- Economic nature of taxes

Содержание

- 2. Basic terminology tax agent — a person who in accordance with this Code is entrusted with

- 3. Basic terminology A tax can be defined as a payment to support the cost of government.

- 4. Basic terminology A taxpayer is any person or organization required by law to pay a tax

- 5. Income tax incidence Government G imposes a new tax on corporate business profits. A manufacturing corporation

- 6. The Relationship between Base, Rate, and Revenue Taxes are usually characterized by reference to their base.

- 7. The Relationship between Base, Rate, and Revenue The amount of a tax is calculated by multiplying

- 8. Standards for good taxes Theorists maintain that every tax can and should be evaluated on certain

- 9. Sufficiency The first standard by which to evaluate a tax is its sufficiency as a revenue

- 10. Sufficiency What is the consequence of an insufficient tax system? The government must make up its

- 11. Sufficiency Another option is for governments to borrow money to finance their operating deficits Debt financing

- 12. TAXES SHOULD BE CONVENIENT Our second standard for evaluating a tax is convenience. From the government's

- 13. TAXES SHOULD BE CONVENIENT From the taxpayer's viewpoint, a good tax should be convenient to pay.

- 14. TAXES SHOULD BE EFFICIENT Our third standard for a good tax is economic efficiency. Tax policymakers

- 15. The Classical Standard of Efficiency The classical economist Adam Smith believed that taxes should have as

- 16. The Classical Standard of Efficiency The laissez-faire system favored by Adam Smith theoretically creates a level

- 17. Taxes as an Instrument of Fiscal Policy The British economist John Maynard Keynes disagreed with the

- 18. Taxes as an Instrument of Fiscal Policy Historically, this instability caused cycles of high unemployment, severe

- 19. Taxes as an Instrument of Fiscal Policy In the Keynesian schema, tax systems are a primary

- 20. Taxes as an Instrument of Fiscal Policy The tax cut should both stimulate demand for consumer

- 21. Taxes and Behavior Modification Modern governments use their tax systems to address not only macroeconomic concerns

- 22. Taxes and Behavior Modification Some of the social problems that the federal income tax system tries

- 23. Income Tax Preferences Provisions in the federal income tax system designed as incentives for certain behaviors

- 24. Taxes should be fair Ability to pay A useful was to begin our discussion of equity

- 25. Taxes should be fair For instance, income taxes are based on the person’s inflow of economic

- 26. Horizontal equity If a tax is designed so that persons with the same ability to pay

- 27. Vertical Equity A tax system is vertically equitable if persons with a greater ability to pay

- 28. The classification of taxes Mainly the taxes can be classified based on different conditions: Depending on

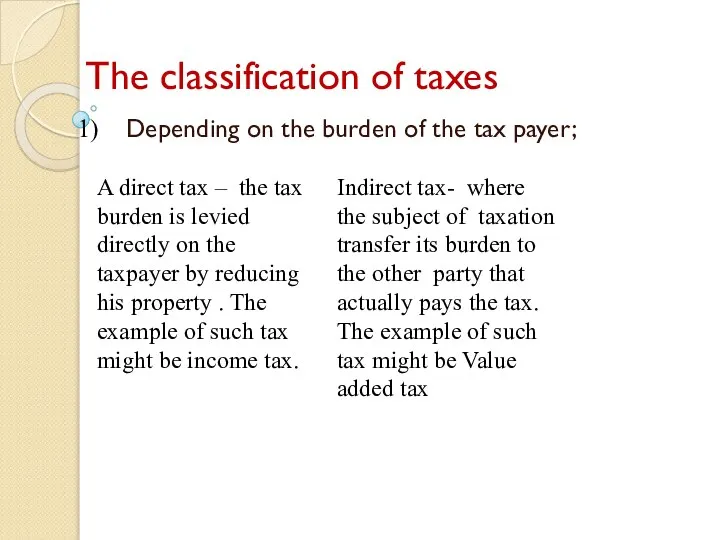

- 29. The classification of taxes Depending on the burden of the tax payer;

