- Methodology of accounting

Содержание

- 2. Damn lucky for someone who has never studied accounting. Then he would have immediately realized that

- 3. A good accountant is expensive, and a bad one is much more expensive Stanislav Jerzy Lez

- 4. Definition Accounting is the formation of documented systematized information about objects provided for by law, in

- 5. Types of accounting Financial accounting - focused on external users of information (this is traditional accounting);

- 6. Maintaining accounting records All organizations are required to maintain accounting records. Some organizations (small businesses) may

- 7. Regulation of accounting Accounting is regulated by special documents -standards. The accounting standard is a document

- 8. Regulation of accounting federal accounting standards; branches of industry accounting standards; regulatory acts of the Central

- 9. Regulation of accounting In addition to national accounting standards, there are also international financial reporting standards

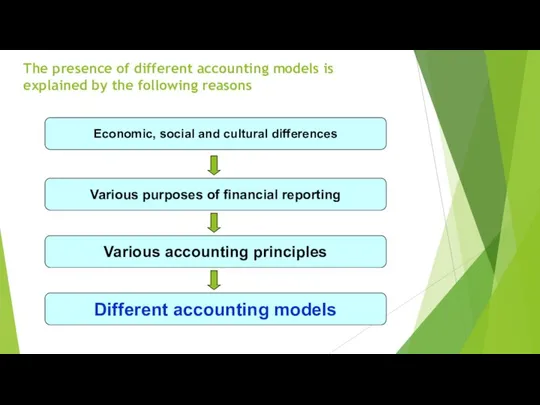

- 10. The presence of different accounting models is explained by the following reasons Economic, social and cultural

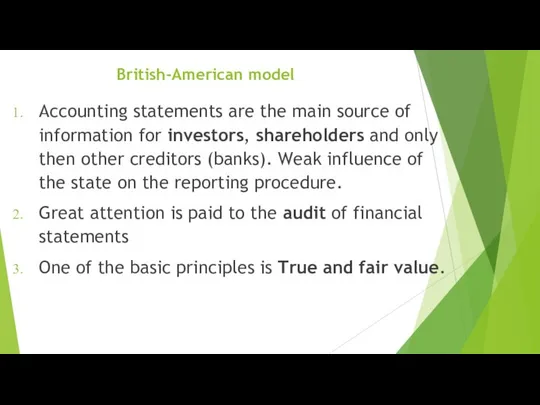

- 11. British-American model Accounting statements are the main source of information for investors, shareholders and only then

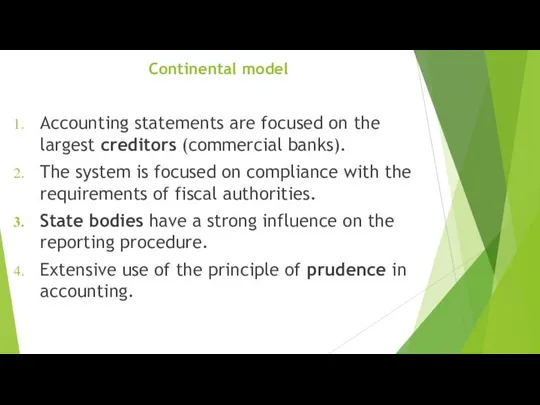

- 12. Continental model Accounting statements are focused on the largest creditors (commercial banks). The system is focused

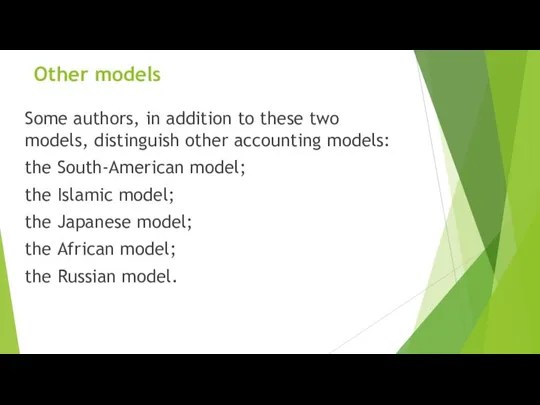

- 13. Other models Some authors, in addition to these two models, distinguish other accounting models: the South-American

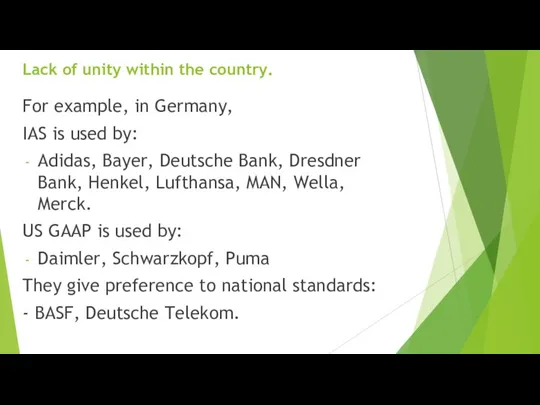

- 14. Lack of unity within the country. For example, in Germany, IAS is used by: Adidas, Bayer,

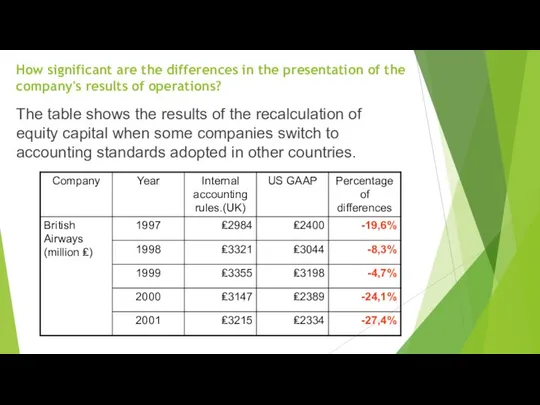

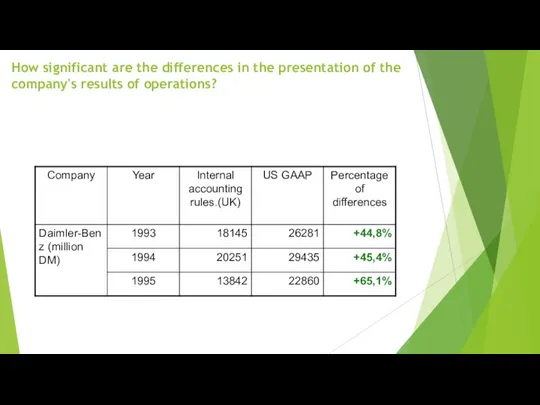

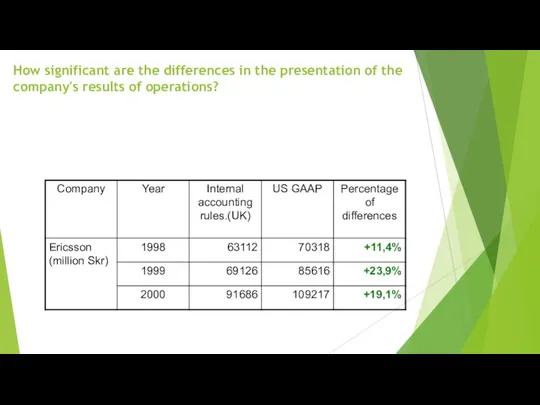

- 15. How significant are the differences in the presentation of the company's results of operations? The table

- 16. How significant are the differences in the presentation of the company's results of operations?

- 17. How significant are the differences in the presentation of the company's results of operations?

