- Depressions and Slumps

Содержание

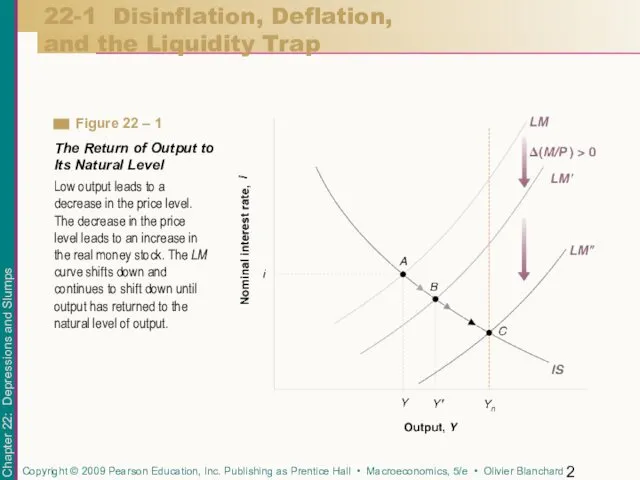

- 2. 22-1 Disinflation, Deflation, and the Liquidity Trap Low output leads to a decrease in the price

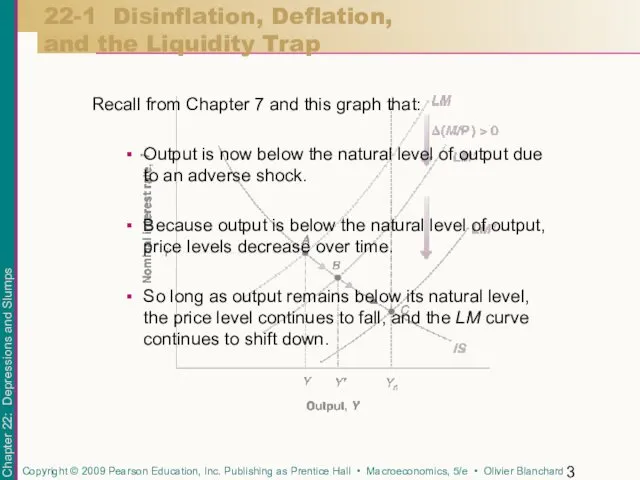

- 3. Recall from Chapter 7 and this graph that: Output is now below the natural level of

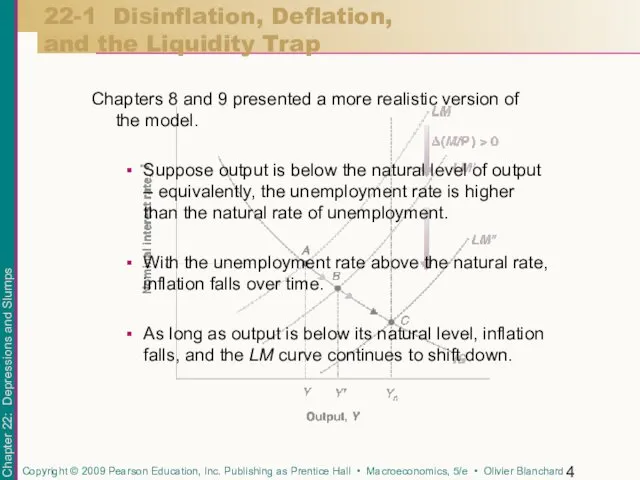

- 4. Chapters 8 and 9 presented a more realistic version of the model. Suppose output is below

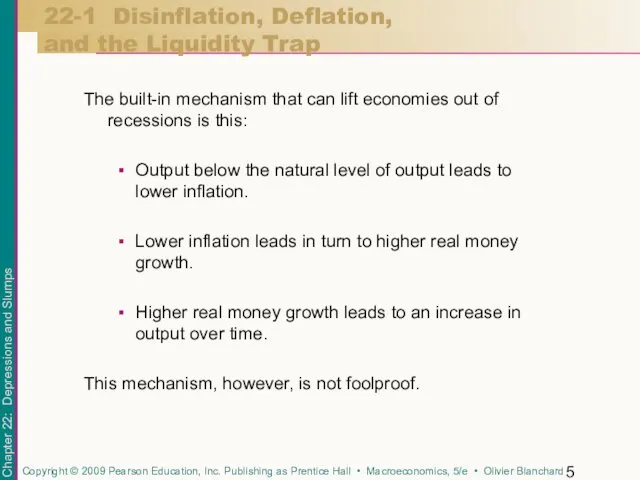

- 5. The built-in mechanism that can lift economies out of recessions is this: Output below the natural

- 6. Recall from Chapter 14 that: What matters for spending decisions, and thus what enters the IS

