- Time series models. Static models and models with lags

Содержание

- 2. 2 HOUS is aggregate consumer expenditure on housing services and DPI is aggregate disposable personal income.

- 3. 3 PRELHOUS is a relative price index for housing services constructed by dividing the nominal price

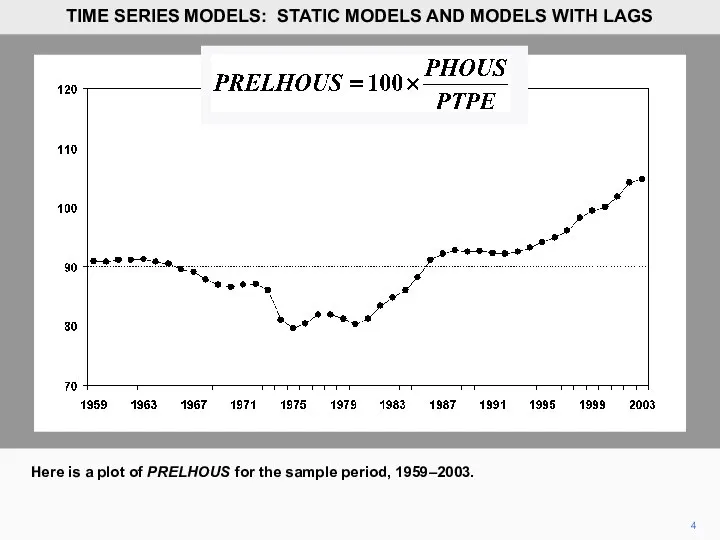

- 4. 4 Here is a plot of PRELHOUS for the sample period, 1959–2003. TIME SERIES MODELS: STATIC

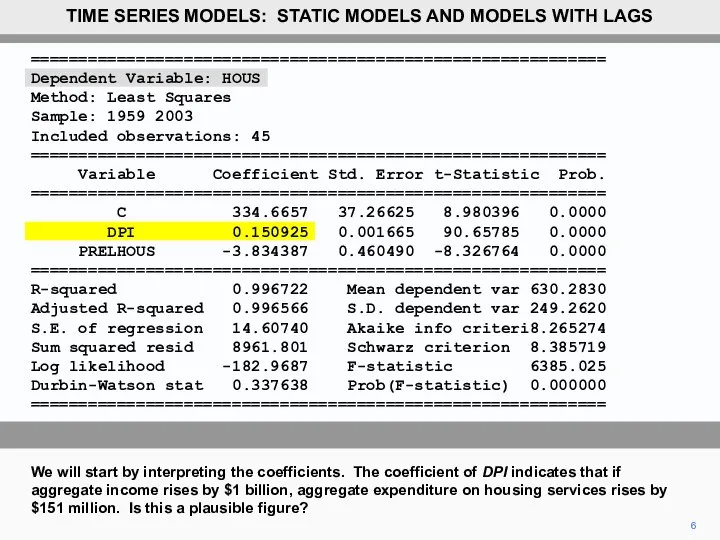

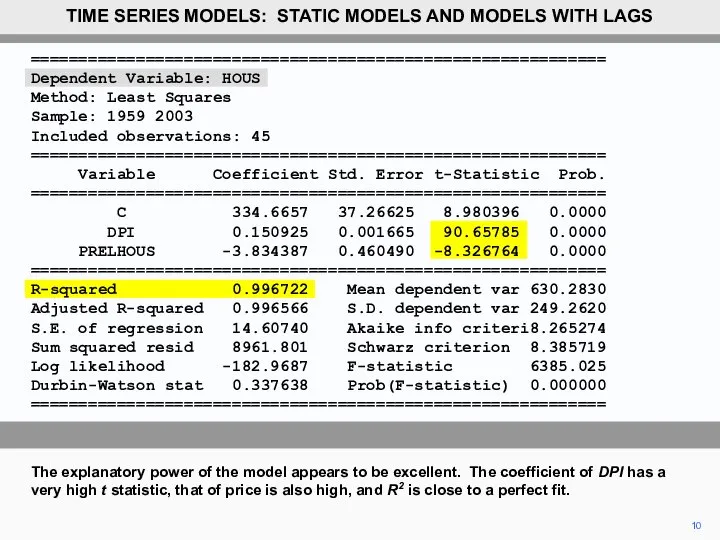

- 5. ============================================================ Dependent Variable: HOUS Method: Least Squares Sample: 1959 2003 Included observations: 45 ============================================================ Variable Coefficient

- 6. ============================================================ Dependent Variable: HOUS Method: Least Squares Sample: 1959 2003 Included observations: 45 ============================================================ Variable Coefficient

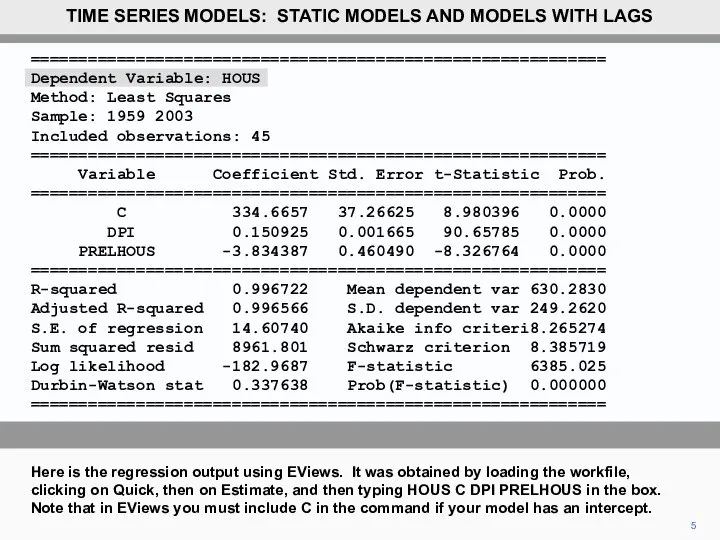

- 7. 7 Possibly. It implies that 15 cents out of the marginal dollar are spent on housing.

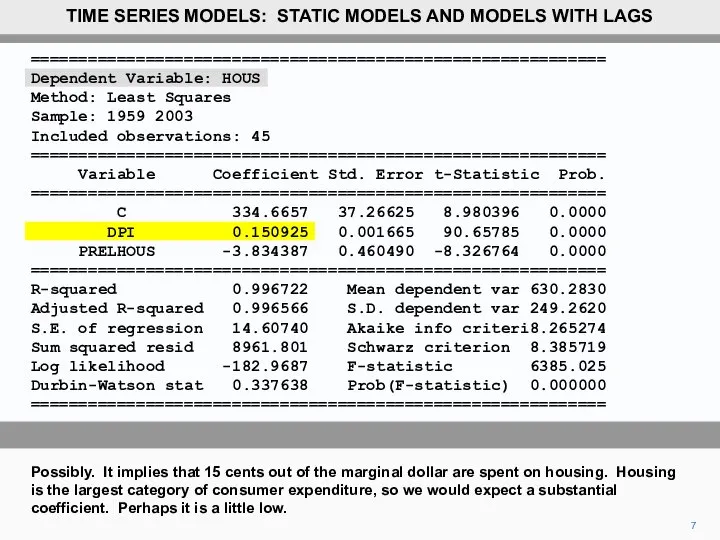

- 8. 8 The coefficient of PRELHOUS indicates that a one-point increase in this price index causes expenditure

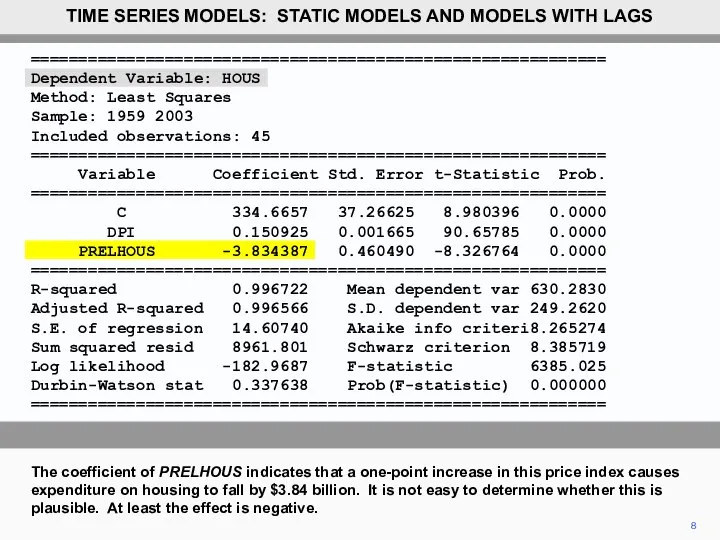

- 9. 9 The constant has no meaningful interpretation. (Literally, it indicates that $335 billion would be spent

