects if there are two or more projects

- 102. Mutually exclusive projects - example You are offered two competing softwares to use in your firm

- 103. Mutually exclusive projects - example Both systems yield a positive net present value, but given the

- 104. Investment timing We return to Obsolete Technologies that was contemplating the purchase of a new computer

- 105. Investment timing Which year should Obsolete buy the new system? You can see that the cost

- 106. Investment timing Isn’t a gain of $25,000 better than one of $20,000? Well, not necessarily—you may

- 107. Investment timing If you postpone from Year 3 to Year 4, the gain rises from $34,000

- 109. Скачать презентацию

Plan of the day

Today we will see financial planning and the

Plan of the day

Today we will see financial planning and the

Financial Planning

The class on financial statements served to understand how a

Financial Planning

The class on financial statements served to understand how a

The Financial Planning Process

Financial planning is a dynamic process that follows

The Financial Planning Process

Financial planning is a dynamic process that follows

The Financial Planning Process

A key factor in setting the strategy and

The Financial Planning Process

A key factor in setting the strategy and

The Financial Planning Process

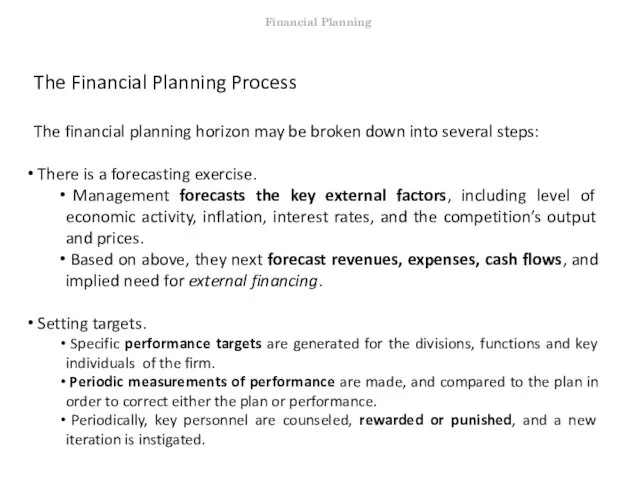

The financial planning horizon may be broken down

The Financial Planning Process

The financial planning horizon may be broken down

The Financial Planning Process – Remarks

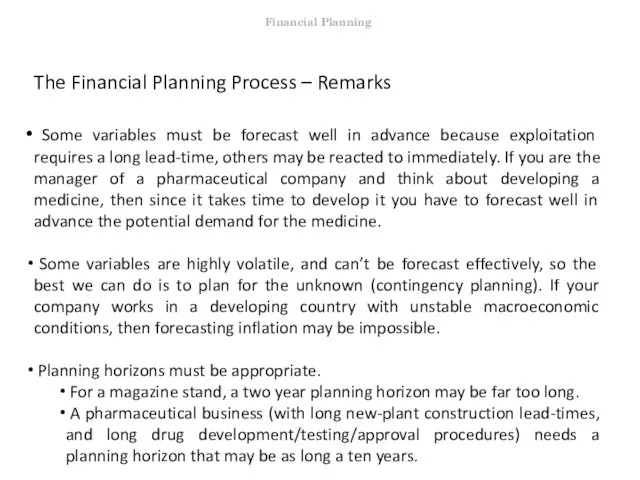

Some variables must be forecast

The Financial Planning Process – Remarks

Some variables must be forecast

The Financial Planning Process – Remarks

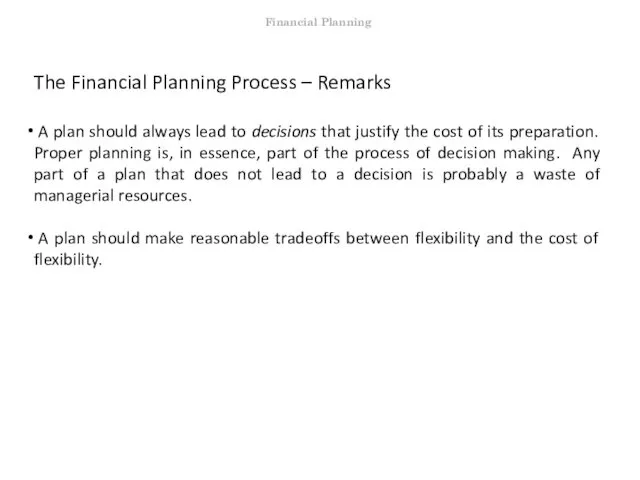

A plan should always lead

The Financial Planning Process – Remarks

A plan should always lead

Financial planning – an example

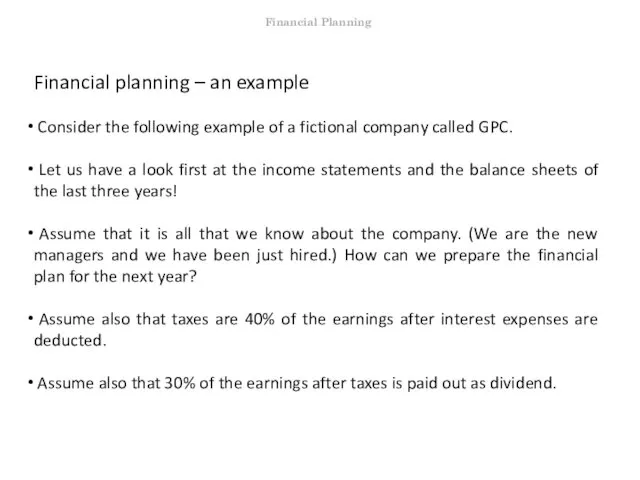

Consider the following example of a

Financial planning – an example

Consider the following example of a

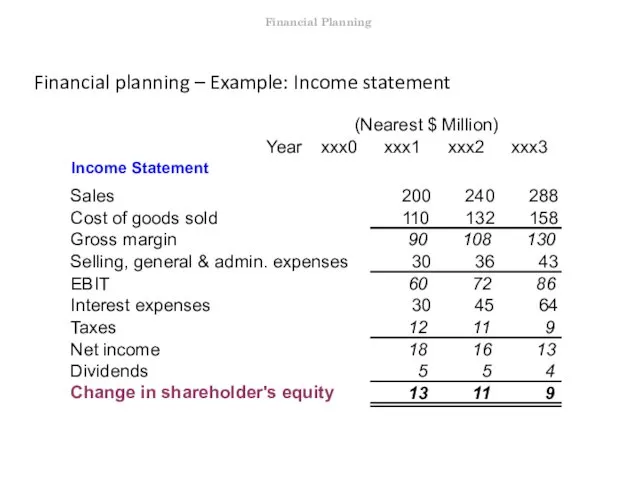

Financial planning – Example: Income statement

Financial Planning

(Nearest $ Million)

Financial planning – Example: Income statement

Financial Planning

(Nearest $ Million)

