- Презентация к уроку английского языка "Audit Planning" - скачать

Содержание

- 2. * Introduction- SCHEDULING AUDITS EQUIPMENT LISTS DISTANCE/MPG ANALYSIS AUDIT NOTIFICATION/ ENGAGEMENT LETTERS PRE-AUDIT QUESTIONNAIRE / INTERNAL

- 3. * PURPOSE OF AUDIT PLANNING WORK IS TO BE ADEQUATELY PLANNED. (IRP A204.1 IFTA A220.200). The

- 4. * The objectives (evaluation of the taxpayer’s system, ensure continued compliance, ensure proper revenue) are what

- 5. * Scope is the boundary of the audit and should be directly tied to the audit

- 6. * The methodology comprises the work involved in gathering and analyzing data to achieve the objectives.

- 7. * SELECTING THE CARRIER AND THE AUDIT PERIODS- How does your jurisdiction select audits? Random selection-

- 8. * SELECTING THE CARRIER AND THE AUDIT PERIODS- All jurisdictions have a certain amount of- Audit

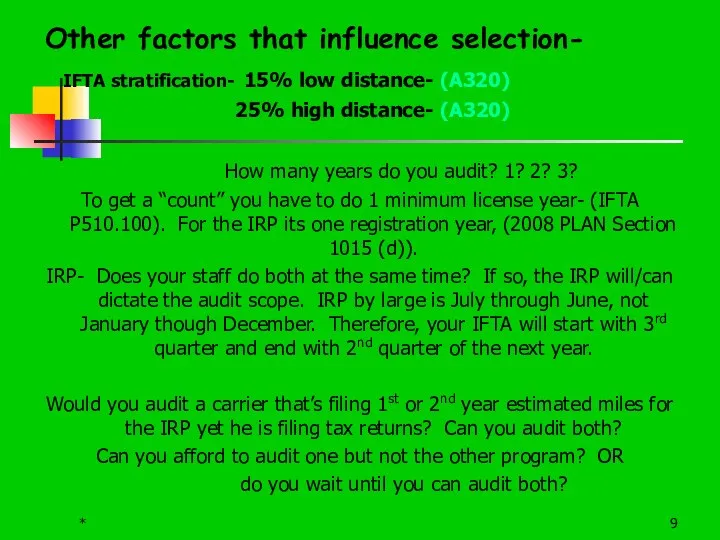

- 9. * Other factors that influence selection- IFTA stratification- 15% low distance- (A320) 25% high distance- (A320)

- 10. IRP gives 1 audit credit per audit year, IFTA doesn’t. Would you then expand a one

- 11. * The pre-audit contact. All communication should be documented in the audit file (IRP A600 &

- 12. * Equipment lists- a.k.a unit listing. Using IRP vehicle schedules to prepare equipment lists (IRP A700).

- 13. * Reconciling equipment lists. (Government vs. Carriers). Reconciliation of equipment lists will identify: Vehicles that are

- 14. * Contacting the carrier- a.k.a “your number is up”. Allow the carrier adequate time to gather

- 15. * Pre-audit questionnaire/Internal control questionnaire AGREEMENT TO PREPARE AND MAINTAIN RECORDS IN ACCORDANCE WITH THE INTERNATIONAL

- 16. FUEL RECORDS (IFTA Only): You must maintain original fuel source documents for each fuel type for

- 17. DECLARATION: The undersigned has read this document, and agrees to prepare and maintain records and report

- 19. Скачать презентацию

*

Introduction-

SCHEDULING AUDITS

EQUIPMENT LISTS

DISTANCE/MPG ANALYSIS

AUDIT NOTIFICATION/ ENGAGEMENT LETTERS

PRE-AUDIT QUESTIONNAIRE / INTERNAL CONTROL

*

Introduction-

SCHEDULING AUDITS

EQUIPMENT LISTS

DISTANCE/MPG ANALYSIS

AUDIT NOTIFICATION/ ENGAGEMENT LETTERS

PRE-AUDIT QUESTIONNAIRE / INTERNAL CONTROL

*

PURPOSE OF AUDIT PLANNING

WORK IS TO BE ADEQUATELY PLANNED. (IRP A204.1

*

PURPOSE OF AUDIT PLANNING

WORK IS TO BE ADEQUATELY PLANNED. (IRP A204.1

*

The objectives (evaluation of the taxpayer’s system, ensure continued compliance,