- 10. ============================================================ Dependent Variable: HOUS Method: Least Squares Sample: 1959 2003 Included observations: 45 ============================================================ Variable Coefficient

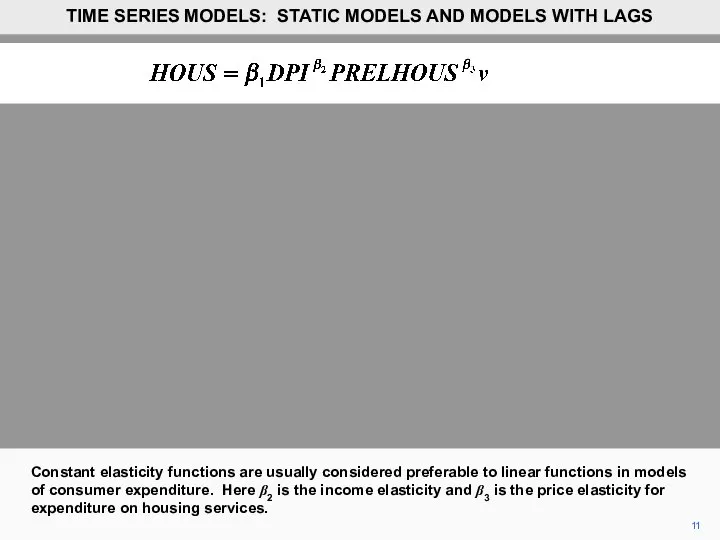

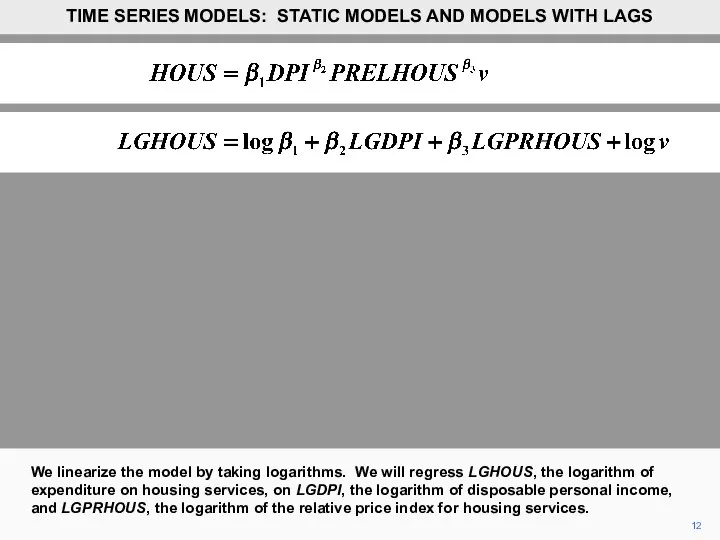

- 11. 11 Constant elasticity functions are usually considered preferable to linear functions in models of consumer expenditure.

- 12. 12 We linearize the model by taking logarithms. We will regress LGHOUS, the logarithm of expenditure

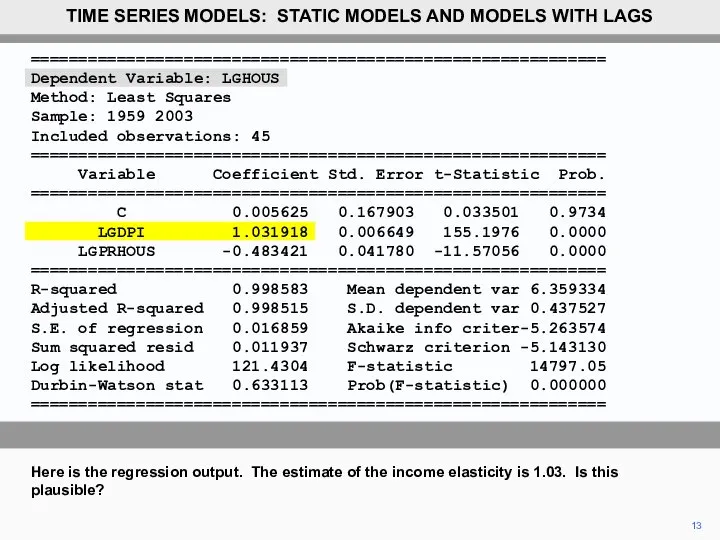

- 13. ============================================================ Dependent Variable: LGHOUS Method: Least Squares Sample: 1959 2003 Included observations: 45 ============================================================ Variable Coefficient

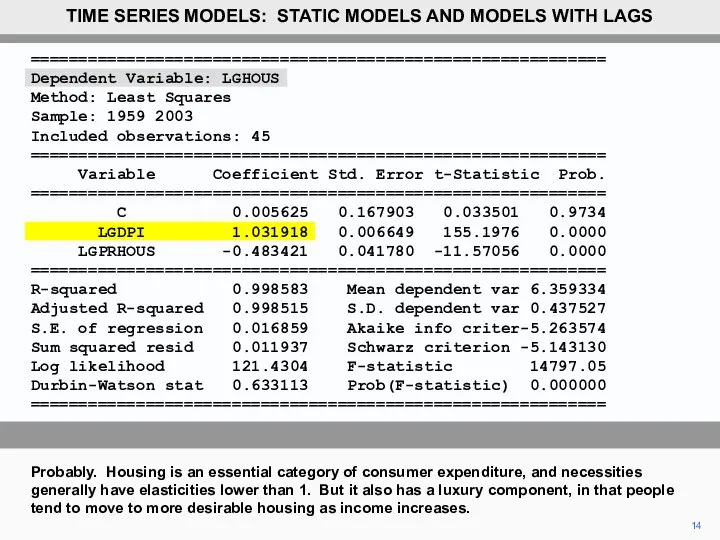

- 14. 14 Probably. Housing is an essential category of consumer expenditure, and necessities generally have elasticities lower

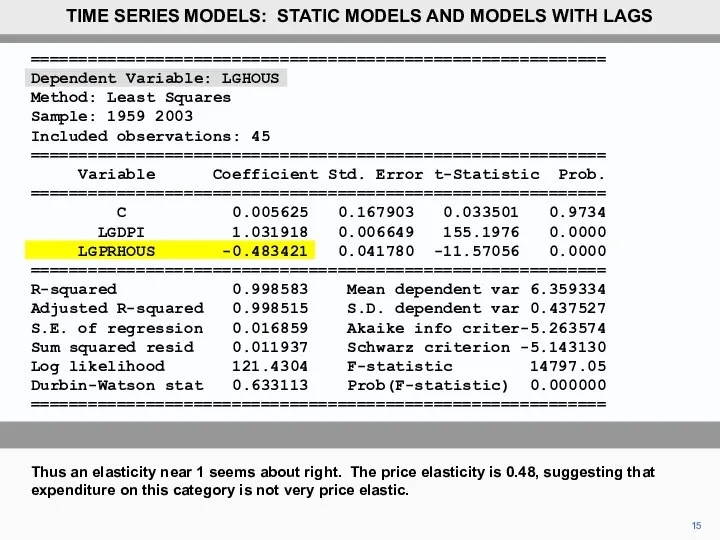

- 15. 15 Thus an elasticity near 1 seems about right. The price elasticity is 0.48, suggesting that

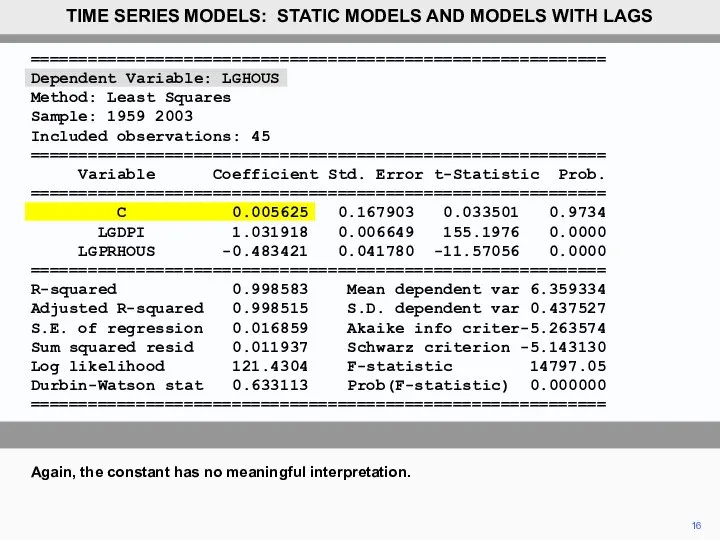

- 16. 16 Again, the constant has no meaningful interpretation. TIME SERIES MODELS: STATIC MODELS AND MODELS WITH