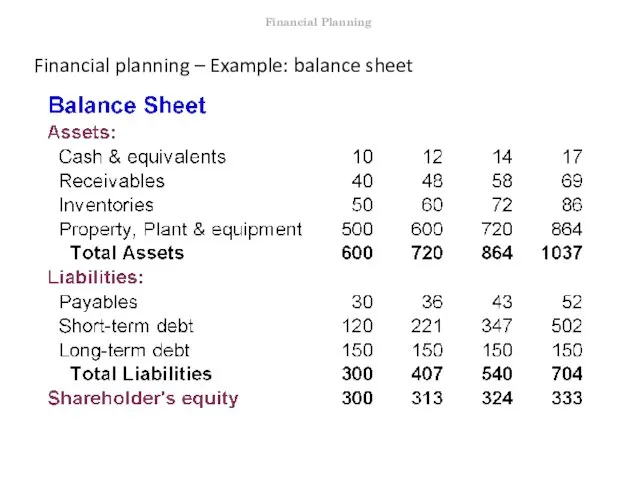

Financial planning – Example: balance sheet

Financial Planning

Financial planning – Example: balance sheet

Financial Planning

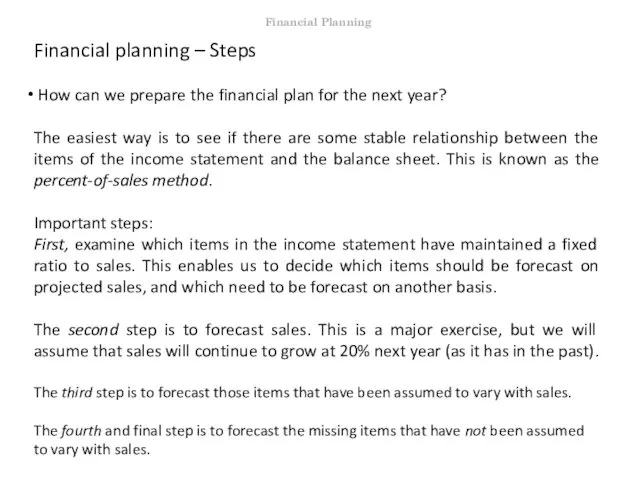

Financial planning – Steps

How can we prepare the financial plan

Financial planning – Steps

How can we prepare the financial plan

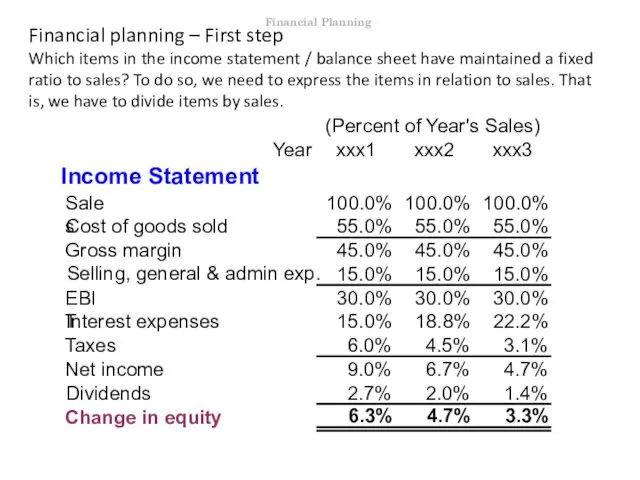

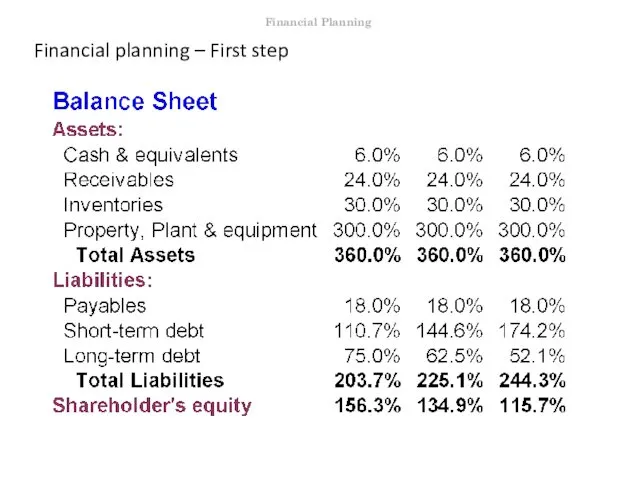

Financial planning – First step

Which items in the income statement /

Financial planning – First step

Which items in the income statement /

Financial planning – First step

Financial Planning

Financial planning – First step

Financial Planning

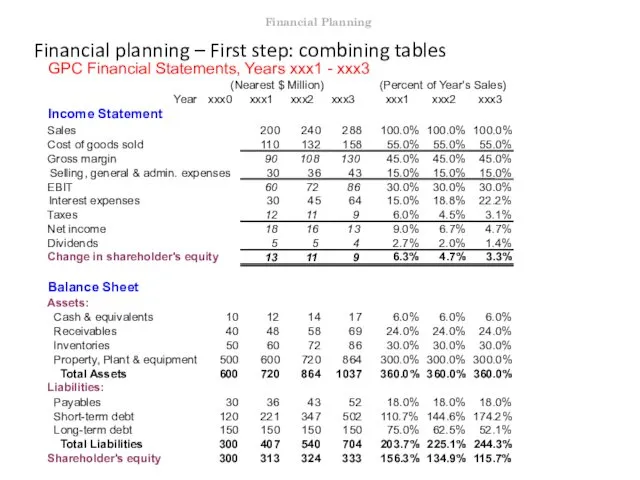

Financial planning – First step: combining tables

Financial Planning

GPC Financial Statements,

Financial planning – First step: combining tables

Financial Planning

GPC Financial Statements,

Financial planning – First step

We compare everything to sales since

Financial planning – First step

We compare everything to sales since

Financial planning – Second and third step

The second step is to

Financial planning – Second and third step

The second step is to

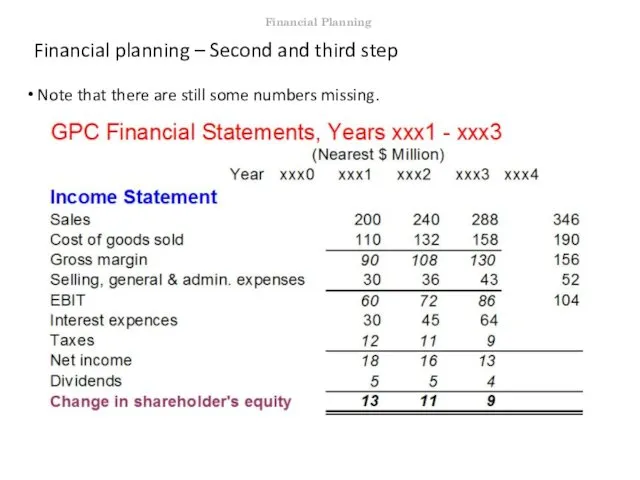

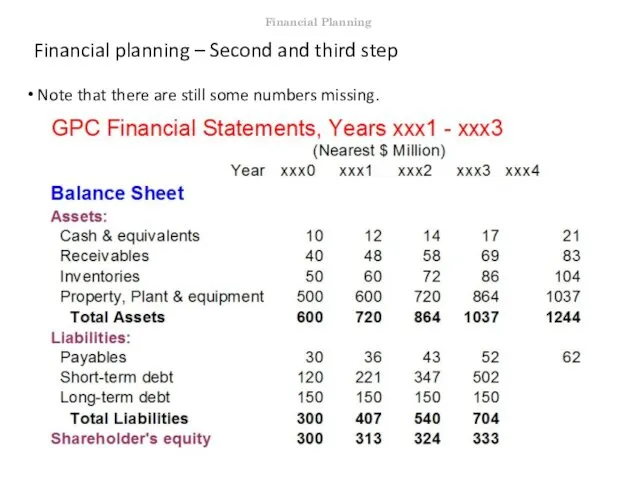

Financial planning – Second and third step

Note that there are

Financial planning – Second and third step

Note that there are

Financial planning – Second and third step

Note that there are

Financial planning – Second and third step

Note that there are

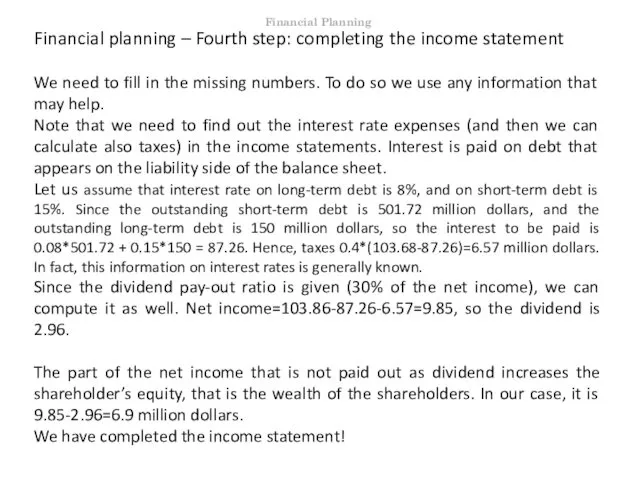

Financial planning – Fourth step: completing the income statement

We need to

Financial planning – Fourth step: completing the income statement

We need to

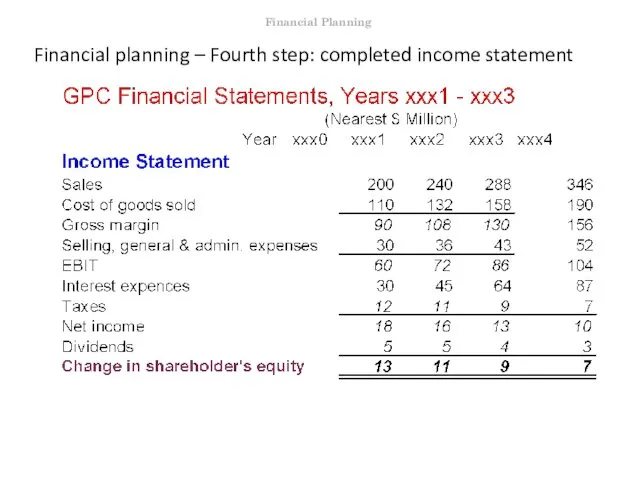

Financial planning – Fourth step: completed income statement

Financial Planning

Financial planning – Fourth step: completed income statement

Financial Planning

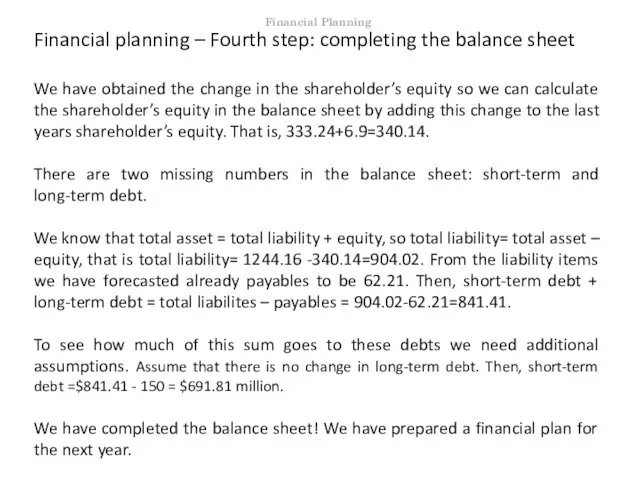

Financial planning – Fourth step: completing the balance sheet

We have obtained

Financial planning – Fourth step: completing the balance sheet

We have obtained

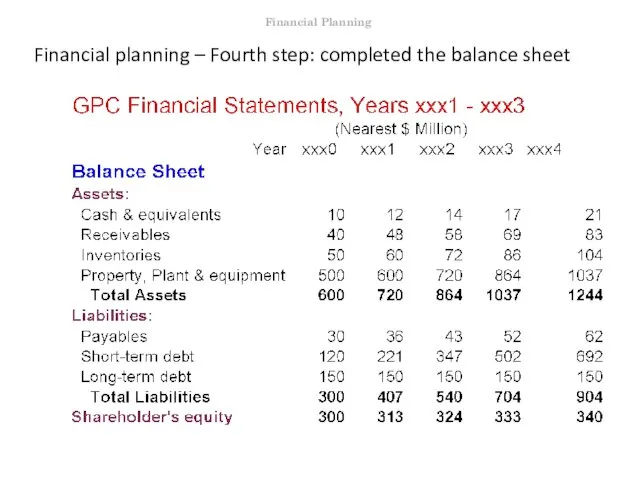

Financial planning – Fourth step: completed the balance sheet

Financial Planning

Financial planning – Fourth step: completed the balance sheet

Financial Planning

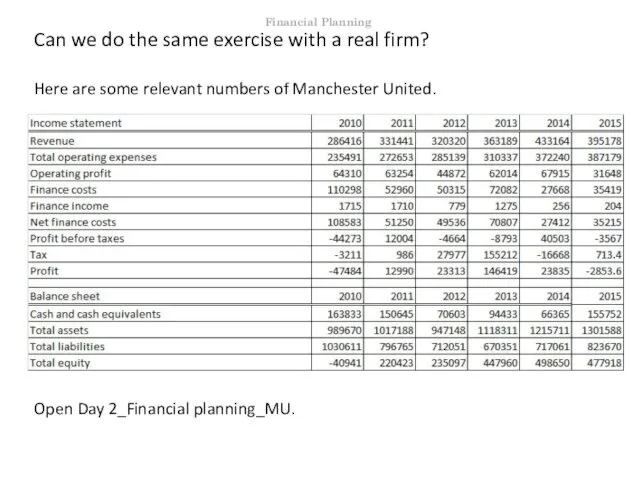

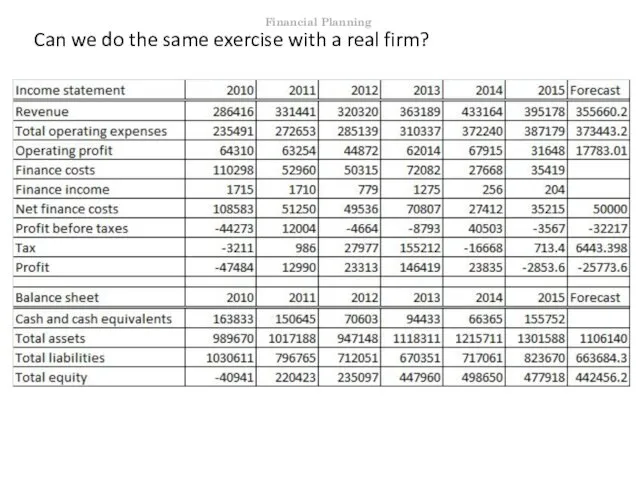

Can we do the same exercise with a real firm?

Here are

Can we do the same exercise with a real firm?

Here are

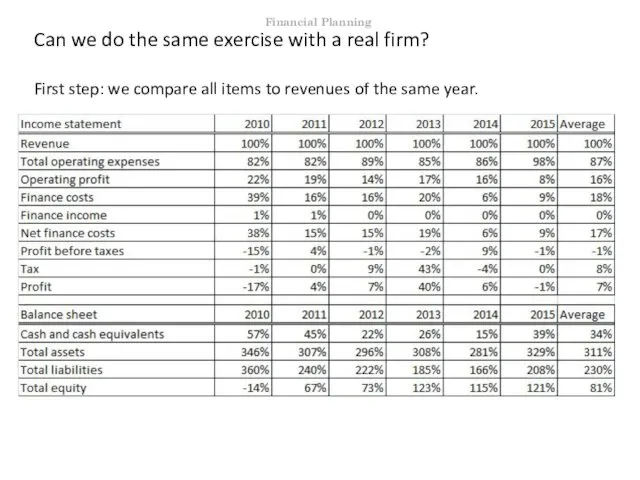

Can we do the same exercise with a real firm?

