- Capital adequacy: Basel 2. Financial institutions management kimep

Содержание

- 2. AGENDA: Functions of bank capital; Definitions of Bank Capital, leverage ratio; Structure of BASEL 2 Bank

- 3. Importance of Bank Capital Absorb unanticipated losses and preserve confidence of the FI; Protect uninsured depositors

- 4. Two DEFINITIONS of capital: Economic = difference in the market value of assets and liabilities. Regulatory

- 5. Problem 1

- 6. Why do FI and Regulators are against market value accounting? Difficult to implement, especially for small

- 7. Leverage Ratio Banks are required to meet minimum capital standards on both a simple leverage basis

- 8. CAPITAL ADEQUACY: Basel 2 OBJECTIVES: Development of more internationally uniform prudential standards for the capital required

- 9. BASEL 2 (adopted in 2007) The new accord is based on 3 pillars: Pillar 1: Minimum

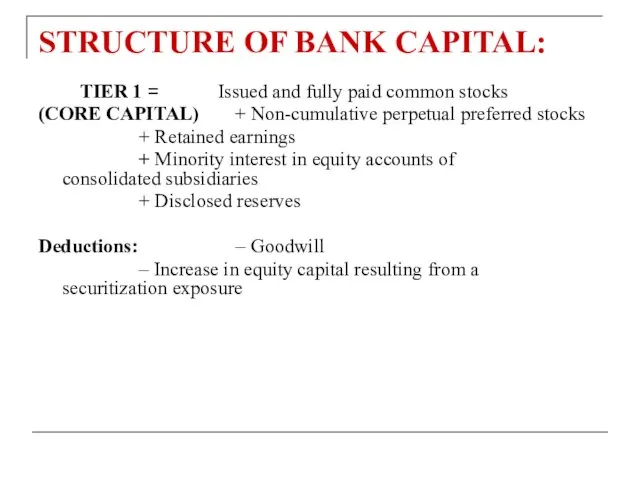

- 10. STRUCTURE OF BANK CAPITAL: TIER 1 = Issued and fully paid common stocks (CORE CAPITAL) +

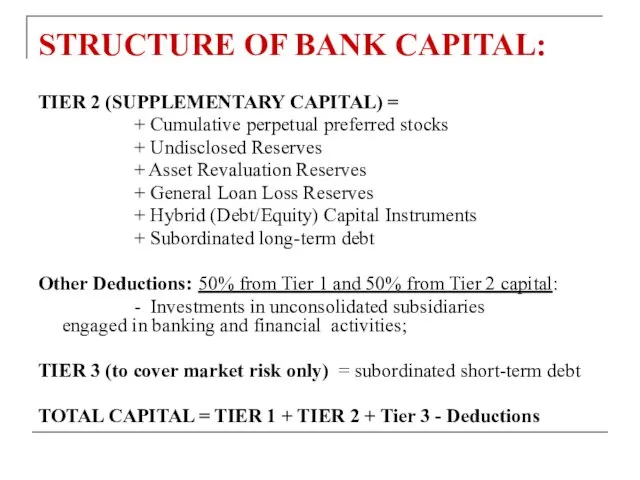

- 11. STRUCTURE OF BANK CAPITAL: TIER 2 (SUPPLEMENTARY CAPITAL) = + Cumulative perpetual preferred stocks + Undisclosed

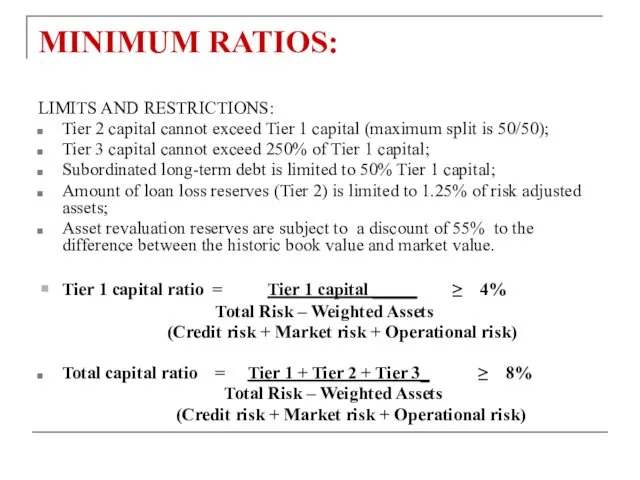

- 12. MINIMUM RATIOS: LIMITS AND RESTRICTIONS: Tier 2 capital cannot exceed Tier 1 capital (maximum split is

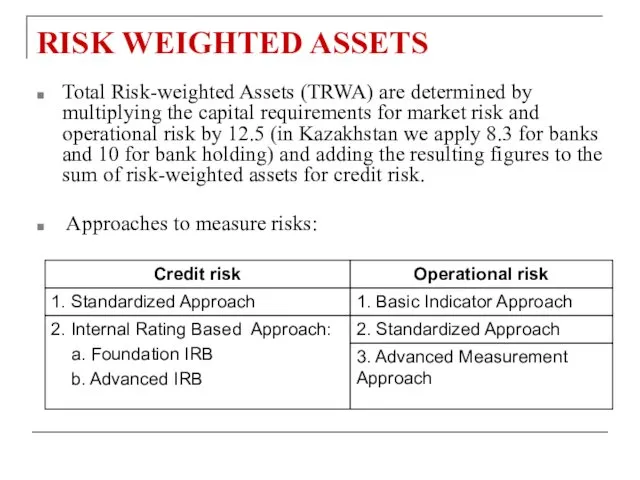

- 13. RISK WEIGHTED ASSETS Total Risk-weighted Assets (TRWA) are determined by multiplying the capital requirements for market