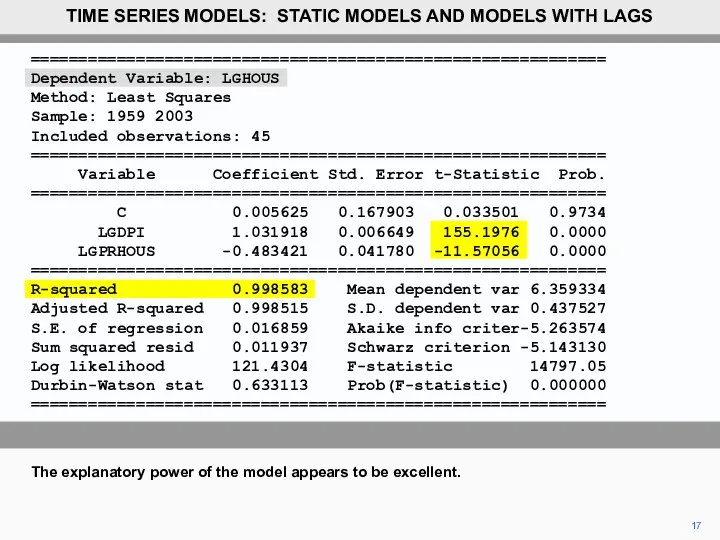

- 17. 17 The explanatory power of the model appears to be excellent. TIME SERIES MODELS: STATIC MODELS

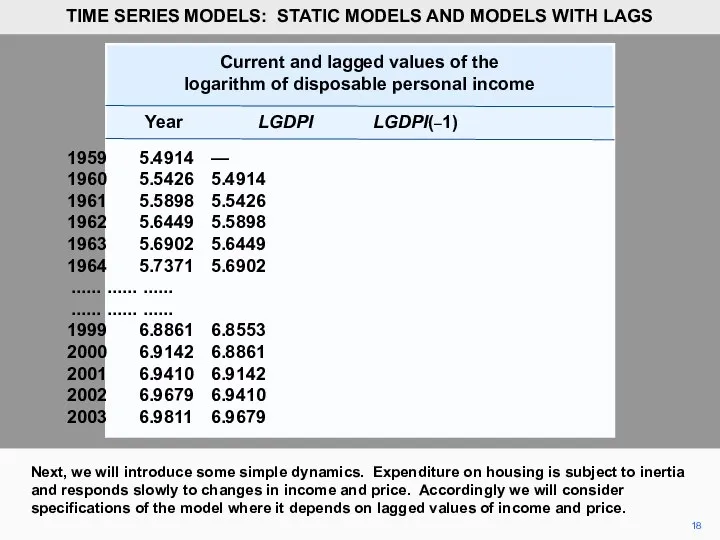

- 18. 18 Next, we will introduce some simple dynamics. Expenditure on housing is subject to inertia and

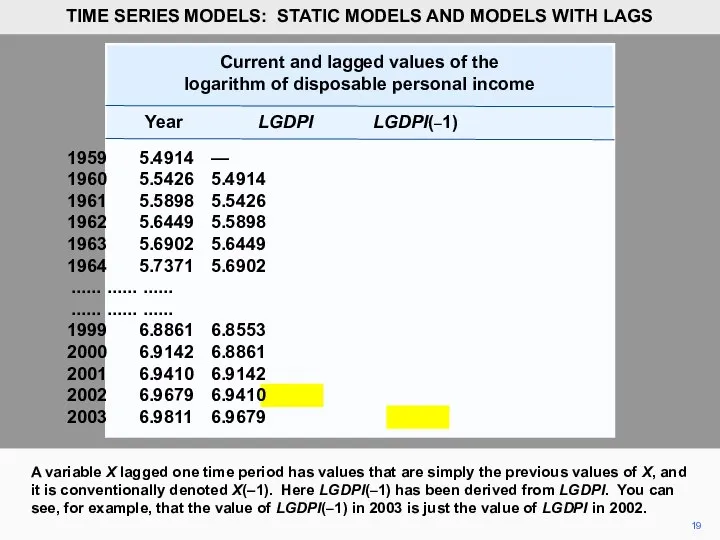

- 19. 19 A variable X lagged one time period has values that are simply the previous values

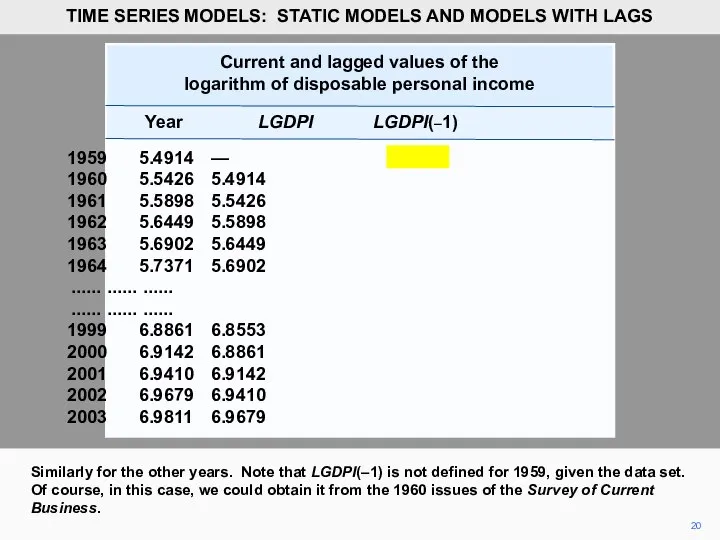

- 20. Current and lagged values of the logarithm of disposable personal income Year LGDPI LGDPI(–1) 1959 5.4914

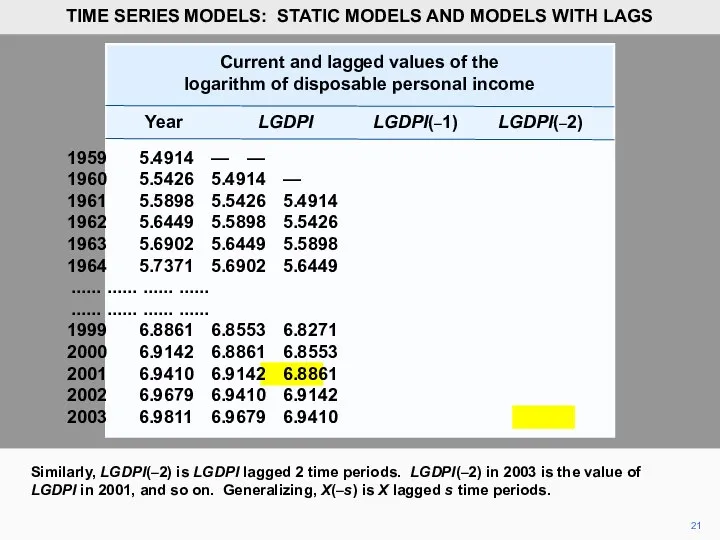

- 21. Current and lagged values of the logarithm of disposable personal income Year LGDPI LGDPI(–1) LGDPI(–2) 1959

