- LNG Market

Содержание

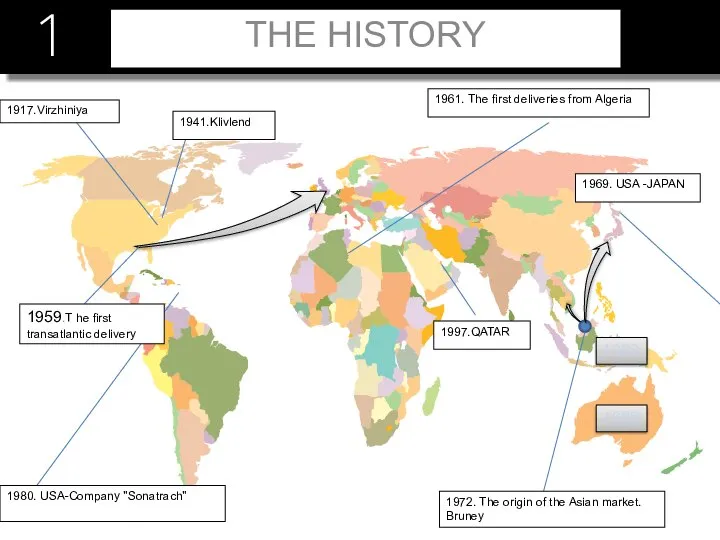

- 2. 1 1989 1983 1941.Klivlend 1997.QATAR 1961. The first deliveries from Algeria 1917.Virzhiniya 1959.T he first transatlantic

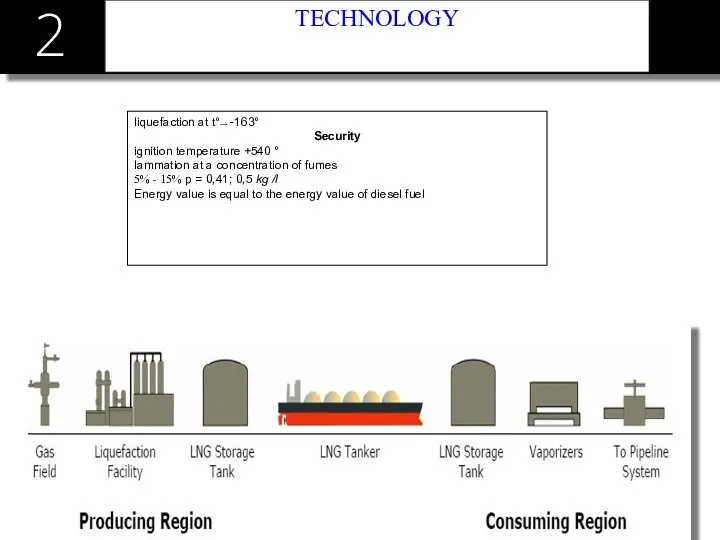

- 3. 2 TECHNOLOGY

- 4. 2 TECHNOLOGY liquefaction at t°→ -163° Security ignition temperature +540 ° lammation at a concentration of