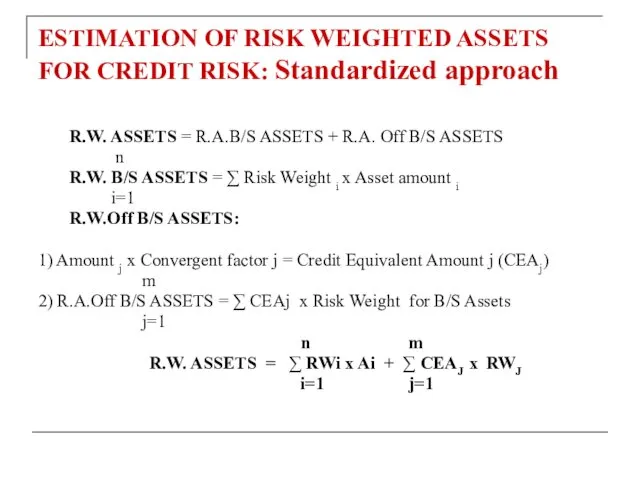

- 14. ESTIMATION OF RISK WEIGHTED ASSETS FOR CREDIT RISK: Standardized approach R.W. ASSETS = R.A.B/S ASSETS +

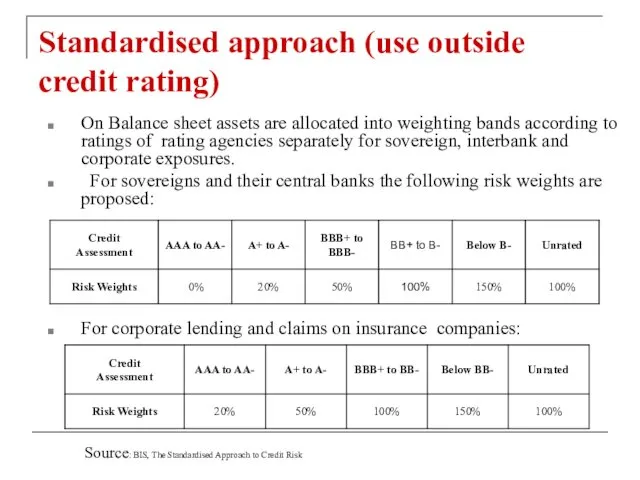

- 15. Standardised approach (use outside credit rating) On Balance sheet assets are allocated into weighting bands according

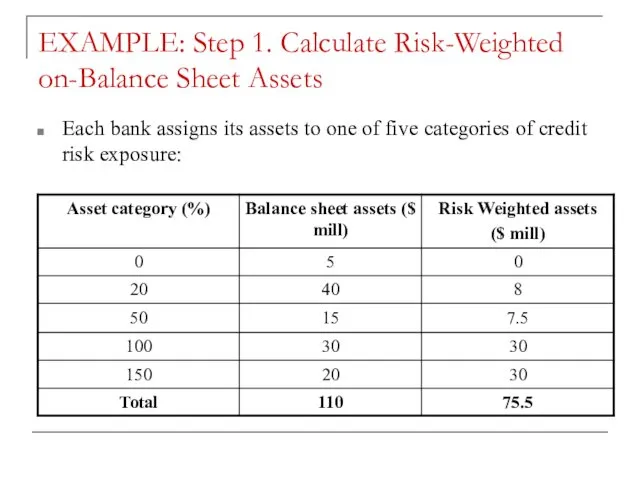

- 16. EXAMPLE: Step 1. Calculate Risk-Weighted on-Balance Sheet Assets Each bank assigns its assets to one of

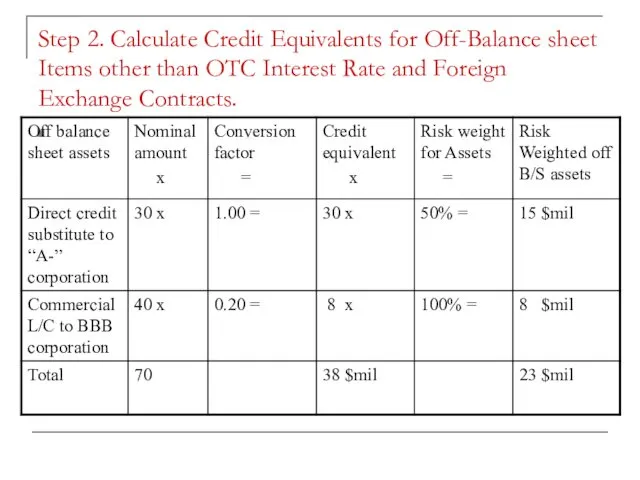

- 17. Step 2. Calculate Credit Equivalents for Off-Balance sheet Items other than OTC Interest Rate and Foreign

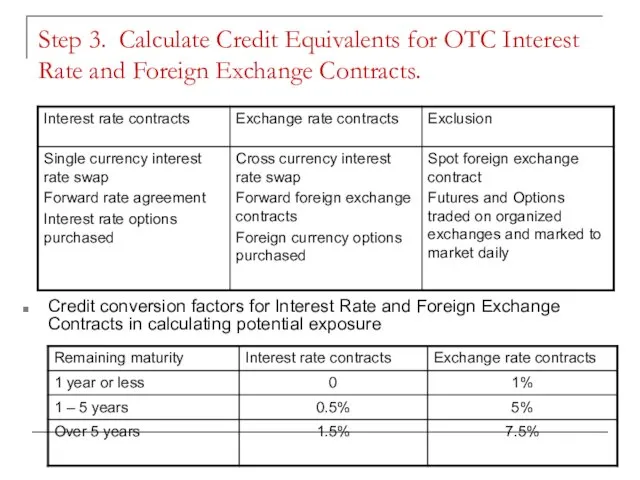

- 18. Step 3. Calculate Credit Equivalents for OTC Interest Rate and Foreign Exchange Contracts. Credit conversion factors

