- Introduction to insurance. ExigenServices

Содержание

- 2. INTRODUCTION TO INSURANCE FUNDAMENTALS AND TERMINOLOGY

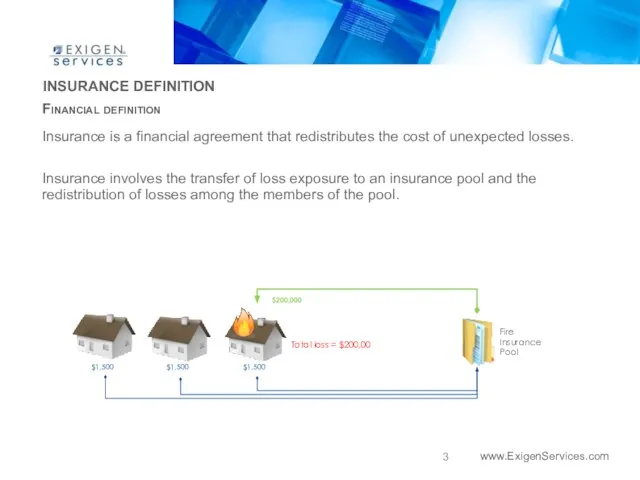

- 3. INSURANCE DEFINITION Insurance is a financial agreement that redistributes the cost of unexpected losses. Insurance involves

- 4. INSURANCE DEFINITION Legal definition Insurance is a contractual arrangement whereby one party agrees to compensate another

- 5. FUNDAMENTAL TERMS Loss A typical insurable loss is an undesired, unplanned reduction of economic value. Direct

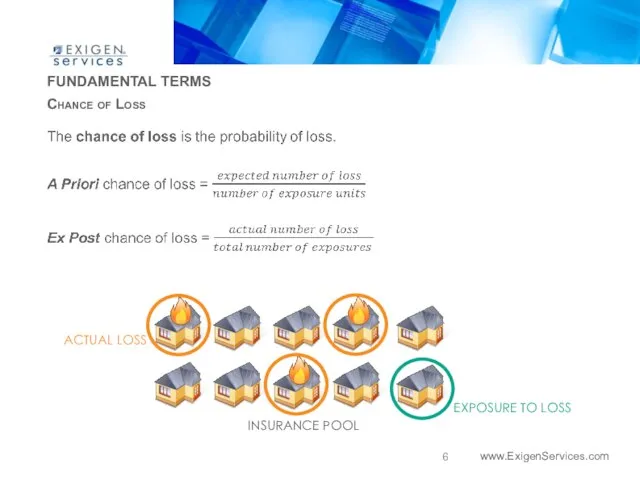

- 6. FUNDAMENTAL TERMS Chance of Loss INSURANCE POOL EXPOSURE TO LOSS ACTUAL LOSS

- 7. FUNDAMENTAL TERMS Peril and Hazard. Proximate cause A peril is defined as the cause of the

- 8. RISK Definitions of Risk Risk is a variation in possible outcomes of an event based on

- 9. RISK Sources of Risk Common sources of pure risk include property risks; liability risks, and life,

- 10. THE MATHEMATICAL BASIS FOR INSRANCE Law of Large Numbers The law states the greater the number

- 12. Скачать презентацию

INTRODUCTION TO INSURANCE

FUNDAMENTALS AND TERMINOLOGY

INTRODUCTION TO INSURANCE

FUNDAMENTALS AND TERMINOLOGY

INSURANCE DEFINITION

Insurance is a financial agreement that redistributes the cost of

INSURANCE DEFINITION

Insurance is a financial agreement that redistributes the cost of

INSURANCE DEFINITION

Legal definition

Insurance is a contractual arrangement whereby one party agrees

INSURANCE DEFINITION

Legal definition

Insurance is a contractual arrangement whereby one party agrees

FUNDAMENTAL TERMS

Loss

A typical insurable loss is an undesired, unplanned reduction

FUNDAMENTAL TERMS

Loss

A typical insurable loss is an undesired, unplanned reduction

FUNDAMENTAL TERMS

Chance of Loss

INSURANCE POOL

EXPOSURE TO LOSS

ACTUAL LOSS

FUNDAMENTAL TERMS

Chance of Loss

INSURANCE POOL

EXPOSURE TO LOSS

ACTUAL LOSS

FUNDAMENTAL TERMS

Peril and Hazard. Proximate cause

A peril is defined as the

FUNDAMENTAL TERMS

Peril and Hazard. Proximate cause

A peril is defined as the

RISK

Definitions of Risk

Risk is a variation in possible outcomes of an

RISK

Definitions of Risk

Risk is a variation in possible outcomes of an

RISK

Sources of Risk

Common sources of pure risk include property risks; liability

RISK

Sources of Risk

Common sources of pure risk include property risks; liability

THE MATHEMATICAL BASIS FOR INSRANCE

Law of Large Numbers

The law states the

THE MATHEMATICAL BASIS FOR INSRANCE

Law of Large Numbers

The law states the

Мать-одиночка. Материнский капитал. Задача

Мать-одиночка. Материнский капитал. Задача Единый урок государственности

Единый урок государственности Сертификация. Обязательное подтверждение соответствия

Сертификация. Обязательное подтверждение соответствия Имущественный комплекс,

Имущественный комплекс, Институт голосования на выборах: опыт России и зарубежных стран

Институт голосования на выборах: опыт России и зарубежных стран Правовой режим права собственности. (тема 19)

Правовой режим права собственности. (тема 19) Документация по планировке территории, расположенной в городе нижнем Новгороде и районе Нижегородской области

Документация по планировке территории, расположенной в городе нижнем Новгороде и районе Нижегородской области Подготовка к ЕГЭ по обществознанию

Подготовка к ЕГЭ по обществознанию Государство, общество, личность: философско-правовые аспекты соотношения. Лекция 2

Государство, общество, личность: философско-правовые аспекты соотношения. Лекция 2 Основы трудового законодательства РК по охране труда

Основы трудового законодательства РК по охране труда Uluslararası İnsan Kaynakları Yönetimi

Uluslararası İnsan Kaynakları Yönetimi Уголовно-правовые средства борьбы с правонарушениями и правовое обучение личного состава в ВС РК. Тема № 3

Уголовно-правовые средства борьбы с правонарушениями и правовое обучение личного состава в ВС РК. Тема № 3 Сущность предпринимательства и его место в современном обществе

Сущность предпринимательства и его место в современном обществе Програма добровільного страхування цивільної відповідальності власників наземних транспортних засобів ДЦВ ONLINE

Програма добровільного страхування цивільної відповідальності власників наземних транспортних засобів ДЦВ ONLINE Правовая культура и правосознание

Правовая культура и правосознание Социальная ответственность предпринимательства

Социальная ответственность предпринимательства Формирование муниципального округа на территории муниципального образования Чарышский район Алтайского края

Формирование муниципального округа на территории муниципального образования Чарышский район Алтайского края Гражданственность

Гражданственность Основы уголовного права

Основы уголовного права Конвенция о правах ребенка

Конвенция о правах ребенка История коррупции в России

История коррупции в России Конституционное право России. Основы конституционного строя России. (Тема 3)

Конституционное право России. Основы конституционного строя России. (Тема 3) Заключение брака в Канаде

Заключение брака в Канаде Переход на работу в условиях введения профессиональных стандартов

Переход на работу в условиях введения профессиональных стандартов Уголовная ответственность несовершеннолетних

Уголовная ответственность несовершеннолетних Основы социального государства

Основы социального государства Уголовное право. 9 класс

Уголовное право. 9 класс Правовой статус человека и гражданина

Правовой статус человека и гражданина