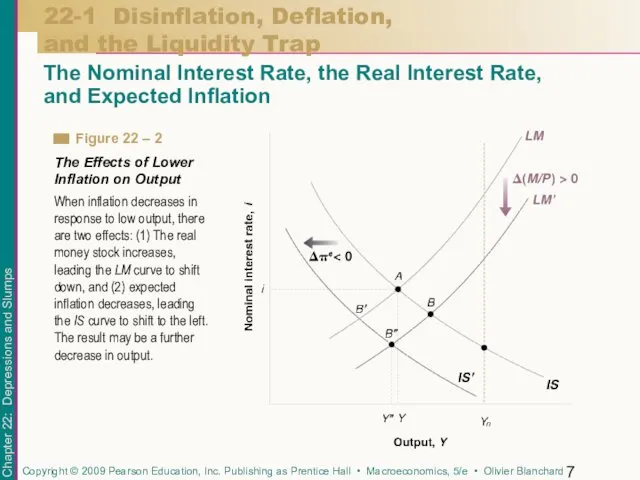

- 7. 22-1 Disinflation, Deflation, and the Liquidity Trap The Nominal Interest Rate, the Real Interest Rate, and

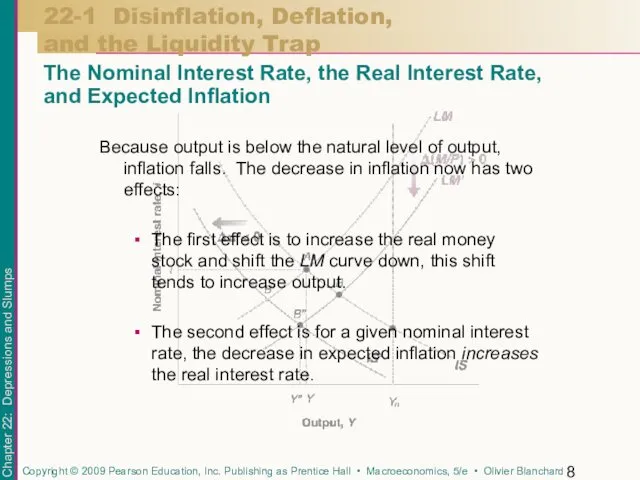

- 8. Because output is below the natural level of output, inflation falls. The decrease in inflation now

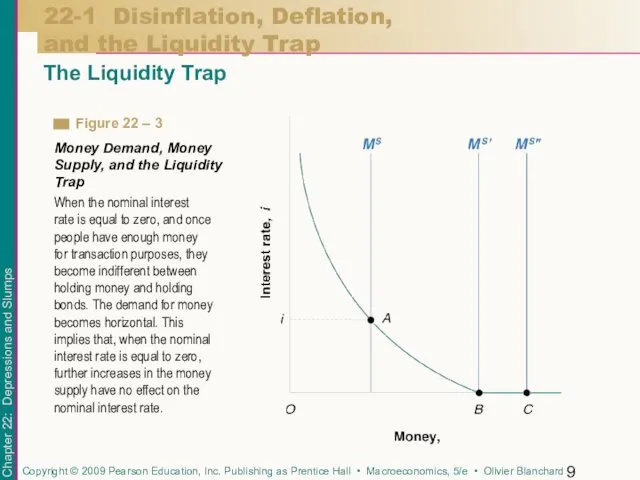

- 9. 22-1 Disinflation, Deflation, and the Liquidity Trap The Liquidity Trap When the nominal interest rate is

- 10. The demand for money is as shown in Figure 22-3. As the nominal interest rate decreases,

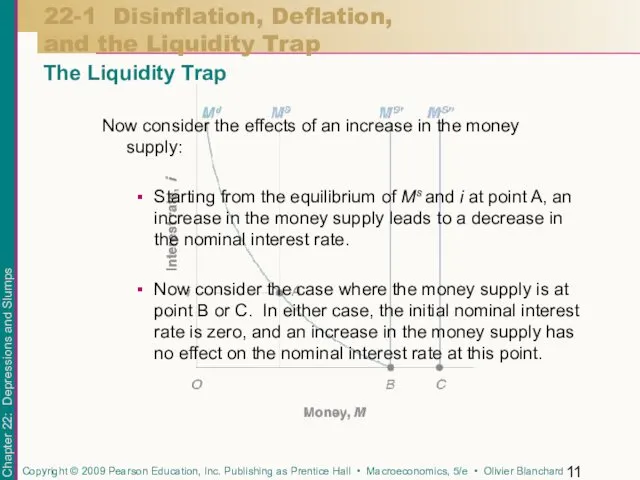

- 11. Now consider the effects of an increase in the money supply: Starting from the equilibrium of

- 12. The liquidity trap describes a situation in which expansionary monetary policy becomes powerless. The increase in