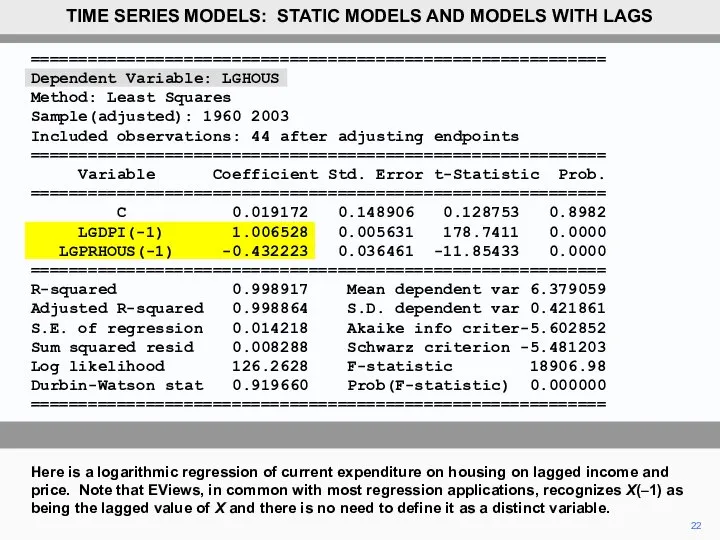

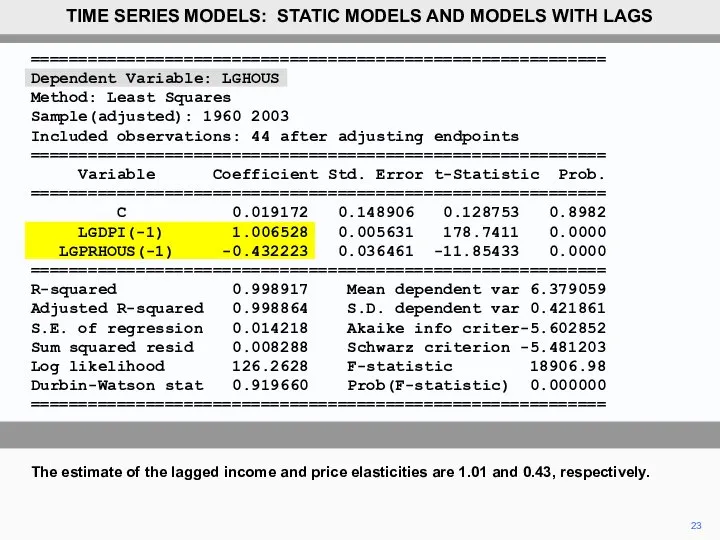

- 22. ============================================================ Dependent Variable: LGHOUS Method: Least Squares Sample(adjusted): 1960 2003 Included observations: 44 after adjusting endpoints

- 23. 23 The estimate of the lagged income and price elasticities are 1.01 and 0.43, respectively. TIME

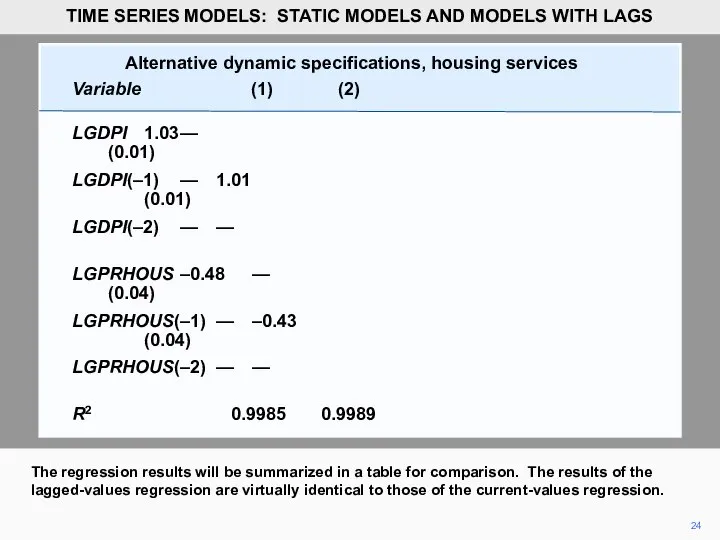

- 24. 24 The regression results will be summarized in a table for comparison. The results of the

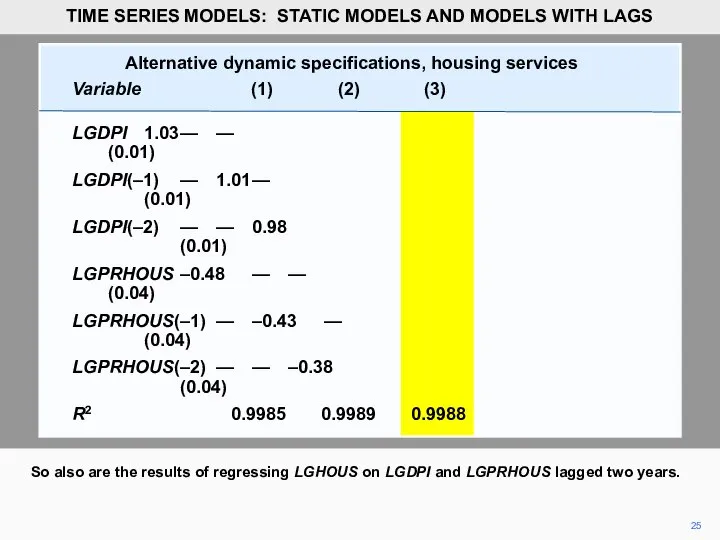

- 25. 25 So also are the results of regressing LGHOUS on LGDPI and LGPRHOUS lagged two years.

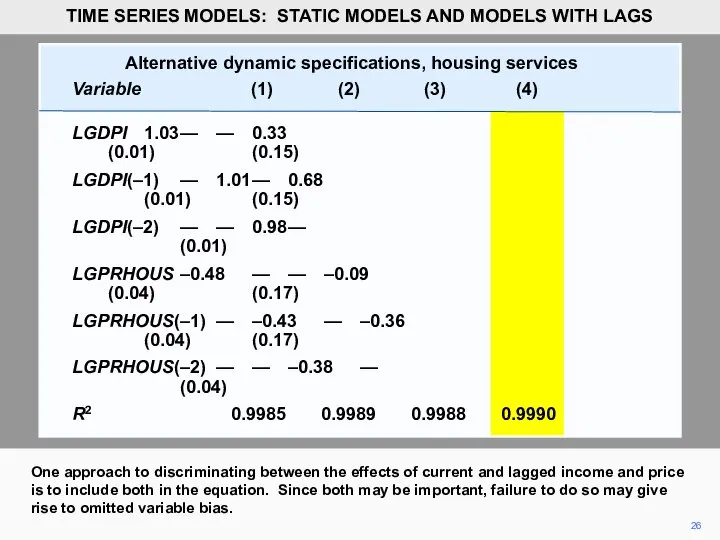

- 26. 26 One approach to discriminating between the effects of current and lagged income and price is

- 27. 27 With the current values of income and price, and their values lagged one year, we

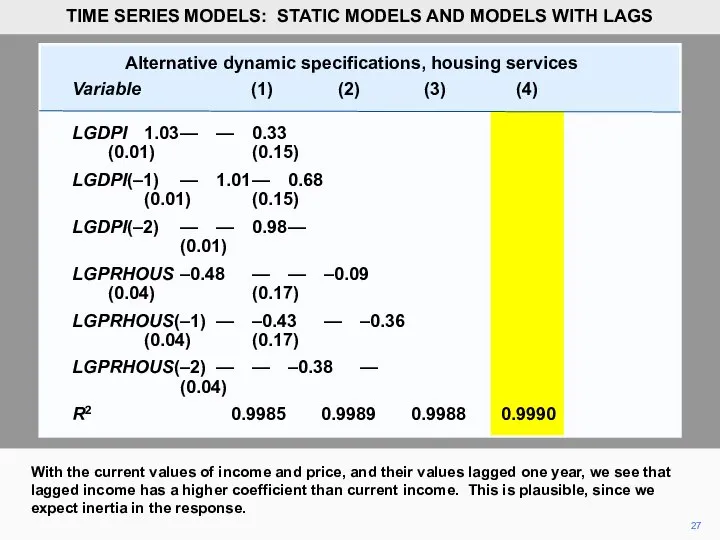

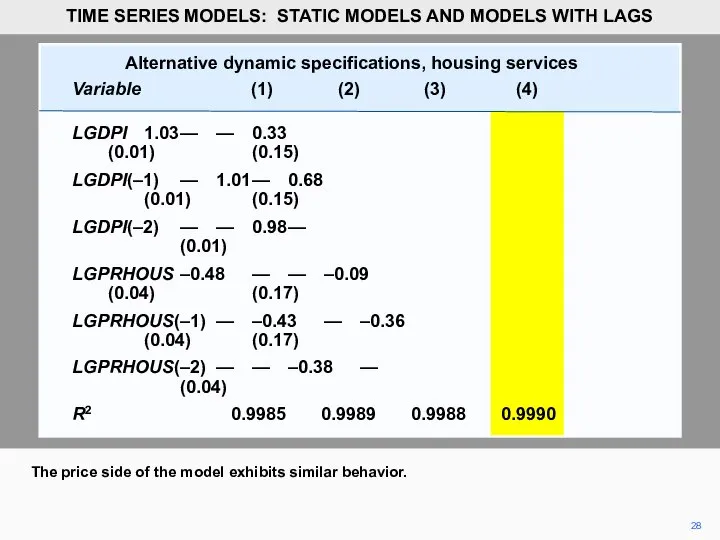

- 28. 28 The price side of the model exhibits similar behavior. TIME SERIES MODELS: STATIC MODELS AND