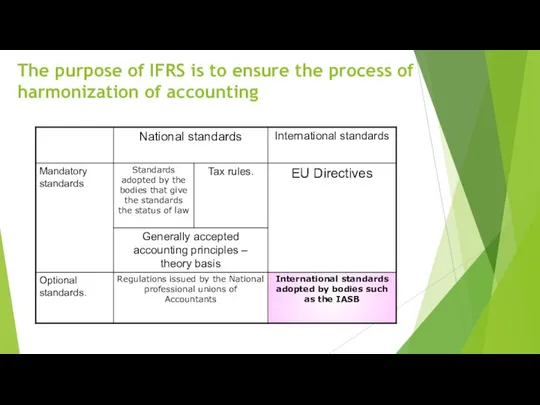

- 18. The purpose of IFRS is to ensure the process of harmonization of accounting

- 19. Application of the IFRS in the world There are several variants for applying IFRS: 1. Applying

- 20. Application of the IFRS in the world 2. National organizations of the development of financial reporting

- 21. Application of the IFRS in the world 3. Stock exchanges and bodies regulating the securities market

- 22. Application of the IFRS in the world 4. Using of the IFRS in the preparation of

- 23. Application of the IFRS in the world 5. Using of the IFRS by the companies themselves

- 24. Benefits of using the IFRS for business Improving the quality of information for decision-making by managers;

- 25. Benefits of using the IFRS for potential investors Improving the quality of information for making investment

- 26. Benefits of using the IFRS for the state Strengthening the capital market and increasing its attractiveness;

- 27. International Accounting Standards Board The main goal of the IASB is to provide a process for

- 28. The IFRS development process Creation of a Preparatory Committee from a wide range of specialists in

- 29. The IFRS development process 2. Development and publication of the original document - the primary draft

- 30. The IFRS development process 3. Preparation of a working draft of the provisions of the standard,

- 31. The IFRS development process 4. Issue of the final international financial reporting standard - IFRS (formerly

- 32. The IFRS development process 5. Introduction of the standard – in most cases, new standards begin

- 33. Types of standards IAS - International accounting standards - were issued until 2003. IAS 1-41 were

- 34. Types of standards In addition, there are interpretations to the standards (sequences) - SIC - Standards

- 35. Bookkeeping Accounting and storage of accounting documents are organized by the head of an organization. The

- 36. Requirements for the chief accountant in Russia For chief accountants of some organizations (PJSCs, investment funds,

- 37. Bookkeeping The totality of accounting methods forms the accounting policy of the organization. An organization independently

- 38. Accounting objects facts of economic life; assets; liabilities; sources of funding for its activities (capital); incomes;

- 39. Accounting objects A fact of economic life is a transaction, event, operation that has or is

- 40. Source documents Mandatory details of the document: 1) the title of the document; 2) date of

- 41. In addition to the required details, extra information can be included in the documents. Moreover, if

- 42. Source documents The primary accounting document must be drawn up when the fact of economic life

- 43. Source documents Requirements of the chief accountant in writing form that are connected with the procedure

- 44. Source documents The primary accounting document is drawn up on paper and (or) in the form

- 45. The documents must be kept in the form in which they were drawn up. Translation of

- 46. Source documents in Russia The documents are prepared in Russian. If the primary document is in

- 47. The date of drawing up the primary document is the day of its signing by the

- 48. When drawing up primary documents, you can draw up several related facts of economic life with

- 49. It is possible to draw up lasting facts of economic life (accrual of interest, depreciation), as

- 50. It is allowed to use as primary documents that one that was drawn up or received

- 51. The list of persons entitled to sign documents is established by the head of the organization.

- 52. Bookkeeping The data contained in primary accounting documents are subject to timely registration and accumulation in

- 53. Financial statements The financial statements should provide a reliable representation of the financial position of an

- 54. The unprecedented thickness of this report protected it from the danger of being read. W. Churchill

- 55. Financial statements There are three types of lying: bragging, lying, and reporting. J. Bulatovich (Polish publicist)

- 56. Отчетность в высказываниях Automation can never completely replace accounting. It is not profitable V. Borisov (Russian

- 57. Отчетность в высказываниях If you want to take control of your life, you must regularly prepare

- 58. Financial statements Financial statements are provided to external users of information Users

- 59. Who are external users? Shareholders Investors Suppliers Users with direct financial interest

- 60. Who are external users? Tax authorities Banks Government bodies Auditing companies Buyers Users with indirect financial

- 61. Who are external users? Exchanges Statistical bodies Judiciary Users without financial interest

- 62. What is reporting for? Analysis of financial condition Evaluation of the efficiency of functioning Planning for

- 63. Assumptions of Formation of Financial Reporting Indicators The assets and liabilities of an organization exist separately

- 64. Assumptions of Formation of Financial Reporting Indicators The organization will continue its activities for the foreseeable

- 65. Assumptions of Formation of Financial Reporting Indicators Business continuity - going concern

- 66. Assumptions of Formation of Financial Reporting Indicators The accounting policy adopted by the organization is applied

- 67. Assumptions of Formation of Financial Reporting Indicators They are reflected in the accounting and reporting of

- 68. General requirements for financial statements The reporting should give a reliable view of the financial position

- 69. Financial statements Annual financial statements consist of a balance sheet, a statement of financial results and

- 70. Financial statements It is mandatory to draw up annual financial statements (for a calendar year). Preparation

- 71. Financial statements The financial statements are considered to be drawn up after they are signed by

- 72. Financial statements State information resource - a set of financial statements of economic entities, as well

- 73. Accounting method

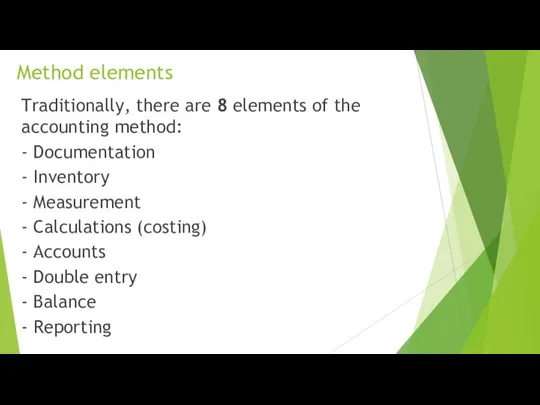

- 74. Method elements Traditionally, there are 8 elements of the accounting method: - Documentation - Inventory -

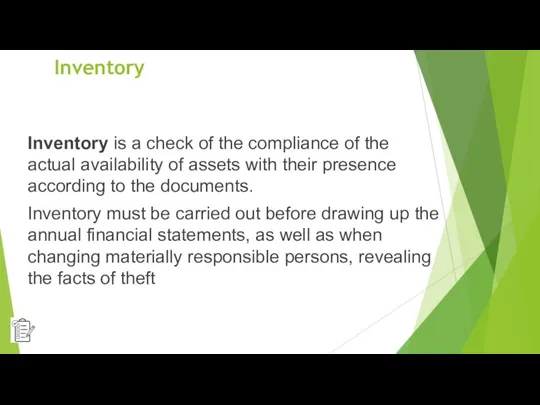

- 75. Inventory Inventory is a check of the compliance of the actual availability of assets with their

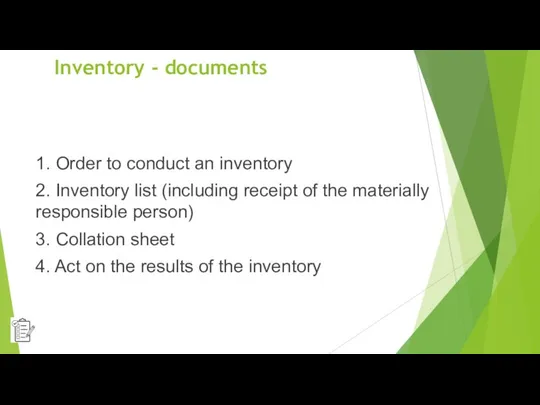

- 76. Inventory - documents 1. Order to conduct an inventory 2. Inventory list (including receipt of the

- 77. Inventory - results 1. Surplus (other incomes at market prices (fair value)) "... Inventory, like any

- 78. Natural loss Methodological recommendations for the development of norms of natural loss (Order of the Ministry