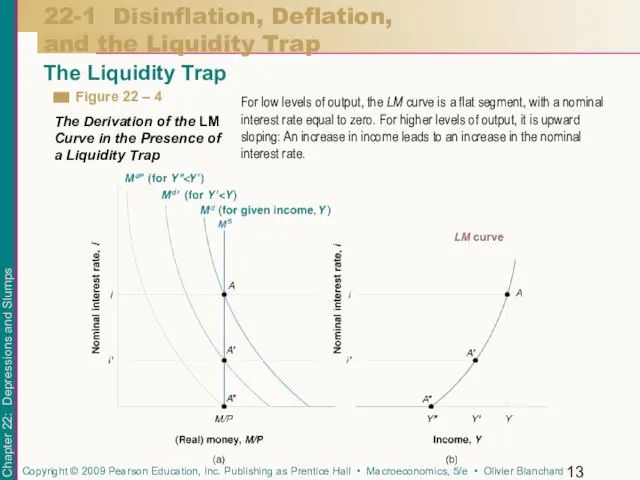

- 13. 22-1 Disinflation, Deflation, and the Liquidity Trap The Liquidity Trap For low levels of output, the

- 14. 22-1 Disinflation, Deflation, and the Liquidity Trap The Liquidity Trap To derive the LM curve, Figure

- 15. 22-1 Disinflation, Deflation, and the Liquidity Trap The Liquidity Trap The equilibrium is given by point

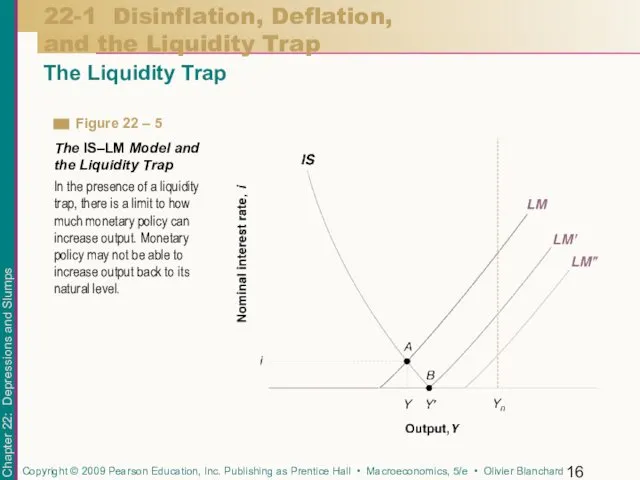

- 16. 22-1 Disinflation, Deflation, and the Liquidity Trap The Liquidity Trap In the presence of a liquidity

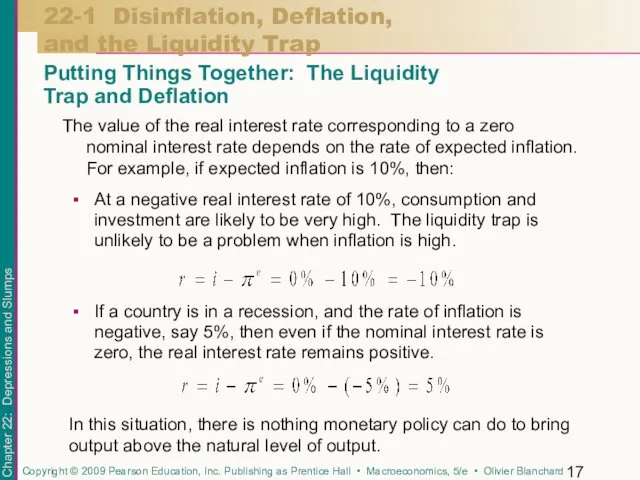

- 17. At a negative real interest rate of 10%, consumption and investment are likely to be very

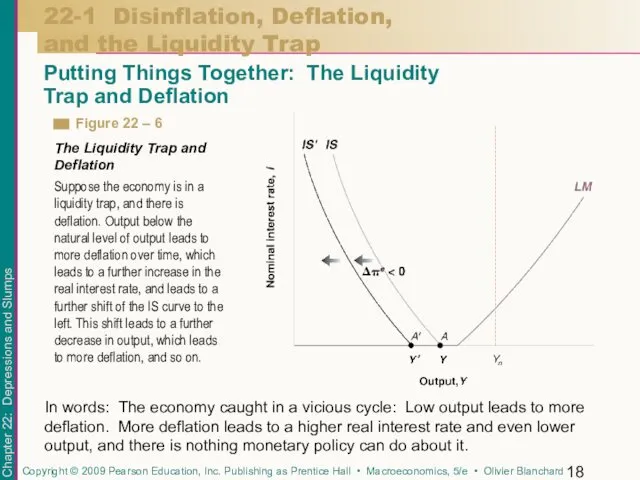

- 18. 22-1 Disinflation, Deflation, and the Liquidity Trap Putting Things Together: The Liquidity Trap and Deflation In