- 5. Сжижение 2 liquefaction

- 6. Терминалы 2 TERMINALS

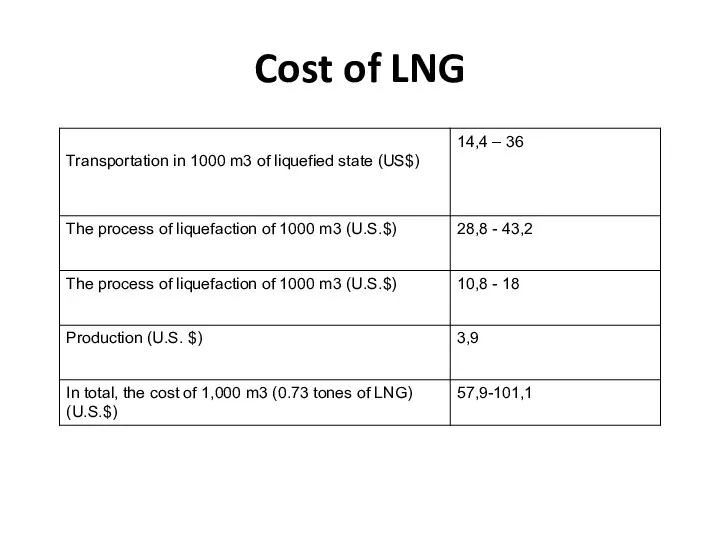

- 7. Cost of LNG

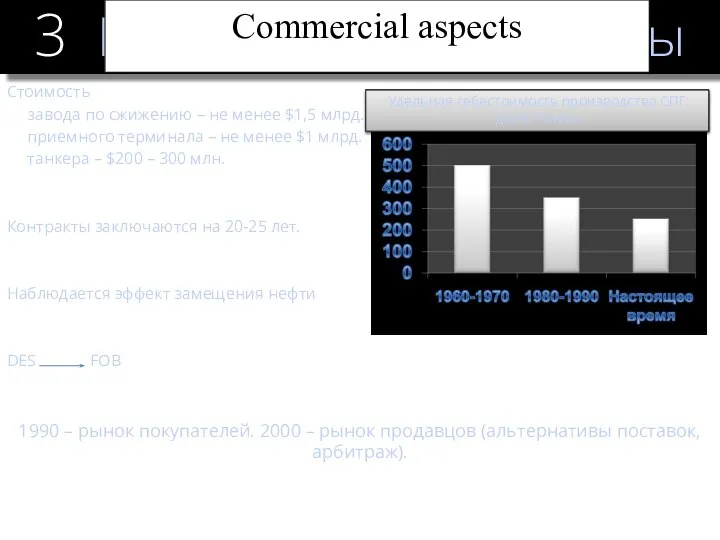

- 8. Стоимость завода по сжижению – не менее $1,5 млрд. приемного терминала – не менее $1 млрд.

- 9. Basic characteristics of markets major markets volumes exports imports trade flows Price

- 10. Основные рынки СПГ 2 4 THE MAJOR MARKETS OF LNG The North American market The European