First step:

Can we do the same exercise with a real firm?

First step:

Can we do the same exercise with a real firm?

Obviously, here

Can we do the same exercise with a real firm?

Obviously, here

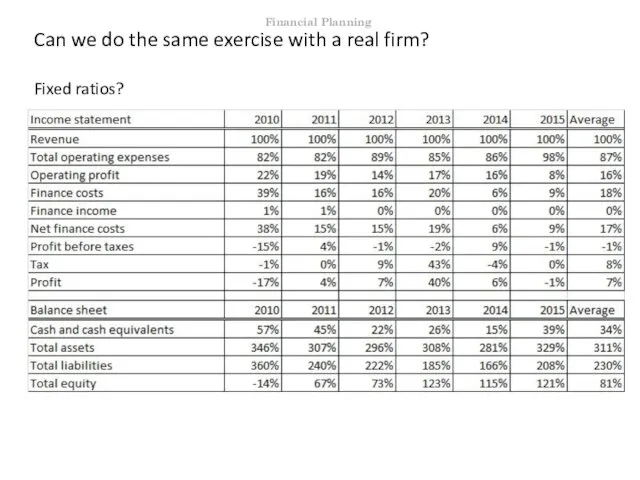

Can we do the same exercise with a real firm?

Fixed ratios?

Financial

Can we do the same exercise with a real firm?

Fixed ratios?

Financial

Can we do the same exercise with a real firm?

Fixed ratios?

As

Can we do the same exercise with a real firm?

Fixed ratios?

As

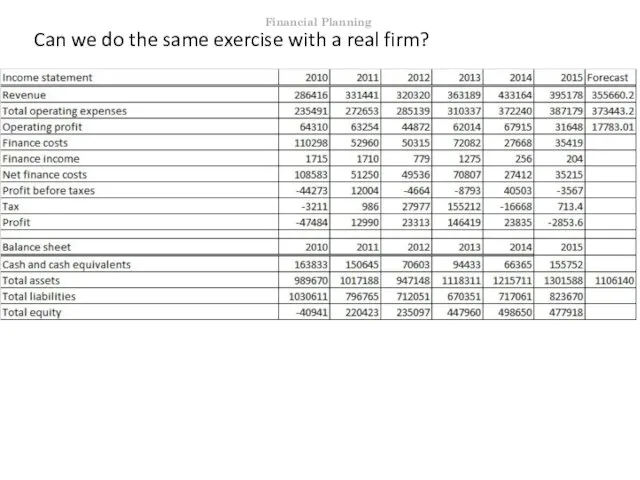

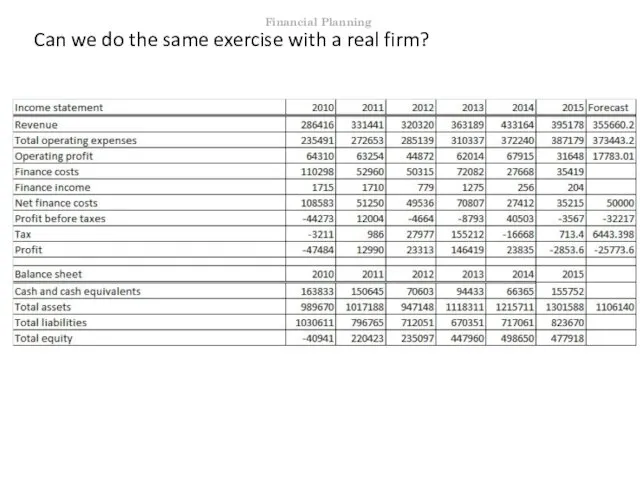

Can we do the same exercise with a real firm?

Financial Planning

Can we do the same exercise with a real firm?

Financial Planning

Can we do the same exercise with a real firm?

The next

Can we do the same exercise with a real firm?

The next

Can we do the same exercise with a real firm?

Financial Planning

Can we do the same exercise with a real firm?

Financial Planning

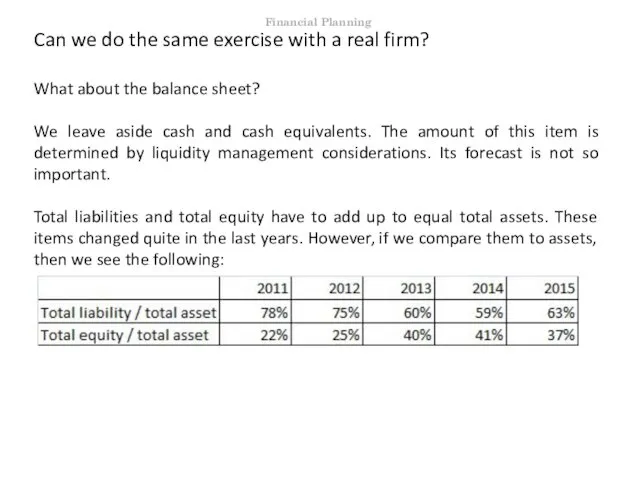

Can we do the same exercise with a real firm?

What about

Can we do the same exercise with a real firm?

What about

Can we do the same exercise with a real firm?

Hence, it

Can we do the same exercise with a real firm?

Hence, it

Can we do the same exercise with a real firm?

Financial Planning

Can we do the same exercise with a real firm?