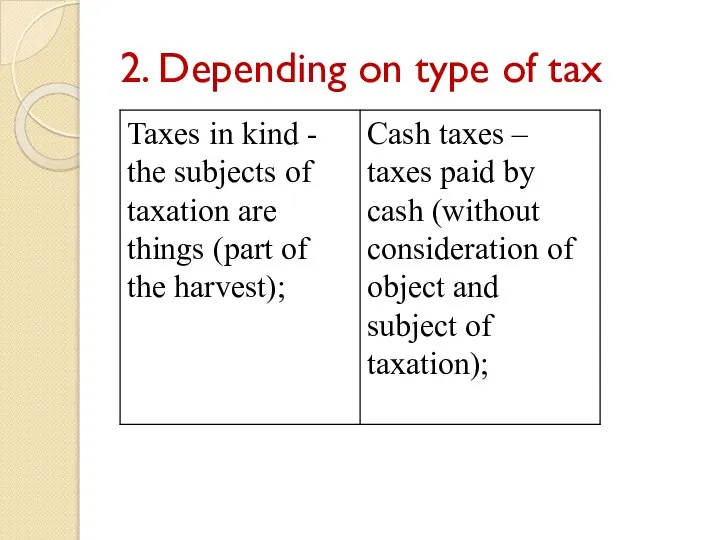

- 30. 2. Depending on type of tax

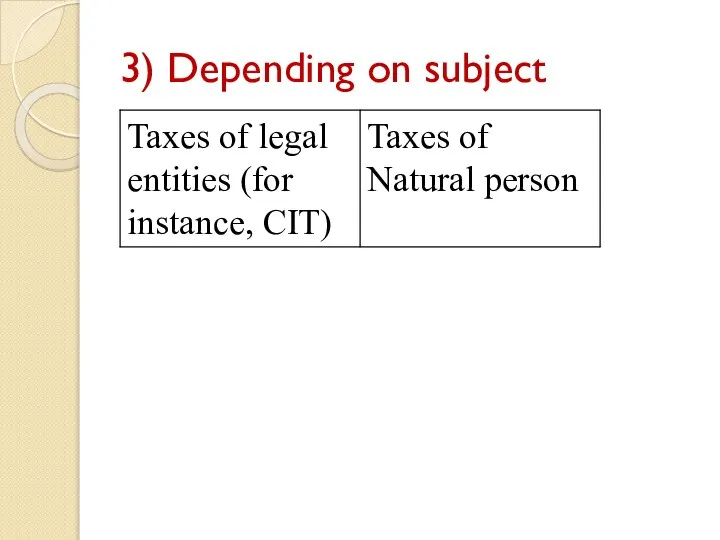

- 31. 3) Depending on subject

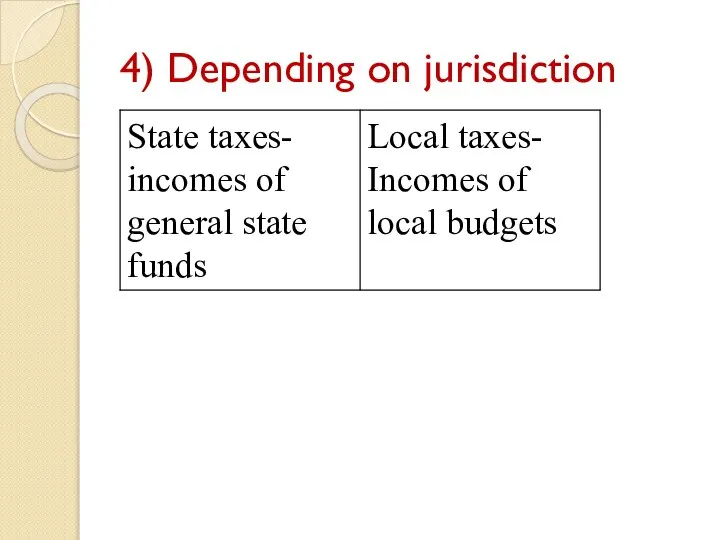

- 32. 4) Depending on jurisdiction

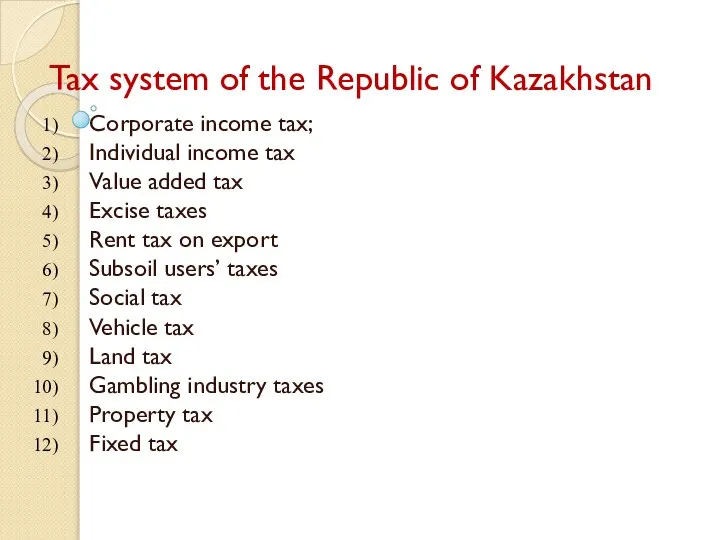

- 33. Tax system of the Republic of Kazakhstan Corporate income tax; Individual income tax Value added tax

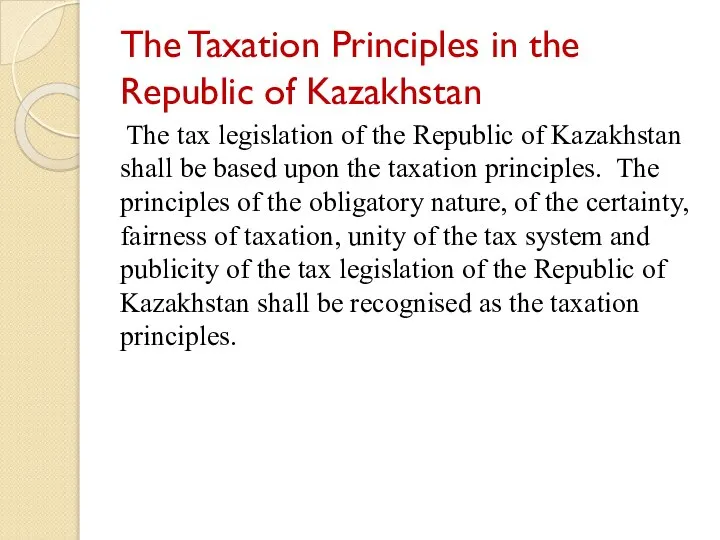

- 34. The Taxation Principles in the Republic of Kazakhstan The tax legislation of the Republic of Kazakhstan

- 35. The Principle of the Obligatory Nature of Taxation The taxpayers shall be obliged to perform tax