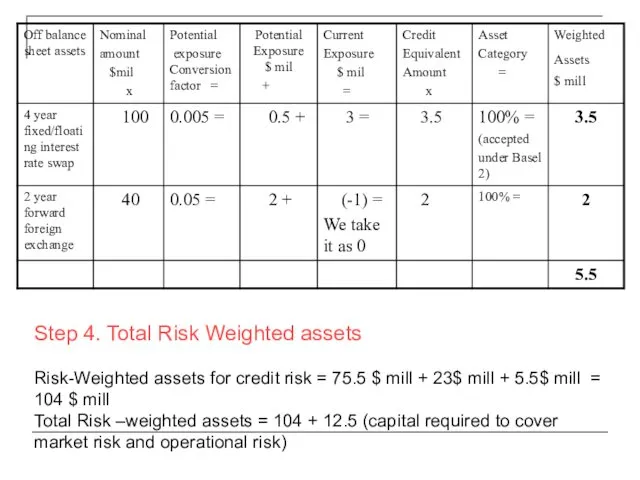

- 19. Step 4. Total Risk Weighted assets Risk-Weighted assets for credit risk = 75.5 $ mill +

- 20. Example continued: Calculate the minimum capital ratios if: Tier 1 =9$ mill , Tier 2 =

- 21. Internal rating based approach (foundation and advanced) Banks are allowed to use their internal estimates of

- 22. Foundation and advanced approaches differ primary in terms of inputs that are provided by banks or

- 23. MARKET RISK April 1995, the Basel Committee announced amended proposals for the treatment of market risk.

- 24. The pro-cyclicality of the VaR requirements VaR to “an airbag that works all the time, except

- 25. What is Stressed VaR? The new component of stressed VaR is defined by the highest: Each

- 26. Definition of Operational Risk Risk of loss resulting from: inadequate or failed internal processes people systems

- 27. Basel II Pillar 1 – Operational Risk

- 28. Basic Indicator Approach (BIA) Banks using the BIA must hold capital for operational risk equal to

- 29. A Standardised Approach (SA) In the SA, banks’ activities are divided into eight business lines and

- 30. PILLAR 2: Supervisory Review SRP (Supervisory Review Process) ICAAP (Internal Capital Adequacy Assessment Process) SREP (Supervisory

- 31. Supervisory Review 4 Key Principals of Supervisory Review: Banks are required to have a process for

- 32. The supervisory review process is intended not only to ensure that banks have adequate capital to

- 33. Internal Capital Adequacy Assessment Process Credit Risk Operational Risk Market risk Pillar 1 Model Risk Settlement

- 34. PILLAR 3: Market discipline The goal is to encourage market discipline through the enhanced disclosure by

- 35. Information to disclosure should include: Capital structure and bank’s approach to assess the capital adequacy of

- 36. Problems with Basel 2 revealed by the financial crisis 2007 Supervisory capital ratios were not sufficiently

- 37. BASEL III On 12th of November 2010 the G20 leaders officially endorse the Basel III framework

- 38. Basel III squeezes capital Predominant form of Tier 1 capital should be common equity Common equity

- 39. Conservation buffer The purpose of the conservation buffer is to ensure that banks maintain a buffer

- 40. Countercyclical buffer Countercyclical buffer An extension of conservation buffer Imposed by national authority to curb excessive

- 41. Capital for Systemically Important Banks only Systemically important banks should have loss absorbing capacity beyond the

- 42. BASEL III: Total capital Total Regulatory Capital Ratio = [Total Capital] + [Capital Conservation Buffer] +

- 44. Скачать презентацию

AGENDA:

Functions of bank capital;

Definitions of Bank Capital, leverage ratio;

Structure of BASEL

AGENDA:

Functions of bank capital;

Definitions of Bank Capital, leverage ratio;

Structure of BASEL

Importance of Bank Capital

Absorb unanticipated losses and preserve confidence of

Importance of Bank Capital

Absorb unanticipated losses and preserve confidence of

Two DEFINITIONS of capital:

Economic = difference in the market value

Two DEFINITIONS of capital:

Economic = difference in the market value

Problem 1

Problem 1

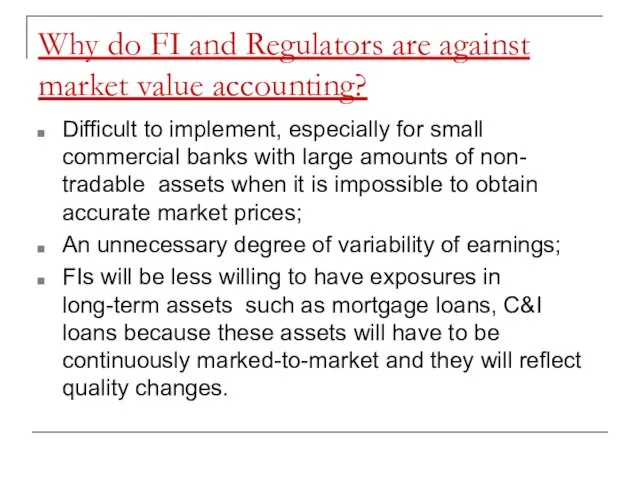

Why do FI and Regulators are against market value accounting?

Difficult to

Why do FI and Regulators are against market value accounting?