Financial Planning

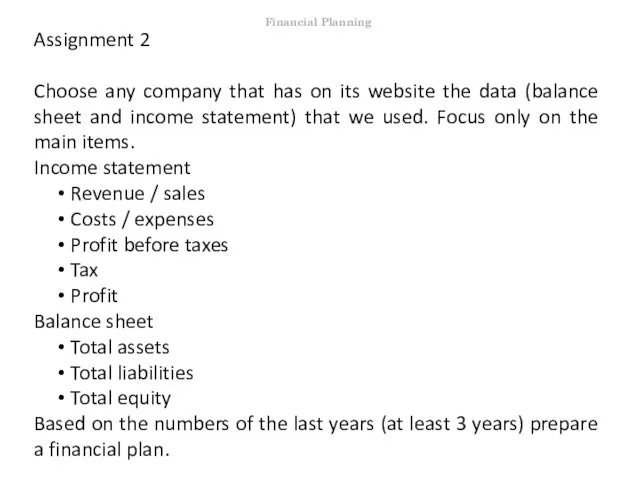

Assignment 2

Choose any company that has on its website the data

Assignment 2

Choose any company that has on its website the data

Assignment 2

Choose wisely the company as you may need to come

Assignment 2

Choose wisely the company as you may need to come

Growth and need for external finance

In the previous example we have

Growth and need for external finance

In the previous example we have

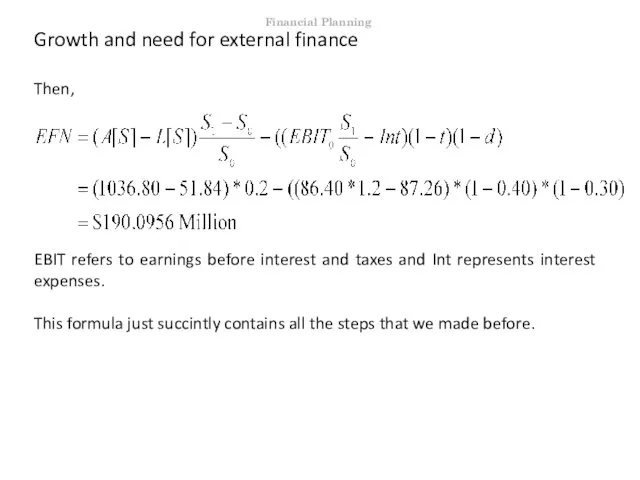

Growth and need for external finance

Then,

EBIT refers to earnings before

Growth and need for external finance

Then,

EBIT refers to earnings before

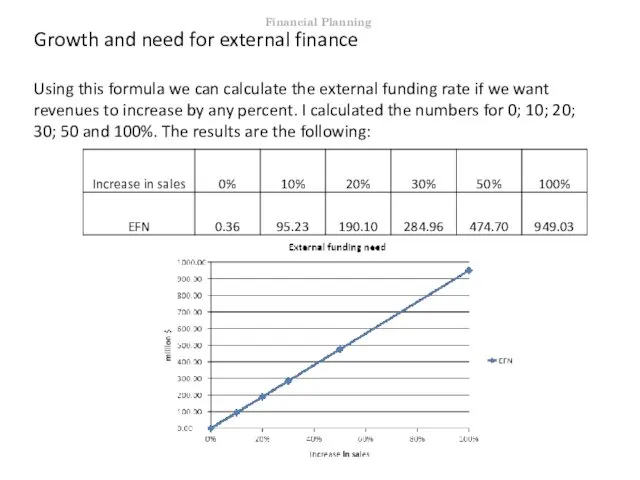

Growth and need for external finance

Using this formula we can calculate

Growth and need for external finance

Using this formula we can calculate

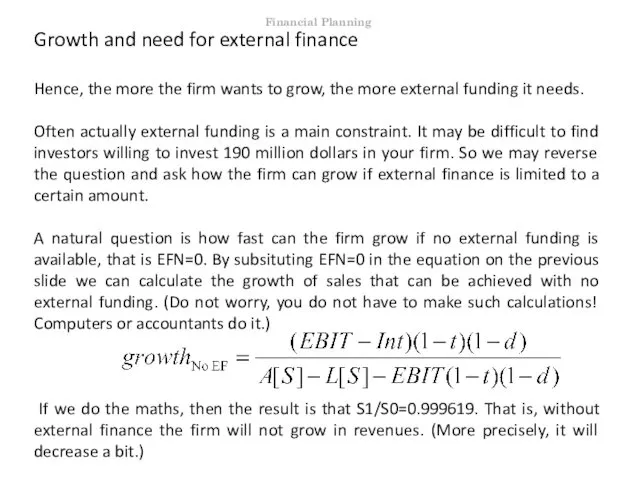

Growth and need for external finance

Hence, the more the firm wants

Growth and need for external finance

Hence, the more the firm wants

Sustainable rate of growth

The sustainable growth rate is a measure of

Sustainable rate of growth

The sustainable growth rate is a measure of

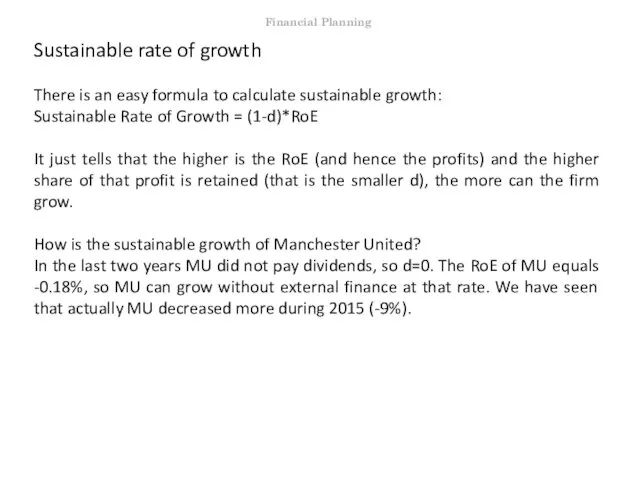

Sustainable rate of growth

There is an easy formula to calculate sustainable

Sustainable rate of growth

There is an easy formula to calculate sustainable

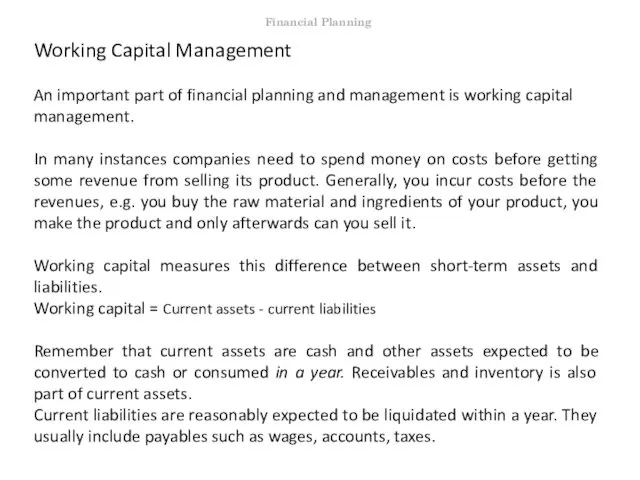

Working Capital Management

An important part of financial planning and management is

Working Capital Management

An important part of financial planning and management is

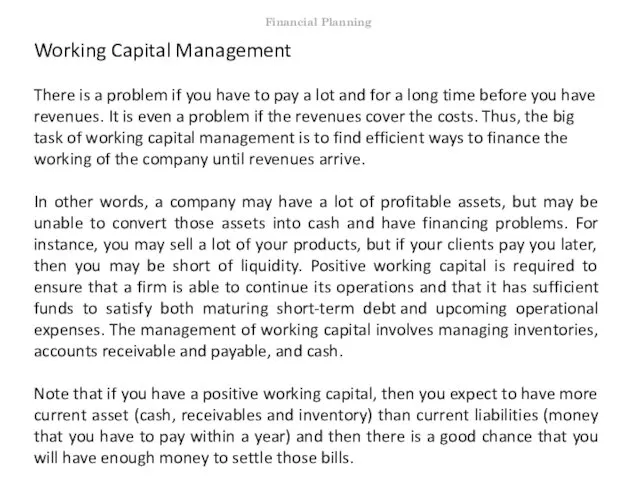

Working Capital Management

There is a problem if you have to pay

Working Capital Management

There is a problem if you have to pay

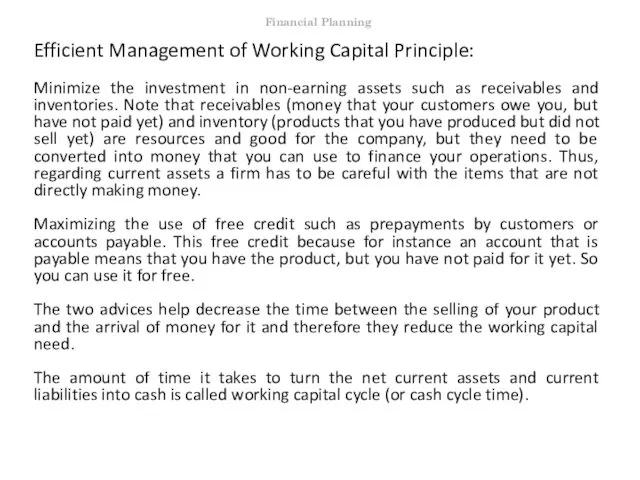

Efficient Management of Working Capital Principle:

Minimize the investment in non-earning assets

Efficient Management of Working Capital Principle:

Minimize the investment in non-earning assets

Working Capital Management

The longer the working capital cycle is, the longer

Working Capital Management

The longer the working capital cycle is, the longer

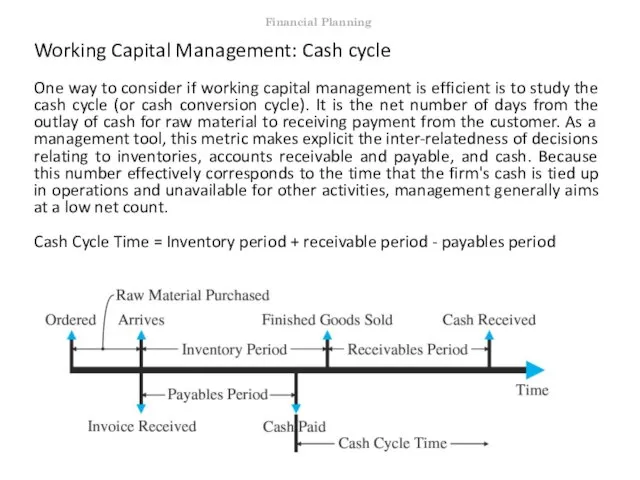

Working Capital Management: Cash cycle

One way to consider if working capital

Working Capital Management: Cash cycle

One way to consider if working capital

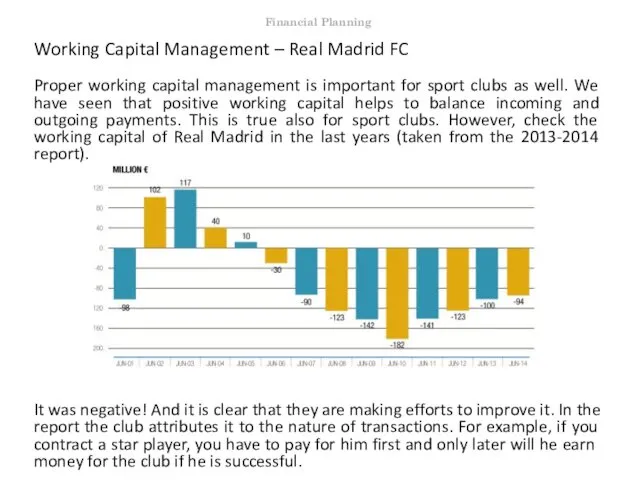

Working Capital Management – Real Madrid FC

Proper working capital management is

Working Capital Management – Real Madrid FC

Proper working capital management is

Cash budgeting

(This section builds heavily on the chapter about working capital

Cash budgeting

(This section builds heavily on the chapter about working capital

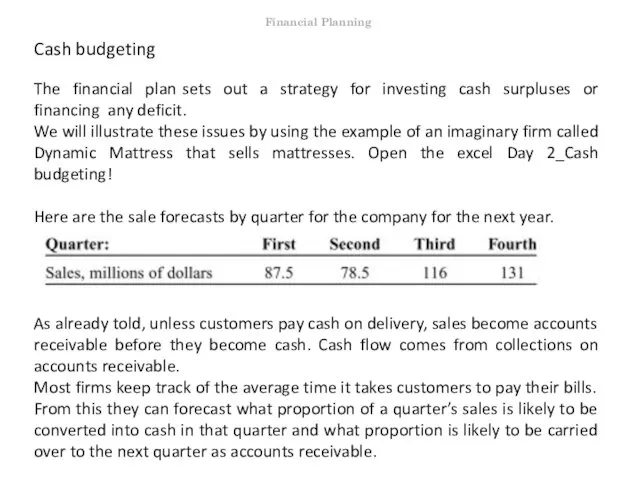

Cash budgeting

The financial plan sets out a strategy for investing cash

Cash budgeting

The financial plan sets out a strategy for investing cash

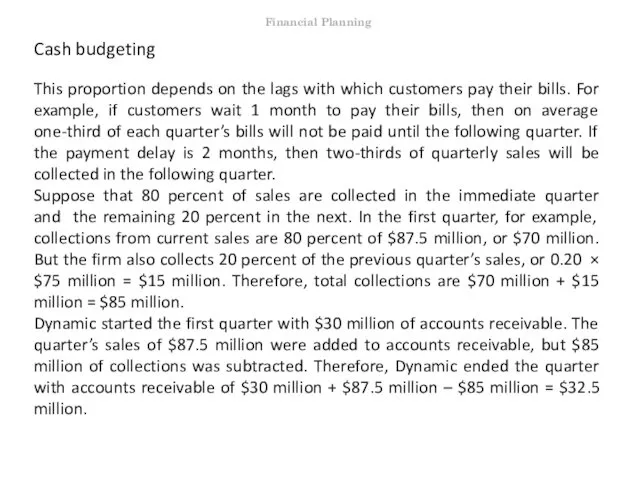

Cash budgeting

This proportion depends on the lags with which customers pay

Cash budgeting

This proportion depends on the lags with which customers pay

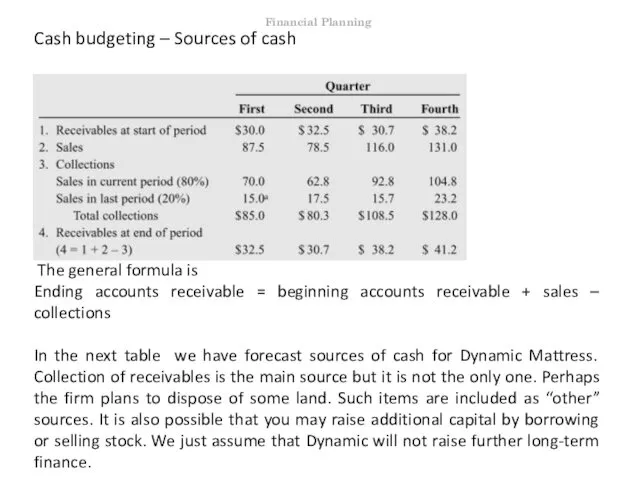

Cash budgeting – Sources of cash

The general formula is

Ending accounts receivable

Cash budgeting – Sources of cash

The general formula is

Ending accounts receivable

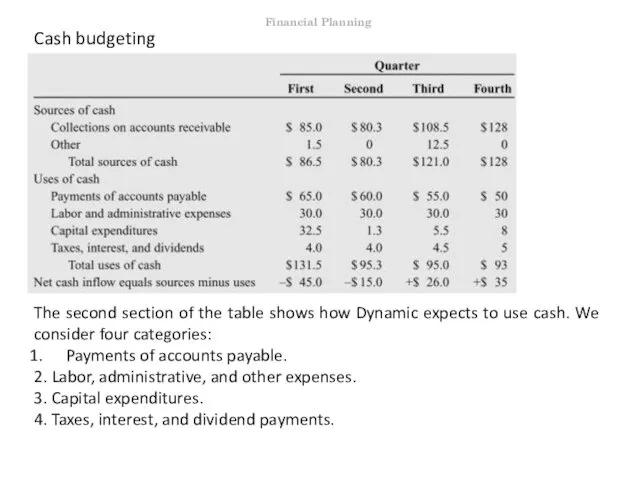

Cash budgeting

The second section of the table shows how Dynamic expects

Cash budgeting

The second section of the table shows how Dynamic expects

Cash budgeting – Uses of cash

Some details.

1. Payments of accounts payable.

Cash budgeting – Uses of cash

Some details.