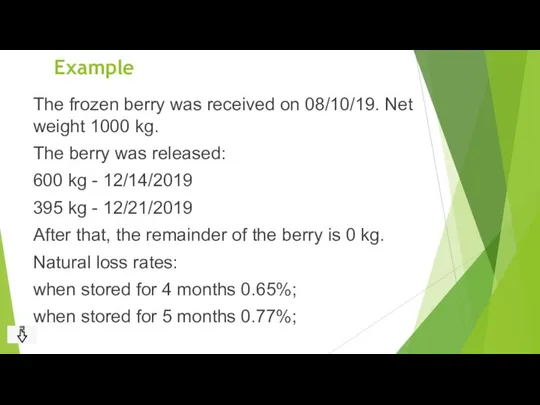

- 79. Example The frozen berry was received on 08/10/19. Net weight 1000 kg. The berry was released:

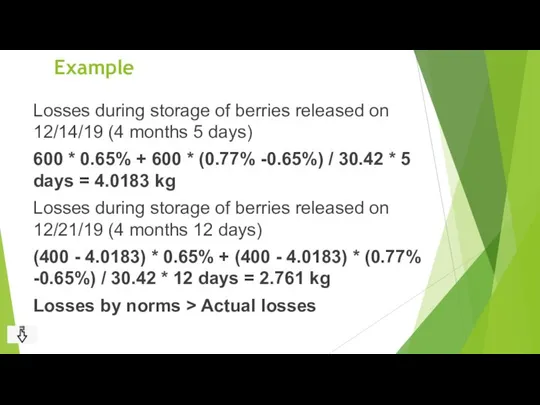

- 80. Example Losses during storage of berries released on 12/14/19 (4 months 5 days) 600 * 0.65%

- 81. The culprit has not been identified Letter of the Ministry of Finance dated 20.05.14 No. 03-03-07

- 82. Doubtful accounts receivable The receivables of the organization are considered doubtful if they are not repaid

- 83. Doubtful accounts receivable Since 2011, organizations are required to create reserves for doubtful debts. Basis -

- 84. Doubtful accounts receivable Accounts receivable are recognized as doubtful from the date of due date of

- 85. Monetary measurement Accounting objects are subject to monetary measurement. Monetary measurement of accounting objects in the

- 86. Calculation (costing) In some cases, it is not possible to directly determine the cost estimate of

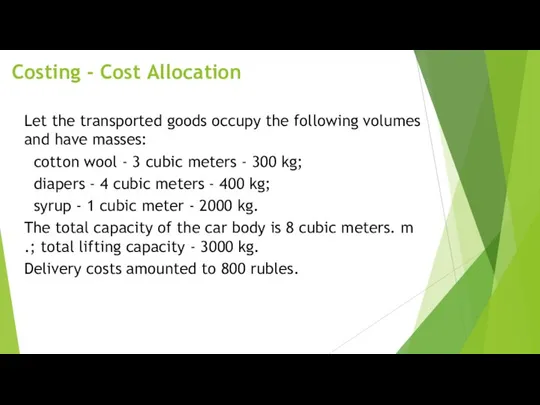

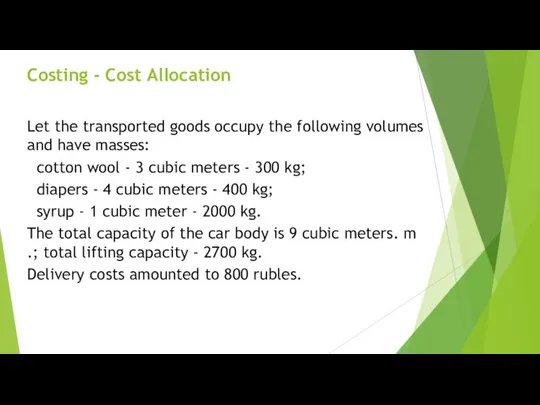

- 87. Costing - Cost Allocation Let the transported goods occupy the following volumes and have masses: cotton

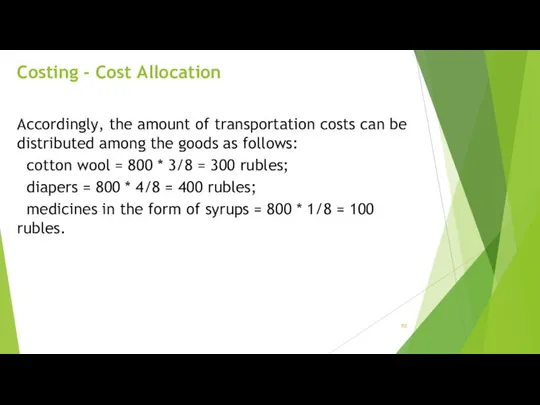

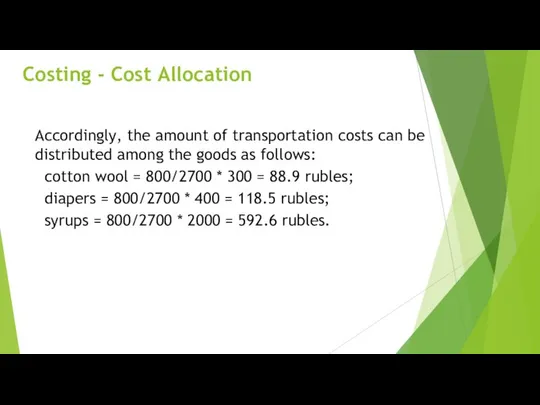

- 88. Costing - Cost Allocation Accordingly, the amount of transportation costs can be distributed among the goods

- 89. Costing - Cost Allocation Let the transported goods occupy the following volumes and have masses: cotton

- 90. Costing - Cost Allocation Accordingly, the amount of transportation costs can be distributed among the goods

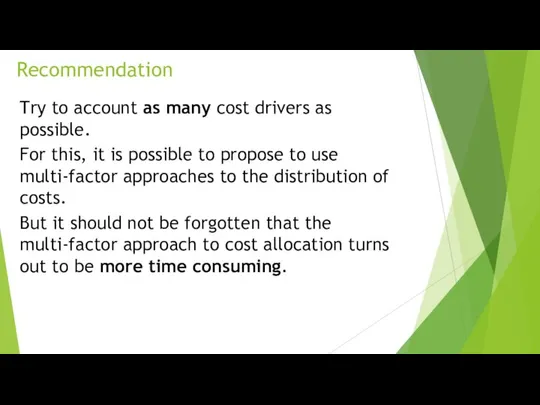

- 91. Recommendation Try to account as many cost drivers as possible. For this, it is possible to

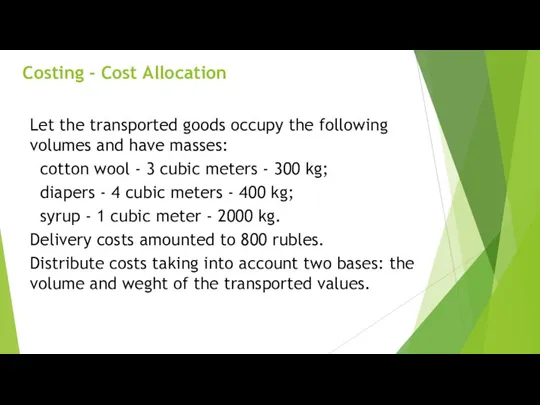

- 92. Costing - Cost Allocation Let the transported goods occupy the following volumes and have masses: cotton

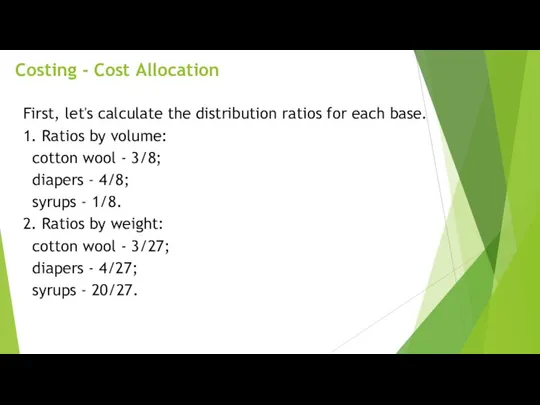

- 93. Costing - Cost Allocation First, let's calculate the distribution ratios for each base. 1. Ratios by

