- The science of macroeconomics

Содержание

- 2. Literature N.Gragory Mankiw MACROECONOMICS. 8TH EDITION, 2014. http://www.slideshare.net/RMA03/mankiw-macroeconomics-8th-edition Additional reading: Abel Bernanke. Introduction to macroeconomics. (2008).

- 3. Part I Introduction 1 1 The Science of Macroeconomics 2 The Data of Macroeconomics Part II

- 4. Part III Growth Theory: The Economy in the Very Long Run 8 Economic Growth I 9

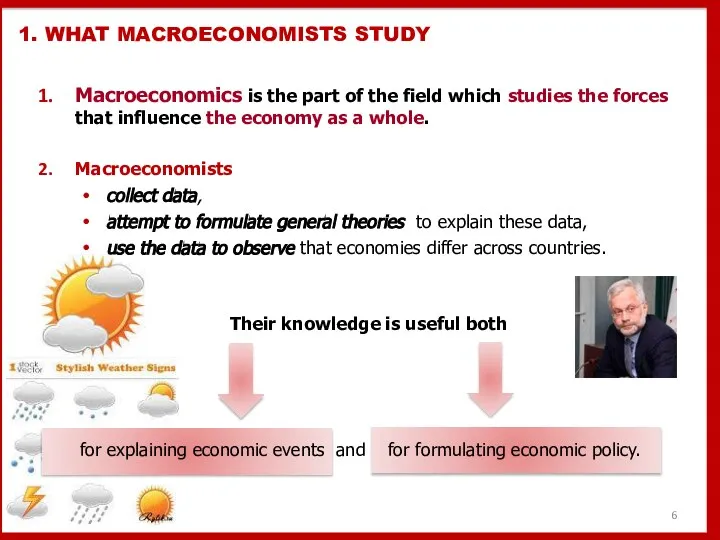

- 5. WHAT MACROECONOMISTS STUDY HOW ECONOMISTS THINK

- 6. Macroeconomics is the part of the field which studies the forces that influence the economy as

- 7. Low unemployment Low and stable inflation Minimal domestic economic fluctuations Minimal international economic fluctuations High rates

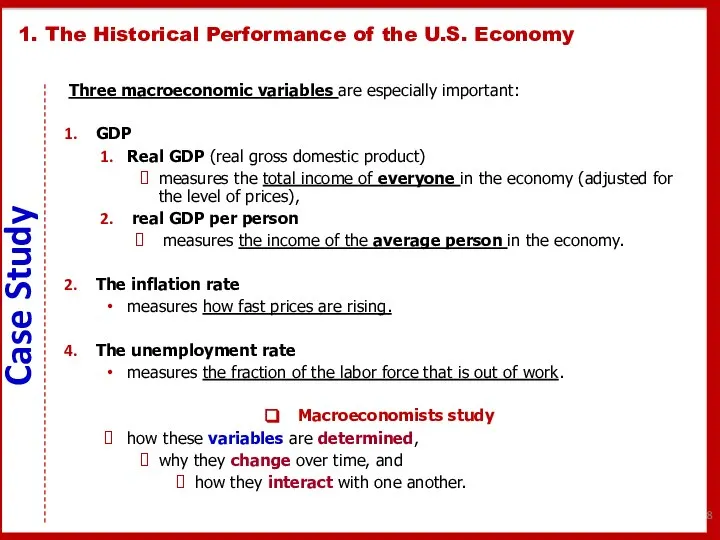

- 8. 1. The Historical Performance of the U.S. Economy Three macroeconomic variables are especially important: GDP Real