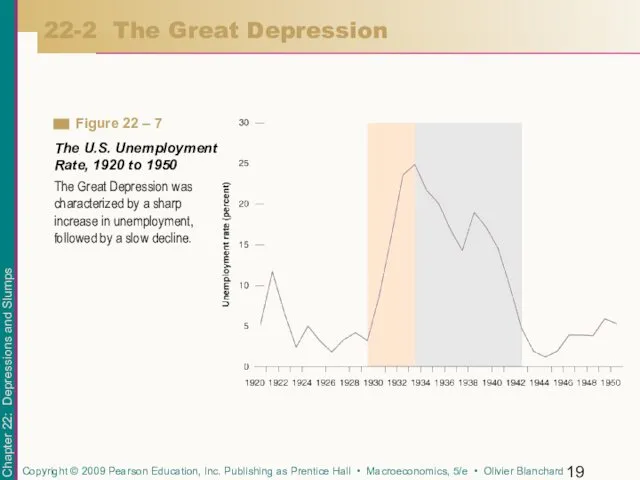

- 19. 22-2 The Great Depression The Great Depression was characterized by a sharp increase in unemployment, followed

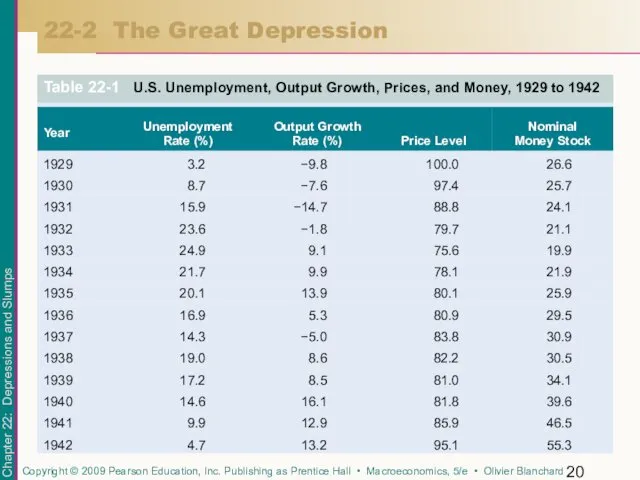

- 20. 22-2 The Great Depression

- 21. Focusing only on unemployment and output for the moment, two facts emerge from the table: How

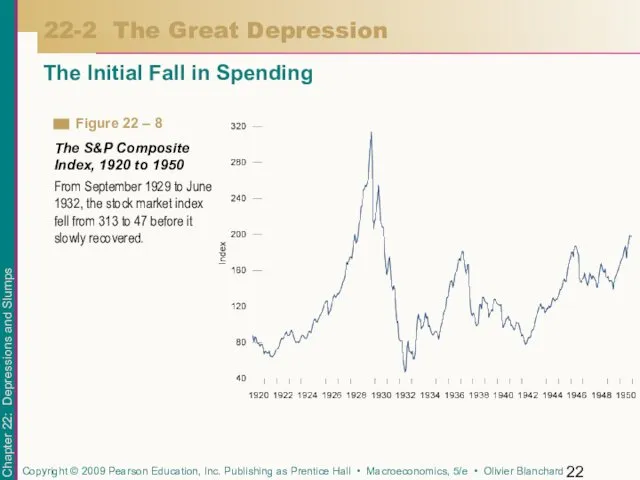

- 22. The Initial Fall in Spending 22-2 The Great Depression From September 1929 to June 1932, the

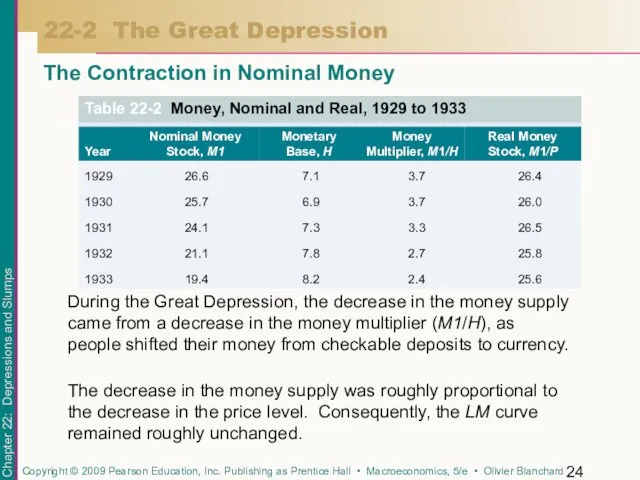

- 23. The Contraction in Nominal Money 22-2 The Great Depression The impact of the stock market crash

- 24. The Contraction in Nominal Money 22-2 The Great Depression During the Great Depression, the decrease in