- 94. Costing - Cost Allocation Then we calculate the total bases for each product: cotton wool -

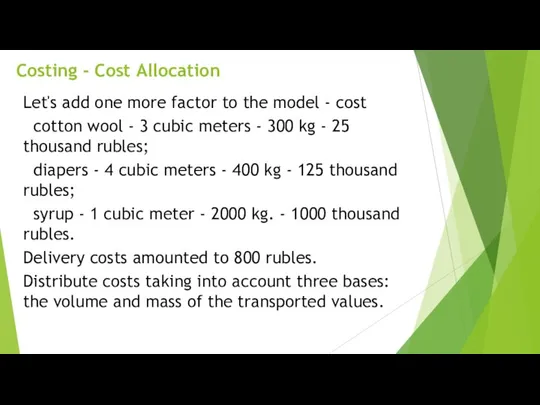

- 95. Costing - Cost Allocation Let's add one more factor to the model - cost cotton wool

- 96. Costing - Cost Allocation

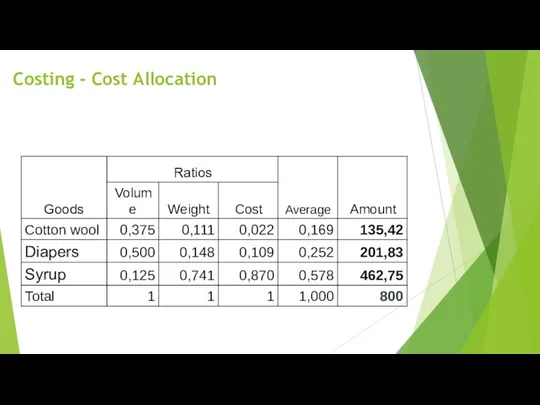

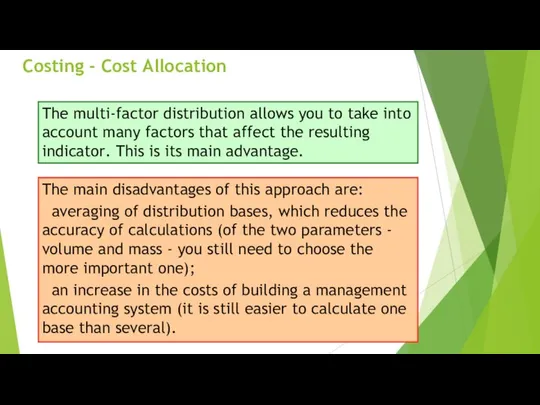

- 97. Costing - Cost Allocation The multi-factor distribution allows you to take into account many factors that

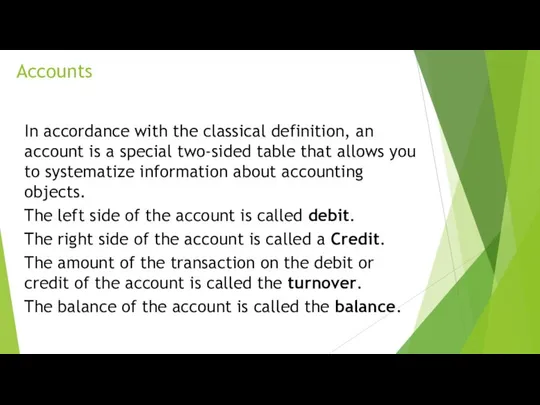

- 98. Accounts In accordance with the classical definition, an account is a special two-sided table that allows

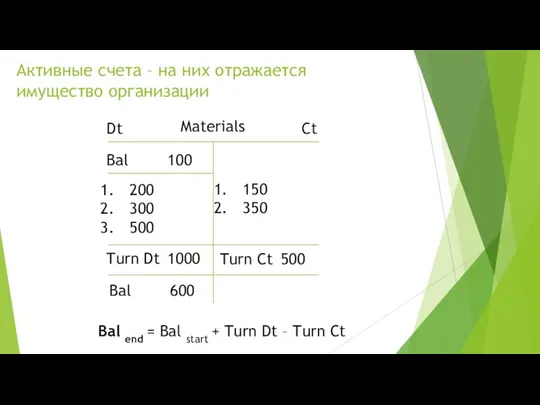

- 99. Активные счета – на них отражается имущество организации Dt Ct Bal 100 200 300 500 Turn

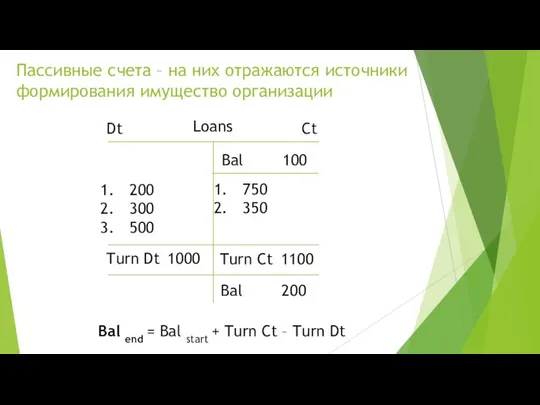

- 100. Пассивные счета – на них отражаются источники формирования имущество организации Dt Ct Bal 100 200 300

- 101. Активные счета – на них отражается имущество организации Dt Ct Bal 100 200 300 500 Turn

- 102. Double entry The simultaneous reflection of a debit transaction on one account and a credit on

- 103. Double entry Dt Ct Bal 400 200 Turn Dt 200 Turn Ct 0 Materials Bal 600

- 104. Double entry There are 4 types of business transactions in total Asset + = Liability +

- 105. Double entry (A- = P-) Dt Ct Bal 500 200 Turn Dt 0 Turn Ct 200

- 106. Double entry (A ± = P) Dt Ct Bal 600 150 Turn Dt 0 Turn Ct

- 107. Double entry (A = P ±) Dt Ct Bal 400 250 Turn Dt 0 Turn Ct

- 108. Accounting objects

- 109. Assets Assets are resources whose value can be estimated and from which the company expects to

- 110. Cash Cash means cash and non-cash funds of an organization stored in the cash desk and

- 111. Cash Non-cash funds are kept in current accounts in banks. Currently, almost all interaction of organizations

- 112. Cash In some cases, transactions on current accounts may be blocked. This usually happens at the

- 113. Cash To store currency, organizations may use foreign currency accounts. However, on the territory of the

- 114. Cash In addition to current and foreign currency accounts, organizations may have special bank accounts. Today,

- 115. Cash Operations with cash is called cash flow. The cash flows of the organization are divided

- 116. Cash a) receipts from the sale of products and goods to buyers; b) payments to suppliers

- 117. Cash An entity's cash flows from transactions related to the acquisition, creation or disposal of an

- 118. Cash a) payments to suppliers and employees of the organization in connection with the acquisition, creation,

- 119. Cash The cash flows of the organization from operations related to the attraction of financing by

- 120. Cash a) monetary payments of owners to the capital, proceeds from the issue of shares, an

- 121. Cash documents Monetary documents are special protected in some way documents (pin codes, passwords, etc.), purchased

- 122. Cash equivalents Cash equivalents are highly liquid financial investments that can be easily converted into a

- 123. Short-term financial investments Financial investments are investments in other companies made through the acquisition of financial

- 124. Short-term financial investments The main differences between short-term financial investments and cash equivalents are: - duration

- 125. Short-term financial investments All financial investments are divided into two groups: - financial investments, for which

- 126. Short-term financial investments If the current market value can be determined (for example, at the rate

- 127. Accounts receivables Accounts receivable are amounts owed to this organization by other participants in economic relations,

- 128. Accounts receivables Accounts receivable are funds withdrawn from the organization's turnover. At the moment, these funds

- 129. Accounts receivables A receivable is recognized as doubtful if the organization has no assurance about the

