- ARCH and GARCH. Modeling Volatility Dynamics

Содержание

- 2. Modeling Unequal Variability Equal Variability: Homoscedasticity Unequal Variability: Heteroscedasticity Means any variability (around the mean) that

- 3. What These Acronym Mean? ARCH Autoregressive Conditional Heteroscedasticity GARCH Generalized ARCH

- 4. Information in e2 Let εt have the mean 0 and the variance σt. Let et be

- 5. ARCH Modeling of σt2. ARCH(1) ARCH as AR(1) on

- 6. GARCH GARCH(1) GARCH (1) as ARMA(1,1) on

- 7. Asymmetry in GARCH - TARCH TARCH(1,1) d = 1 if εt 0

- 8. Asymmetry in GARCH - EGARCH EGARCH(1,1)

- 10. Скачать презентацию

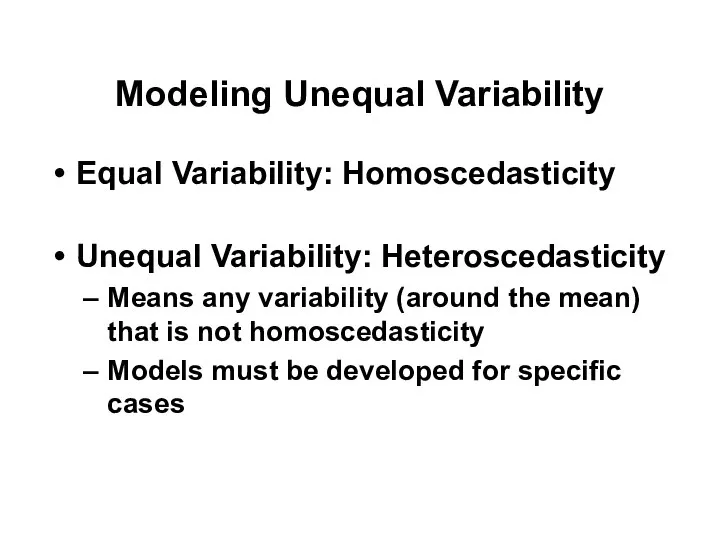

Modeling Unequal Variability

Equal Variability: Homoscedasticity

Unequal Variability: Heteroscedasticity

Means any variability (around the

Modeling Unequal Variability

Equal Variability: Homoscedasticity

Unequal Variability: Heteroscedasticity

Means any variability (around the

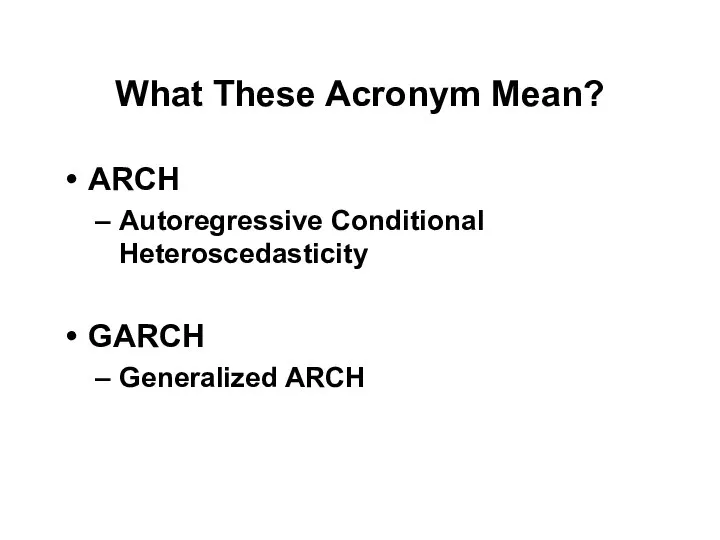

What These Acronym Mean?

ARCH

Autoregressive Conditional Heteroscedasticity

GARCH

Generalized ARCH

What These Acronym Mean?