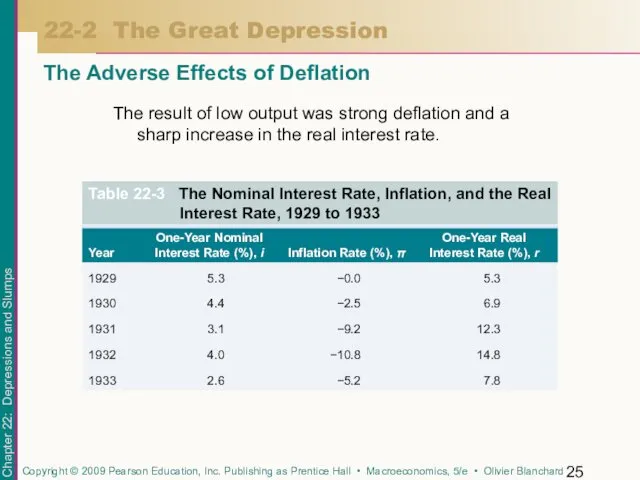

- 25. The result of low output was strong deflation and a sharp increase in the real interest

- 26. Monetary policy played an important role in the recovery. From 1933 to 1941, the nominal money

- 27. The puzzle is why deflation ended in 1933. One proximate cause may be the set of

- 28. The robust growth that Japan had experienced since the end of World War II came to

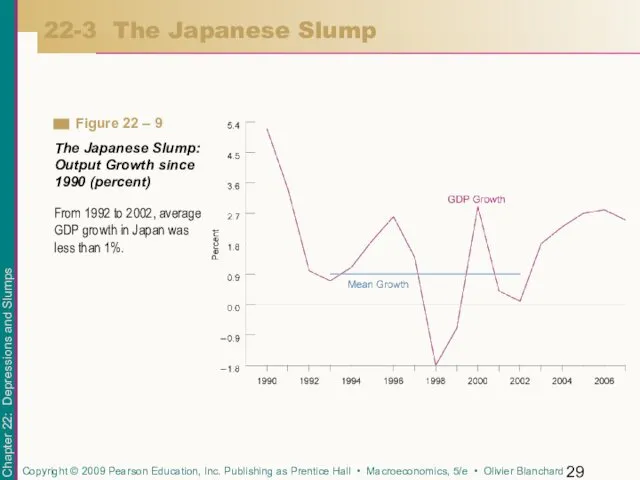

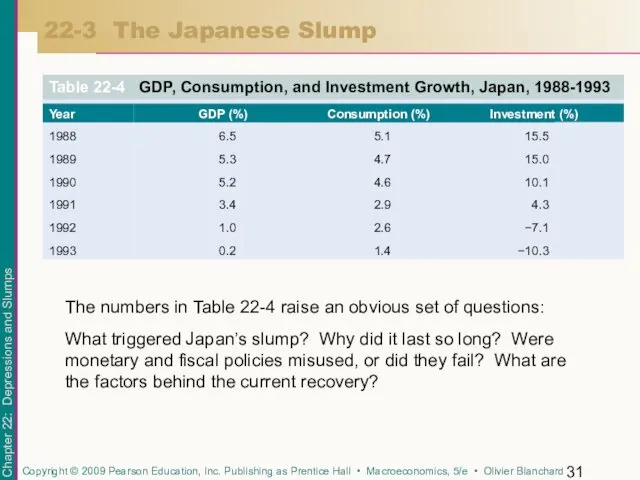

- 29. 22-3 The Japanese Slump From 1992 to 2002, average GDP growth in Japan was less than

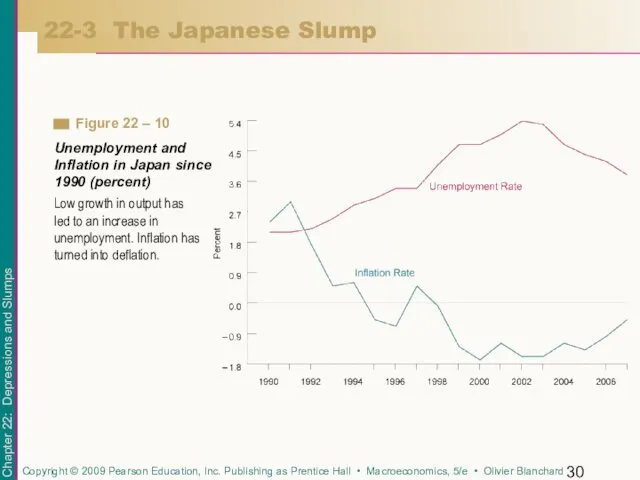

- 30. 22-3 The Japanese Slump Low growth in output has led to an increase in unemployment. Inflation

- 31. 22-3 The Japanese Slump The numbers in Table 22-4 raise an obvious set of questions: What

- 32. There are two reasons for the increase in a stock price: A change in the fundamental