- 130. Accounts receivables Organizations can use several tools to manage doubtful accounts receivable. One of the most

- 131. Accounts receivables An extreme case of doubtful accounts receivable is bad accounts receivable. Bad debts (that

- 132. Accounts receivables In addition the debtors of the organization may be its own employees (for example,

- 133. VAT The amounts of VAT on the purchased values are actually a kind of accounts receivable,

- 134. Stocks Inventories are one of the main group of assets, which includes several important components: -

- 135. Fixed assets Fixed assets are assets that have a tangible form that can bring economic benefits

- 136. Fixed assets - buildings and constructions. In recent years, this subgroup is increasingly referred to as

- 137. Fixed assets Organizations are given the right to revalue fixed assets, that is, to bring their

- 138. Intangible assets These are non-monetary assets protected by certain copyrights. These include: - works of science,

- 139. Goodwill One of the most specific types of intangible assets is goodwill - business reputation. Goodwill

- 140. Investments in future non-current assets Fixed assets and intangibles sometimes have a long period of preparation

- 141. Profitable investments in material assets Income investments in tangible assets include those fixed assets that are

- 142. Long-term financial investments Long-term financial investments are investments in securities for a period of more than

- 143. Capital - sources of property formation The sources of property formation are divided into two groups:

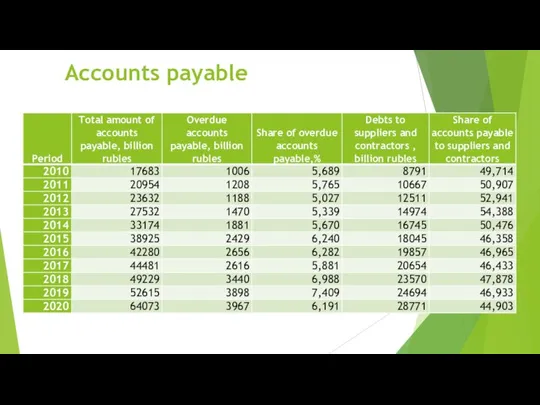

- 144. Accounts payable Accounts payable is a debt owed by this organization to someone. There are many

- 145. Accounts payable Accounts payable to suppliers and contractors for goods, works, services - this type of

- 146. Accounts payable When the liability is extinguished in cash or other assets, then there is a

- 147. Accounts payable

- 148. Short-term credit and loans Short-term credits and short-term loans provided to organizations by other entities, for

- 149. Provisions Provisions are liabilities with an uncertain amount or period that either will necessarily arise in

- 150. Long credit and loans Long-term credit and borrowings provided to organizations by other entities for the

- 151. Equity The authorized capital is the valuation of the organization's property, which was contributed to it

- 152. Equity The share in the authorized capital belonging to the participants of the established organization gives

- 153. Equity Additional capital ("air capital") - capital resulting from the revaluation of fixed assets. Gradually over

- 154. Equity In addition to the revaluation of fixed assets, share premium can also be a source

- 155. Equity Profit of the organization: - gross profit, defined as the difference between the revenues and

- 156. Equity Part of the profit can be used to pay dividends, and part - to form

- 158. Скачать презентацию

Damn lucky for someone who has never studied accounting. Then he

Damn lucky for someone who has never studied accounting. Then he

A good accountant is expensive, and a bad one is much

A good accountant is expensive, and a bad one is much

Definition

Accounting is the formation of documented systematized information about objects provided

Definition

Accounting is the formation of documented systematized information about objects provided

Types of accounting

Financial accounting - focused on external users of information

Types of accounting

Financial accounting - focused on external users of information

Maintaining accounting records

All organizations are required to maintain accounting records.

Some organizations

Maintaining accounting records

All organizations are required to maintain accounting records.

Some organizations

Regulation of accounting

Accounting is regulated by special documents -standards.

The accounting standard

Regulation of accounting

Accounting is regulated by special documents -standards.

The accounting standard

Regulation of accounting

federal accounting standards;

branches of industry accounting standards;

regulatory acts of

Regulation of accounting

federal accounting standards;

branches of industry accounting standards;

regulatory acts of

Regulation of accounting

In addition to national accounting standards, there are also

Regulation of accounting

In addition to national accounting standards, there are also

The presence of different accounting models is explained by the following

The presence of different accounting models is explained by the following

British-American model

Accounting statements are the main source of information for investors,

British-American model

Accounting statements are the main source of information for investors,

Continental model

Accounting statements are focused on the largest creditors (commercial banks).

The

Continental model

Accounting statements are focused on the largest creditors (commercial banks).

The

Other models

Some authors, in addition to these two models, distinguish other

Other models

Some authors, in addition to these two models, distinguish other

Lack of unity within the country.

For example, in Germany,

IAS is

Lack of unity within the country.

For example, in Germany,

IAS is

How significant are the differences in the presentation of the company's

How significant are the differences in the presentation of the company's

How significant are the differences in the presentation of the company's

How significant are the differences in the presentation of the company's

How significant are the differences in the presentation of the company's

How significant are the differences in the presentation of the company's

The purpose of IFRS is to ensure the process of harmonization

The purpose of IFRS is to ensure the process of harmonization

Application of the IFRS in the world

There are several variants for

Application of the IFRS in the world

There are several variants for

Application of the IFRS in the world

2. National organizations of the

Application of the IFRS in the world

2. National organizations of the

Application of the IFRS in the world

3. Stock exchanges and bodies

Application of the IFRS in the world

3. Stock exchanges and bodies

Application of the IFRS in the world

4. Using of the IFRS

Application of the IFRS in the world

4. Using of the IFRS

Application of the IFRS in the world

5. Using of the IFRS

Application of the IFRS in the world

5. Using of the IFRS

Benefits of using the IFRS for business

Improving the quality of

Benefits of using the IFRS for business

Improving the quality of

Benefits of using the IFRS for potential investors

Improving the quality

Benefits of using the IFRS for potential investors

Improving the quality

Benefits of using the IFRS for the state

Strengthening the capital

Benefits of using the IFRS for the state

Strengthening the capital

International Accounting Standards Board

The main goal of the IASB is

International Accounting Standards Board

The main goal of the IASB is

The IFRS development process

Creation of a Preparatory Committee from a wide

The IFRS development process

Creation of a Preparatory Committee from a wide

The IFRS development process

2. Development and publication of the original document

The IFRS development process

2. Development and publication of the original document

The IFRS development process

3. Preparation of a working draft of the

The IFRS development process

3. Preparation of a working draft of the

The IFRS development process

4. Issue of the final international financial reporting

The IFRS development process

4. Issue of the final international financial reporting

The IFRS development process

5. Introduction of the standard – in most

The IFRS development process

5. Introduction of the standard – in most

Types of standards

IAS - International accounting standards - were issued until

Types of standards

IAS - International accounting standards - were issued until

Types of standards

In addition, there are interpretations to the standards (sequences)

Types of standards

In addition, there are interpretations to the standards (sequences)

Bookkeeping

Accounting and storage of accounting documents are organized by the head

Bookkeeping

Accounting and storage of accounting documents are organized by the head

Requirements for the chief accountant in Russia

For chief accountants of

Requirements for the chief accountant in Russia

For chief accountants of

Bookkeeping

The totality of accounting methods forms the accounting policy of the

Bookkeeping

The totality of accounting methods forms the accounting policy of the

Accounting objects

facts of economic life;

assets;

liabilities;

sources of funding

Accounting objects

facts of economic life;

assets;

liabilities;

sources of funding

Accounting objects

A fact of economic life is a transaction, event,

Accounting objects

A fact of economic life is a transaction, event,

Source documents

Mandatory details of the document:

1) the title of the

Source documents

Mandatory details of the document:

1) the title of the

In addition to the required details, extra information can be included

In addition to the required details, extra information can be included

Source documents

The primary accounting document must be drawn up when

Source documents

The primary accounting document must be drawn up when

Source documents

Requirements of the chief accountant in writing form that

Source documents

Requirements of the chief accountant in writing form that

Source documents

The primary accounting document is drawn up on paper

Source documents

The primary accounting document is drawn up on paper

The documents must be kept in the form in which they

The documents must be kept in the form in which they

Source documents in Russia

The documents are prepared in Russian. If the

Source documents in Russia

The documents are prepared in Russian. If the

The date of drawing up the primary document is the day

The date of drawing up the primary document is the day

When drawing up primary documents, you can draw up several related

When drawing up primary documents, you can draw up several related

It is possible to draw up lasting facts of economic life

It is possible to draw up lasting facts of economic life

It is allowed to use as primary documents that one that

It is allowed to use as primary documents that one that

The list of persons entitled to sign documents is established by

The list of persons entitled to sign documents is established by

Bookkeeping

The data contained in primary accounting documents are subject to timely

Bookkeeping

The data contained in primary accounting documents are subject to timely

Financial statements

The financial statements should provide a reliable representation of

Financial statements

The financial statements should provide a reliable representation of

The unprecedented thickness of this report protected it from the danger

The unprecedented thickness of this report protected it from the danger

Financial statements

There are three types of lying: bragging, lying, and

Financial statements

There are three types of lying: bragging, lying, and

Отчетность в высказываниях

Automation can never completely replace accounting. It is not

Отчетность в высказываниях

Automation can never completely replace accounting. It is not

Отчетность в высказываниях

If you want to take control of your life,

Отчетность в высказываниях

If you want to take control of your life,

Financial statements

Financial statements are provided to external users of information

Users

Financial statements

Financial statements are provided to external users of information

Users

Who are external users?

Shareholders

Investors

Suppliers

Users with direct financial interest

Who are external users?

Shareholders

Investors

Suppliers

Users with direct financial interest

Who are external users?

Tax authorities

Banks

Government bodies

Auditing companies

Who are external users?

Tax authorities

Banks

Government bodies

Auditing companies

Who are external users?

Exchanges

Statistical bodies

Judiciary

Users without financial

Who are external users?

Exchanges

Statistical bodies

Judiciary

Users without financial

What is reporting for?

Analysis of financial condition

Evaluation of the

What is reporting for?

Analysis of financial condition

Evaluation of the

Assumptions of Formation of Financial Reporting Indicators

The assets and liabilities

Assumptions of Formation of Financial Reporting Indicators

The assets and liabilities

Assumptions of Formation of Financial Reporting Indicators

The organization will continue

Assumptions of Formation of Financial Reporting Indicators

The organization will continue

Assumptions of Formation of Financial Reporting Indicators

Business continuity - going

Assumptions of Formation of Financial Reporting Indicators

Business continuity - going

Assumptions of Formation of Financial Reporting Indicators

The accounting policy adopted

Assumptions of Formation of Financial Reporting Indicators

The accounting policy adopted

Assumptions of Formation of Financial Reporting Indicators

They are reflected in

Assumptions of Formation of Financial Reporting Indicators

They are reflected in

General requirements for financial statements

The reporting should give a reliable

General requirements for financial statements

The reporting should give a reliable

Financial statements

Annual financial statements consist of a balance sheet, a statement

Financial statements

Annual financial statements consist of a balance sheet, a statement

Financial statements

It is mandatory to draw up annual financial statements (for

Financial statements

It is mandatory to draw up annual financial statements (for

Financial statements

The financial statements are considered to be drawn up after

Financial statements

The financial statements are considered to be drawn up after

Financial statements

State information resource - a set of financial statements of

Financial statements

State information resource - a set of financial statements of

Accounting method

Accounting method

Method elements

Traditionally, there are 8 elements of the accounting method:

-

Method elements

Traditionally, there are 8 elements of the accounting method:

-

Inventory

Inventory is a check of the compliance of the actual

Inventory

Inventory is a check of the compliance of the actual

Inventory - documents

1. Order to conduct an inventory

2. Inventory list

Inventory - documents

1. Order to conduct an inventory

2. Inventory list

Inventory - results

1. Surplus (other incomes at market prices (fair

Inventory - results

1. Surplus (other incomes at market prices (fair

Natural loss

Methodological recommendations for the development of norms of natural

Natural loss

Methodological recommendations for the development of norms of natural

Example

The frozen berry was received on 08/10/19. Net weight 1000 kg.

The

Example

The frozen berry was received on 08/10/19. Net weight 1000 kg.

The

Example

Losses during storage of berries released on 12/14/19 (4 months 5

Example

Losses during storage of berries released on 12/14/19 (4 months 5

The culprit has not been identified

Letter of the Ministry of Finance

The culprit has not been identified

Letter of the Ministry of Finance

Doubtful accounts receivable

The receivables of the organization are considered doubtful

Doubtful accounts receivable

The receivables of the organization are considered doubtful

Doubtful accounts receivable

Since 2011, organizations are required to create reserves

Doubtful accounts receivable

Since 2011, organizations are required to create reserves

Doubtful accounts receivable

Accounts receivable are recognized as doubtful from the

Doubtful accounts receivable

Accounts receivable are recognized as doubtful from the

Monetary measurement

Accounting objects are subject to monetary measurement.

Monetary measurement of accounting

Monetary measurement

Accounting objects are subject to monetary measurement.

Monetary measurement of accounting

Calculation (costing)

In some cases, it is not possible to directly determine

Calculation (costing)

In some cases, it is not possible to directly determine

Costing - Cost Allocation

Let the transported goods occupy the following

Costing - Cost Allocation

Let the transported goods occupy the following

Costing - Cost Allocation

Accordingly, the amount of transportation costs can

Costing - Cost Allocation

Accordingly, the amount of transportation costs can

Costing - Cost Allocation

Let the transported goods occupy the following

Costing - Cost Allocation

Let the transported goods occupy the following

Costing - Cost Allocation

Accordingly, the amount of transportation costs can

Costing - Cost Allocation

Accordingly, the amount of transportation costs can

Recommendation

Try to account as many cost drivers as possible.

For this, it

Recommendation

Try to account as many cost drivers as possible.