Difficult to

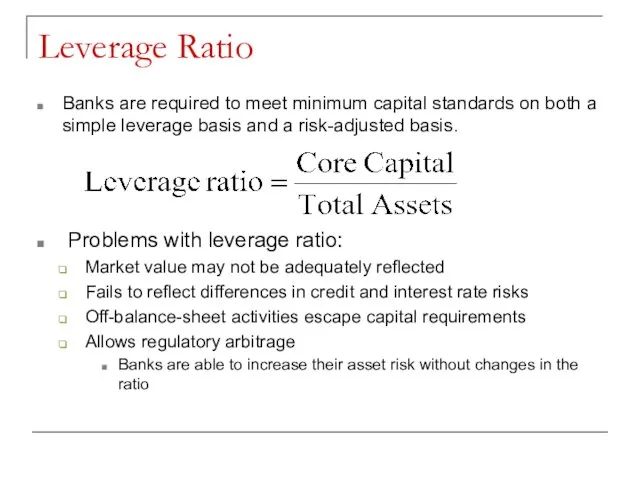

Leverage Ratio

Banks are required to meet minimum capital standards on both

Leverage Ratio

Banks are required to meet minimum capital standards on both

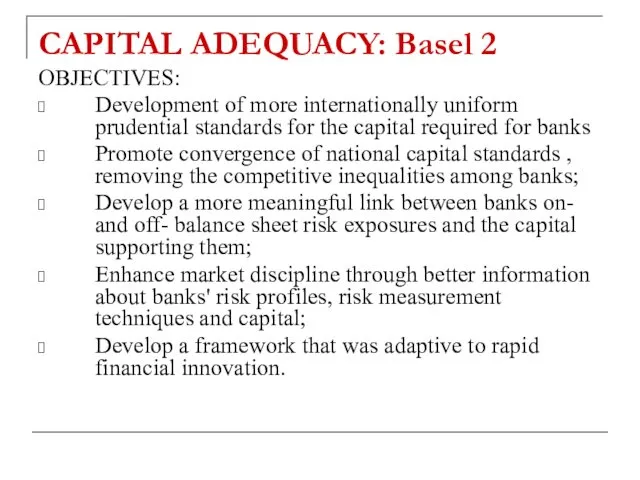

CAPITAL ADEQUACY: Basel 2

OBJECTIVES:

Development of more internationally uniform prudential standards

CAPITAL ADEQUACY: Basel 2

OBJECTIVES:

Development of more internationally uniform prudential standards

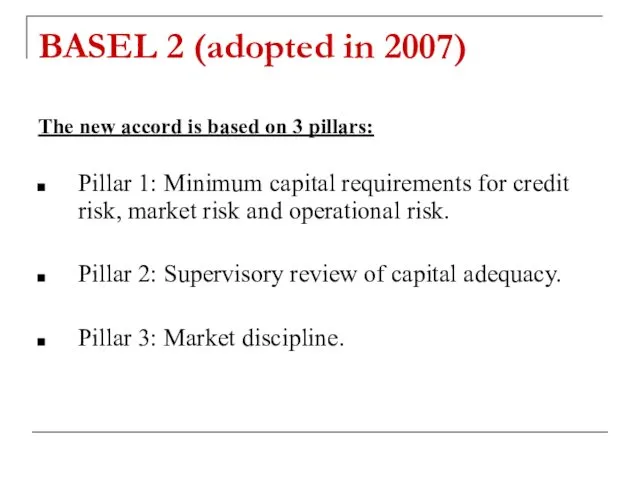

BASEL 2 (adopted in 2007)

The new accord is based on 3

BASEL 2 (adopted in 2007)

The new accord is based on 3

STRUCTURE OF BANK CAPITAL:

TIER 1 = Issued and fully

STRUCTURE OF BANK CAPITAL:

TIER 1 = Issued and fully

STRUCTURE OF BANK CAPITAL:

TIER 2 (SUPPLEMENTARY CAPITAL) =

+ Cumulative

STRUCTURE OF BANK CAPITAL:

TIER 2 (SUPPLEMENTARY CAPITAL) =

+ Cumulative

MINIMUM RATIOS:

LIMITS AND RESTRICTIONS:

Tier 2 capital cannot exceed Tier 1

MINIMUM RATIOS:

LIMITS AND RESTRICTIONS:

Tier 2 capital cannot exceed Tier 1

RISK WEIGHTED ASSETS

Total Risk-weighted Assets (TRWA) are determined by multiplying the

RISK WEIGHTED ASSETS

Total Risk-weighted Assets (TRWA) are determined by multiplying the

ESTIMATION OF RISK WEIGHTED ASSETS FOR CREDIT RISK: Standardized approach

R.W.

ESTIMATION OF RISK WEIGHTED ASSETS FOR CREDIT RISK: Standardized approach

R.W.

Standardised approach (use outside credit rating)

On Balance sheet assets are allocated

Standardised approach (use outside credit rating)

On Balance sheet assets are allocated

EXAMPLE: Step 1. Calculate Risk-Weighted on-Balance Sheet Assets

Each bank assigns its

EXAMPLE: Step 1. Calculate Risk-Weighted on-Balance Sheet Assets

Each bank assigns its

Step 2. Calculate Credit Equivalents for Off-Balance sheet Items other than

Step 2. Calculate Credit Equivalents for Off-Balance sheet Items other than

Step 3. Calculate Credit Equivalents for OTC Interest Rate and Foreign

Step 3. Calculate Credit Equivalents for OTC Interest Rate and Foreign

Step 4. Total Risk Weighted assets

Risk-Weighted assets for credit risk =

Step 4. Total Risk Weighted assets

Risk-Weighted assets for credit risk =

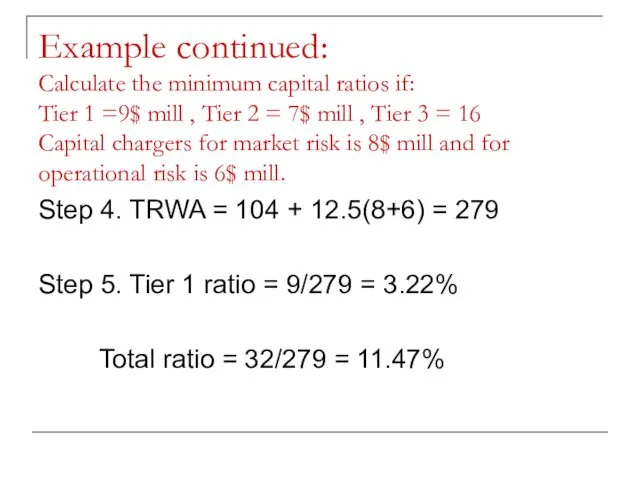

Example continued:

Calculate the minimum capital ratios if:

Tier 1 =9$ mill

Example continued: Calculate the minimum capital ratios if: Tier 1 =9$ mill

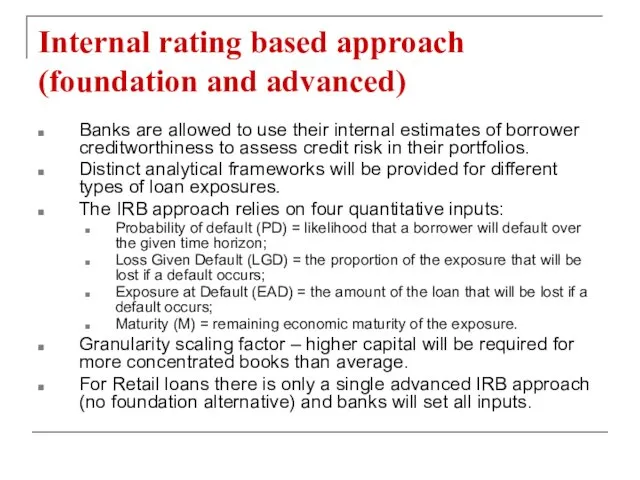

Internal rating based approach (foundation and advanced)