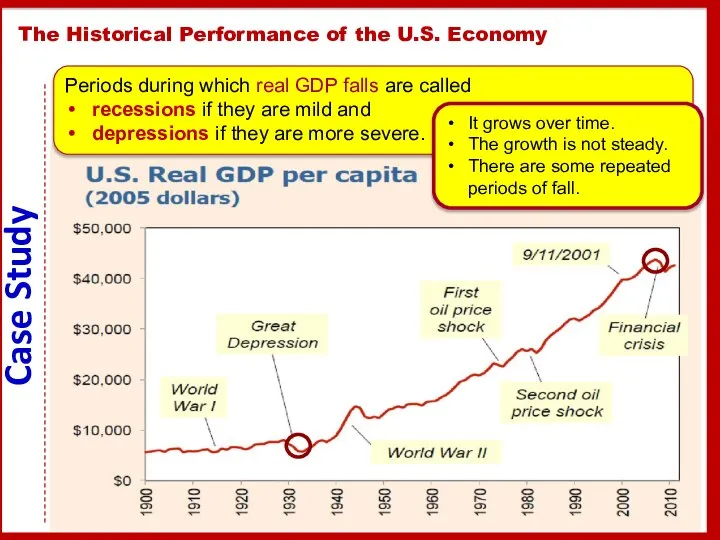

- 9. Real GDP per person The Historical Performance of the U.S. Economy Periods during which real GDP

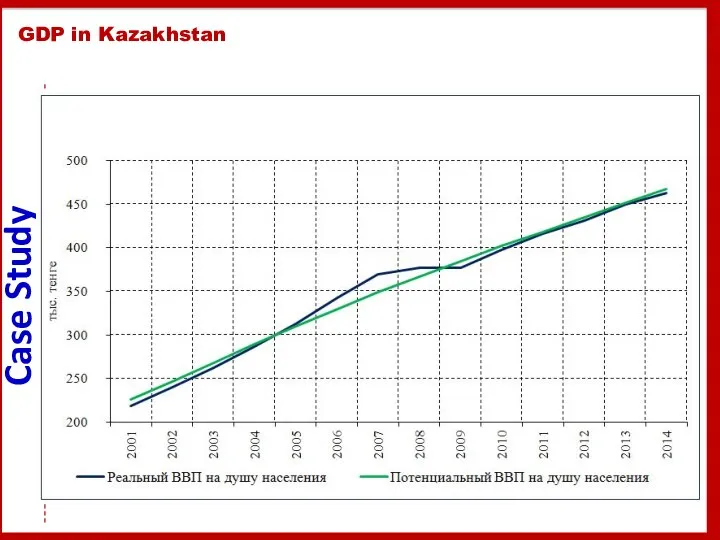

- 10. GDP in Kazakhstan

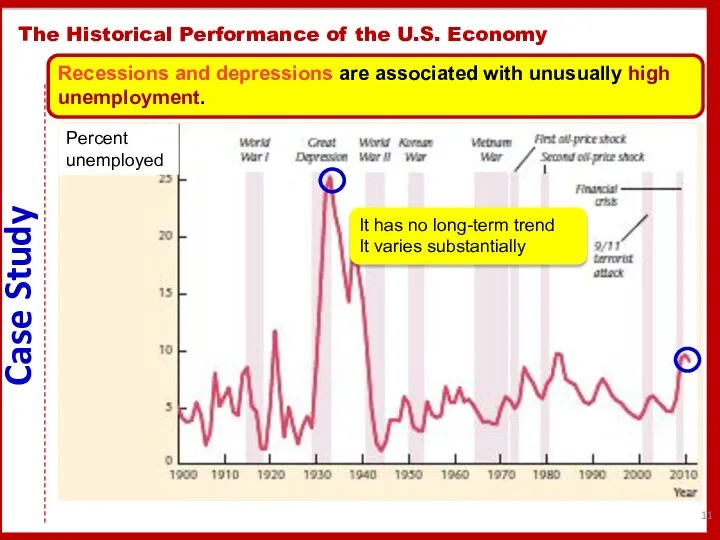

- 11. The Historical Performance of the U.S. Economy Recessions and depressions are associated with unusually high unemployment.