- 36. The Principle of Certainty of Taxation Taxes and other obligatory payments to the budget of the

- 37. The Principle of Fairness of Taxation 1. Taxation in the Republic of Kazakhstan shall be universal

- 38. The Principle of Unity of the Tax System The tax system of the Republic of Kazakhstan

- 39. The Principle of Publicity of Tax Legislation of the Republic of Kazakhstan Regulatory legal acts which

- 40. Contemporary conditions At February 6, 2008, the President of Kazakhstan assigned to the government of the

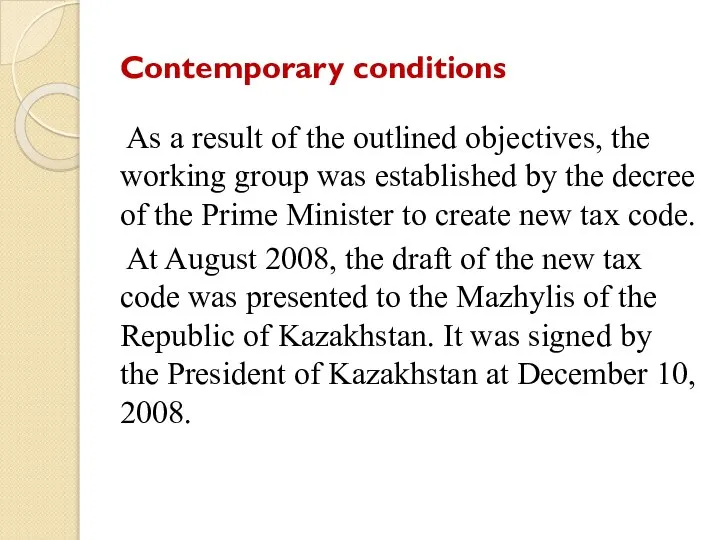

- 41. Contemporary conditions As a result of the outlined objectives, the working group was established by the