ARCH

Autoregressive Conditional Heteroscedasticity

GARCH

Generalized ARCH

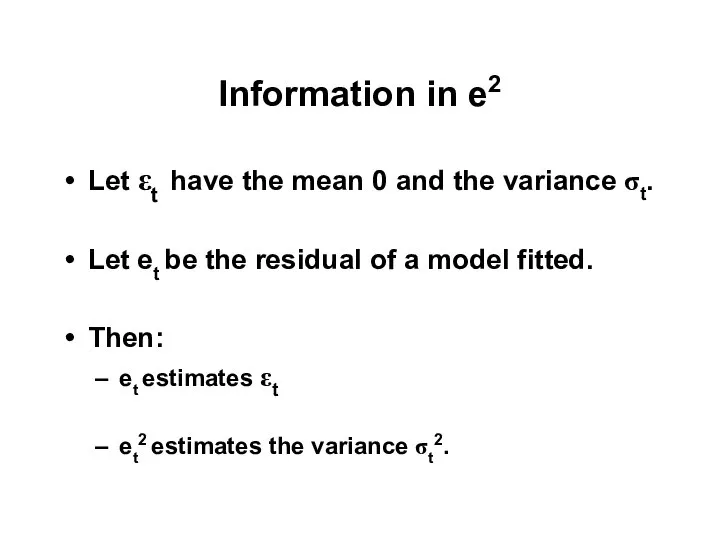

Information in e2

Let εt have the mean 0 and the variance

Information in e2

Let εt have the mean 0 and the variance

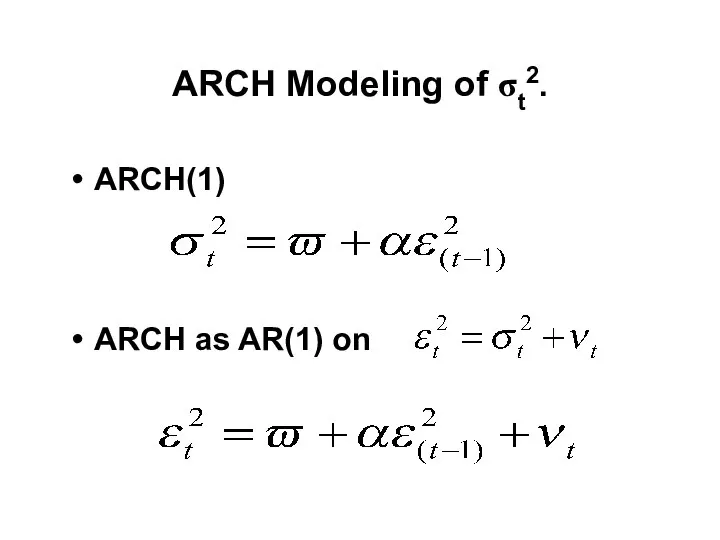

ARCH Modeling of σt2.

ARCH(1)

ARCH as AR(1) on

ARCH Modeling of σt2.

ARCH(1)

ARCH as AR(1) on

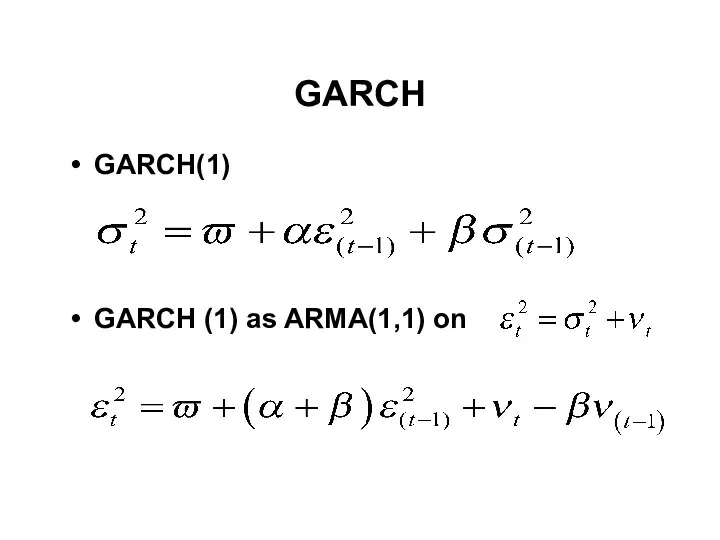

GARCH

GARCH(1)