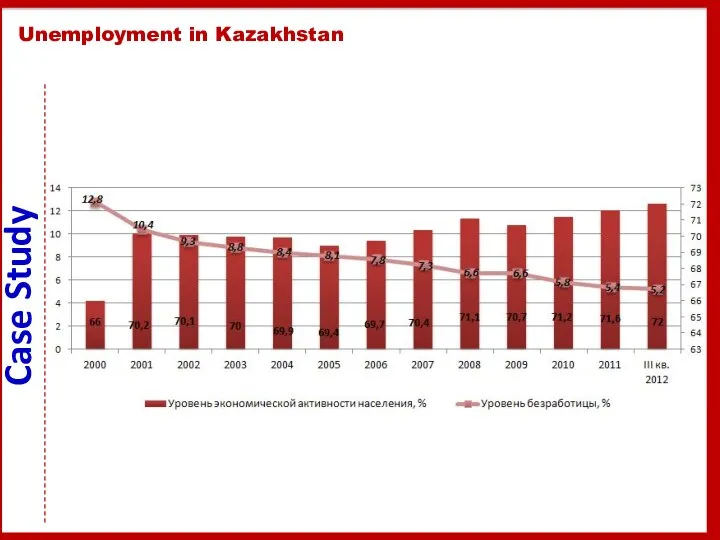

- 12. Unemployment in Kazakhstan

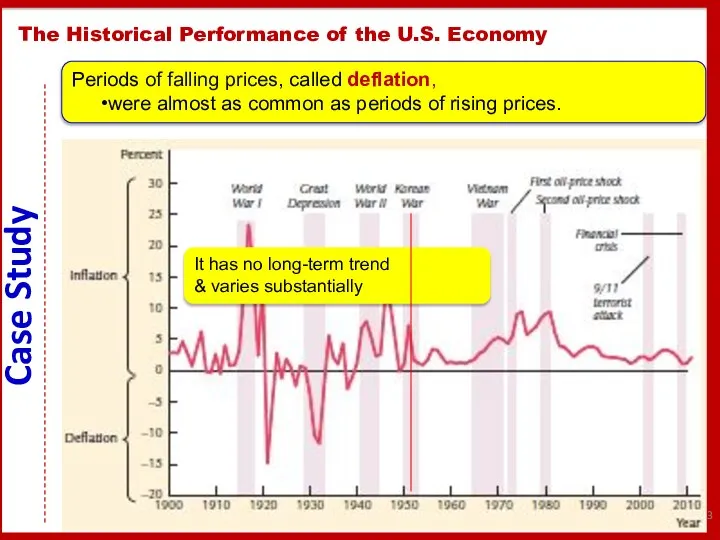

- 13. The Historical Performance of the U.S. Economy Periods of falling prices, called deflation, were almost as