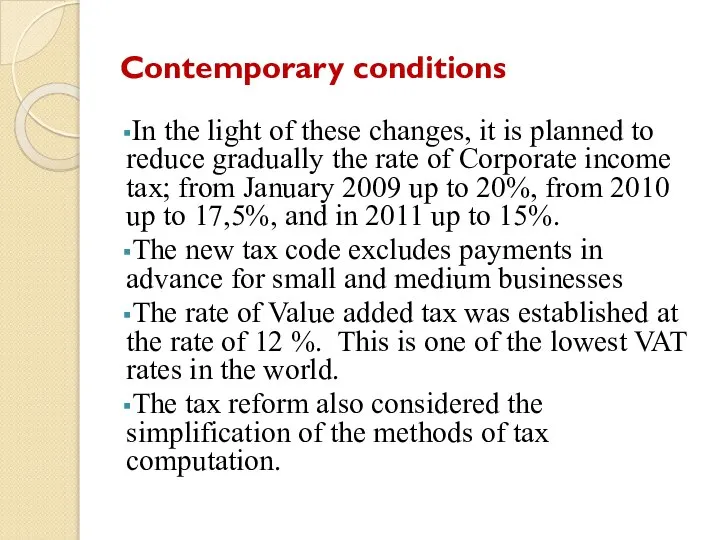

- 42. Contemporary conditions In the light of these changes, it is planned to reduce gradually the rate