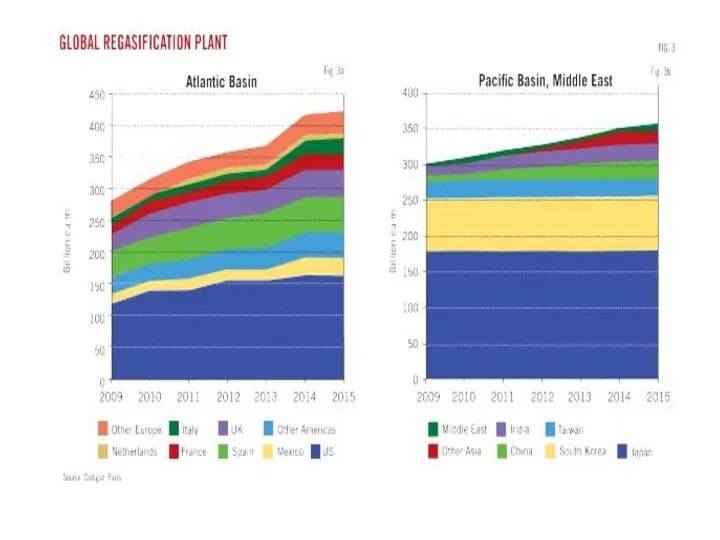

- 11. 5 Volumes of supplies, and participants 2005-2012

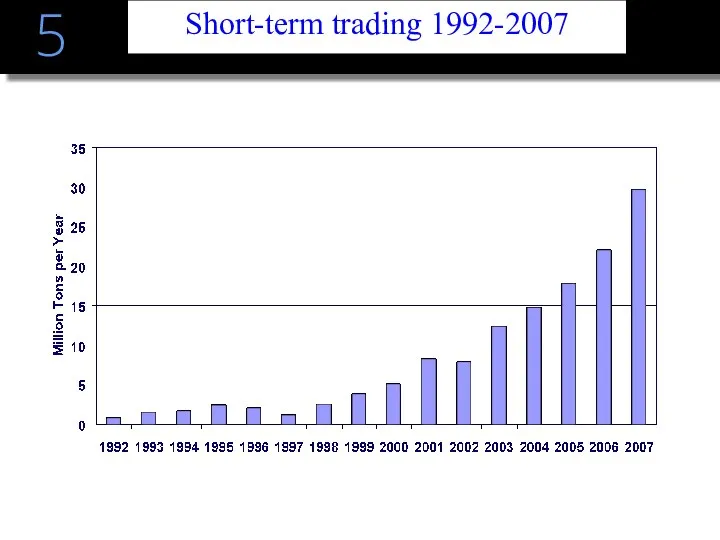

- 14. 5 Short-term trading 1992-2007

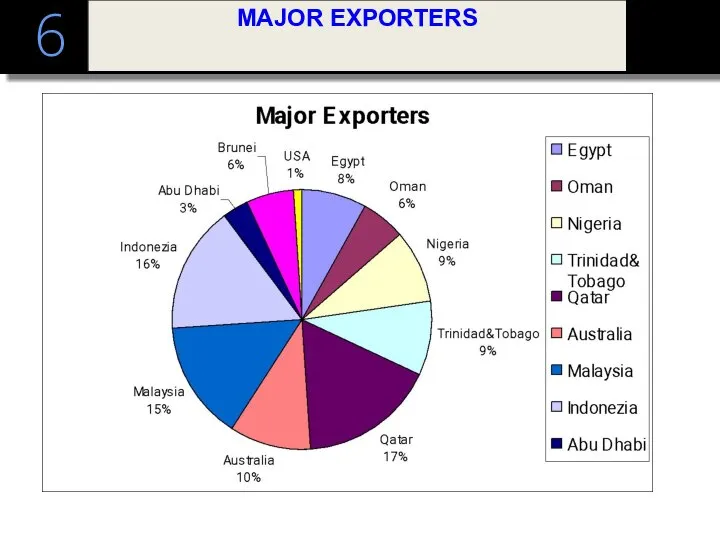

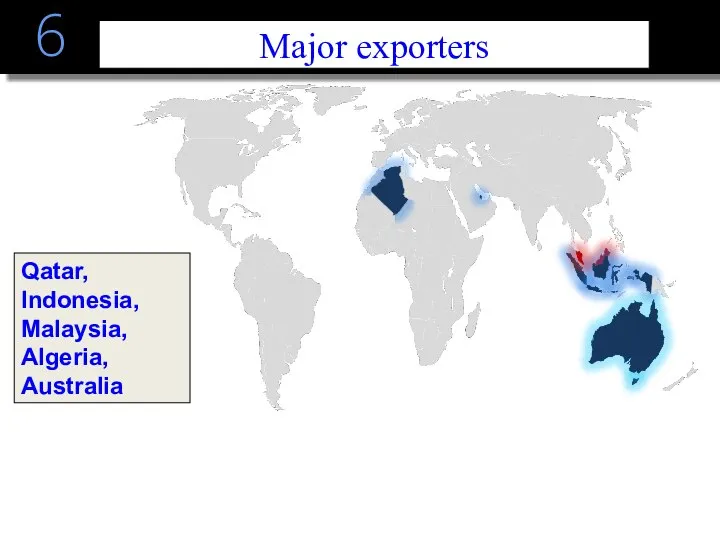

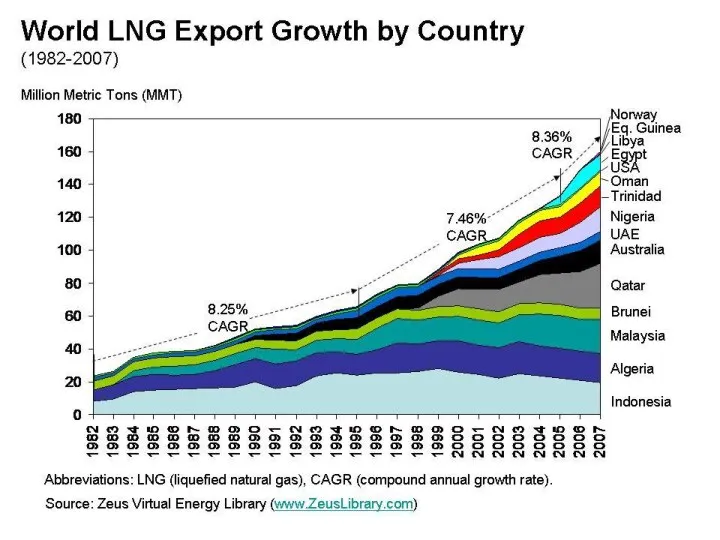

- 15. 6 MAJOR EXPORTERS