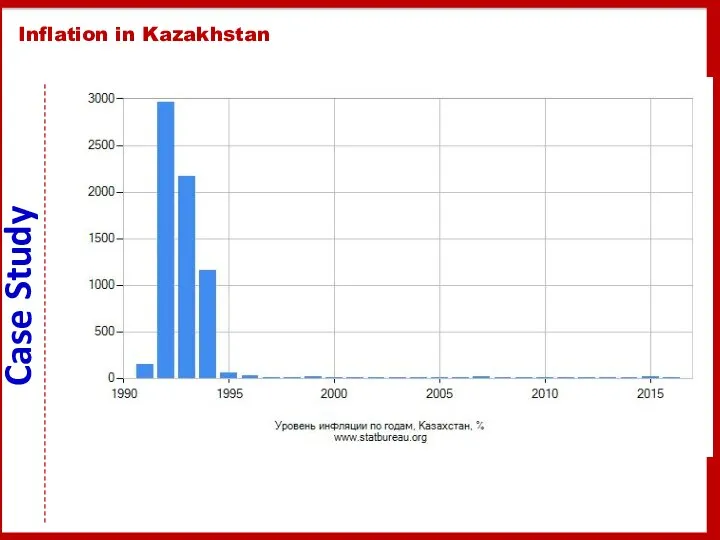

- 14. Inflation in Kazakhstan

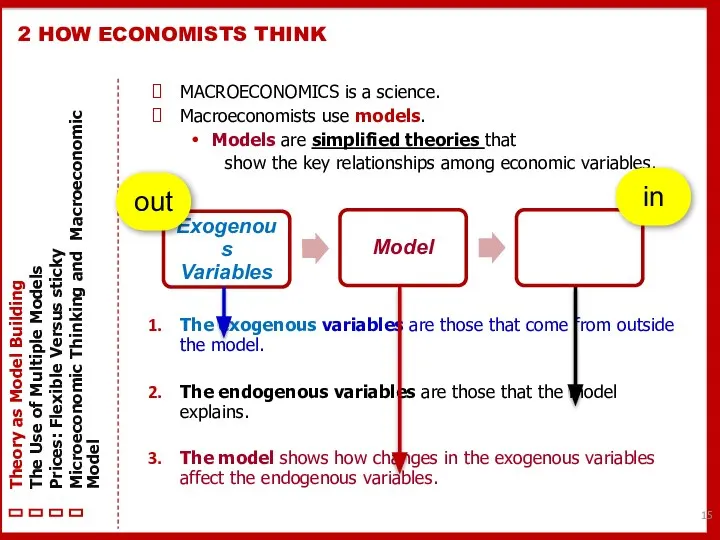

- 15. MACROECONOMICS is a science. Macroeconomists use models. Models are simplified theories that show the key relationships

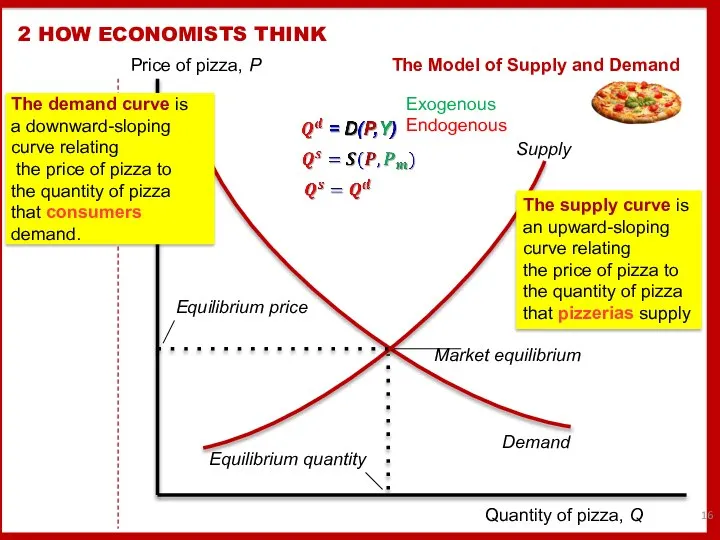

- 16. 2 HOW ECONOMISTS THINK Price of pizza, P Quantity of pizza, Q Demand Supply Market equilibrium