1. Payments of accounts payable.

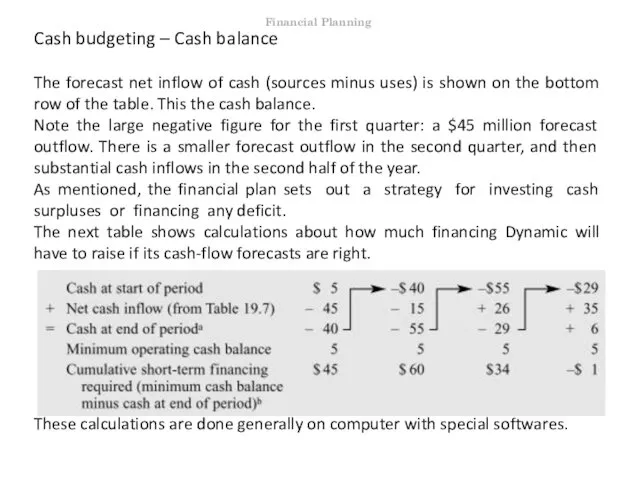

Cash budgeting – Cash balance

The forecast net inflow of cash (sources

Cash budgeting – Cash balance

The forecast net inflow of cash (sources

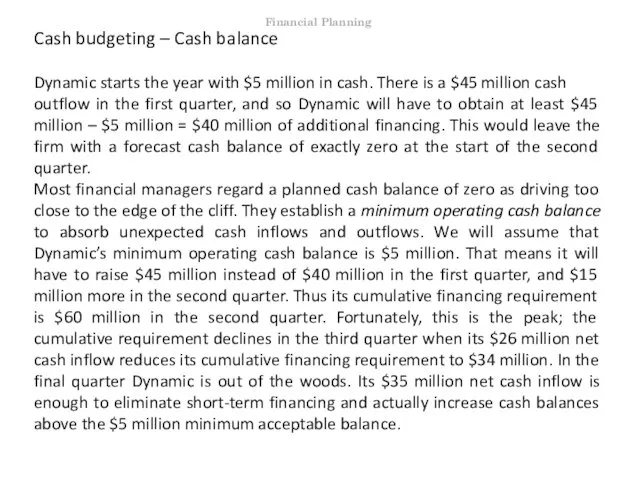

Cash budgeting – Cash balance

Dynamic starts the year with $5 million

Cash budgeting – Cash balance

Dynamic starts the year with $5 million

Cash budgeting – Cash balance

Some remarks.

The large cash outflows in

Cash budgeting – Cash balance

Some remarks.

The large cash outflows in

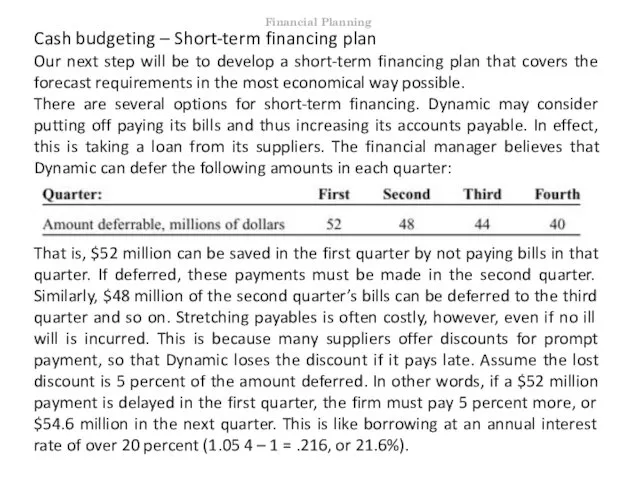

Cash budgeting – Short-term financing plan

Our next step will be to

Cash budgeting – Short-term financing plan

Our next step will be to

Cash budgeting – Short-term financing plan

Alternatively, Dynamic can borrow up to

Cash budgeting – Short-term financing plan

Alternatively, Dynamic can borrow up to

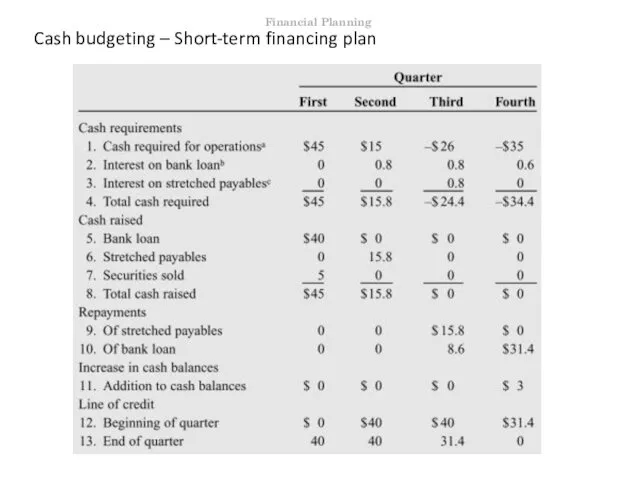

Cash budgeting – Short-term financing plan

Financial Planning

Cash budgeting – Short-term financing plan

Financial Planning

Cash budgeting – Short-term financing plan

In the first quarter the plan

Cash budgeting – Short-term financing plan

In the first quarter the plan

Cash budgeting – Evaluation of the plan

Does the plan solve Dynamic’s

Cash budgeting – Evaluation of the plan

Does the plan solve Dynamic’s

Cash budgeting – Evaluation of the plan

4. Should Dynamic try to

Cash budgeting – Evaluation of the plan

4. Should Dynamic try to

Cash budgeting – Evaluation of the plan

4. Should Dynamic try to

Cash budgeting – Evaluation of the plan

4. Should Dynamic try to

Cash budgeting – Sources of Short-Term Financing: Bank loans

Let us briefly

Cash budgeting – Sources of Short-Term Financing: Bank loans

Let us briefly

Cash budgeting – Sources of Short-Term Financing: Bank loans

However, banks also

Cash budgeting – Sources of Short-Term Financing: Bank loans

However, banks also

Cash budgeting – Sources of Short-Term Financing: Commercial Papers

Commercial papers

When banks

Cash budgeting – Sources of Short-Term Financing: Commercial Papers

Commercial papers

When banks

Cash budgeting – Sources of Short-Term Financing: Secured loans

Secured loans

Many short-term

Cash budgeting – Sources of Short-Term Financing: Secured loans

Secured loans

Many short-term

Conclusion – Financial planning

Hopefully, after this lesson you are convinced about

Conclusion – Financial planning

Hopefully, after this lesson you are convinced about

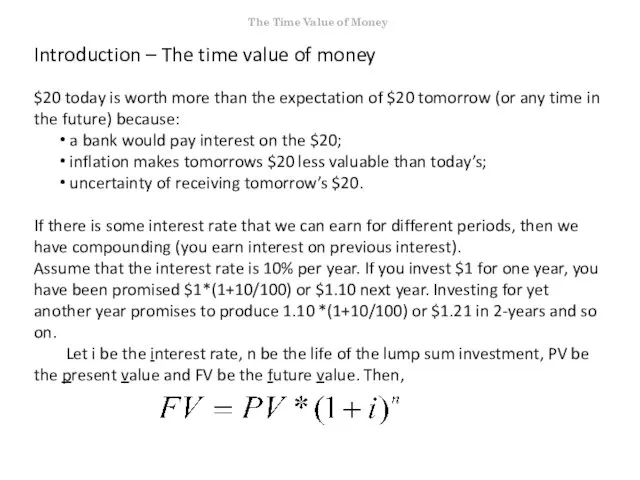

Introduction – The time value of money

$20 today is worth more

Introduction – The time value of money

$20 today is worth more

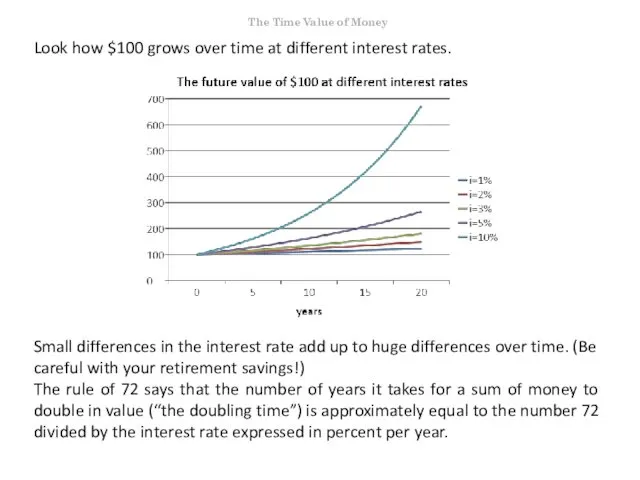

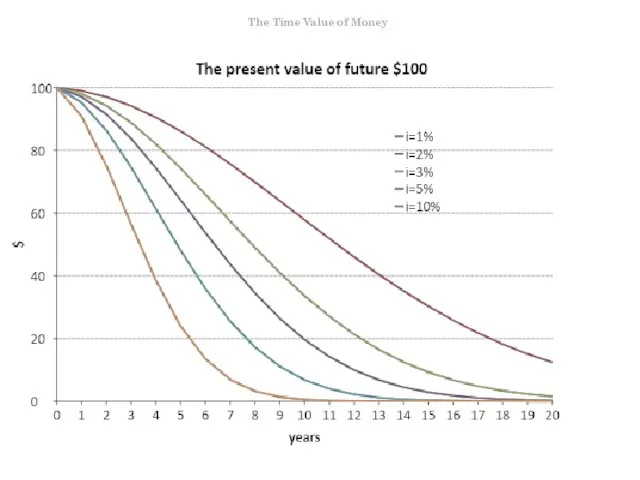

Look how $100 grows over time at different interest rates.

Small differences

Look how $100 grows over time at different interest rates.

Small differences

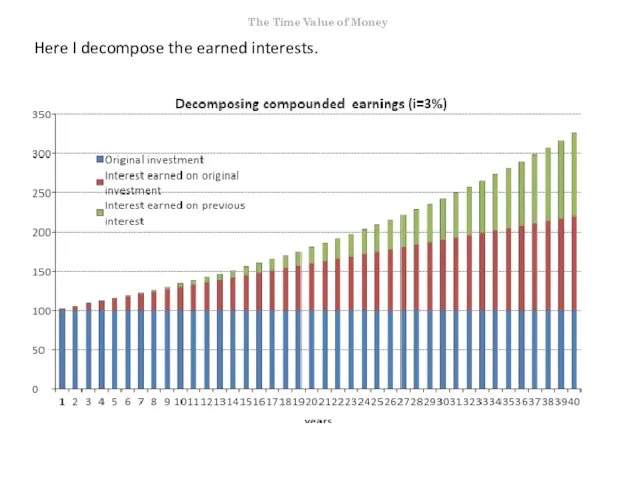

Here I decompose the earned interests.

The Time Value of Money

Here I decompose the earned interests.