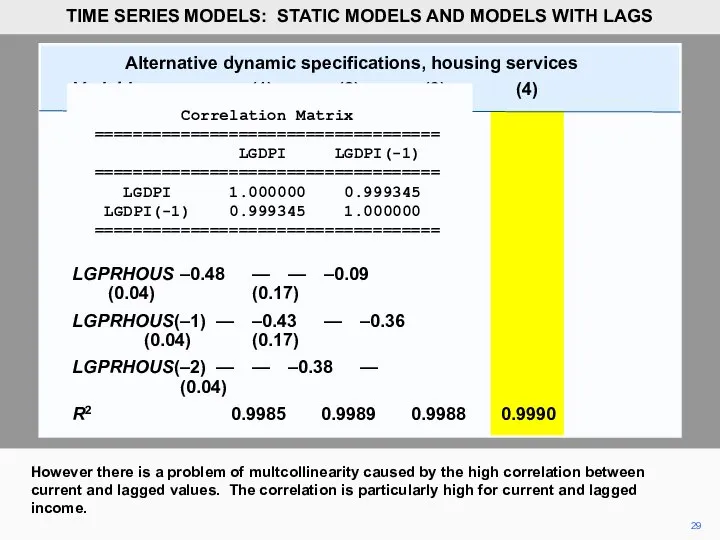

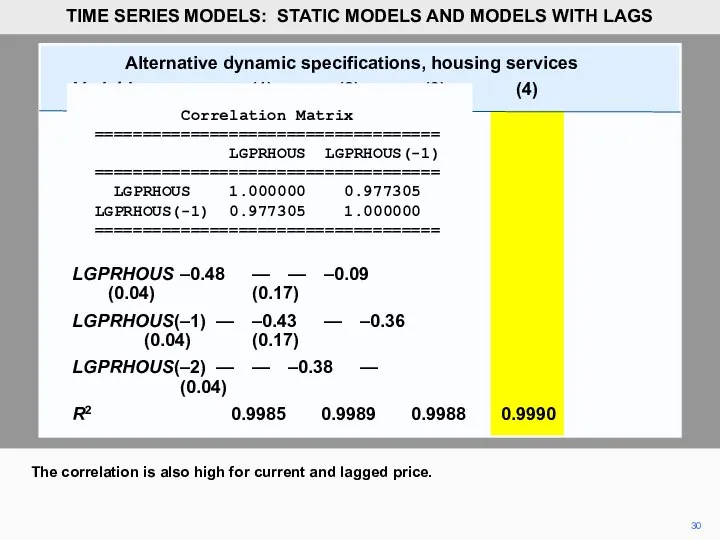

- 29. 29 However there is a problem of multcollinearity caused by the high correlation between current and

- 30. Alternative dynamic specifications, housing services Variable (1) (2) (3) (4) LGDPI 1.03 — — 0.33 (0.01)

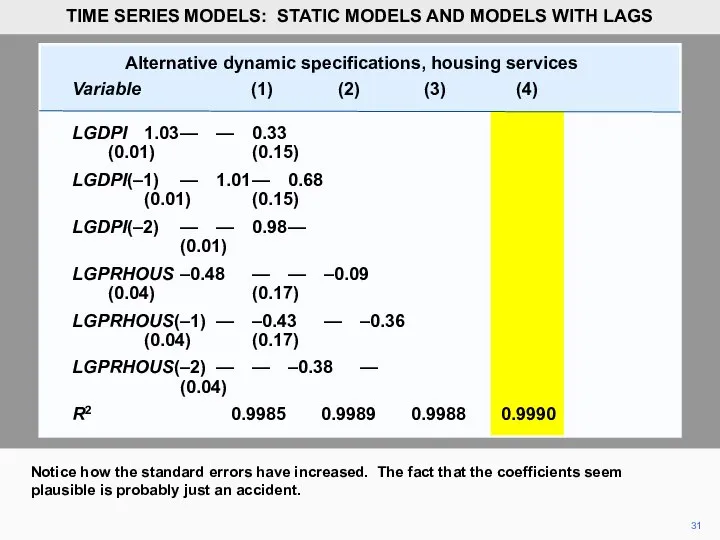

- 31. 31 Notice how the standard errors have increased. The fact that the coefficients seem plausible is

- 32. Alternative dynamic specifications, housing services Variable (1) (2) (3) (4) (5) LGDPI 1.03 — — 0.33

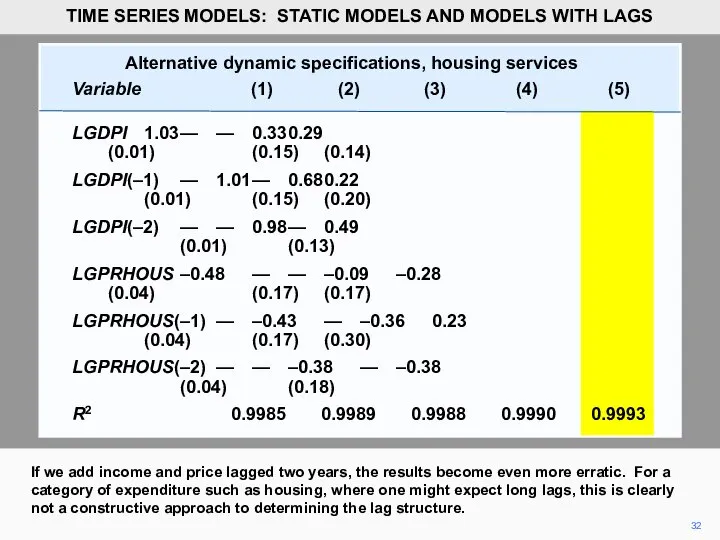

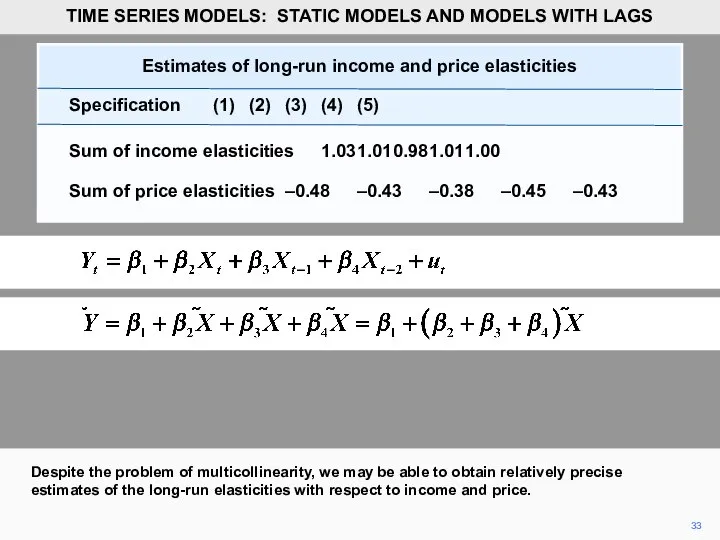

- 33. 33 Despite the problem of multicollinearity, we may be able to obtain relatively precise estimates of

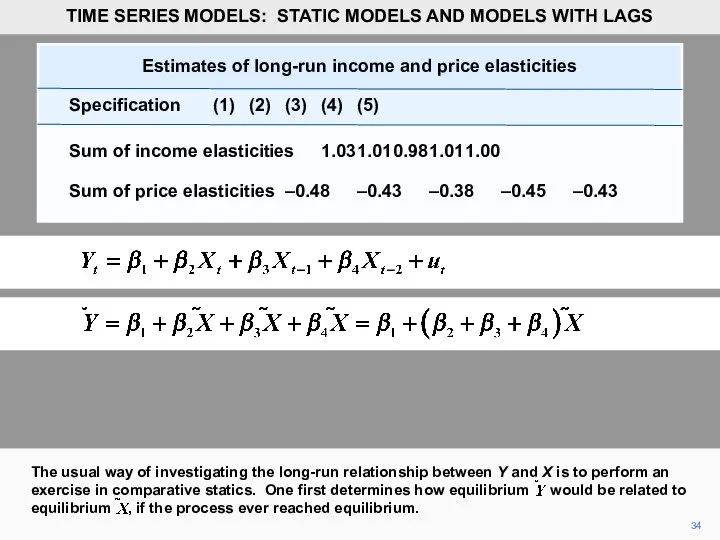

- 34. 34 The usual way of investigating the long-run relationship between Y and X is to perform