For this, it

Costing - Cost Allocation

Let the transported goods occupy the following

Costing - Cost Allocation

Let the transported goods occupy the following

Costing - Cost Allocation

First, let's calculate the distribution ratios for

Costing - Cost Allocation

First, let's calculate the distribution ratios for

Costing - Cost Allocation

Then we calculate the total bases for

Costing - Cost Allocation

Then we calculate the total bases for

Costing - Cost Allocation

Let's add one more factor to the

Costing - Cost Allocation

Let's add one more factor to the

Costing - Cost Allocation

Costing - Cost Allocation

Costing - Cost Allocation

The multi-factor distribution allows you to take

Costing - Cost Allocation

The multi-factor distribution allows you to take

Accounts

In accordance with the classical definition, an account is a special

Accounts

In accordance with the classical definition, an account is a special

Активные счета – на них отражается имущество организации

Dt

Ct

Bal 100

200

300

500

Turn Dt 1000

150

350

Turn Ct 500

Materials

Bal 600

Bal end

Активные счета – на них отражается имущество организации

Dt

Ct

Bal 100

200

300

500

Turn Dt 1000

150

350

Turn Ct 500

Materials

Bal 600

Bal end

Пассивные счета – на них отражаются источники формирования имущество организации

Dt

Ct

Bal 100

200

300

500

Turn Dt 1000

750

350

Turn

Пассивные счета – на них отражаются источники формирования имущество организации

Dt

Ct

Bal 100

200

300

500

Turn Dt 1000

750

350

Turn

Активные счета – на них отражается имущество организации

Dt

Ct

Bal 100

200

300

500

Turn Dt 1000

650

550

Turn Ct 1200

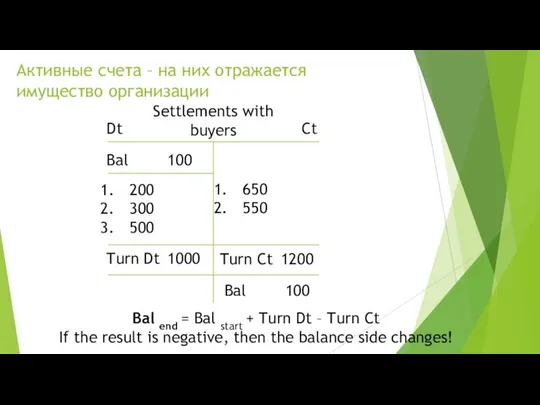

Settlements with

Активные счета – на них отражается имущество организации

Dt

Ct

Bal 100

200

300

500

Turn Dt 1000

650

550

Turn Ct 1200

Settlements with

Double entry

The simultaneous reflection of a debit transaction on one

Double entry

The simultaneous reflection of a debit transaction on one

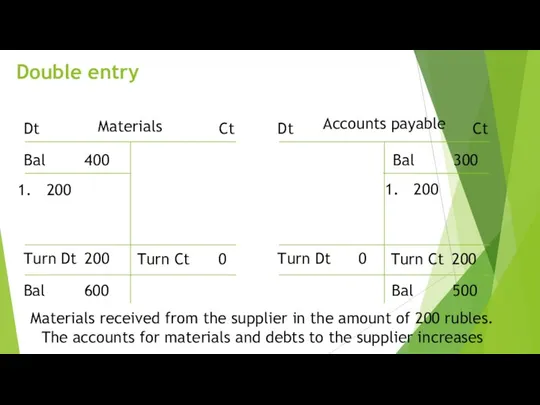

Double entry

Dt

Ct

Bal 400

200

Turn Dt 200

Turn Ct 0

Materials

Bal 600

Dt

Ct

Bal 300

Turn Dt 0

200

Turn Ct 200

Accounts payable

Bal 500

Materials received from the

Double entry

Dt

Ct

Bal 400

200

Turn Dt 200

Turn Ct 0

Materials

Bal 600

Dt

Ct

Bal 300

Turn Dt 0

200

Turn Ct 200

Accounts payable

Bal 500

Materials received from the

Double entry

There are 4 types of business transactions in total

Asset

Double entry

There are 4 types of business transactions in total

Asset

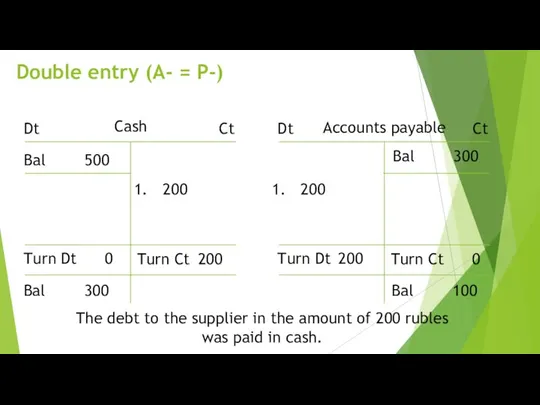

Double entry (A- = P-)

Dt

Ct

Bal 500

200

Turn Dt 0

Turn Ct 200

Cash

Bal 300

Dt

Ct

Bal 300

Turn Dt 200

200

Turn Ct 0

Accounts payable

Bal 100

The

Double entry (A- = P-)

Dt

Ct

Bal 500

200

Turn Dt 0

Turn Ct 200

Cash

Bal 300

Dt

Ct

Bal 300

Turn Dt 200

200

Turn Ct 0

Accounts payable

Bal 100

The

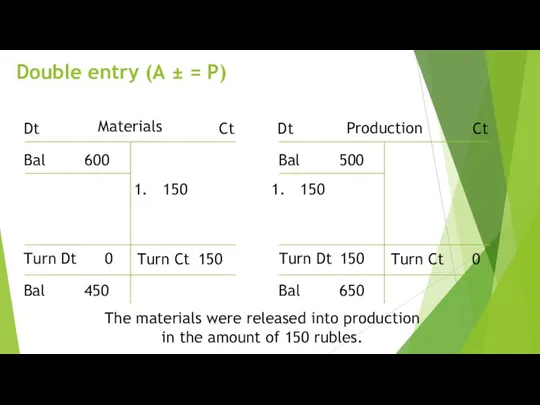

Double entry (A ± = P)

Dt

Ct

Bal 600

150

Turn Dt 0

Turn Ct 150

Materials

Bal 450

Dt

Ct

Bal 500

Turn Dt 150

150

Turn Ct 0

Production

Bal 650

The

Double entry (A ± = P)

Dt

Ct

Bal 600

150

Turn Dt 0

Turn Ct 150

Materials

Bal 450

Dt

Ct

Bal 500

Turn Dt 150

150

Turn Ct 0

Production

Bal 650

The

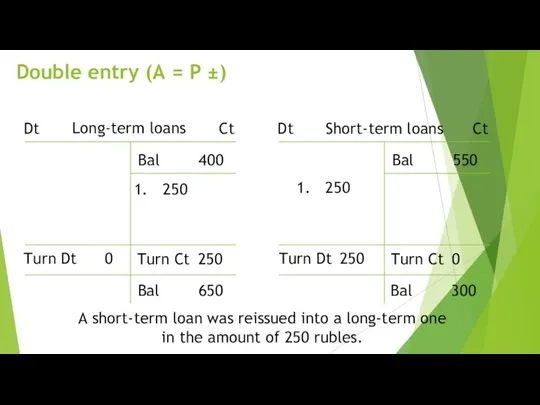

Double entry (A = P ±)

Dt

Ct

Bal 400

250

Turn Dt 0

Turn Ct 250

Long-term loans

Bal 650

Dt

Ct

Bal 550

Turn

Double entry (A = P ±)

Dt

Ct

Bal 400

250

Turn Dt 0

Turn Ct 250

Long-term loans

Bal 650

Dt

Ct

Bal 550

Turn

Accounting objects

Accounting objects

Assets

Assets are resources whose value can be estimated and from which

Assets

Assets are resources whose value can be estimated and from which

Cash

Cash means cash and non-cash funds of an organization stored in

Cash

Cash means cash and non-cash funds of an organization stored in

Cash

Non-cash funds are kept in current accounts in banks. Currently, almost

Cash

Non-cash funds are kept in current accounts in banks. Currently, almost

Cash

In some cases, transactions on current accounts may be blocked. This

Cash

In some cases, transactions on current accounts may be blocked. This

Cash

To store currency, organizations may use foreign currency accounts. However, on

Cash

To store currency, organizations may use foreign currency accounts. However, on

Cash

In addition to current and foreign currency accounts, organizations may have

Cash

In addition to current and foreign currency accounts, organizations may have

Cash

Operations with cash is called cash flow.

The cash flows of the

Cash

Operations with cash is called cash flow.

The cash flows of the

Cash

a) receipts from the sale of products and goods to buyers;

b)

Cash

a) receipts from the sale of products and goods to buyers;

b)

Cash

An entity's cash flows from transactions related to the acquisition, creation

Cash

An entity's cash flows from transactions related to the acquisition, creation

Cash

a) payments to suppliers and employees of the organization in connection

Cash

a) payments to suppliers and employees of the organization in connection

Cash

The cash flows of the organization from operations related to the

Cash

The cash flows of the organization from operations related to the

Cash

a) monetary payments of owners to the capital, proceeds from the

Cash

a) monetary payments of owners to the capital, proceeds from the

Cash documents

Monetary documents are special protected in some way documents (pin

Cash documents

Monetary documents are special protected in some way documents (pin

Cash equivalents

Cash equivalents are highly liquid financial investments that can

Cash equivalents

Cash equivalents are highly liquid financial investments that can

Short-term financial investments

Financial investments are investments in other companies made

Short-term financial investments

Financial investments are investments in other companies made

Short-term financial investments

The main differences between short-term financial investments and

Short-term financial investments

The main differences between short-term financial investments and

Short-term financial investments

All financial investments are divided into two groups:

-

Short-term financial investments

All financial investments are divided into two groups:

-

Short-term financial investments

If the current market value can be determined

Short-term financial investments

If the current market value can be determined

Accounts receivables

Accounts receivable are amounts owed to this organization by other

Accounts receivables

Accounts receivable are amounts owed to this organization by other

Accounts receivables

Accounts receivable are funds withdrawn from the organization's turnover. At

Accounts receivables

Accounts receivable are funds withdrawn from the organization's turnover. At

Accounts receivables

A receivable is recognized as doubtful if the organization has

Accounts receivables

A receivable is recognized as doubtful if the organization has

Accounts receivables

Organizations can use several tools to manage doubtful accounts receivable.