Banks are allowed to use

Internal rating based approach (foundation and advanced)

Banks are allowed to use

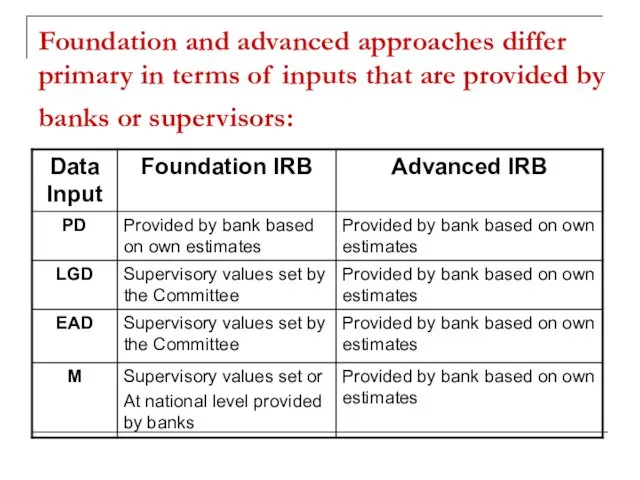

Foundation and advanced approaches differ primary in terms of inputs that

Foundation and advanced approaches differ primary in terms of inputs that

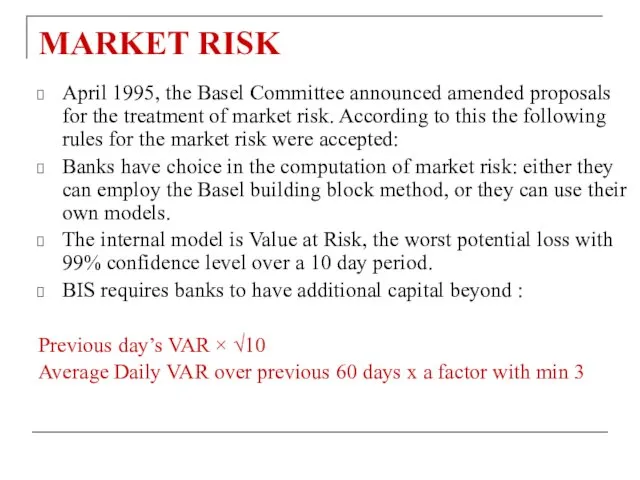

MARKET RISK

April 1995, the Basel Committee announced amended proposals for the

MARKET RISK

April 1995, the Basel Committee announced amended proposals for the

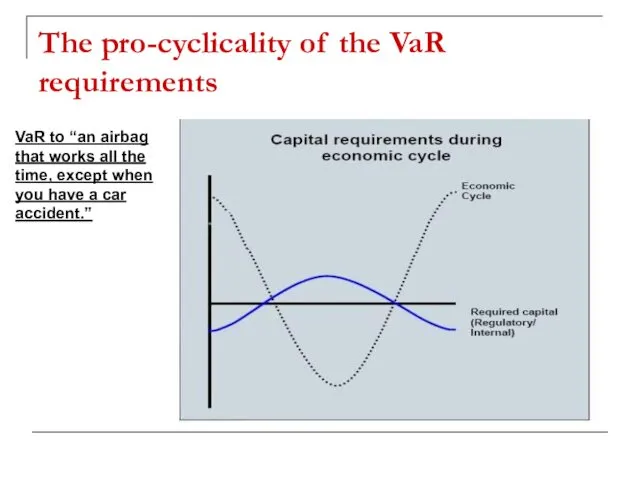

The pro-cyclicality of the VaR requirements

VaR to “an airbag that works

The pro-cyclicality of the VaR requirements

VaR to “an airbag that works

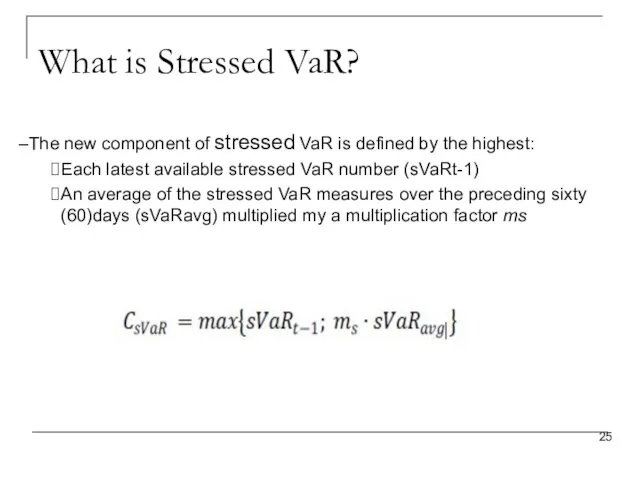

What is Stressed VaR?

The new component of stressed VaR is defined

What is Stressed VaR?