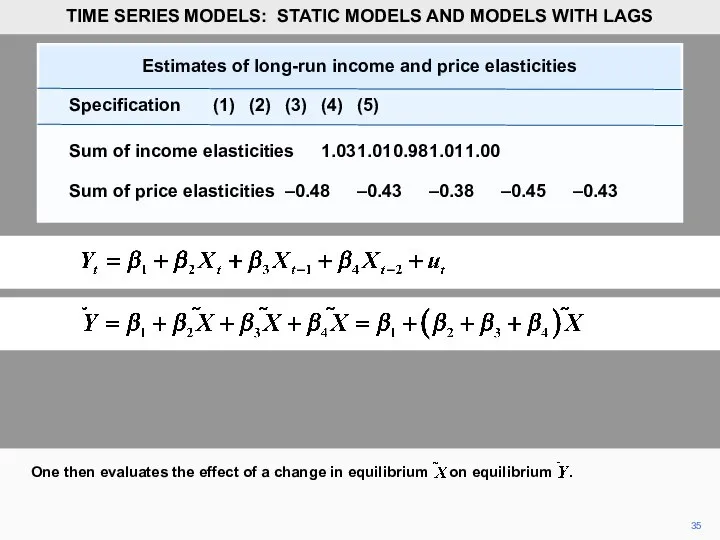

- 35. 35 One then evaluates the effect of a change in equilibrium on equilibrium . TIME SERIES

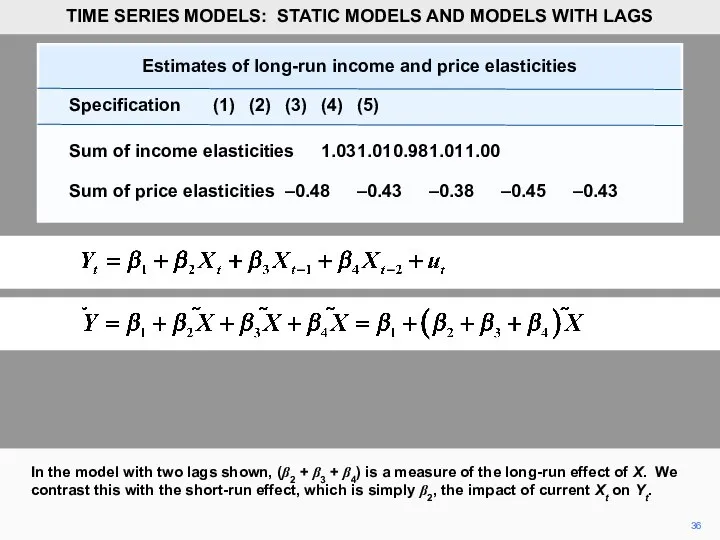

- 36. 36 In the model with two lags shown, (β2 + β3 + β4) is a measure

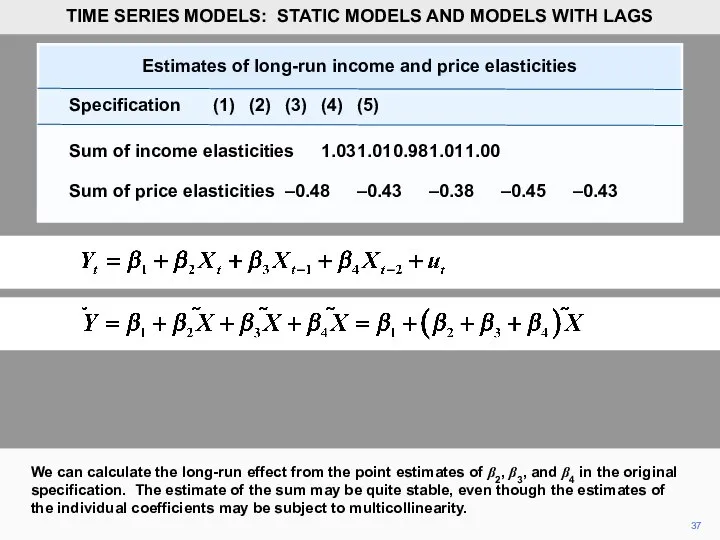

- 37. 37 We can calculate the long-run effect from the point estimates of β2, β3, and β4

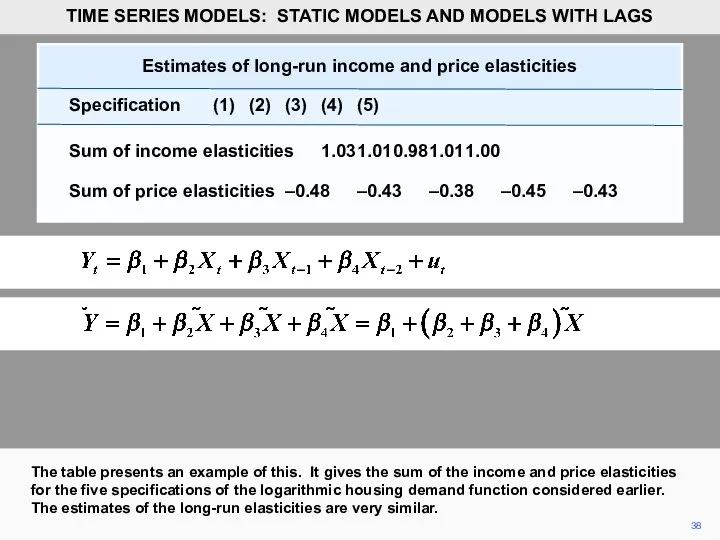

- 38. 38 The table presents an example of this. It gives the sum of the income and

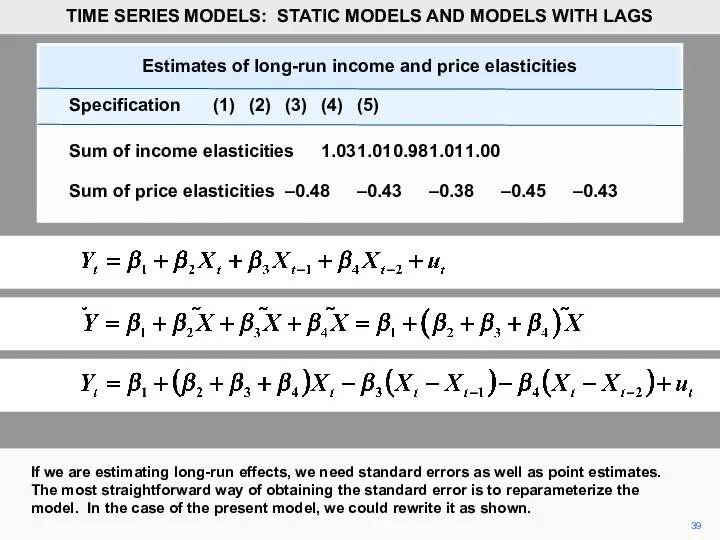

- 39. 39 If we are estimating long-run effects, we need standard errors as well as point estimates.

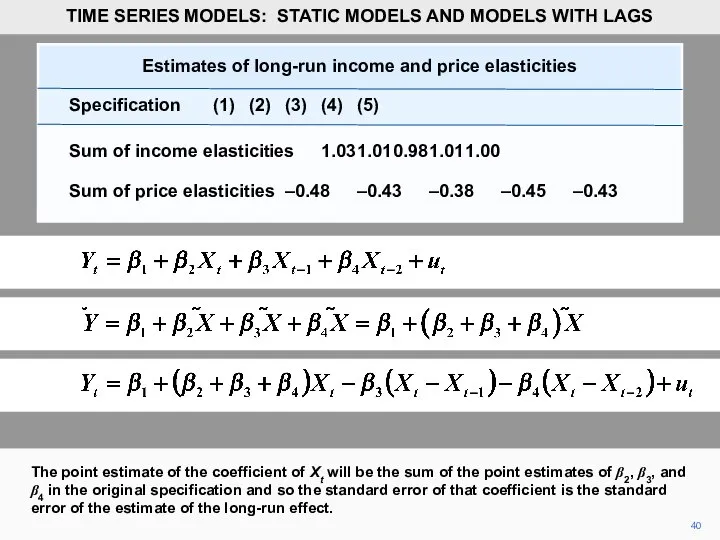

- 40. 40 The point estimate of the coefficient of Xt will be the sum of the point