The Time Value of Money

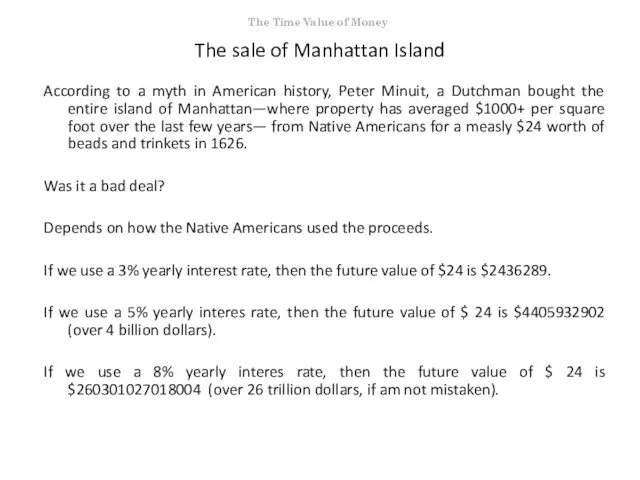

The Time Value of Money

The sale of Manhattan Island

According to a

The Time Value of Money

The sale of Manhattan Island

According to a

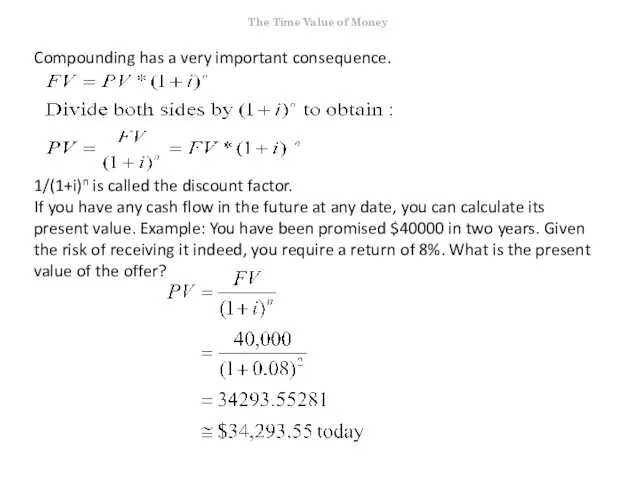

Compounding has a very important consequence.

1/(1+i)n is called the discount factor.

If

Compounding has a very important consequence.

1/(1+i)n is called the discount factor.

If

The Time Value of Money

The Time Value of Money

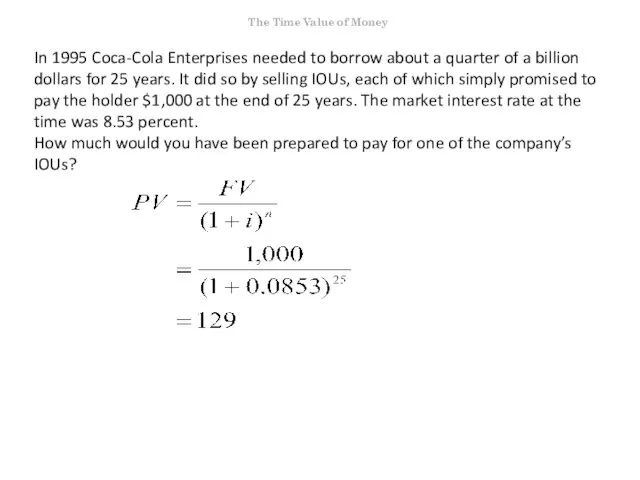

In 1995 Coca-Cola Enterprises needed to borrow about a quarter of

In 1995 Coca-Cola Enterprises needed to borrow about a quarter of

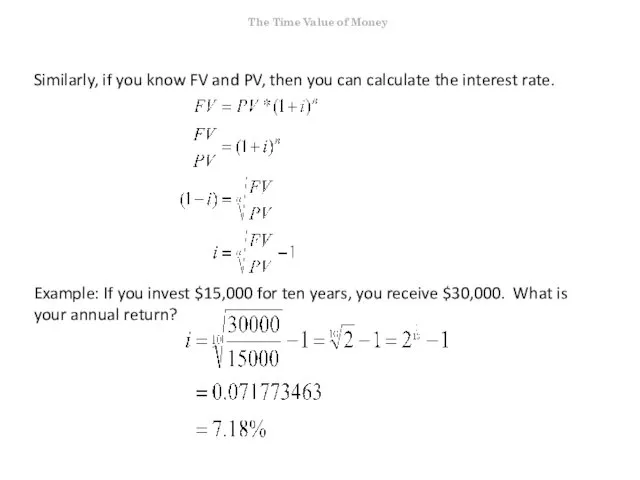

Similarly, if you know FV and PV, then you can calculate

Similarly, if you know FV and PV, then you can calculate

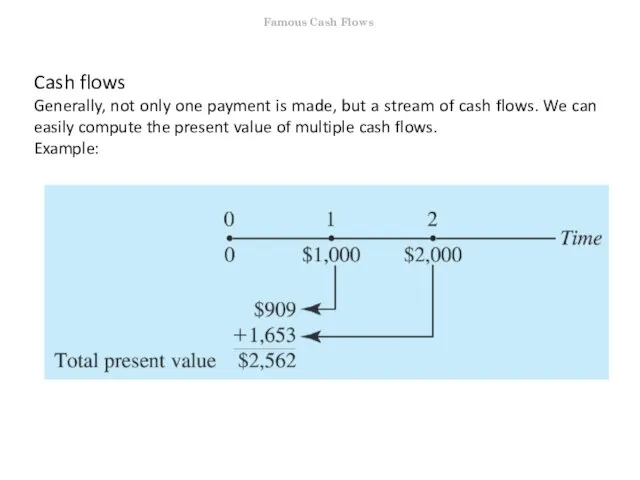

Cash flows

Generally, not only one payment is made, but a stream

Cash flows

Generally, not only one payment is made, but a stream

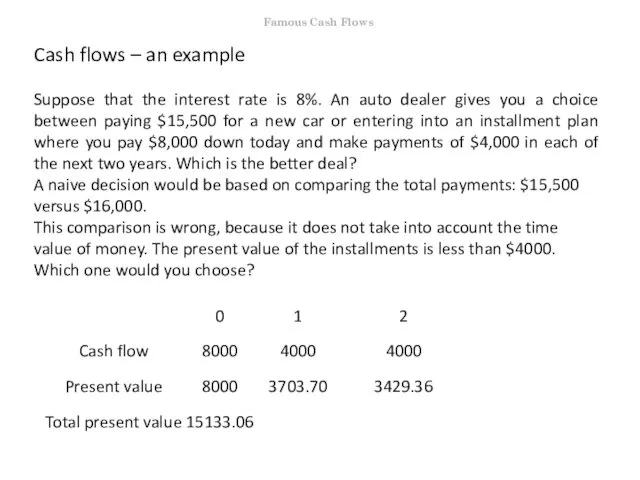

Cash flows – an example

Suppose that the interest rate is 8%.

Cash flows – an example

Suppose that the interest rate is 8%.

Level cash flows

There are cash flows that feature very regular payments.

For

Level cash flows

There are cash flows that feature very regular payments.

For

Annuity

Annuity is a sequence of equally spaced identical cash flows.

We

Annuity

Annuity is a sequence of equally spaced identical cash flows.

We

The present value of an annuity

How much would you pay for

The present value of an annuity

How much would you pay for

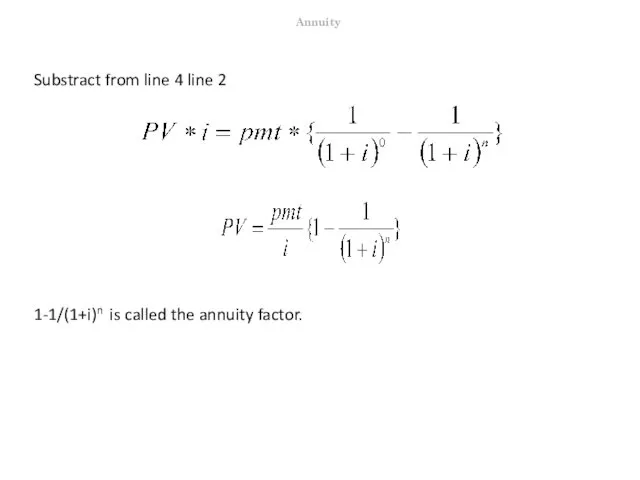

Substract from line 4 line 2

1-1/(1+i)n is called the annuity factor.

Annuity

Substract from line 4 line 2

1-1/(1+i)n is called the annuity factor.

Annuity

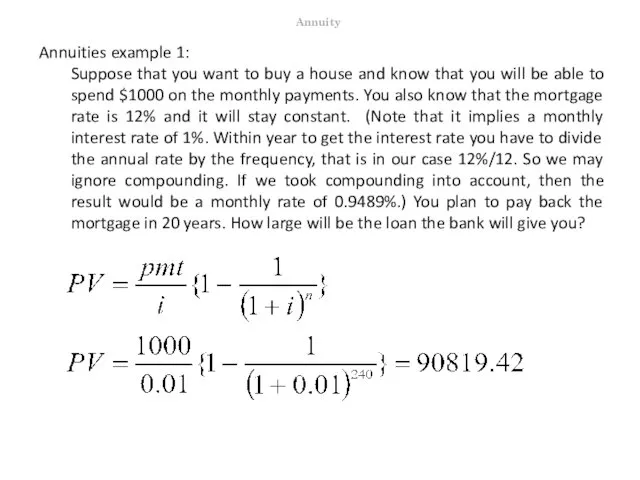

Annuities example 1:

Suppose that you want to buy a house and

Annuities example 1:

Suppose that you want to buy a house and

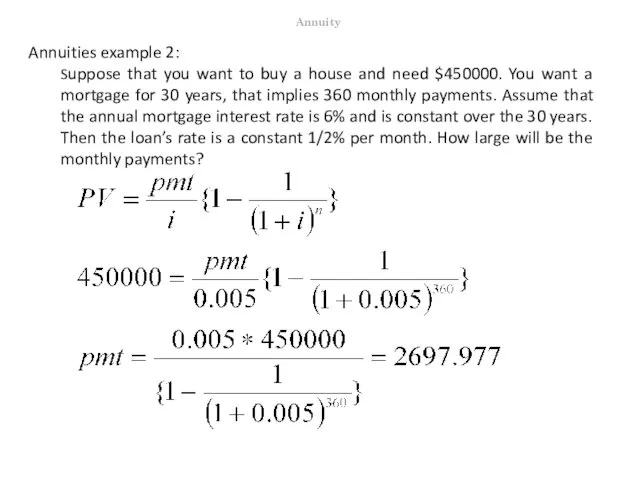

Annuities example 2:

Suppose that you want to buy a house and

Annuities example 2:

Suppose that you want to buy a house and

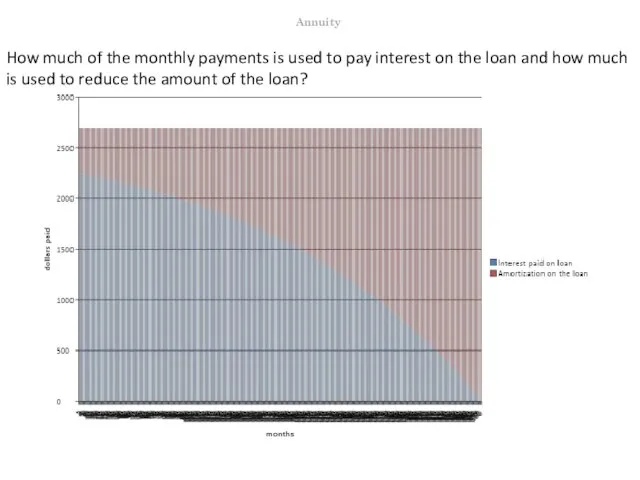

How much of the monthly payments is used to pay interest

How much of the monthly payments is used to pay interest

The retirement example

Let’s see how we can use knowing how „famous”

