- Market structure of production resources

Содержание

- 2. Topics: 1. General characteristics of the market of production resources. 2. Labor market and wages. 3.

- 3. References: A practical guide to seminars on economic theory. – M.: Vlados, 2016 .– 272 p.

- 4. Resource Demand As long as the additional revenue from employing another worker exceeds the additional cost,

- 5. Resource Supply Resource owners will supply their resources to the highest-paying alternative, other things equal Since

- 6. Demand and Supply of Resources Firms demand resources so as to maximize profit and households supply

- 7. Exhibit 1: Resource Market for Carpenters W 0 E Hours of labor per period D S

- 8. Market Demand for Resources Why do firms employ resources? Resources are used to produce goods and

- 9. Market Demand for Resources The market demand for a particular resource is the sum of demands

- 10. Market Demand for Resources Consider first the producer’s greater willingness to hire resources as the resource

- 11. Market Demand for Resources A lower price for a resource also increases a producer’s ability to

- 12. Market Supply for Resources The market supply curve of a resource sums all the individual supply

- 13. Market Supply for Resources Resource suppliers are more willing because a higher resource price, other things

- 14. Market Supply for Resources Resource supply curves also slope upward because resource owners are able to

- 15. Temporary and Permanent Resource Price Differences Resource owners have a strong interest in selling their resources

- 16. Exhibit 2: Market for Carpenters in Alternative Uses $25 (a) Home building Sh D h 0

- 17. Temporary Differences in Resource Prices Resource prices sometimes differ temporarily across markets because adjustment takes time

- 18. Permanent Differences in Resource Prices Not all resource price differences cause a reallocation of resources For

- 19. Summary Temporary price differences spark the movement of resources away from lower-paid uses toward higher-paid uses

- 20. Opportunity Cost and Economic Rent Recall that opportunity cost is what that resources could earn in

- 21. Opportunity Cost and Economic Rent The division between these two categories depends on the resource owner’s

- 22. All Earnings are Economic Rent If the supply of a resource to a particular market is

- 23. Exhibit 3: Opportunity Cost and Economic Rent D o l l a r s p e

- 24. D o l l a r s p e r u n i t $10 0

- 25. $10 5 0 5,000 10,000 Hours of labor per week Opportunity costs Economic rent S D

- 26. Summary Note that specialized resources tend to earn a higher proportion of economic rent than do

- 27. Closer Look at Resource Demand In our discussion of a firm’s costs, we varied the amount

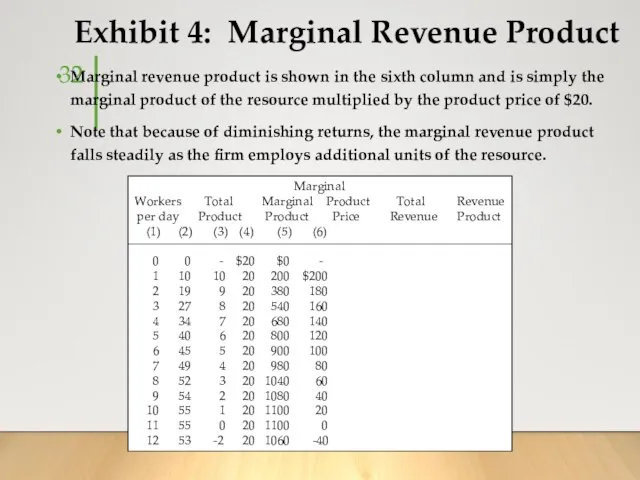

- 28. Exhibit 4: Marginal Revenue Product Possible employment levels of the variable resource listed in column (1).

- 29. Marginal Revenue Product The important question is what happens to the firm’s revenue when additional workers

- 30. Marginal Revenue Product A resource’s marginal revenue product depends on How much additional output the resource

- 31. Selling Output as a Price Taker The calculation of marginal revenue product is simplest when the

- 32. Exhibit 4: Marginal Revenue Product Marginal revenue product is shown in the sixth column and is

- 33. Selling Output as a Price Maker If the firm has some market power over the price

- 34. Exhibit 5: Marginal Revenue Product for a Price Maker The marginal revenue product of labor, which

- 35. Marginal Resource Cost Marginal resource cost is the additional cost to the firm of employing one