The new component of stressed VaR is defined

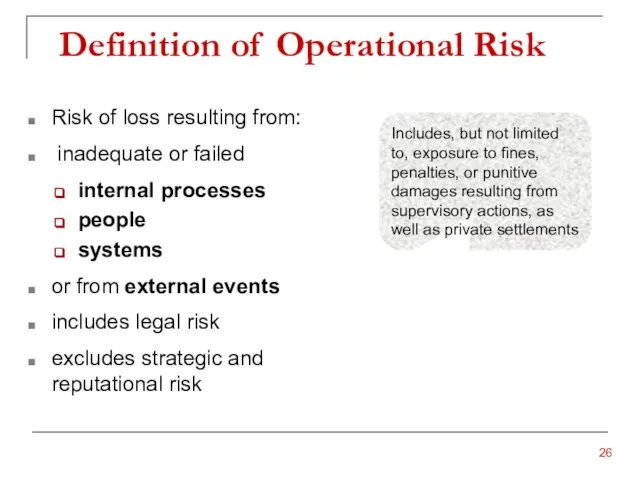

Definition of Operational Risk

Risk of loss resulting from:

inadequate or failed

internal

Definition of Operational Risk

Risk of loss resulting from:

inadequate or failed

internal

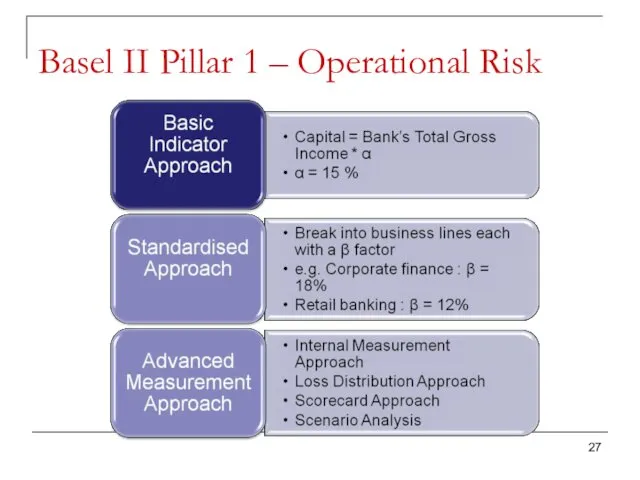

Basel II Pillar 1 – Operational Risk

Basel II Pillar 1 – Operational Risk

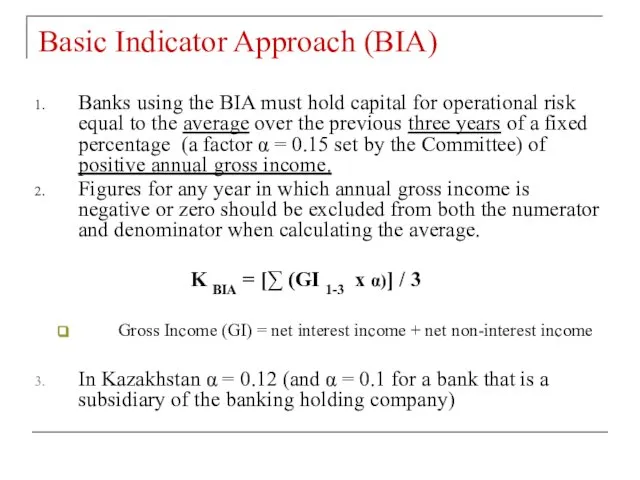

Basic Indicator Approach (BIA)

Banks using the BIA must hold capital for

Basic Indicator Approach (BIA)

Banks using the BIA must hold capital for

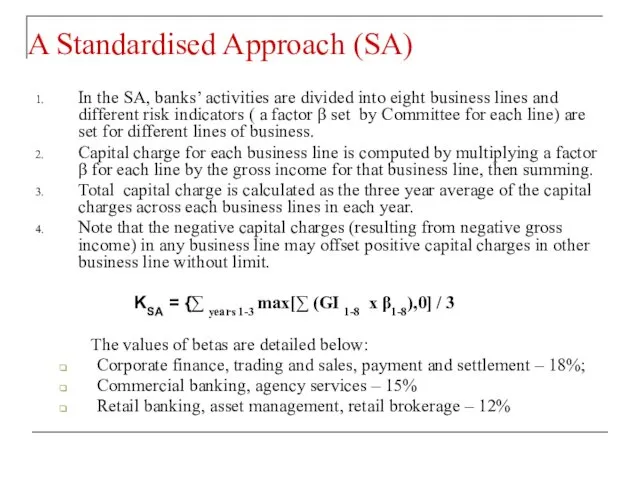

A Standardised Approach (SA)

In the SA, banks’ activities are divided into

A Standardised Approach (SA)

In the SA, banks’ activities are divided into

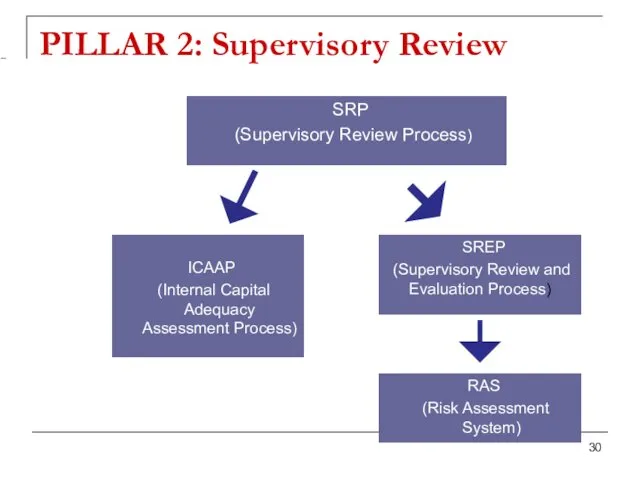

PILLAR 2: Supervisory Review

SRP

(Supervisory Review Process)

ICAAP

(Internal Capital Adequacy

PILLAR 2: Supervisory Review

SRP

(Supervisory Review Process)