- 16. 6 Major exporters Qatar, Indonesia, Malaysia, Algeria, Australia

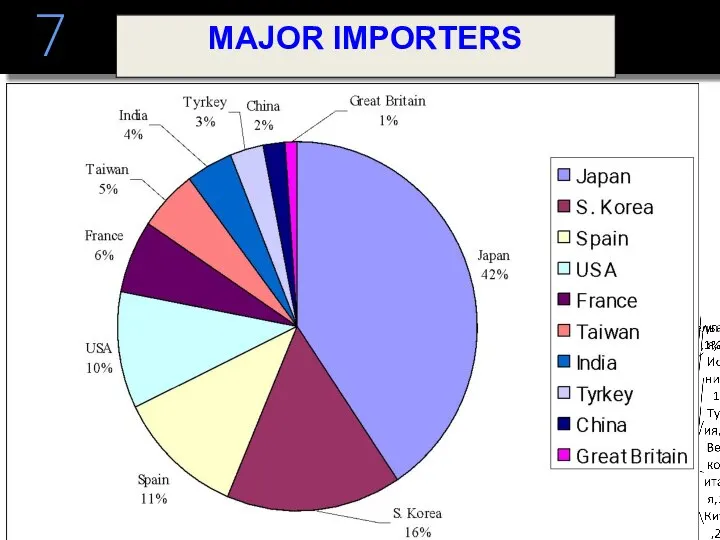

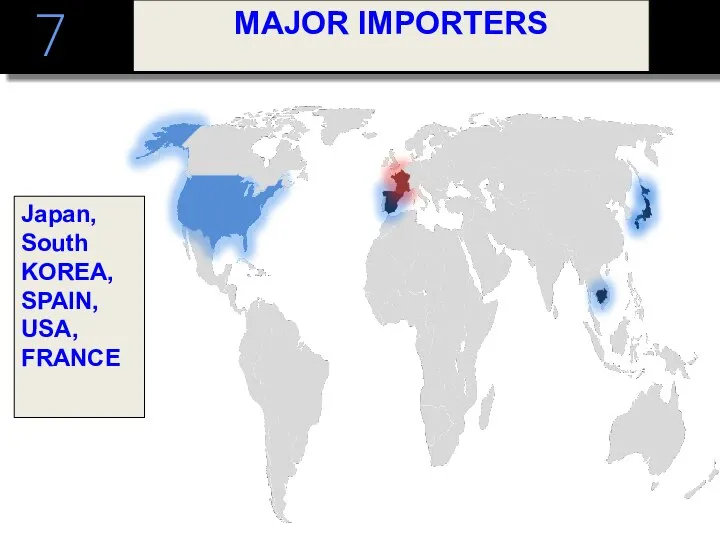

- 17. 7 MAJOR IMPORTERS

- 18. 7 MAJOR IMPORTERS Japan, South KOREA, SPAIN, USA, FRANCE

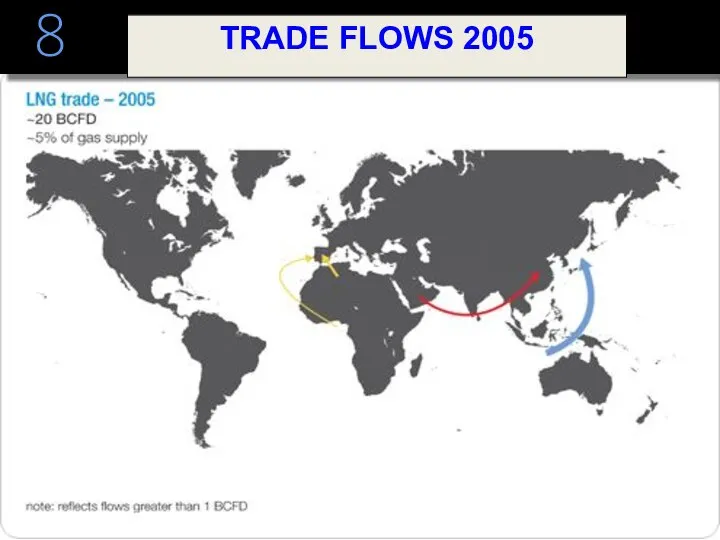

- 20. 8 TRADE FLOWS 2005

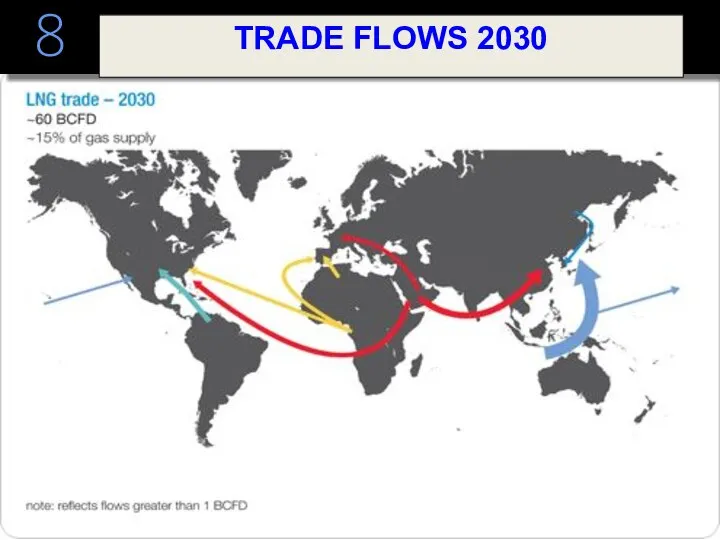

- 21. 8 TRADE FLOWS 2030