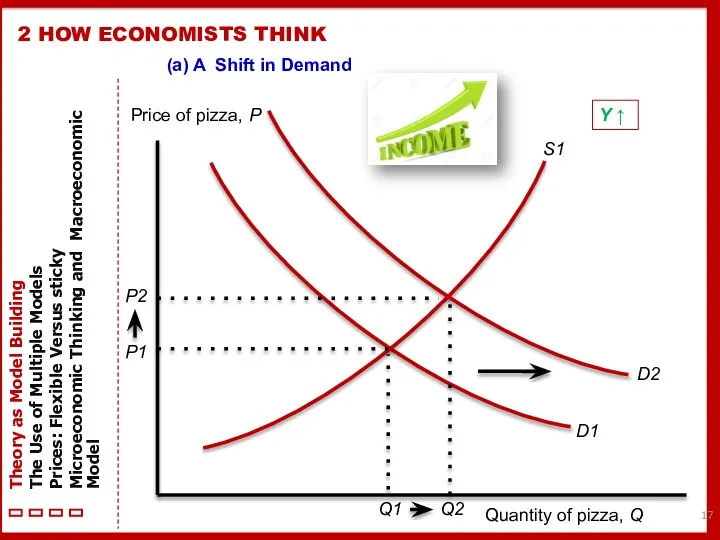

- 17. 2 HOW ECONOMISTS THINK Price of pizza, P Quantity of pizza, Q D1 S1 (a) A

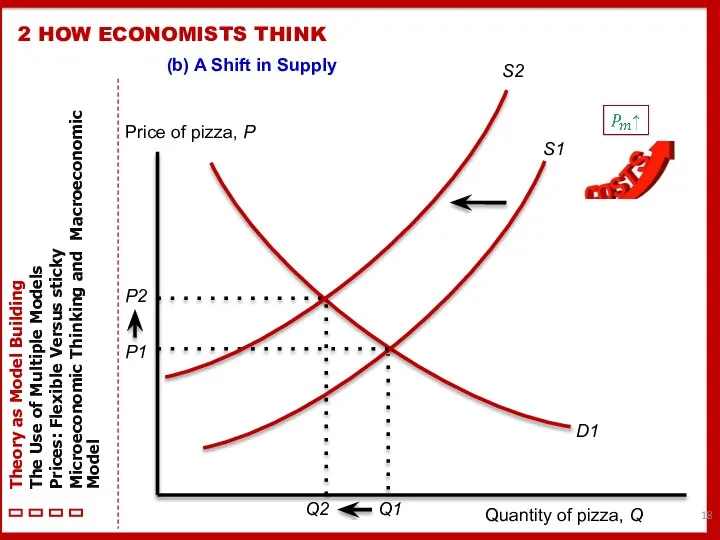

- 18. 2 HOW ECONOMISTS THINK Price of pizza, P Quantity of pizza, Q D1 S1 (b) A

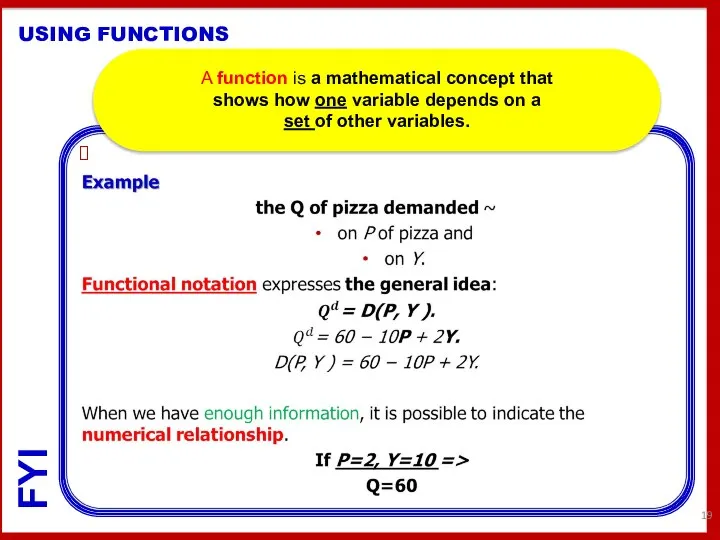

- 19. USING FUNCTIONS A function is a mathematical concept that shows how one variable depends on a

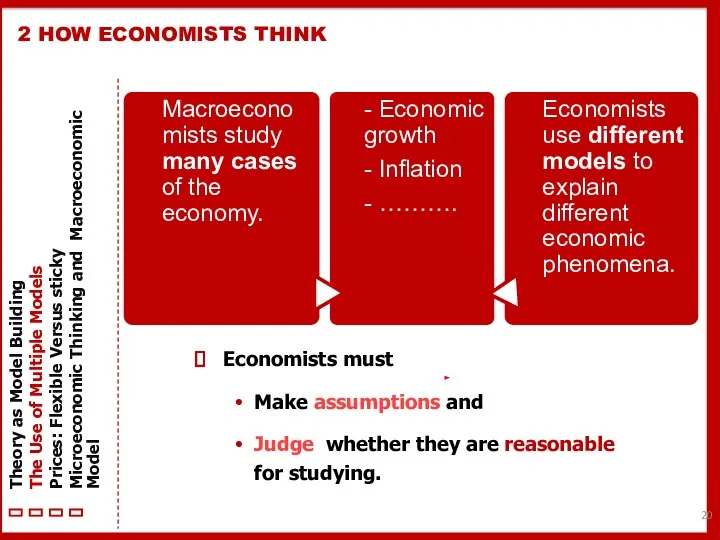

- 20. Economists must Make assumptions and Judge whether they are reasonable for studying. 2 HOW ECONOMISTS THINK