*

The objectives (evaluation of the taxpayer’s system, ensure continued compliance,

*

Scope is the boundary of the audit and should be directly

*

Scope is the boundary of the audit and should be directly

*

The methodology comprises the work involved in gathering and analyzing data

*

The methodology comprises the work involved in gathering and analyzing data

*

SELECTING THE CARRIER AND THE AUDIT PERIODS-

How does your jurisdiction

*

SELECTING THE CARRIER AND THE AUDIT PERIODS-

How does your jurisdiction

*

SELECTING THE CARRIER AND THE AUDIT PERIODS-

All jurisdictions have

*

SELECTING THE CARRIER AND THE AUDIT PERIODS-

All jurisdictions have

*

Other factors that influence selection-

IFTA stratification- 15% low distance-

*

Other factors that influence selection-

IFTA stratification- 15% low distance-

IRP gives 1 audit credit per audit year, IFTA doesn’t. Would

IRP gives 1 audit credit per audit year, IFTA doesn’t. Would

*

The pre-audit contact. All communication should be documented in the

*

The pre-audit contact. All communication should be documented in the

*

Equipment lists- a.k.a unit listing.

Using IRP vehicle schedules to prepare equipment

*

Equipment lists- a.k.a unit listing.

Using IRP vehicle schedules to prepare equipment

*

Reconciling equipment lists.

(Government vs. Carriers).

Reconciliation of equipment lists

*

Reconciling equipment lists.

(Government vs. Carriers).

Reconciliation of equipment lists

*

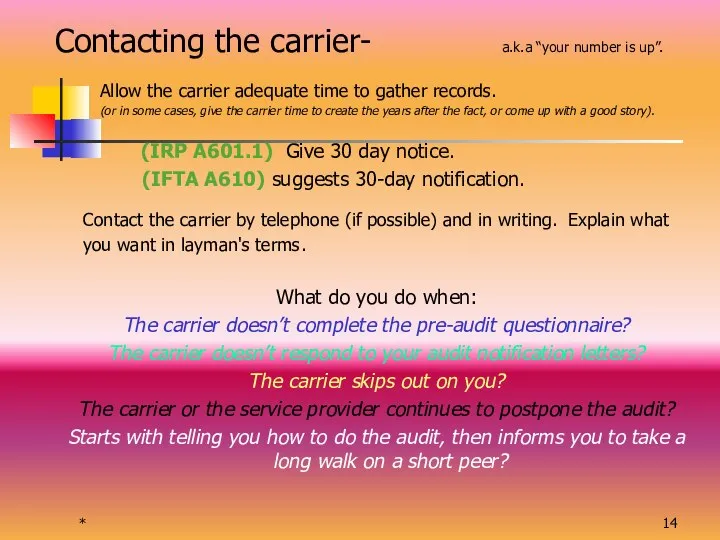

Contacting the carrier- a.k.a “your number is up”.

Allow the

*

Contacting the carrier- a.k.a “your number is up”.