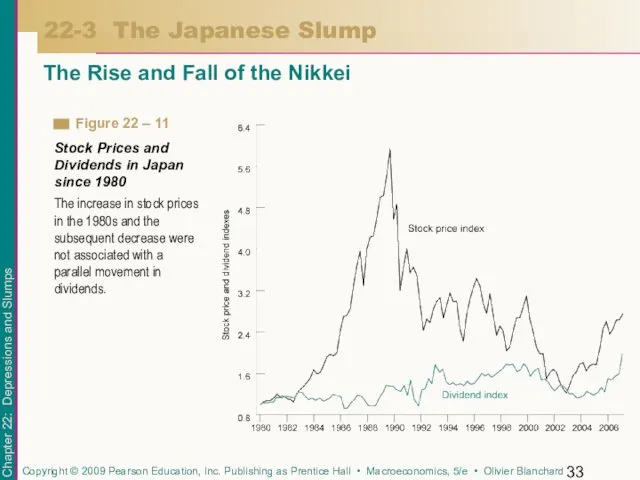

- 33. 22-3 The Japanese Slump The Rise and Fall of the Nikkei The increase in stock prices

- 34. The fact that dividends remained flat while stock prices increased strongly suggests that a large bubble

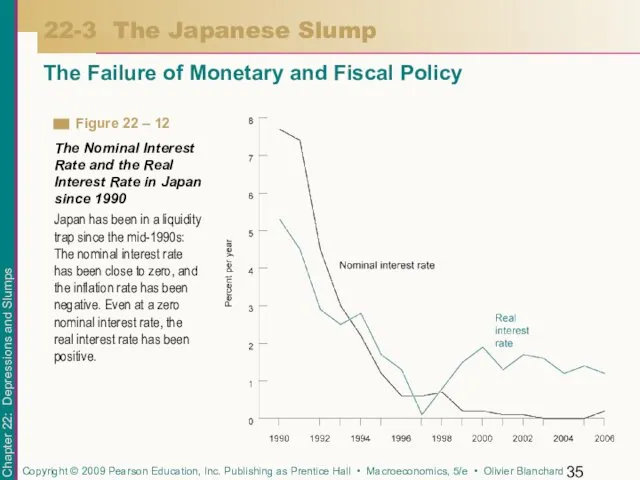

- 35. 22-3 The Japanese Slump The Failure of Monetary and Fiscal Policy Japan has been in a

- 36. Monetary policy was used, but it was used too late, and when it was used, if

- 37. Fiscal policy was used as well. Taxes decreased at the start of the slump, and there

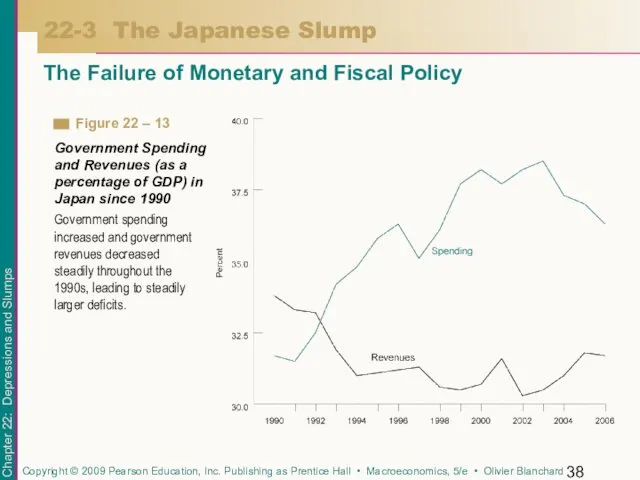

- 38. 22-3 The Japanese Slump The Failure of Monetary and Fiscal Policy Government spending increased and government

- 39. Output growth has been higher since 2003, and most economists cautiously predict that the recovery will

- 40. It is suggested that even if the nominal interest rate is already equal to zero and

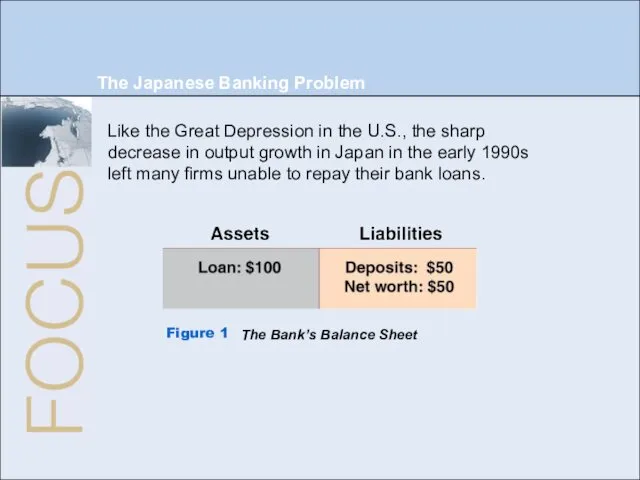

- 41. The Japanese Banking Problem Like the Great Depression in the U.S., the sharp decrease in output