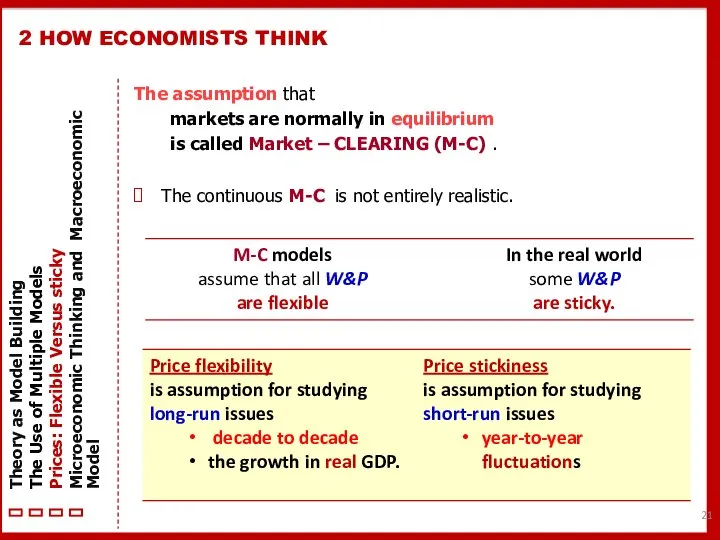

- 21. The assumption that markets are normally in equilibrium is called Market – CLEARING (M-C) . The

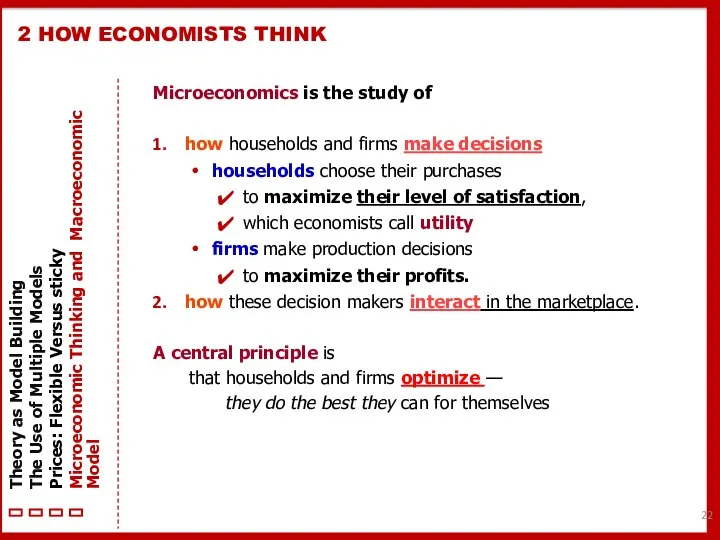

- 22. Microeconomics is the study of how households and firms make decisions households choose their purchases to

- 23. Macroeconomics and microeconomics are inextricably linked. Although microeconomic decisions underlie macroeconomic phenomena, macroeconomic models DO NOT

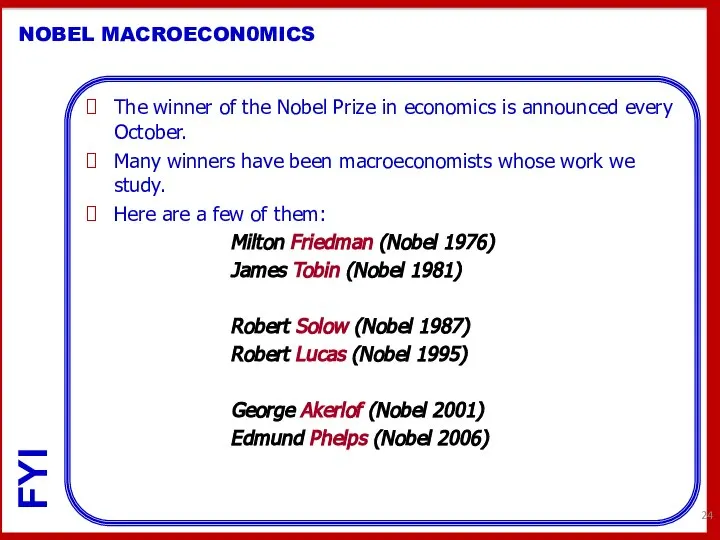

- 24. The winner of the Nobel Prize in economics is announced every October. Many winners have been