Allow the

*

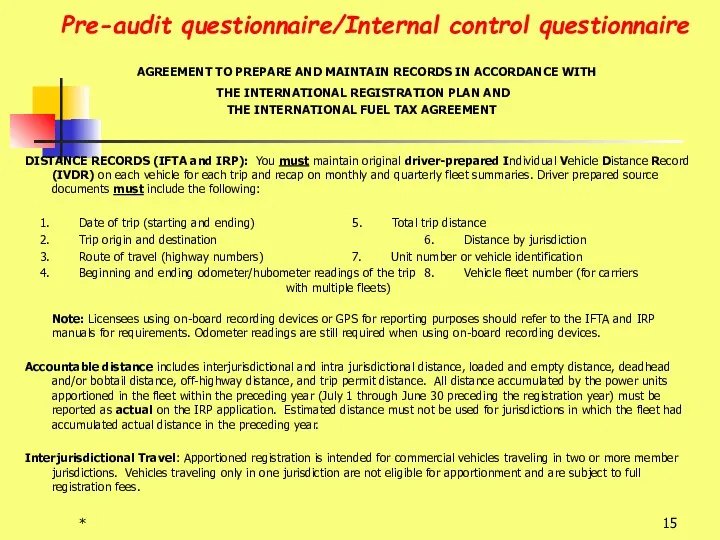

Pre-audit questionnaire/Internal control questionnaire

AGREEMENT TO PREPARE AND MAINTAIN RECORDS IN

*

Pre-audit questionnaire/Internal control questionnaire

AGREEMENT TO PREPARE AND MAINTAIN RECORDS IN

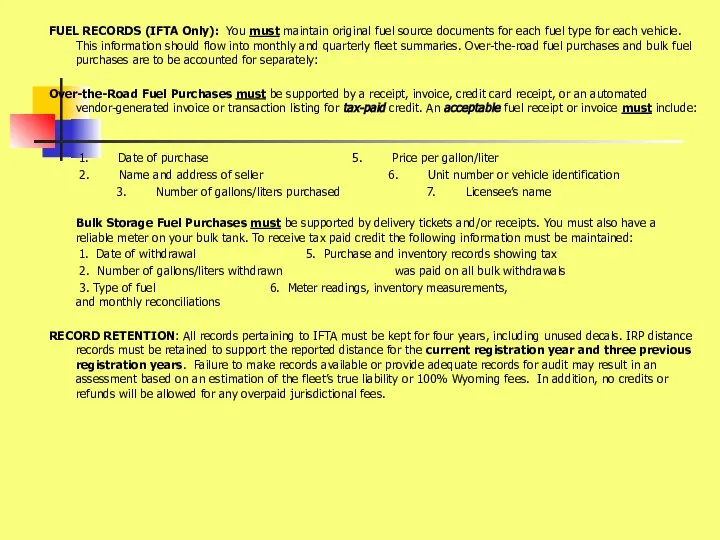

FUEL RECORDS (IFTA Only): You must maintain original fuel source documents

FUEL RECORDS (IFTA Only): You must maintain original fuel source documents

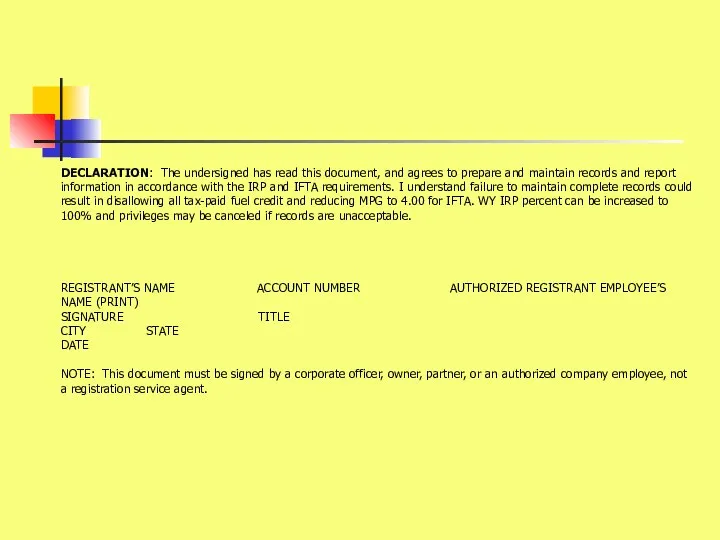

DECLARATION: The undersigned has read this document, and agrees to prepare

DECLARATION: The undersigned has read this document, and agrees to prepare

Which sports need this equipment?