- 44. Скачать презентацию

Basic terminology

tax agent — a person who in accordance with

Basic terminology

tax agent — a person who in accordance with

Basic terminology

A tax can be defined as a payment to

Basic terminology

A tax can be defined as a payment to

Basic terminology

A taxpayer is any person or organization required by

Basic terminology

A taxpayer is any person or organization required by

Income tax incidence

Government G imposes a new tax on corporate

Income tax incidence

Government G imposes a new tax on corporate

The Relationship between Base, Rate, and Revenue

Taxes are usually characterized by

The Relationship between Base, Rate, and Revenue

Taxes are usually characterized by

The Relationship between Base, Rate, and Revenue

The amount of a tax

The Relationship between Base, Rate, and Revenue

The amount of a tax

Standards for good taxes

Theorists maintain that every tax can and

Standards for good taxes

Theorists maintain that every tax can and

Sufficiency

The first standard by which to evaluate a tax is its

Sufficiency

The first standard by which to evaluate a tax is its

Sufficiency

What is the consequence of an insufficient tax system? The government

Sufficiency

What is the consequence of an insufficient tax system? The government

Sufficiency

Another option is for governments to borrow money to finance their

Sufficiency

Another option is for governments to borrow money to finance their

TAXES SHOULD BE CONVENIENT

Our second standard for evaluating a tax is

TAXES SHOULD BE CONVENIENT

Our second standard for evaluating a tax is

TAXES SHOULD BE CONVENIENT

From the taxpayer's viewpoint, a good tax should

TAXES SHOULD BE CONVENIENT

From the taxpayer's viewpoint, a good tax should

TAXES SHOULD BE EFFICIENT

Our third standard for a good tax is

TAXES SHOULD BE EFFICIENT

Our third standard for a good tax is

The Classical Standard of Efficiency

The classical economist Adam Smith believed that

The Classical Standard of Efficiency

The classical economist Adam Smith believed that

The Classical Standard of Efficiency

The laissez-faire system favored by Adam Smith

The Classical Standard of Efficiency

The laissez-faire system favored by Adam Smith

Taxes as an Instrument of Fiscal Policy

The British economist John Maynard

Taxes as an Instrument of Fiscal Policy

The British economist John Maynard

Taxes as an Instrument of Fiscal Policy

Historically, this instability caused cycles

Taxes as an Instrument of Fiscal Policy

Historically, this instability caused cycles

Taxes as an Instrument of Fiscal Policy

In the Keynesian schema, tax

Taxes as an Instrument of Fiscal Policy

In the Keynesian schema, tax

Taxes as an Instrument of Fiscal Policy

The tax cut should both

Taxes as an Instrument of Fiscal Policy

The tax cut should both

Taxes and Behavior Modification

Modern governments use their tax systems to address

Taxes and Behavior Modification

Modern governments use their tax systems to address

Taxes and Behavior Modification

Some of the social problems that the federal

Taxes and Behavior Modification

Some of the social problems that the federal

Income Tax Preferences

Provisions in the federal income tax system designed as

Income Tax Preferences

Provisions in the federal income tax system designed as

Taxes should be fair

Ability to pay

A useful was to

Taxes should be fair

Ability to pay

A useful was to

Taxes should be fair

For instance, income taxes are based on the

Taxes should be fair

For instance, income taxes are based on the

Horizontal equity

If a tax is designed so that persons with

Horizontal equity

If a tax is designed so that persons with

Vertical Equity

A tax system is vertically equitable if persons with a

Vertical Equity

A tax system is vertically equitable if persons with a

The classification of taxes

Mainly the taxes can be classified based

The classification of taxes

Mainly the taxes can be classified based

The classification of taxes

Depending on the burden of the tax

The classification of taxes

Depending on the burden of the tax

2. Depending on type of tax

2. Depending on type of tax

3) Depending on subject

3) Depending on subject

4) Depending on jurisdiction

4) Depending on jurisdiction

Tax system of the Republic of Kazakhstan

Corporate income tax;

Individual income

Tax system of the Republic of Kazakhstan

Corporate income tax;

Individual income

The Taxation Principles in the Republic of Kazakhstan

The tax legislation of

The Taxation Principles in the Republic of Kazakhstan

The tax legislation of

The Principle of the Obligatory Nature of Taxation

The taxpayers shall be

The Principle of the Obligatory Nature of Taxation

The taxpayers shall be

The Principle of Certainty of Taxation

Taxes and other obligatory payments to

The Principle of Certainty of Taxation

Taxes and other obligatory payments to

The Principle of Fairness of Taxation

1. Taxation in the Republic of

The Principle of Fairness of Taxation

1. Taxation in the Republic of

The Principle of Unity of the Tax System

The tax system of

The Principle of Unity of the Tax System

The tax system of

The Principle of Publicity of Tax Legislation of the Republic of

The Principle of Publicity of Tax Legislation of the Republic of

Contemporary conditions

At February 6, 2008, the President of Kazakhstan assigned

Contemporary conditions

At February 6, 2008, the President of Kazakhstan assigned

Contemporary conditions

As a result of the outlined objectives, the working

Contemporary conditions

As a result of the outlined objectives, the working

Contemporary conditions

In the light of these changes, it is planned

Contemporary conditions

In the light of these changes, it is planned

Бюджет государства и семьи. (8 класс)

Бюджет государства и семьи. (8 класс) Развитие малых инновационных предприятий в современных условиях в России

Развитие малых инновационных предприятий в современных условиях в России Асимметричность информации и отношения «принципал-агент»

Асимметричность информации и отношения «принципал-агент» Розрахунково - графічна робота "Регіональна економіка"