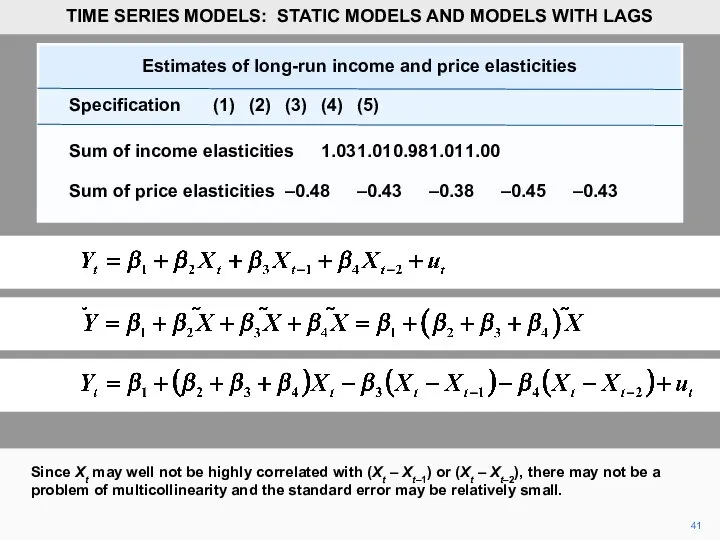

- 41. 41 Since Xt may well not be highly correlated with (Xt – Xt–1) or (Xt –

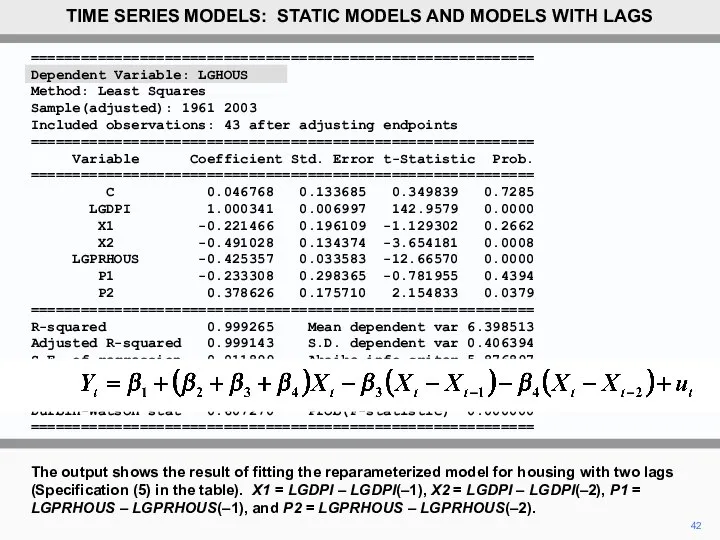

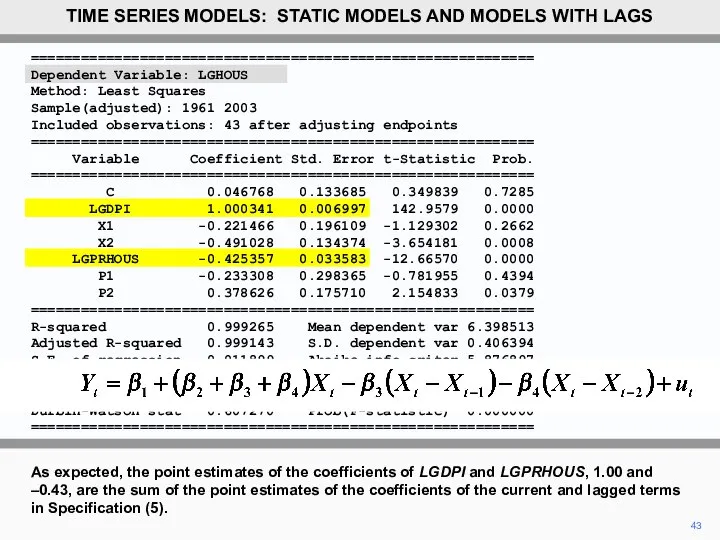

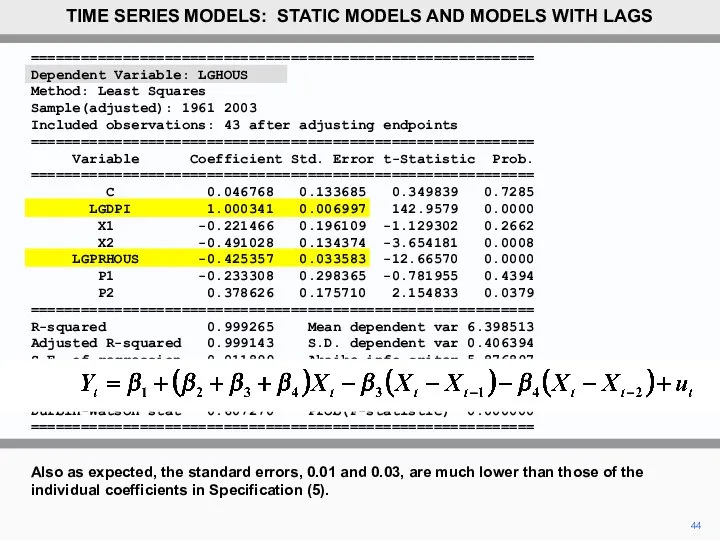

- 42. ============================================================ Dependent Variable: LGHOUS Method: Least Squares Sample(adjusted): 1961 2003 Included observations: 43 after adjusting endpoints

- 43. 43 As expected, the point estimates of the coefficients of LGDPI and LGPRHOUS, 1.00 and –0.43,

- 44. 44 Also as expected, the standard errors, 0.01 and 0.03, are much lower than those of

- 46. Скачать презентацию

2

HOUS is aggregate consumer expenditure on housing services and DPI is

2

HOUS is aggregate consumer expenditure on housing services and DPI is

3

PRELHOUS is a relative price index for housing services constructed by

3

PRELHOUS is a relative price index for housing services constructed by

4

Here is a plot of PRELHOUS for the sample period, 1959–2003.

TIME

4

Here is a plot of PRELHOUS for the sample period, 1959–2003.

TIME

============================================================

Dependent Variable: HOUS

Method: Least Squares

Sample: 1959 2003

Included observations:

============================================================

Dependent Variable: HOUS

Method: Least Squares

Sample: 1959 2003

Included observations:

============================================================

Dependent Variable: HOUS

Method: Least Squares

Sample: 1959 2003

Included observations:

============================================================

Dependent Variable: HOUS

Method: Least Squares

Sample: 1959 2003

Included observations:

7

Possibly. It implies that 15 cents out of the marginal dollar

7

Possibly. It implies that 15 cents out of the marginal dollar

8

The coefficient of PRELHOUS indicates that a one-point increase in this

8

The coefficient of PRELHOUS indicates that a one-point increase in this

9

The constant has no meaningful interpretation. (Literally, it indicates that $335

9

The constant has no meaningful interpretation. (Literally, it indicates that $335

============================================================

Dependent Variable: HOUS

Method: Least Squares

Sample: 1959 2003

Included observations:

============================================================

Dependent Variable: HOUS

Method: Least Squares

Sample: 1959 2003

Included observations:

11

Constant elasticity functions are usually considered preferable to linear functions in

11

Constant elasticity functions are usually considered preferable to linear functions in

12

We linearize the model by taking logarithms. We will regress LGHOUS,

12

We linearize the model by taking logarithms. We will regress LGHOUS,

============================================================

Dependent Variable: LGHOUS

Method: Least Squares

Sample: 1959 2003

Included observations:

============================================================

Dependent Variable: LGHOUS

Method: Least Squares

Sample: 1959 2003

Included observations:

14

Probably. Housing is an essential category of consumer expenditure, and necessities

14

Probably. Housing is an essential category of consumer expenditure, and necessities

15

Thus an elasticity near 1 seems about right. The price elasticity

15

Thus an elasticity near 1 seems about right. The price elasticity

16

Again, the constant has no meaningful interpretation.

TIME SERIES MODELS: STATIC MODELS

16

Again, the constant has no meaningful interpretation.

TIME SERIES MODELS: STATIC MODELS

17

The explanatory power of the model appears to be excellent.

TIME SERIES

17

The explanatory power of the model appears to be excellent.

TIME SERIES

18

Next, we will introduce some simple dynamics. Expenditure on housing is

18

Next, we will introduce some simple dynamics. Expenditure on housing is

19

A variable X lagged one time period has values that are

19

A variable X lagged one time period has values that are

Current and lagged values of the

logarithm of disposable personal income

Year

Current and lagged values of the

logarithm of disposable personal income

Year

Current and lagged values of the

logarithm of disposable personal income

Year

Current and lagged values of the

logarithm of disposable personal income

Year

============================================================

Dependent Variable: LGHOUS

Method: Least Squares

Sample(adjusted): 1960 2003

Included observations:

============================================================

Dependent Variable: LGHOUS

Method: Least Squares

Sample(adjusted): 1960 2003

Included observations:

23

The estimate of the lagged income and price elasticities are 1.01

23

The estimate of the lagged income and price elasticities are 1.01

24

The regression results will be summarized in a table for comparison.