- 25. S U M M A R Y Macroeconomics is the study of the economy as a

- 27. Скачать презентацию

Literature

N.Gragory Mankiw MACROECONOMICS. 8TH EDITION, 2014.

http://www.slideshare.net/RMA03/mankiw-macroeconomics-8th-edition

Additional reading:

Abel Bernanke. Introduction to

Literature

N.Gragory Mankiw MACROECONOMICS. 8TH EDITION, 2014.

http://www.slideshare.net/RMA03/mankiw-macroeconomics-8th-edition

Additional reading:

Abel Bernanke. Introduction to

Part I Introduction 1

1 The Science of Macroeconomics

2 The Data of

1 The Science of Macroeconomics

2 The Data of

Part III Growth Theory: The Economy in the Very Long Run

8

Part III Growth Theory: The Economy in the Very Long Run

8

WHAT MACROECONOMISTS STUDY

HOW ECONOMISTS THINK

WHAT MACROECONOMISTS STUDY

HOW ECONOMISTS THINK

Macroeconomics is the part of the field which studies the forces

Macroeconomics is the part of the field which studies the forces

Low unemployment

Low and stable inflation

Minimal domestic economic fluctuations

Minimal international economic fluctuations

High

Low unemployment

Low and stable inflation

Minimal domestic economic fluctuations

Minimal international economic fluctuations

High

1. The Historical Performance of the U.S. Economy

Three macroeconomic variables are

1. The Historical Performance of the U.S. Economy

Three macroeconomic variables are

Real GDP per person

The Historical Performance of the U.S. Economy

Periods during

Real GDP per person

The Historical Performance of the U.S. Economy

Periods during

GDP in Kazakhstan

GDP in Kazakhstan

The Historical Performance of the U.S. Economy

Recessions and depressions are associated

The Historical Performance of the U.S. Economy

Recessions and depressions are associated

Unemployment in Kazakhstan

Unemployment in Kazakhstan

The Historical Performance of the U.S. Economy

Periods of falling prices, called

The Historical Performance of the U.S. Economy

Periods of falling prices, called

Inflation in Kazakhstan

Inflation in Kazakhstan

MACROECONOMICS is a science.

Macroeconomists use models.

Models are simplified theories that

MACROECONOMICS is a science.

Macroeconomists use models.

Models are simplified theories that

2 HOW ECONOMISTS THINK

Price of pizza, P

Quantity of pizza, Q

Demand

Supply

Market

2 HOW ECONOMISTS THINK

Price of pizza, P

Quantity of pizza, Q

Demand

Supply

Market

2 HOW ECONOMISTS THINK

Price of pizza, P

Quantity of pizza, Q

D1

S1

(a)

2 HOW ECONOMISTS THINK

Price of pizza, P

Quantity of pizza, Q

D1

S1

(a)

2 HOW ECONOMISTS THINK

Price of pizza, P

Quantity of pizza, Q

D1

S1

(b)

2 HOW ECONOMISTS THINK

Price of pizza, P

Quantity of pizza, Q

D1

S1

(b)

USING FUNCTIONS

A function is a mathematical concept that

shows how

USING FUNCTIONS

A function is a mathematical concept that

shows how

Economists must

Make assumptions and

Judge whether they are reasonable for studying.

2

Economists must

Make assumptions and

Judge whether they are reasonable for studying.

2

The assumption that

markets are normally in equilibrium

is called Market

The assumption that

markets are normally in equilibrium

is called Market

Microeconomics is the study of

how households and firms make decisions

Microeconomics is the study of

how households and firms make decisions

Macroeconomics and microeconomics are inextricably linked.