- 43. Скачать презентацию

22-1 Disinflation, Deflation,

and the Liquidity Trap

Low output leads to a decrease

22-1 Disinflation, Deflation,

and the Liquidity Trap

Low output leads to a decrease

Recall from Chapter 7 and this graph that:

Output is now below

Recall from Chapter 7 and this graph that:

Output is now below

Chapters 8 and 9 presented a more realistic version of the

Chapters 8 and 9 presented a more realistic version of the

The built-in mechanism that can lift economies out of recessions is

The built-in mechanism that can lift economies out of recessions is

Recall from Chapter 14 that:

What matters for spending decisions, and thus

Recall from Chapter 14 that:

What matters for spending decisions, and thus

22-1 Disinflation, Deflation,

and the Liquidity Trap

The Nominal Interest Rate, the Real

22-1 Disinflation, Deflation,

and the Liquidity Trap

The Nominal Interest Rate, the Real

Because output is below the natural level of output, inflation falls.

Because output is below the natural level of output, inflation falls.

22-1 Disinflation, Deflation,

and the Liquidity Trap

The Liquidity Trap

When the nominal interest

22-1 Disinflation, Deflation,

and the Liquidity Trap

The Liquidity Trap

When the nominal interest

The demand for money is as shown in Figure 22-3.

As the

The demand for money is as shown in Figure 22-3.

As the

Now consider the effects of an increase in the money supply:

Starting

Now consider the effects of an increase in the money supply:

Starting

The liquidity trap describes a situation in which expansionary monetary policy

The liquidity trap describes a situation in which expansionary monetary policy

22-1 Disinflation, Deflation,

and the Liquidity Trap

The Liquidity Trap

For low levels of

22-1 Disinflation, Deflation,

and the Liquidity Trap

The Liquidity Trap

For low levels of

22-1 Disinflation, Deflation,

and the Liquidity Trap

The Liquidity Trap

To derive the LM

22-1 Disinflation, Deflation,

and the Liquidity Trap

The Liquidity Trap

To derive the LM

22-1 Disinflation, Deflation,

and the Liquidity Trap

The Liquidity Trap

The equilibrium is given

22-1 Disinflation, Deflation,

and the Liquidity Trap

The Liquidity Trap

The equilibrium is given

22-1 Disinflation, Deflation,

and the Liquidity Trap

The Liquidity Trap

In the presence of

22-1 Disinflation, Deflation,

and the Liquidity Trap

The Liquidity Trap

In the presence of

At a negative real interest rate of 10%, consumption and investment

At a negative real interest rate of 10%, consumption and investment

22-1 Disinflation, Deflation,

and the Liquidity Trap

Putting Things Together: The Liquidity

Trap

22-1 Disinflation, Deflation,

and the Liquidity Trap

Putting Things Together: The Liquidity Trap

22-2 The Great Depression

The Great Depression was characterized by a sharp

22-2 The Great Depression

The Great Depression was characterized by a sharp

22-2 The Great Depression

22-2 The Great Depression

Focusing only on unemployment and output for the moment, two facts

Focusing only on unemployment and output for the moment, two facts

The Initial Fall in Spending

22-2 The Great Depression

From September 1929 to

The Initial Fall in Spending

22-2 The Great Depression

From September 1929 to

The Contraction in Nominal Money

22-2 The Great Depression

The impact of the

The Contraction in Nominal Money

22-2 The Great Depression

The impact of the

The Contraction in Nominal Money

22-2 The Great Depression

During the Great Depression,

The Contraction in Nominal Money

22-2 The Great Depression

During the Great Depression,

The result of low output was strong deflation and a sharp

The result of low output was strong deflation and a sharp

Monetary policy played an important role in the recovery. From 1933

Monetary policy played an important role in the recovery. From 1933

The puzzle is why deflation ended in 1933.

One proximate cause may

The puzzle is why deflation ended in 1933.

One proximate cause may

The robust growth that Japan had experienced since the end of

The robust growth that Japan had experienced since the end of

22-3 The Japanese Slump

From 1992 to 2002, average GDP growth in

22-3 The Japanese Slump

From 1992 to 2002, average GDP growth in

22-3 The Japanese Slump

Low growth in output has led to an

22-3 The Japanese Slump

Low growth in output has led to an

22-3 The Japanese Slump

The numbers in Table 22-4 raise an obvious

22-3 The Japanese Slump

The numbers in Table 22-4 raise an obvious

There are two reasons for the increase in a stock price:

A

There are two reasons for the increase in a stock price:

A

22-3 The Japanese Slump

The Rise and Fall of the Nikkei

The increase

22-3 The Japanese Slump

The Rise and Fall of the Nikkei

The increase

The fact that dividends remained flat while stock prices increased strongly

The fact that dividends remained flat while stock prices increased strongly

22-3 The Japanese Slump

The Failure of Monetary and Fiscal Policy

Japan has

22-3 The Japanese Slump

The Failure of Monetary and Fiscal Policy

Japan has

Monetary policy was used, but it was used too late, and

Monetary policy was used, but it was used too late, and

Fiscal policy was used as well. Taxes decreased at the start

Fiscal policy was used as well. Taxes decreased at the start

22-3 The Japanese Slump

The Failure of Monetary and Fiscal Policy

Government spending

22-3 The Japanese Slump

The Failure of Monetary and Fiscal Policy

Government spending

Output growth has been higher since 2003, and most economists cautiously

Output growth has been higher since 2003, and most economists cautiously

It is suggested that even if the nominal interest rate is

It is suggested that even if the nominal interest rate is

The Japanese Banking Problem

Like the Great Depression in the U.S., the

The Japanese Banking Problem

Like the Great Depression in the U.S., the

Понятие предприятия

Понятие предприятия Статистические методы изучения взаимосвязи социально-экономических явлений. (Лекция 4)

Статистические методы изучения взаимосвязи социально-экономических явлений. (Лекция 4) Світове господарство та етапи його формування. 10 клас

Світове господарство та етапи його формування. 10 клас Экономическая теория. Введение в макроэкономику. Система национальных счетов. (Модуль 2.1)

Экономическая теория. Введение в макроэкономику. Система национальных счетов. (Модуль 2.1) Кризис как фактор жизнедеятельности социально-экономических систем

Кризис как фактор жизнедеятельности социально-экономических систем Структурная перестройка в экономике РФ

Структурная перестройка в экономике РФ Внешнеторговые показатели в международной торговле

Внешнеторговые показатели в международной торговле Асимметричность информации и отношения «принципал-агент»

Асимметричность информации и отношения «принципал-агент» Модель межотраслевого баланса

Модель межотраслевого баланса Особенности, динамика, перспективы внешнеэкономических связей Ростовской области

Особенности, динамика, перспективы внешнеэкономических связей Ростовской области Экспорт российской продукции АПК

Экспорт российской продукции АПК Экономический морской бой

Экономический морской бой Проблема занятости молодежи

Проблема занятости молодежи Проект экономика родного края (село Бабяково)

Проект экономика родного края (село Бабяково) Правила обращения за региональной социальной доплатой к пенсии, порядок ее установления, выплаты и пересмотра ее размера

Правила обращения за региональной социальной доплатой к пенсии, порядок ее установления, выплаты и пересмотра ее размера Теория отраслевых рынков

Теория отраслевых рынков Инвестиции и инвестиционная деятельность

Инвестиции и инвестиционная деятельность Программа по выходу из кризиса города Возрождения

Программа по выходу из кризиса города Возрождения Основные Средства

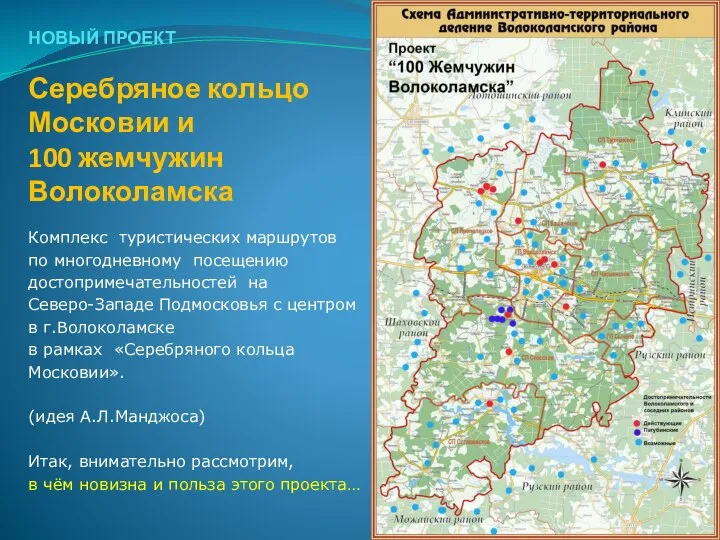

Основные Средства Комплекс туристических маршрутов по многодневному посещению достопримечательностей в рамках «Серебряного кольца Московии»

Комплекс туристических маршрутов по многодневному посещению достопримечательностей в рамках «Серебряного кольца Московии» Самые популярные профессии Ростова-на-Дону

Самые популярные профессии Ростова-на-Дону Учет оборотных активов. (Тема 5)

Учет оборотных активов. (Тема 5) Теория производства и предельной производительности факторов (первая часть)

Теория производства и предельной производительности факторов (первая часть) Экономическая теория

Экономическая теория Экономические системы А. Смита и Д. Рикардо

Экономические системы А. Смита и Д. Рикардо Практичне застосування GJR model в Азії

Практичне застосування GJR model в Азії Российский морской регистр судоходства

Российский морской регистр судоходства Социальная политика государства и управление социальным развитием организации. Россия и Сингапур

Социальная политика государства и управление социальным развитием организации. Россия и Сингапур