- 22. Enabling factors The tendency to reduce the cost of production, because improved liquefaction technology Rising consumption

- 23. constraints The high cost of LNG compared to coal and oil Attractiveness of the traditional gas

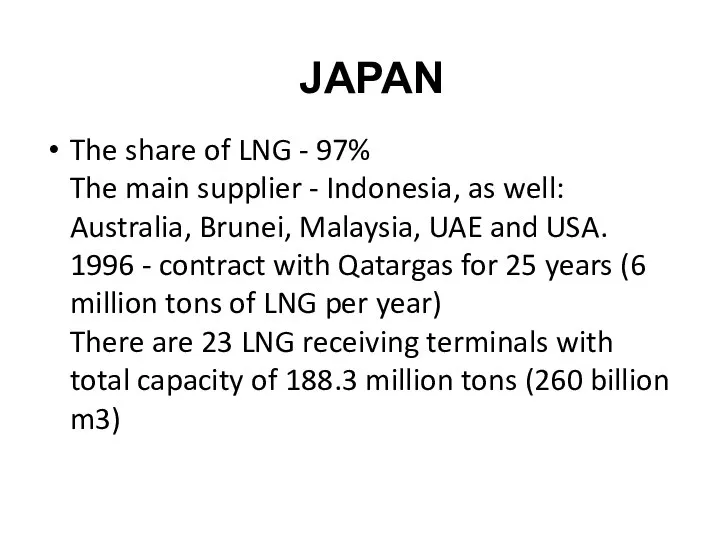

- 24. The share of LNG - 97% The main supplier - Indonesia, as well: Australia, Brunei, Malaysia,