GARCH (1) as ARMA(1,1) on

GARCH

GARCH(1)

GARCH (1) as ARMA(1,1) on

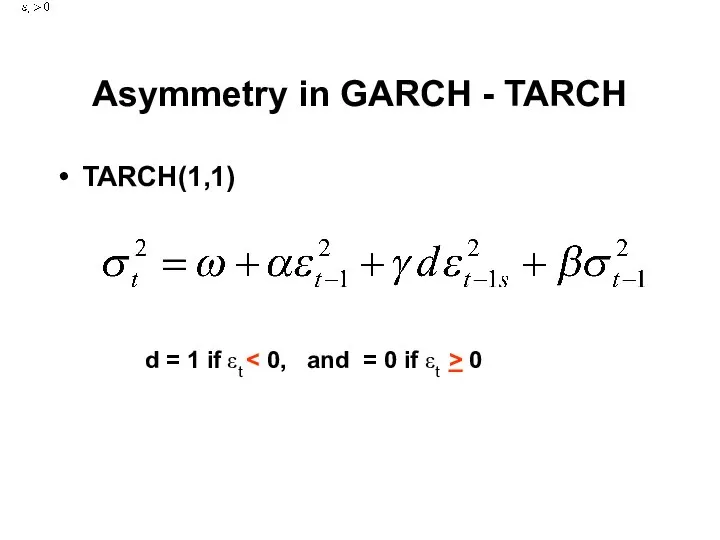

Asymmetry in GARCH - TARCH

TARCH(1,1)

d = 1 if εt < 0,

Asymmetry in GARCH - TARCH

TARCH(1,1)

d = 1 if εt < 0,

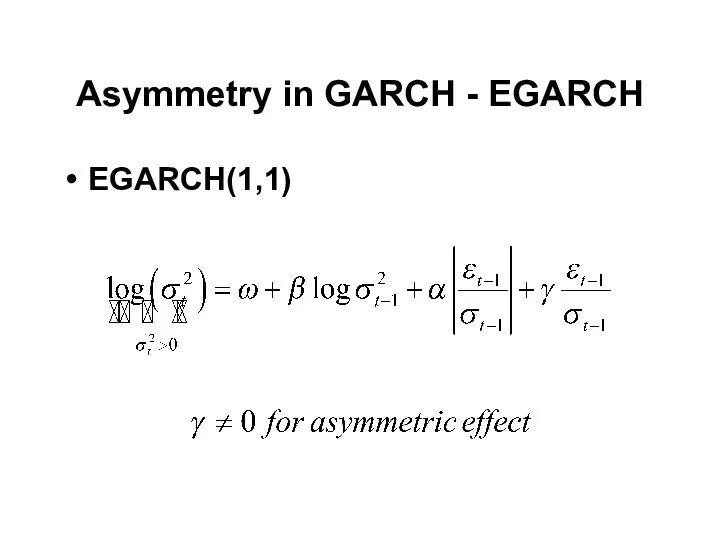

Asymmetry in GARCH - EGARCH

EGARCH(1,1)

Asymmetry in GARCH - EGARCH

EGARCH(1,1)

Объект социально-экономической статистики

Объект социально-экономической статистики Методология научных исследований. Планирование экспериментов

Методология научных исследований. Планирование экспериментов Тренажёр. Табличное умножение

Тренажёр. Табличное умножение Современный урок математики в условиях реализации ФГОС НОО и «Концепции развития математического образования в РФ»