The retirement example

Let’s see how we can use knowing how „famous”

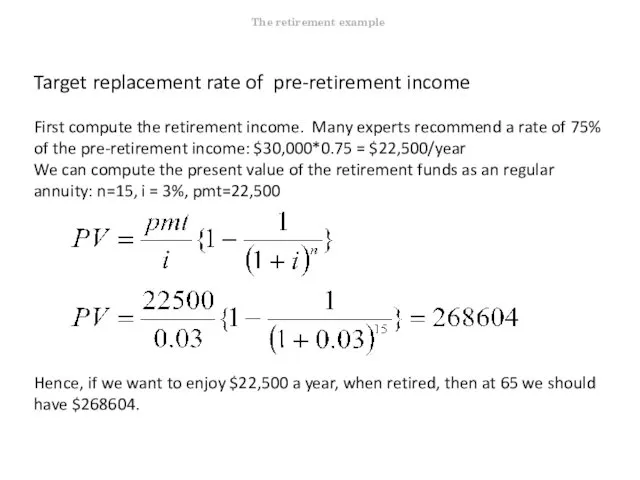

Target replacement rate of pre-retirement income

First compute the retirement income. Many

Target replacement rate of pre-retirement income

First compute the retirement income. Many

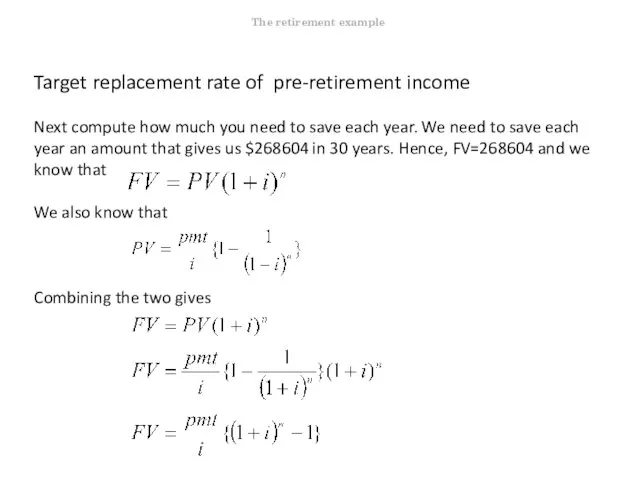

Target replacement rate of pre-retirement income

Next compute how much you need

Target replacement rate of pre-retirement income

Next compute how much you need

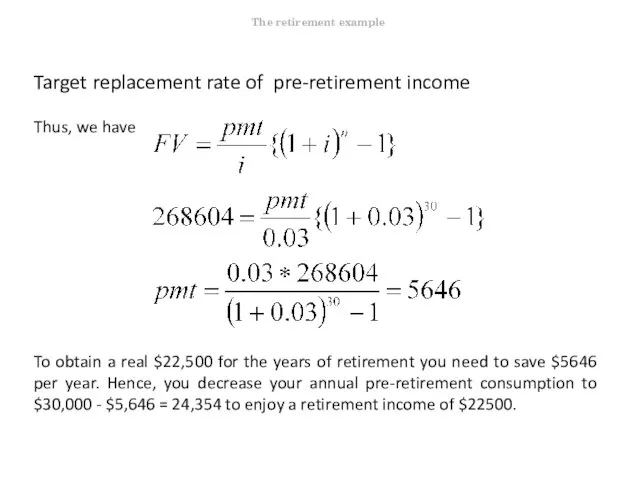

Target replacement rate of pre-retirement income

Thus, we have

To obtain a real

Target replacement rate of pre-retirement income

Thus, we have

To obtain a real

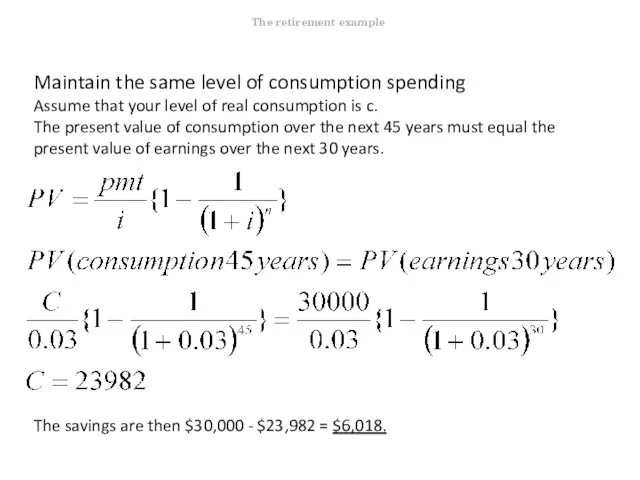

Maintain the same level of consumption spending

Assume that your level of

Maintain the same level of consumption spending

Assume that your level of

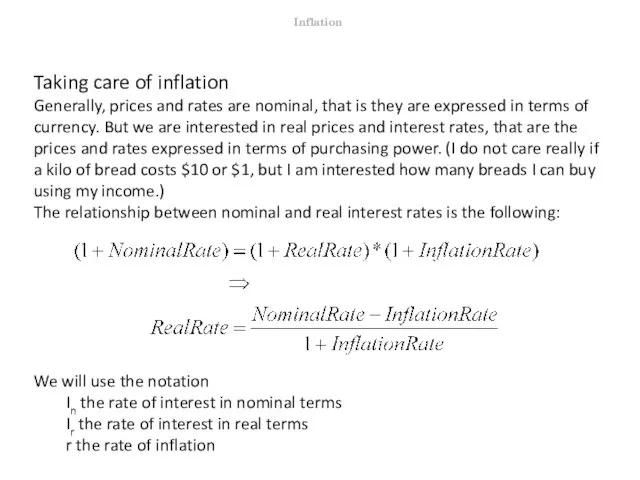

Taking care of inflation

Generally, prices and rates are nominal, that is

Taking care of inflation

Generally, prices and rates are nominal, that is

Taking care of inflation

What is the real rate of interest if

Taking care of inflation

What is the real rate of interest if

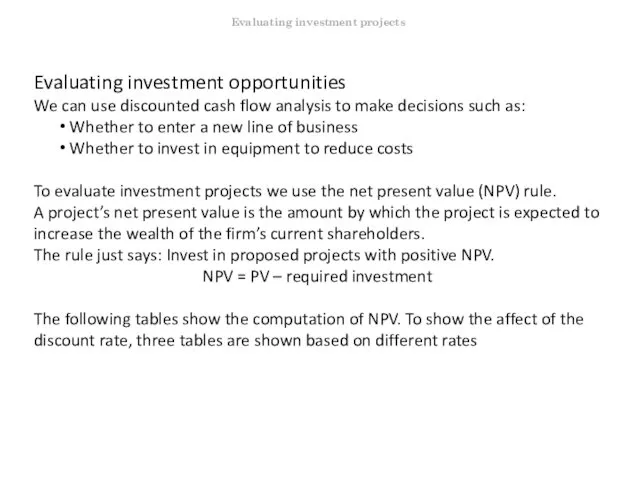

Evaluating investment opportunities

We can use discounted cash flow analysis to make

Evaluating investment opportunities

We can use discounted cash flow analysis to make

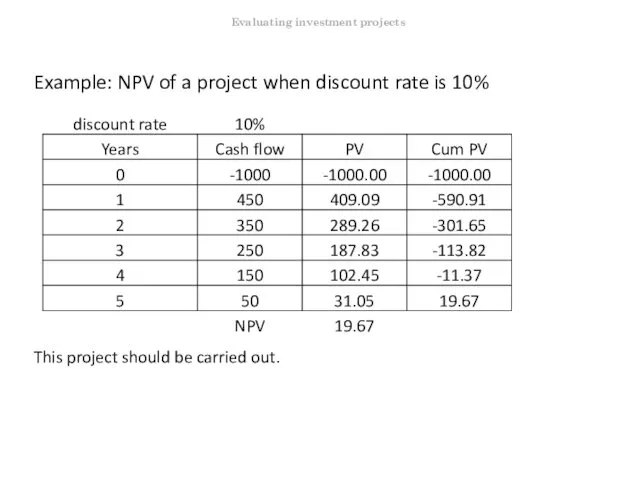

Example: NPV of a project when discount rate is 10%

This project

Example: NPV of a project when discount rate is 10%

This project

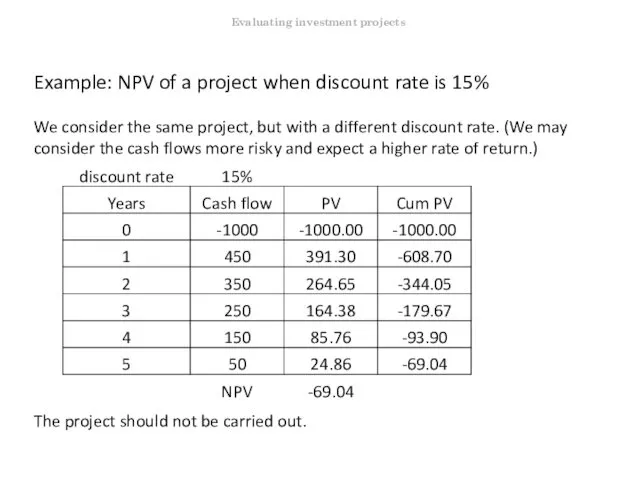

Example: NPV of a project when discount rate is 15%

We consider

Example: NPV of a project when discount rate is 15%

We consider

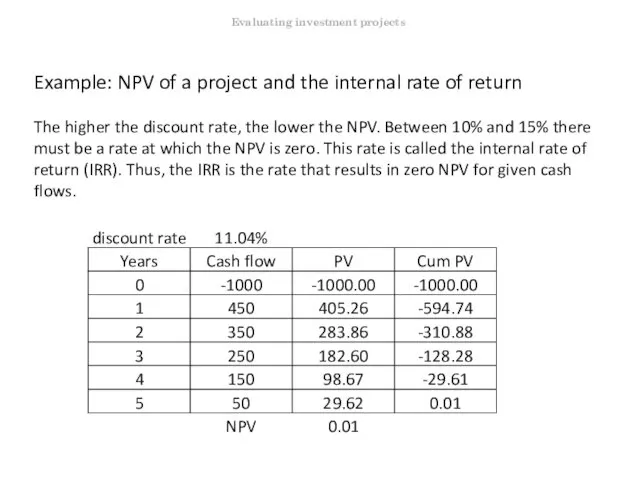

Example: NPV of a project and the internal rate of return

The

Example: NPV of a project and the internal rate of return

The

NPV and the internal rate of return

From the previous example we

NPV and the internal rate of return

From the previous example we

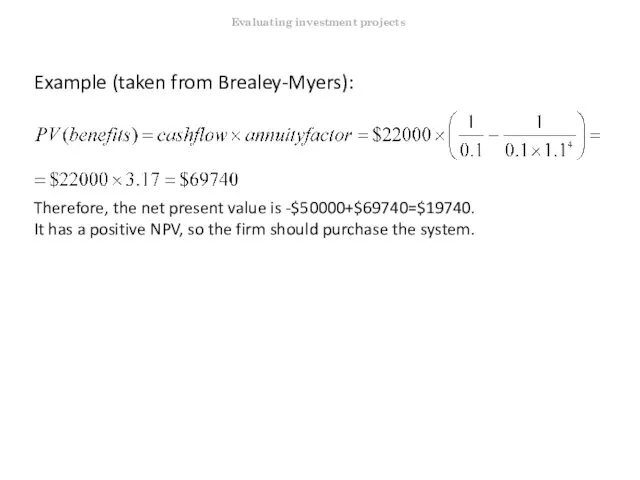

Example (taken from Brealey-Myers):

Obsolete Technologies is considering the purchase of a

Example (taken from Brealey-Myers):

Obsolete Technologies is considering the purchase of a

Example (taken from Brealey-Myers):

Therefore, the net present value is -$50000+$69740=$19740.