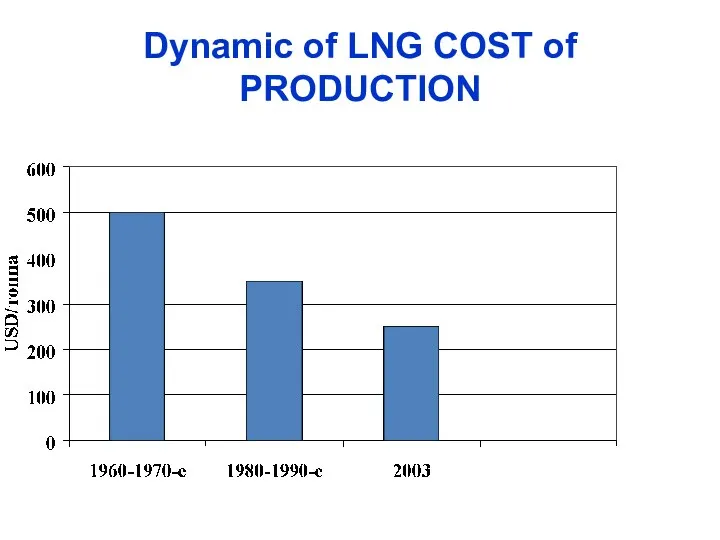

- 25. Dynamic of LNG COST of PRODUCTION

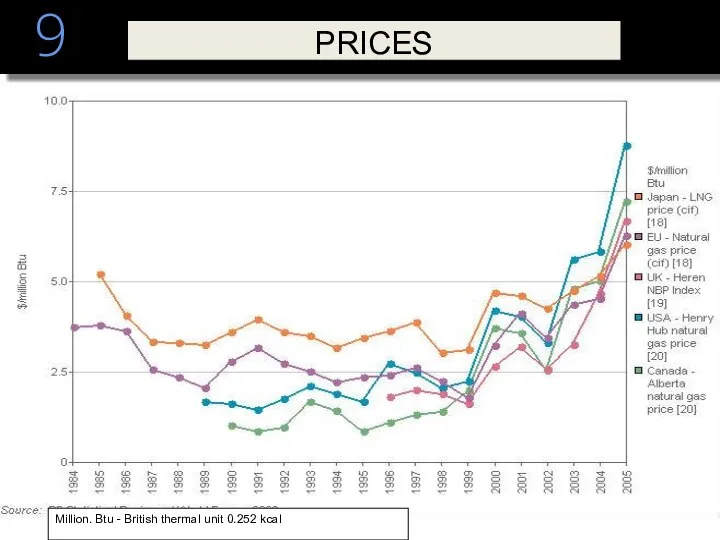

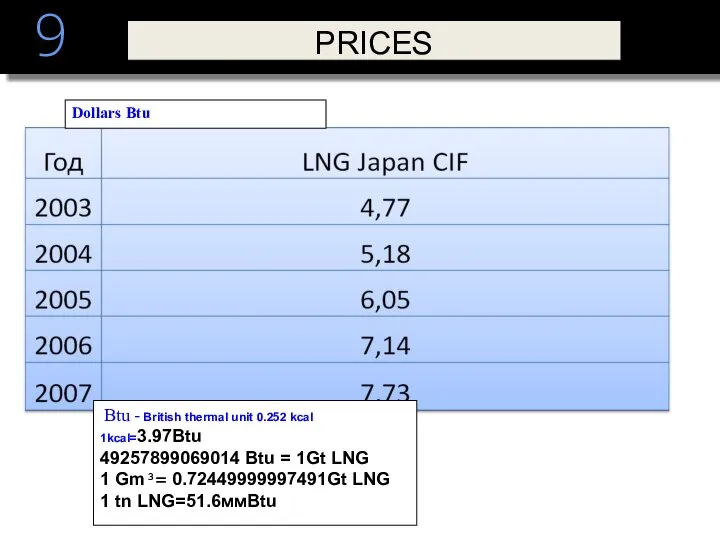

- 26. 9 PRICES Million. Btu - British thermal unit 0.252 kcal

- 27. 9 Btu - British thermal unit 0.252 kcal 1kcal=3.97Btu 49257899069014 Btu = 1Gt LNG 1 Gm³=

- 29. Скачать презентацию

1

1989

1983

1941.Klivlend

1997.QATAR

1961. The first deliveries from Algeria

1917.Virzhiniya

1959.T he first transatlantic delivery

1969.