ICAAP

(Internal Capital Adequacy

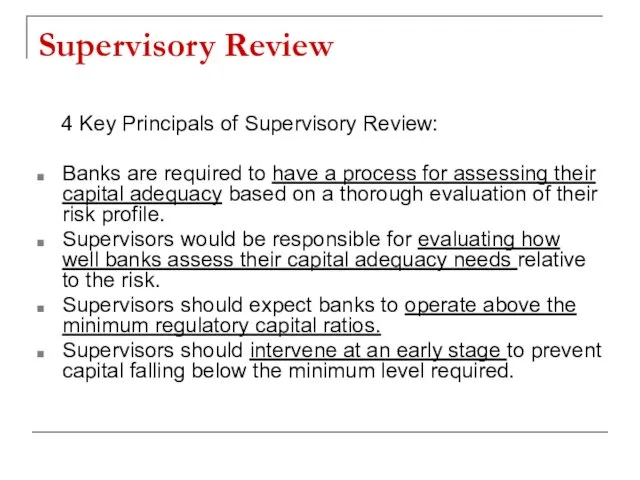

Supervisory Review

4 Key Principals of Supervisory Review:

Banks are required to

Supervisory Review

4 Key Principals of Supervisory Review:

Banks are required to

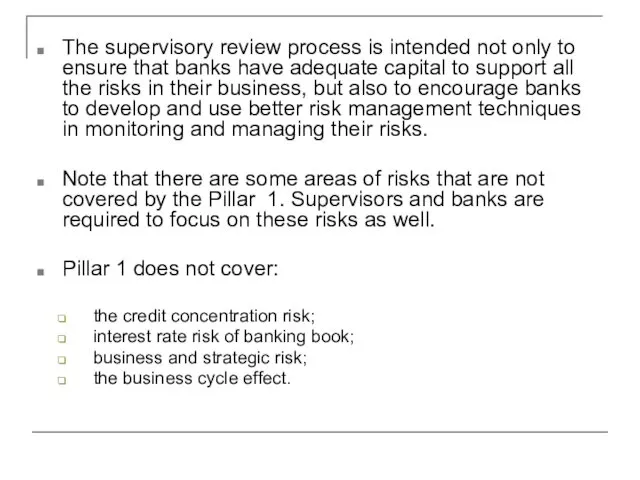

The supervisory review process is intended not only to ensure that

The supervisory review process is intended not only to ensure that

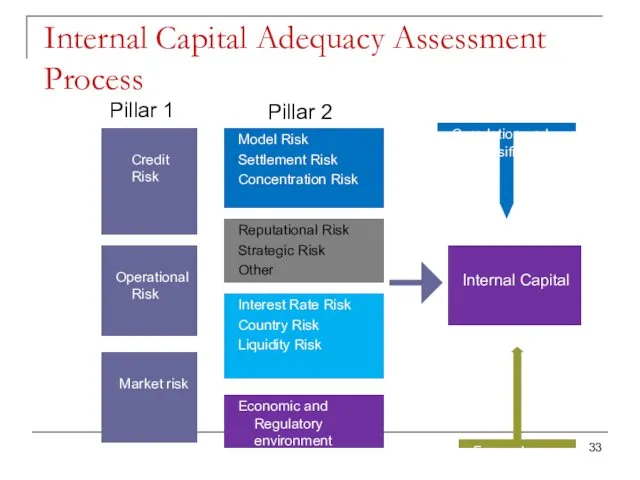

Internal Capital Adequacy Assessment Process

Credit Risk

Operational Risk

Market risk

Pillar 1

Model

Internal Capital Adequacy Assessment Process

Credit Risk

Operational Risk

Market risk

Pillar 1

Model

PILLAR 3: Market discipline

The goal is to encourage market discipline

PILLAR 3: Market discipline

The goal is to encourage market discipline

Information to disclosure should include:

Capital structure and bank’s approach to

Information to disclosure should include:

Capital structure and bank’s approach to

Problems with Basel 2 revealed by the financial crisis 2007

Supervisory capital

Problems with Basel 2 revealed by the financial crisis 2007

Supervisory capital

BASEL III

On 12th of November 2010 the G20 leaders officially

endorse

BASEL III

On 12th of November 2010 the G20 leaders officially endorse

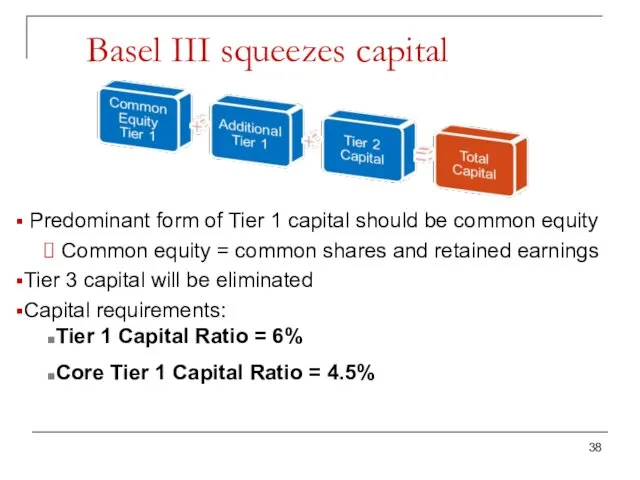

Basel III squeezes capital

Predominant form of Tier 1 capital should

Basel III squeezes capital

Predominant form of Tier 1 capital should

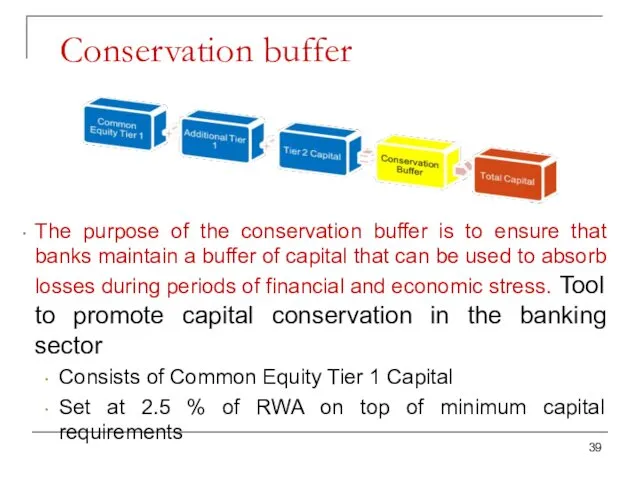

Conservation buffer

The purpose of the conservation buffer is to ensure that

Conservation buffer

The purpose of the conservation buffer is to ensure that

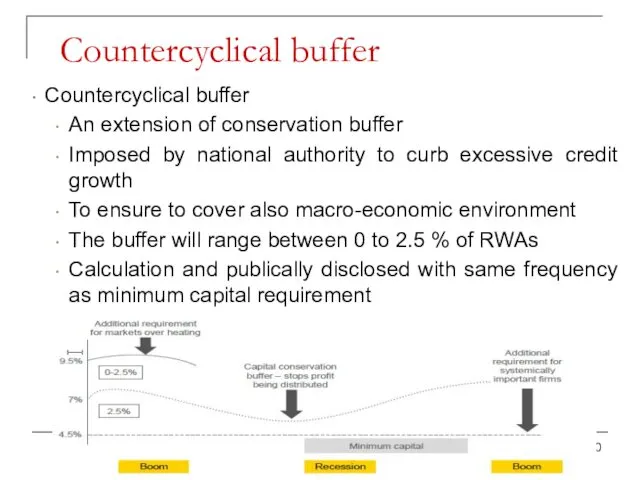

Countercyclical buffer

Countercyclical buffer

An extension of conservation buffer

Imposed by national authority to

Countercyclical buffer

Countercyclical buffer

An extension of conservation buffer

Imposed by national authority to

Capital for Systemically Important Banks only

Systemically important banks should have loss

Capital for Systemically Important Banks only

Systemically important banks should have loss

![BASEL III: Total capital Total Regulatory Capital Ratio = [Total Capital]](/_ipx/f_webp&q_80&fit_contain&s_1440x1080/imagesDir/jpg/462660/slide-41.jpg)

BASEL III: Total capital

Total Regulatory Capital Ratio =

[Total Capital]

BASEL III: Total capital

Total Regulatory Capital Ratio =

[Total Capital]

Колл-центр Лексикон крупнейший авторизированный партнёр АО Банк Тинькофф

Колл-центр Лексикон крупнейший авторизированный партнёр АО Банк Тинькофф Анализ финансовых результатов деятельности предприятия

Анализ финансовых результатов деятельности предприятия Финансовые пирамиды 1990-х: причины и последствия

Финансовые пирамиды 1990-х: причины и последствия Деньги. виды денег

Деньги. виды денег Учет основных средств

Учет основных средств Последние изменения в нормативные правовые акты, касающиеся вопросов ценообразования, в сфере электроэнергетики

Последние изменения в нормативные правовые акты, касающиеся вопросов ценообразования, в сфере электроэнергетики Развитие национальной платежной системы

Развитие национальной платежной системы Making banking accessible for Pakistan

Making banking accessible for Pakistan Природа форм и видов денег

Природа форм и видов денег Концептуальные основы оценки бизнеса. Нормативно-правовая база в сфере оценочной деятельности. (Лекция 1)

Концептуальные основы оценки бизнеса. Нормативно-правовая база в сфере оценочной деятельности. (Лекция 1) Исследование рынка фитнес услуг

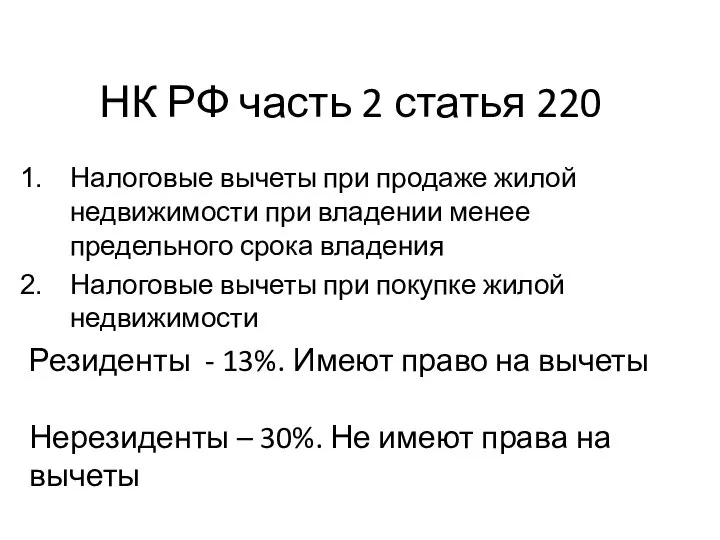

Исследование рынка фитнес услуг НК РФ часть 2 статья 220

НК РФ часть 2 статья 220 Модели продолжения тенденции

Модели продолжения тенденции Региональные налоги: понятие, виды, порядок начисления и сроки уплаты. Тема № 10

Региональные налоги: понятие, виды, порядок начисления и сроки уплаты. Тема № 10 Бюджет муниципального образования Лабинский район на 2018 год и плановый период 2019 и 2020 годов

Бюджет муниципального образования Лабинский район на 2018 год и плановый период 2019 и 2020 годов Страхование дома. Классические продукты ИФЛ: квартира-комфорт, усадьба

Страхование дома. Классические продукты ИФЛ: квартира-комфорт, усадьба Звіт з виробничої технологічної практики

Звіт з виробничої технологічної практики Ризик-менеджмент у банку

Ризик-менеджмент у банку Изменения в экзаменационной модели ГИА. Банковские услуги

Изменения в экзаменационной модели ГИА. Банковские услуги Банковская система РФ

Банковская система РФ Что такое налоги и почему их надо платить

Что такое налоги и почему их надо платить Создание условий для формирования основ финансовой грамотности в детском саду

Создание условий для формирования основ финансовой грамотности в детском саду Финансовые результаты деятельности предприятия

Финансовые результаты деятельности предприятия Учет и анализ в физкультурно-спортивных организациях. Понятие о счетах бухгалтерского учета

Учет и анализ в физкультурно-спортивных организациях. Понятие о счетах бухгалтерского учета ЗП для коммерческих организаций

ЗП для коммерческих организаций HFT стратегии, фронтранинг на быстром рынке

HFT стратегии, фронтранинг на быстром рынке Організація процесу аудиторської перевірки фінансової звітності та її інформаційного забезпечення. (Тема 3)

Організація процесу аудиторської перевірки фінансової звітності та її інформаційного забезпечення. (Тема 3) Статистика материальных оборотных ресурсов

Статистика материальных оборотных ресурсов