It has

Example (taken from Brealey-Myers):

Therefore, the net present value is -$50000+$69740=$19740.

It has

Mutually exclusive projects

We speak about mutually exclusive projects if there are

Mutually exclusive projects

We speak about mutually exclusive projects if there are

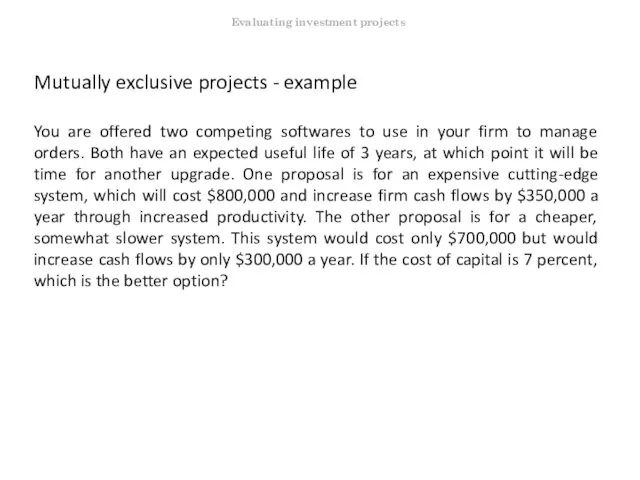

Mutually exclusive projects - example

You are offered two competing softwares to

Mutually exclusive projects - example

You are offered two competing softwares to

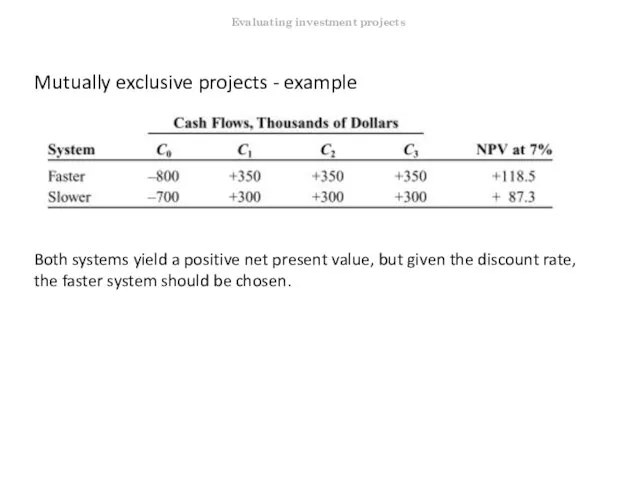

Mutually exclusive projects - example

Both systems yield a positive net present

Mutually exclusive projects - example

Both systems yield a positive net present

Investment timing

We return to Obsolete Technologies that was contemplating the purchase

Investment timing

We return to Obsolete Technologies that was contemplating the purchase

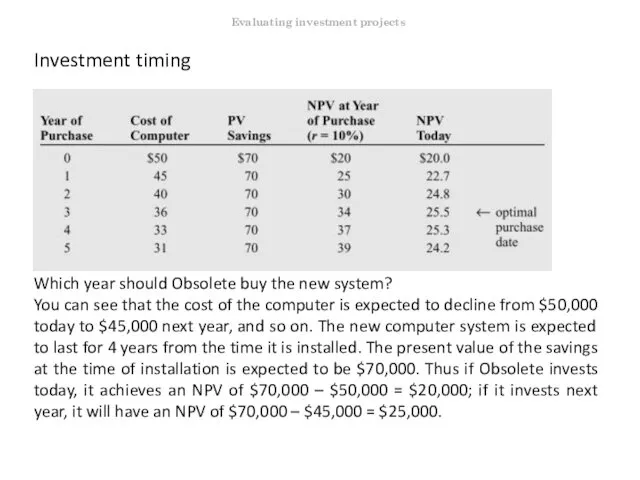

Investment timing

Which year should Obsolete buy the new system?

You can see

Investment timing

Which year should Obsolete buy the new system?

You can see

Investment timing

Isn’t a gain of $25,000 better than one of $20,000?

Investment timing

Isn’t a gain of $25,000 better than one of $20,000?

Investment timing

If you postpone from Year 3 to Year 4, the

Investment timing

If you postpone from Year 3 to Year 4, the

Построение схемы Налоги и сборы в РФ

Построение схемы Налоги и сборы в РФ Действующие налоги и сборы. Специальные налоговые режимы в РФ

Действующие налоги и сборы. Специальные налоговые режимы в РФ Антикризисное управление предприятием

Антикризисное управление предприятием Чистый оборотный капитал организации

Чистый оборотный капитал организации Этапы становления бухгалтерского учета как науки

Этапы становления бухгалтерского учета как науки Проект бюджета на 2020 год и плановый период 2021 и 2022 годов города Котельнича Кировской области

Проект бюджета на 2020 год и плановый период 2021 и 2022 годов города Котельнича Кировской области Тема лекции Объекты учета затрат в системе управленческого учета

Тема лекции Объекты учета затрат в системе управленческого учета Совершенствоание организации сбытовой деятельности предприятия ОАО Агрокомбинат Южный

Совершенствоание организации сбытовой деятельности предприятия ОАО Агрокомбинат Южный Таможенная стоимость и методы её определения

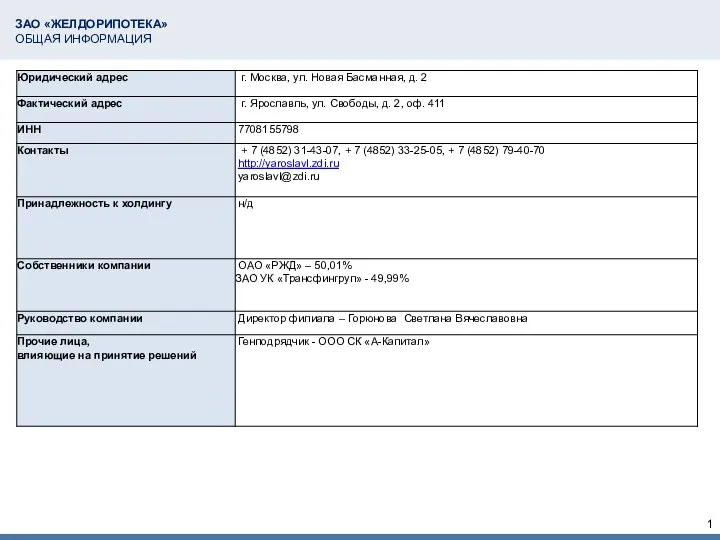

Таможенная стоимость и методы её определения ЗАО Желдорипотека. Общая информация

ЗАО Желдорипотека. Общая информация Виды и классификация затрат на производство

Виды и классификация затрат на производство Доходы бюджетов

Доходы бюджетов Бюджетный процесс: совставление, рассмотрение, утверждение и исполнение бюджетов п хвеньям бюджетной системы

Бюджетный процесс: совставление, рассмотрение, утверждение и исполнение бюджетов п хвеньям бюджетной системы Добровольное медицинское страхование

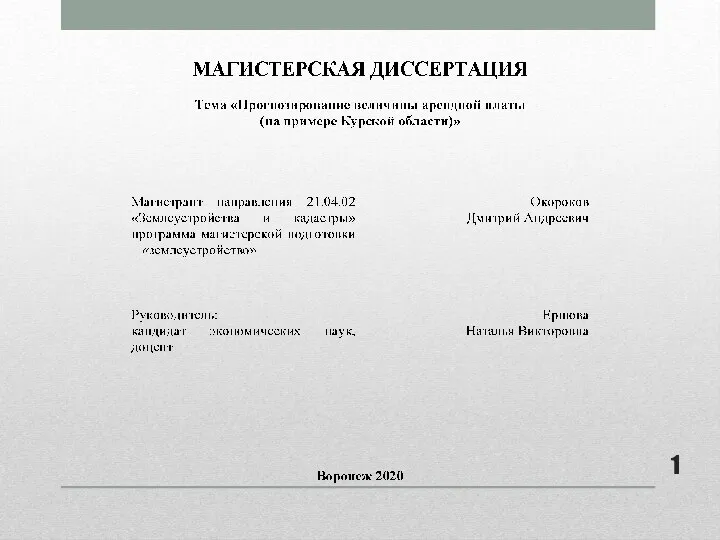

Добровольное медицинское страхование ВКР: Прогнозирование величины арендной платы

ВКР: Прогнозирование величины арендной платы Расчет затрат на создание ИС

Расчет затрат на создание ИС Учёт на торговом объекте

Учёт на торговом объекте Учет денежных средств

Учет денежных средств Сравнительный подход

Сравнительный подход Метод бухгалтерского учета

Метод бухгалтерского учета Ипотечные и кредитные каникулы

Ипотечные и кредитные каникулы Valuation Финансовый клуб ВШМ

Valuation Финансовый клуб ВШМ Кредитные карты. Кредит Европа Банк

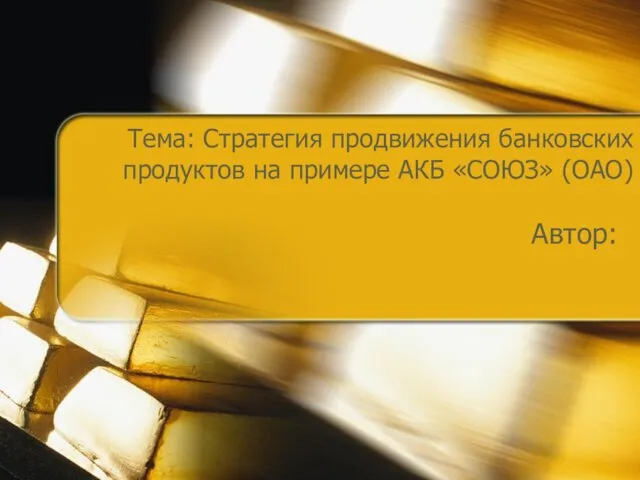

Кредитные карты. Кредит Европа Банк Стратегия продвижения банковских продуктов на примере АКБ СОЮЗ (ОАО)

Стратегия продвижения банковских продуктов на примере АКБ СОЮЗ (ОАО) Презентация ОТ -2019

Презентация ОТ -2019 Листовка для информирования ЗП 10%

Листовка для информирования ЗП 10% Практика использования платёжных банковских карт в коммерческом банке и пути её совершенствования

Практика использования платёжных банковских карт в коммерческом банке и пути её совершенствования Биржа LME

Биржа LME