Современный урок математики в условиях реализации ФГОС НОО и «Концепции развития математического образования в РФ» Действия с дробями

Действия с дробями Отношения. Пропорции. Подготовка к контрольной работе. 6 класс

Отношения. Пропорции. Подготовка к контрольной работе. 6 класс Умножение натуральных чисел. Задачи

Умножение натуральных чисел. Задачи Задачи раскраски графов. Вершинная раскраска

Задачи раскраски графов. Вершинная раскраска Графики функций

Графики функций Древние меры длин

Древние меры длин Презентация по математике "Умножение одночленов. Возведение одночленов в степень" - скачать бесплатно

Презентация по математике "Умножение одночленов. Возведение одночленов в степень" - скачать бесплатно Длина окружности. Площадь круга

Длина окружности. Площадь круга Стереометрия. Геометрические тела

Стереометрия. Геометрические тела Математическая регата (8 класс)

Математическая регата (8 класс) Презентация по математике "ДЕЛИМОЕ И ДЕЛИТЕЛЬ (2 КЛАСС)" - скачать бесплатно

Презентация по математике "ДЕЛИМОЕ И ДЕЛИТЕЛЬ (2 КЛАСС)" - скачать бесплатно Числові характеристики випадкових величин, показники варіації; первинна статистична обробка кількісних ознак

Числові характеристики випадкових величин, показники варіації; первинна статистична обробка кількісних ознак Многогранник с двумя основаниями

Многогранник с двумя основаниями Презентация по математике "Чебышев Пафнутий Львович" - скачать

Презентация по математике "Чебышев Пафнутий Львович" - скачать  Тема «Движения» в задачах ЕГЭ

Тема «Движения» в задачах ЕГЭ Презентация по математике "Решение квадратных уравнений по формуле" - скачать бесплатно

Презентация по математике "Решение квадратных уравнений по формуле" - скачать бесплатно Тренажер. Единицы площади

Тренажер. Единицы площади Задачи на построение

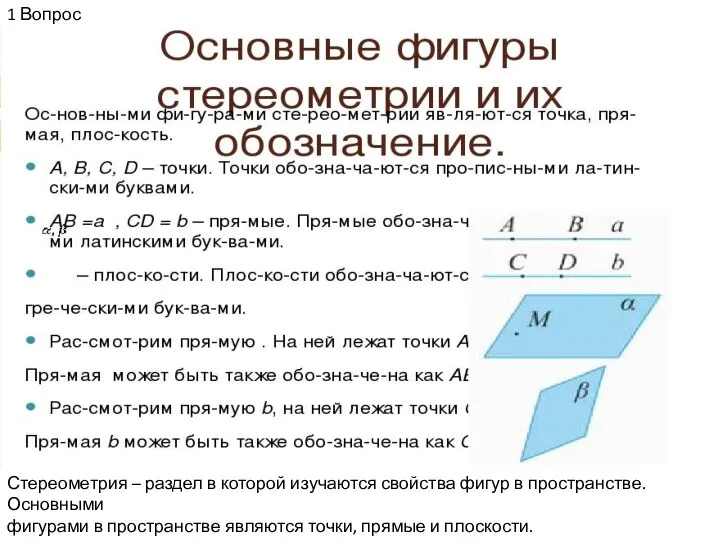

Задачи на построение Основные фигуры стереометрии и их обозначение

Основные фигуры стереометрии и их обозначение Основные понятия теории множеств

Основные понятия теории множеств Множества. Операция над множествами

Множества. Операция над множествами Путешествие в сказку математика

Путешествие в сказку математика Сложение однозначных чисел переходом через десяток вида +4

Сложение однозначных чисел переходом через десяток вида +4 Презентация по математике "Викторина. Ребусы в картинках" - скачать

Презентация по математике "Викторина. Ребусы в картинках" - скачать