24

The regression results will be summarized in a table for comparison.

25

So also are the results of regressing LGHOUS on LGDPI and

25

So also are the results of regressing LGHOUS on LGDPI and

26

One approach to discriminating between the effects of current and lagged

26

One approach to discriminating between the effects of current and lagged

27

With the current values of income and price, and their values

27

With the current values of income and price, and their values

28

The price side of the model exhibits similar behavior.

TIME SERIES MODELS:

28

The price side of the model exhibits similar behavior.

TIME SERIES MODELS:

29

However there is a problem of multcollinearity caused by the high

29

However there is a problem of multcollinearity caused by the high

Alternative dynamic specifications, housing services

Variable (1) (2) (3) (4)

LGDPI 1.03 — — 0.33

(0.01) (0.15)

LGDPI(–1) — 1.01 — 0.68

(0.01) (0.15)

LGDPI(–2) — — 0.98 —

(0.01)

LGPRHOUS –0.48 — — –0.09

(0.04) (0.17)

LGPRHOUS(–1) — –0.43 — –0.36

(0.04) (0.17)

LGPRHOUS(–2) — — –0.38 —

(0.04)

R2 0.9985

Variable (1) (2) (3) (4)

LGDPI 1.03 — — 0.33

(0.01) (0.15)

LGDPI(–1) — 1.01 — 0.68

(0.01) (0.15)

LGDPI(–2) — — 0.98 —

(0.01)

LGPRHOUS –0.48 — — –0.09

(0.04) (0.17)

LGPRHOUS(–1) — –0.43 — –0.36

(0.04) (0.17)

LGPRHOUS(–2) — — –0.38 —

(0.04)

R2 0.9985

31

Notice how the standard errors have increased. The fact that the

31

Notice how the standard errors have increased. The fact that the

Alternative dynamic specifications, housing services

Variable (1) (2) (3) (4) (5)

LGDPI 1.03 — — 0.33 0.29

(0.01) (0.15) (0.14)

LGDPI(–1) — 1.01 — 0.68 0.22

(0.01) (0.15) (0.20)

LGDPI(–2) — — 0.98 — 0.49

(0.01) (0.13)

LGPRHOUS –0.48 — — –0.09 –0.28

(0.04) (0.17) (0.17)

LGPRHOUS(–1) — –0.43 — –0.36 0.23

(0.04) (0.17) (0.30)

LGPRHOUS(–2) — — –0.38 — –0.38

(0.04) (0.18)

R2 0.9985

Variable (1) (2) (3) (4) (5)

LGDPI 1.03 — — 0.33 0.29

(0.01) (0.15) (0.14)

LGDPI(–1) — 1.01 — 0.68 0.22

(0.01) (0.15) (0.20)

LGDPI(–2) — — 0.98 — 0.49

(0.01) (0.13)

LGPRHOUS –0.48 — — –0.09 –0.28

(0.04) (0.17) (0.17)

LGPRHOUS(–1) — –0.43 — –0.36 0.23

(0.04) (0.17) (0.30)

LGPRHOUS(–2) — — –0.38 — –0.38

(0.04) (0.18)

R2 0.9985

33

Despite the problem of multicollinearity, we may be able to obtain

33

Despite the problem of multicollinearity, we may be able to obtain

34

The usual way of investigating the long-run relationship between Y and

34

The usual way of investigating the long-run relationship between Y and

35

One then evaluates the effect of a change in equilibrium on

35

One then evaluates the effect of a change in equilibrium on

36

In the model with two lags shown, (β2 + β3 +

36

In the model with two lags shown, (β2 + β3 +

37

We can calculate the long-run effect from the point estimates of

37

We can calculate the long-run effect from the point estimates of

38

The table presents an example of this. It gives the sum

38

The table presents an example of this. It gives the sum

39

If we are estimating long-run effects, we need standard errors as

39

If we are estimating long-run effects, we need standard errors as

40

The point estimate of the coefficient of Xt will be the

40

The point estimate of the coefficient of Xt will be the

41

Since Xt may well not be highly correlated with (Xt –

41

Since Xt may well not be highly correlated with (Xt –

============================================================

Dependent Variable: LGHOUS

Method: Least Squares

Sample(adjusted): 1961 2003

Included observations:

============================================================

Dependent Variable: LGHOUS

Method: Least Squares

Sample(adjusted): 1961 2003

Included observations:

43

As expected, the point estimates of the coefficients of LGDPI and

43

As expected, the point estimates of the coefficients of LGDPI and

44

Also as expected, the standard errors, 0.01 and 0.03, are much

44

Also as expected, the standard errors, 0.01 and 0.03, are much

Теория систем. Вводная лекция

Теория систем. Вводная лекция Решение уравнений и неравенств, содержащих параметр, с использованием параллельного переноса вдоль оси Oy

Решение уравнений и неравенств, содержащих параметр, с использованием параллельного переноса вдоль оси Oy Принцип Дирихле

Принцип Дирихле Целые числа. Рациональные числа

Целые числа. Рациональные числа Таблица основных неопределенных интегралов

Таблица основных неопределенных интегралов Доли и дроби

Доли и дроби Презентация по математике "Показательная функция, её свойства и график" - скачать

Презентация по математике "Показательная функция, её свойства и график" - скачать  Деление и степень числа. Тест

Деление и степень числа. Тест Доли числа

Доли числа Случаи вычитания 14 -

Случаи вычитания 14 - Применение распределительного свойства умножения. 6 класс

Применение распределительного свойства умножения. 6 класс Решение задач ЕГЭ по матеиатике

Решение задач ЕГЭ по матеиатике Подготовка к контрольной работе по теме «Системы линейных уравнений»

Подготовка к контрольной работе по теме «Системы линейных уравнений» Алгебраическая дробь. Сокращение дробей

Алгебраическая дробь. Сокращение дробей Треугольники

Треугольники Скалярное произведение векторов и его свойства

Скалярное произведение векторов и его свойства Презентация . На тему: «Золотое сечение и применение золотого сечения в жизни. Автор работы: Полянских Александр ученик 10 «б» клас

Презентация . На тему: «Золотое сечение и применение золотого сечения в жизни. Автор работы: Полянских Александр ученик 10 «б» клас Признаки подобия треугольников

Признаки подобия треугольников Основные теоремы о пределах. Способы вычисления пределов функций. (Семинар 5)

Основные теоремы о пределах. Способы вычисления пределов функций. (Семинар 5) Формулы сокращенного умнажения

Формулы сокращенного умнажения Решение уравнений Математика, 5 класс

Решение уравнений Математика, 5 класс Наименьшее общее кратное (НОК);

Наименьшее общее кратное (НОК); Проверка непараметрических статистических гипотез

Проверка непараметрических статистических гипотез Презентация по математике "Нормальное распределение: свойства и следствия из них" -

Презентация по математике "Нормальное распределение: свойства и следствия из них" -  Функция у = sin x , её свойства и график

Функция у = sin x , её свойства и график Решение задач на площадь треугольника

Решение задач на площадь треугольника Обыкновенная дробь. 5 класс

Обыкновенная дробь. 5 класс Пропорциональные отрезки в прямоугольном треугольнике (8 класс)

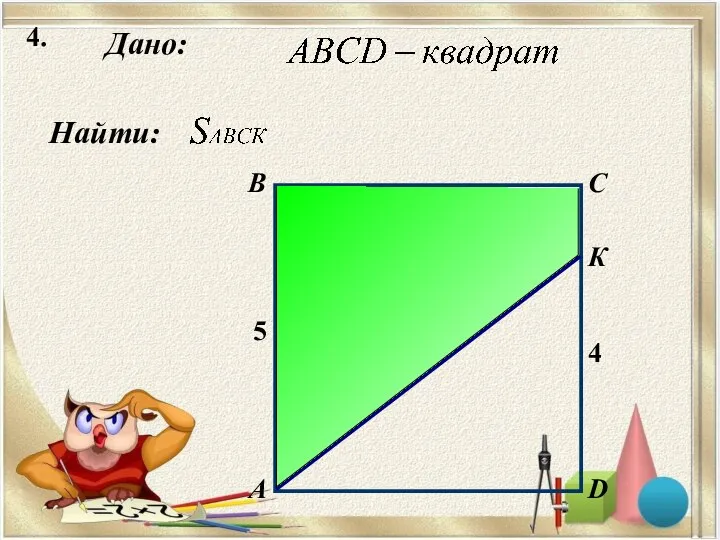

Пропорциональные отрезки в прямоугольном треугольнике (8 класс)