Розрахунково - графічна робота "Регіональна економіка" Мое отношение к коррупции

Мое отношение к коррупции Микроэкономика и макроэкономика

Микроэкономика и макроэкономика París climate del welcomed

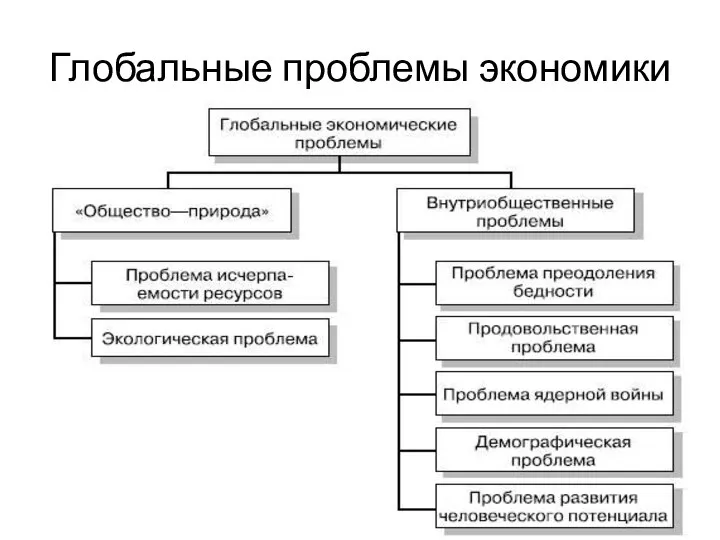

París climate del welcomed Глобальные проблемы экономики

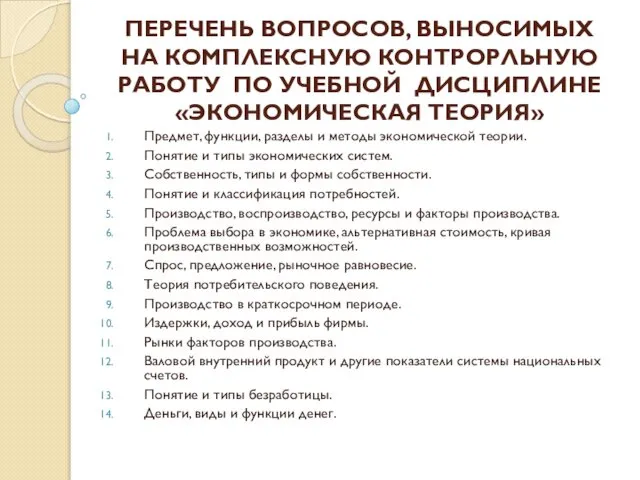

Глобальные проблемы экономики Перечень вопросов, выносимых на комплексную контрорльную работу по учебной дисциплине Экономическая теория

Перечень вопросов, выносимых на комплексную контрорльную работу по учебной дисциплине Экономическая теория Макроэкономические показатели и их измерение

Макроэкономические показатели и их измерение Постиндустриальное (информационное) общество

Постиндустриальное (информационное) общество Макроэкономика

Макроэкономика Životní podmínky - příjmy a spotřeba obyvatelstva

Životní podmínky - příjmy a spotřeba obyvatelstva Причорноморський економічний район

Причорноморський економічний район Ұлттық экономикадағы қаржы және ақша-несие жүйесі

Ұлттық экономикадағы қаржы және ақша-несие жүйесі Расчет экспортной, импортной, внешнеторговой квот за период с 2000 по 2012 годы в Турции и ОАЭ ( с помощью баз данных ВТО и UNCTAD) Подгото

Расчет экспортной, импортной, внешнеторговой квот за период с 2000 по 2012 годы в Турции и ОАЭ ( с помощью баз данных ВТО и UNCTAD) Подгото Өндірісті басқаруды ұйымдастыру

Өндірісті басқаруды ұйымдастыру Спрос, предложение и рыночное равновесие. Эластичность спроса и предложения

Спрос, предложение и рыночное равновесие. Эластичность спроса и предложения Поведение потребителя

Поведение потребителя Основные сведения об инжиниринге. Классификация инжиниринга

Основные сведения об инжиниринге. Классификация инжиниринга Задачи определения нижних границ цен и многоступенчатого расчета маржинальной прибыли

Задачи определения нижних границ цен и многоступенчатого расчета маржинальной прибыли Измерение результатов экономической деятельности

Измерение результатов экономической деятельности Economics of innovation. Lecture 3: Innovation, Demand and Consumption

Economics of innovation. Lecture 3: Innovation, Demand and Consumption Потребности. Виды потребностей

Потребности. Виды потребностей Оптимізаційні методи та моделі. Нелінійні задачі оптимізації. Метод множників Лагранжа. (Тема 12)

Оптимізаційні методи та моделі. Нелінійні задачі оптимізації. Метод множників Лагранжа. (Тема 12) Кривые Энгеля

Кривые Энгеля Безграничность потребностей и ограниченность ресурсов. Проблема выбора

Безграничность потребностей и ограниченность ресурсов. Проблема выбора Предприятия розничной торговли

Предприятия розничной торговли