1

1989

1983

1941.Klivlend

1997.QATAR

1961. The first deliveries from Algeria

1917.Virzhiniya

1959.T he first transatlantic delivery

1969.

2

TECHNOLOGY

2

TECHNOLOGY

2

TECHNOLOGY

liquefaction at t°→ -163°

Security

ignition temperature +540 °

lammation at a concentration of

2

TECHNOLOGY

liquefaction at t°→ -163°

Security

ignition temperature +540 °

lammation at a concentration of

Сжижение

2

liquefaction

Сжижение

2

liquefaction

Терминалы

2

TERMINALS

Терминалы

2

TERMINALS

Cost of LNG

Cost of LNG

Стоимость

завода по сжижению – не менее $1,5 млрд.

приемного

Стоимость

завода по сжижению – не менее $1,5 млрд.

приемного

Basic characteristics of markets

major markets

volumes

exports

imports

trade flows

Price

Basic characteristics of markets

major markets

volumes

exports

imports

trade flows

Price

Основные рынки СПГ

2

4

THE MAJOR MARKETS OF LNG

The North American market

The European

Основные рынки СПГ

2

4

THE MAJOR MARKETS OF LNG

The North American market The European

5

Volumes of supplies, and participants 2005-2012

5

Volumes of supplies, and participants 2005-2012

5

Short-term trading 1992-2007

5

Short-term trading 1992-2007

6

MAJOR EXPORTERS

6

MAJOR EXPORTERS

6

Major exporters

Qatar, Indonesia, Malaysia, Algeria, Australia

6

Major exporters

Qatar, Indonesia, Malaysia, Algeria, Australia

7

MAJOR IMPORTERS

7

MAJOR IMPORTERS

7

MAJOR IMPORTERS

Japan, South KOREA, SPAIN, USA, FRANCE

7

MAJOR IMPORTERS

Japan, South KOREA, SPAIN, USA, FRANCE

8

TRADE FLOWS 2005

8

TRADE FLOWS 2005

8

TRADE FLOWS 2030

8

TRADE FLOWS 2030

Enabling factors

The tendency to reduce the cost of production, because

Enabling factors

The tendency to reduce the cost of production, because

constraints

The high cost of LNG compared to coal and oil

Attractiveness of

constraints

The high cost of LNG compared to coal and oil

Attractiveness of

The share of LNG - 97%

The main supplier - Indonesia, as

The share of LNG - 97% The main supplier - Indonesia, as

Dynamic of LNG COST of PRODUCTION

Dynamic of LNG COST of PRODUCTION

9

PRICES

Million. Btu - British thermal unit 0.252 kcal

9

PRICES

Million. Btu - British thermal unit 0.252 kcal

9

Btu - British thermal unit 0.252 kcal 1kcal=3.97Btu

49257899069014 Btu =

9

Btu - British thermal unit 0.252 kcal 1kcal=3.97Btu

49257899069014 Btu =

The particularity of cosplayers identity with different motivation

The particularity of cosplayers identity with different motivation Презентация на тему "Как научить детей сотрудничать?" - скачать презентации по Педагогике

Презентация на тему "Как научить детей сотрудничать?" - скачать презентации по Педагогике Обеспечение безопасной эксплуатации жилых зданий Фрунзенского района Санкт-Петербурга

Обеспечение безопасной эксплуатации жилых зданий Фрунзенского района Санкт-Петербурга Гражданско-правовая ответственность медицинских работников

Гражданско-правовая ответственность медицинских работников Презентация на тему "Социальный комикс" - скачать презентации по Педагогике