Which sports need this equipment? Презентация к уроку английского языка "Faces of London" - скачать

Презентация к уроку английского языка "Faces of London" - скачать  ПРЕЗЕНТАЦИЯ К УРОКУ К УМК И.Н.Верещагиной, О.В. Афанасьевой, 5 класс LESSON 5

ПРЕЗЕНТАЦИЯ К УРОКУ К УМК И.Н.Верещагиной, О.В. Афанасьевой, 5 класс LESSON 5  Dalmatovo

Dalmatovo СЛОВАРЬ / DICTIONARY Словарь - это вся вселенная в алфавитном порядке! Если хорошенько подумать, словарь – это книга книг. Он включает в

СЛОВАРЬ / DICTIONARY Словарь - это вся вселенная в алфавитном порядке! Если хорошенько подумать, словарь – это книга книг. Он включает в  Places in the school

Places in the school Listening – прослушивание

Listening – прослушивание Произношение слов

Произношение слов Дни недели

Дни недели Game on numbers and colours

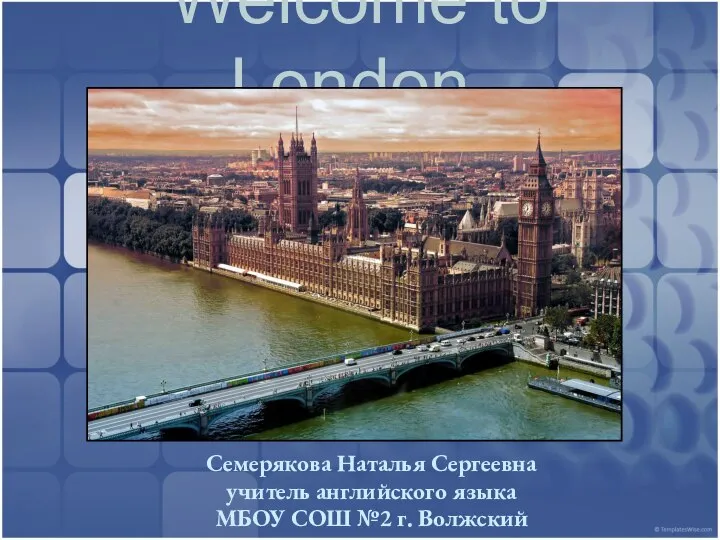

Game on numbers and colours Welcome to London. Семерякова Наталья Сергеевна учитель английского языка МБОУ СОШ №2 г. Волжский

Welcome to London. Семерякова Наталья Сергеевна учитель английского языка МБОУ СОШ №2 г. Волжский  New Year in Russia, Israel, France, USA, Denmark and Vietnam

New Year in Russia, Israel, France, USA, Denmark and Vietnam Презентация Модели бюджетного федерализма

Презентация Модели бюджетного федерализма Современный курс английского языка для подростков авторы Michael Vince with Judy West

Современный курс английского языка для подростков авторы Michael Vince with Judy West L I M E R I C K S

L I M E R I C K S Влияние международных отношений на политическую карту мира

Влияние международных отношений на политическую карту мира Healthy Habits

Healthy Habits First impression

First impression Hello children!! My name is Owly and together we are going to talk about WHquestions!

Hello children!! My name is Owly and together we are going to talk about WHquestions! City problems

City problems Village and Town

Village and Town Презентация к уроку английского языка "Coca-Cola" - скачать

Презентация к уроку английского языка "Coca-Cola" - скачать  Pictures. Word-game

Pictures. Word-game Моя семья. My family

Моя семья. My family Презентация к уроку английского языка "The Portraits" - скачать

Презентация к уроку английского языка "The Portraits" - скачать  Cambridge academic. English part 1

Cambridge academic. English part 1 Negative prefixes. Game

Negative prefixes. Game S.Alisher. Vancouver

S.Alisher. Vancouver