Accounts receivables

Organizations can use several tools to manage doubtful accounts receivable.

Accounts receivables

An extreme case of doubtful accounts receivable is bad accounts

Accounts receivables

An extreme case of doubtful accounts receivable is bad accounts

Accounts receivables

In addition the debtors of the organization may be its

Accounts receivables

In addition the debtors of the organization may be its

VAT

The amounts of VAT on the purchased values are actually a

VAT

The amounts of VAT on the purchased values are actually a

Stocks

Inventories are one of the main group of assets, which

Stocks

Inventories are one of the main group of assets, which

Fixed assets

Fixed assets are assets that have a tangible form

Fixed assets

Fixed assets are assets that have a tangible form

Fixed assets

- buildings and constructions. In recent years, this subgroup

Fixed assets

- buildings and constructions. In recent years, this subgroup

Fixed assets

Organizations are given the right to revalue fixed assets,

Fixed assets

Organizations are given the right to revalue fixed assets,

Intangible assets

These are non-monetary assets protected by certain copyrights. These

Intangible assets

These are non-monetary assets protected by certain copyrights. These

Goodwill

One of the most specific types of intangible assets is goodwill

Goodwill

One of the most specific types of intangible assets is goodwill

Investments in future non-current assets

Fixed assets and intangibles sometimes have

Investments in future non-current assets

Fixed assets and intangibles sometimes have

Profitable investments in material assets

Income investments in tangible assets include

Profitable investments in material assets

Income investments in tangible assets include

Long-term financial investments

Long-term financial investments are investments in securities for

Long-term financial investments

Long-term financial investments are investments in securities for

Capital - sources of property formation

The sources of property formation

Capital - sources of property formation

The sources of property formation

Accounts payable

Accounts payable is a debt owed by this organization

Accounts payable

Accounts payable is a debt owed by this organization

Accounts payable

Accounts payable to suppliers and contractors for goods, works,

Accounts payable

Accounts payable to suppliers and contractors for goods, works,

Accounts payable

When the liability is extinguished in cash or other

Accounts payable

When the liability is extinguished in cash or other

Accounts payable

Accounts payable

Short-term credit and loans

Short-term credits and short-term loans provided to organizations

Short-term credit and loans

Short-term credits and short-term loans provided to organizations

Provisions

Provisions are liabilities with an uncertain amount or period that either

Provisions

Provisions are liabilities with an uncertain amount or period that either

Long credit and loans

Long-term credit and borrowings provided to organizations by

Long credit and loans

Long-term credit and borrowings provided to organizations by

Equity

The authorized capital is the valuation of the organization's property, which

Equity

The authorized capital is the valuation of the organization's property, which

Equity

The share in the authorized capital belonging to the participants of

Equity

The share in the authorized capital belonging to the participants of

Equity

Additional capital ("air capital") - capital resulting from the revaluation of

Equity

Additional capital ("air capital") - capital resulting from the revaluation of

Equity

In addition to the revaluation of fixed assets, share premium can

Equity

In addition to the revaluation of fixed assets, share premium can

Equity

Profit of the organization:

- gross profit, defined as the difference between

Equity

Profit of the organization:

- gross profit, defined as the difference between

Equity

Part of the profit can be used to pay dividends, and

Equity

Part of the profit can be used to pay dividends, and

Построение схемы Налоги и сборы в РФ

Построение схемы Налоги и сборы в РФ Действующие налоги и сборы. Специальные налоговые режимы в РФ

Действующие налоги и сборы. Специальные налоговые режимы в РФ Антикризисное управление предприятием

Антикризисное управление предприятием Чистый оборотный капитал организации

Чистый оборотный капитал организации Этапы становления бухгалтерского учета как науки

Этапы становления бухгалтерского учета как науки Проект бюджета на 2020 год и плановый период 2021 и 2022 годов города Котельнича Кировской области

Проект бюджета на 2020 год и плановый период 2021 и 2022 годов города Котельнича Кировской области Тема лекции Объекты учета затрат в системе управленческого учета

Тема лекции Объекты учета затрат в системе управленческого учета Совершенствоание организации сбытовой деятельности предприятия ОАО Агрокомбинат Южный

Совершенствоание организации сбытовой деятельности предприятия ОАО Агрокомбинат Южный Таможенная стоимость и методы её определения

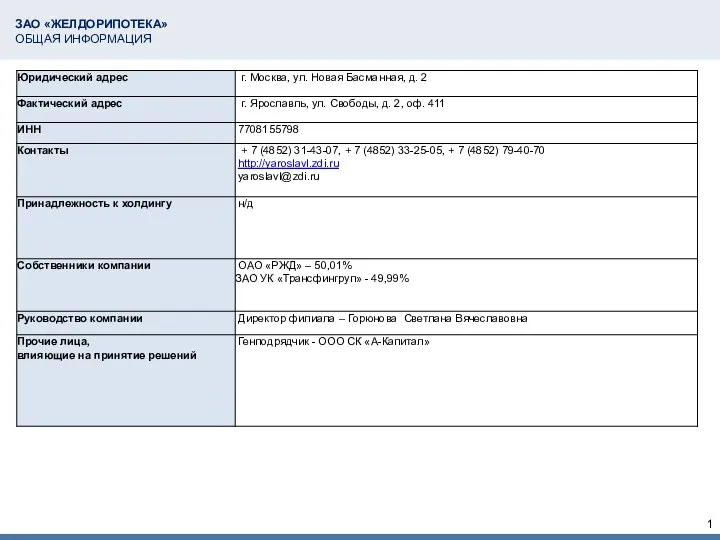

Таможенная стоимость и методы её определения ЗАО Желдорипотека. Общая информация

ЗАО Желдорипотека. Общая информация Виды и классификация затрат на производство

Виды и классификация затрат на производство Доходы бюджетов

Доходы бюджетов Бюджетный процесс: совставление, рассмотрение, утверждение и исполнение бюджетов п хвеньям бюджетной системы

Бюджетный процесс: совставление, рассмотрение, утверждение и исполнение бюджетов п хвеньям бюджетной системы Добровольное медицинское страхование

Добровольное медицинское страхование ВКР: Прогнозирование величины арендной платы

ВКР: Прогнозирование величины арендной платы Расчет затрат на создание ИС

Расчет затрат на создание ИС Учёт на торговом объекте

Учёт на торговом объекте Учет денежных средств

Учет денежных средств Сравнительный подход

Сравнительный подход Метод бухгалтерского учета

Метод бухгалтерского учета Ипотечные и кредитные каникулы

Ипотечные и кредитные каникулы Valuation Финансовый клуб ВШМ

Valuation Финансовый клуб ВШМ Кредитные карты. Кредит Европа Банк

Кредитные карты. Кредит Европа Банк Стратегия продвижения банковских продуктов на примере АКБ СОЮЗ (ОАО)

Стратегия продвижения банковских продуктов на примере АКБ СОЮЗ (ОАО) Презентация ОТ -2019

Презентация ОТ -2019 Листовка для информирования ЗП 10%

Листовка для информирования ЗП 10% Практика использования платёжных банковских карт в коммерческом банке и пути её совершенствования

Практика использования платёжных банковских карт в коммерческом банке и пути её совершенствования Биржа LME

Биржа LME