Презентация на тему "Социальный комикс" - скачать презентации по Педагогике Аттестационная работа. Традиционная культура кубанских казаков

Аттестационная работа. Традиционная культура кубанских казаков 4_5877587462389236442

4_5877587462389236442 Федеральное собрание

Федеральное собрание  Организация питания в походе

Организация питания в походе Рабочие чертежи (с актуализированными изменениями 2015 года)

Рабочие чертежи (с актуализированными изменениями 2015 года) Джорджо Моранди

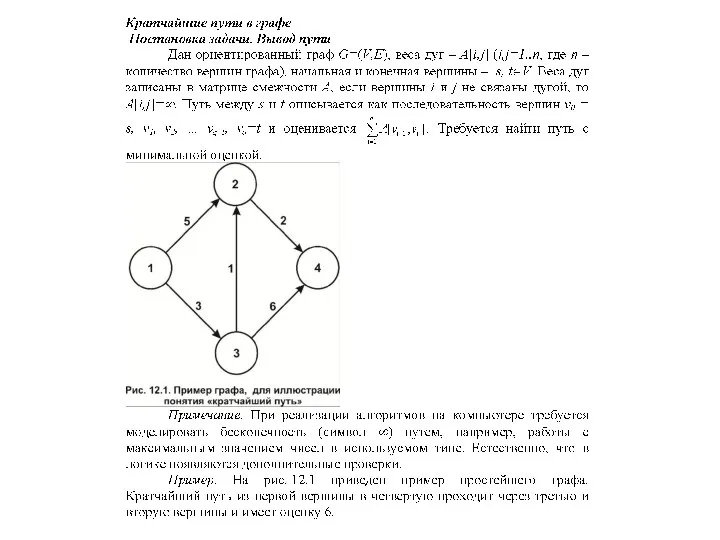

Джорджо Моранди  Кратчайшие пути

Кратчайшие пути Функциональная организация головного мозга

Функциональная организация головного мозга Самураи

Самураи Современные подходы к целеполаганию

Современные подходы к целеполаганию Особенности современного этапа развития мирового хозяйства Выполнил: студент 1-го курса очной формы обучения факультета тамо

Особенности современного этапа развития мирового хозяйства Выполнил: студент 1-го курса очной формы обучения факультета тамо Проект-РСО

Проект-РСО Технология сборки и сварки корпуса и днища резервуара РВС 2000 куб.м

Технология сборки и сварки корпуса и днища резервуара РВС 2000 куб.м Опыт использования бизнес-моделей в процессе обучения предпринимательству в магистратуре Екатерина Бузулукова к.э.н., ст.преп

Опыт использования бизнес-моделей в процессе обучения предпринимательству в магистратуре Екатерина Бузулукова к.э.н., ст.преп Гостиница “Метрополь”

Гостиница “Метрополь”  Задача Диофанта

Задача Диофанта Matka Boska Pajęczańska

Matka Boska Pajęczańska Царство Животные

Царство Животные  Вычисление линейной скорости и ускорения

Вычисление линейной скорости и ускорения РЕЧЕВОЕ ПОВЕДЕНИЕ СПОРЯЩИХ

РЕЧЕВОЕ ПОВЕДЕНИЕ СПОРЯЩИХ  ПСИХОЛОГИЧЕСКОЕ ОБЕСПЕЧЕНИЕ ПРОФЕССИОНАЛЬНОГО ЗДОРОВЬЯ ПЕДАГОГОВ САНКТ-ПЕТЕРБУРГ 2010

ПСИХОЛОГИЧЕСКОЕ ОБЕСПЕЧЕНИЕ ПРОФЕССИОНАЛЬНОГО ЗДОРОВЬЯ ПЕДАГОГОВ САНКТ-ПЕТЕРБУРГ 2010 С масленицей

С масленицей Шувалова Н. С., заместитель директора по УВР МУ СОШ № 66 г. Иваново

Шувалова Н. С., заместитель директора по УВР МУ СОШ № 66 г. Иваново