Although

microeconomic decisions underlie macroeconomic phenomena,

Macroeconomics and microeconomics are inextricably linked.

Although

microeconomic decisions underlie macroeconomic phenomena,

The winner of the Nobel Prize in economics is announced every

The winner of the Nobel Prize in economics is announced every

S U M M A R Y

Macroeconomics is the study

S U M M A R Y

Macroeconomics is the study

Теория спроса и предложения. Рыночное равновесие

Теория спроса и предложения. Рыночное равновесие Фондовый рынок ценных бумаг

Фондовый рынок ценных бумаг Теоретические, методологические основы исследования системы обеспечения экономической безопасности

Теоретические, методологические основы исследования системы обеспечения экономической безопасности Экономика медиа. Издержки. Точка безубыточности

Экономика медиа. Издержки. Точка безубыточности Экономические циклы

Экономические циклы Мировая экономика

Мировая экономика Построение модели прогнозирования банкротства банков на основе показателя DD

Построение модели прогнозирования банкротства банков на основе показателя DD Общая характеристика дисциплины «Макроэкономическое планирование и прогнозирование»

Общая характеристика дисциплины «Макроэкономическое планирование и прогнозирование» Инфляция. Виды инфляции

Инфляция. Виды инфляции Анализ статьи

Анализ статьи Государственная экономическая политика

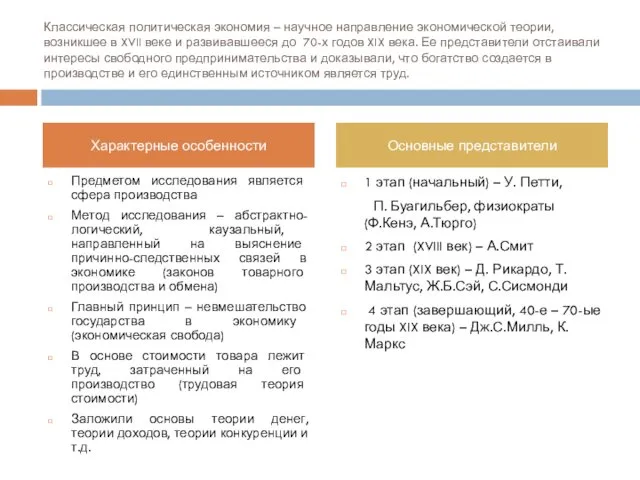

Государственная экономическая политика Классическая политическая экономия

Классическая политическая экономия Социальный капитал. Характеристика и роль развития в экономических субъектах

Социальный капитал. Характеристика и роль развития в экономических субъектах Экономическая система Дании

Экономическая система Дании История развития экономической теории

История развития экономической теории Модели развития организации

Модели развития организации Міжнародна конкурентоспроможність підприємства

Міжнародна конкурентоспроможність підприємства Содержание причин и условий преступлений в отношении предпринимателей

Содержание причин и условий преступлений в отношении предпринимателей Глобализация. Предпосылки и направления глобализации

Глобализация. Предпосылки и направления глобализации Положительная практика поддержки ТОСов на региональном уровне

Положительная практика поддержки ТОСов на региональном уровне Транснациональные корпорации и транснациональные банки

Транснациональные корпорации и транснациональные банки Таможенно-тарифное регулирование внешнеэкономической деятельности. (Лекция 1)

Таможенно-тарифное регулирование внешнеэкономической деятельности. (Лекция 1) Теория потребительского поведения в рыночной экономики

Теория потребительского поведения в рыночной экономики Effectiveness of NGOs. (Lecture 5)

Effectiveness of NGOs. (Lecture 5) Международное движение капитала

Международное движение капитала Управление проектом производства молочной продукции на примере К(Ф)Х ИП Воробьев И.А. Хвалынского района Саратовской области

Управление проектом производства молочной продукции на примере К(Ф)Х ИП Воробьев И.А. Хвалынского района Саратовской области Энергоэффективность и энергосбережение

Энергоэффективность и энергосбережение Урок-практикум "Человек в системе экономических отношений"

Урок-практикум "Человек в системе экономических отношений"