- 36. Exhibit 6: Market Equilibrium For a Resource and the Firm’s Employment Decision $200 Workers per day

- 37. Resource Employment For all resources employed, the firm should hire additional units up to the level

- 38. Summary Maximum profit (or minimum loss) occurs where the marginal revenue from output equals its marginal

- 39. Shifts in the Demand for Resources A resource’s marginal revenue product consists of two components The

- 40. Change in the Price of Other Resources The marginal product of any resource depends on the

- 41. Change in the Price of Other Resources Complements A decrease in the price of one resource

- 42. Changes in Technology Technological improvements can boost the productivity of some resources but can make others

- 43. Change in the Demand for the Final Product Because the demand is derived from the demand

- 44. More than One Resource As long as the marginal revenue product exceeds the marginal resource cost,

- 46. Скачать презентацию

Topics:

1. General characteristics of the market of production resources.

2. Labor market

Topics:

1. General characteristics of the market of production resources.

2. Labor market

References:

A practical guide to seminars on economic theory. – M.: Vlados,

References:

A practical guide to seminars on economic theory. – M.: Vlados,

Resource Demand

As long as the additional revenue from employing another worker

Resource Demand

As long as the additional revenue from employing another worker

Resource Supply

Resource owners will supply their resources to the highest-paying alternative,

Resource Supply

Resource owners will supply their resources to the highest-paying alternative,

Demand and Supply of Resources

Firms demand resources so as to maximize

Demand and Supply of Resources

Firms demand resources so as to maximize

Exhibit 1: Resource Market for Carpenters

W

0

E

Hours of labor

Exhibit 1: Resource Market for Carpenters

W

0

E

Hours of labor

Market Demand for Resources

Why do firms employ resources?

Resources are used to

Market Demand for Resources

Why do firms employ resources?

Resources are used to

Market Demand for Resources

The market demand for a particular resource is

Market Demand for Resources

The market demand for a particular resource is

Market Demand for Resources

Consider first the producer’s greater willingness to hire

Market Demand for Resources

Consider first the producer’s greater willingness to hire

Market Demand for Resources

A lower price for a resource also increases

Market Demand for Resources

A lower price for a resource also increases

Market Supply for Resources

The market supply curve of a resource sums

Market Supply for Resources

The market supply curve of a resource sums

Market Supply for Resources

Resource suppliers are more willing because a higher

Market Supply for Resources

Resource suppliers are more willing because a higher

Market Supply for Resources

Resource supply curves also slope upward because resource

Market Supply for Resources

Resource supply curves also slope upward because resource

Temporary and Permanent Resource Price Differences

Resource owners have a strong interest

Temporary and Permanent Resource Price Differences

Resource owners have a strong interest

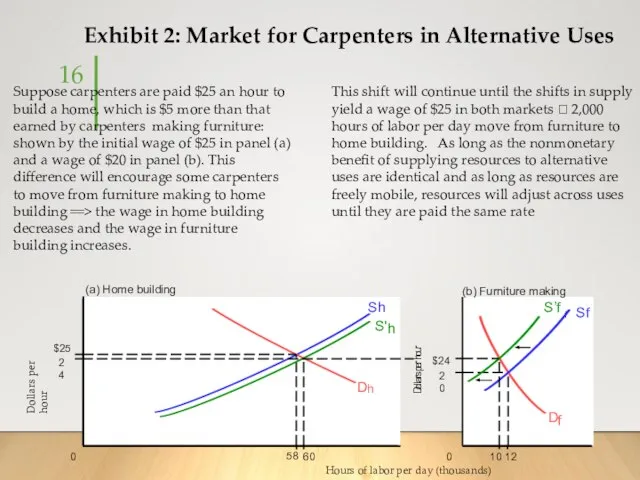

Exhibit 2: Market for Carpenters in Alternative Uses

$25

(a) Home building

Sh

D

h

0

Hours

Exhibit 2: Market for Carpenters in Alternative Uses

$25

(a) Home building

Sh

D

h

0

Hours

Temporary Differences in Resource Prices

Resource prices sometimes differ temporarily across markets

Temporary Differences in Resource Prices

Resource prices sometimes differ temporarily across markets

Permanent Differences in Resource Prices

Not all resource price differences cause a

Permanent Differences in Resource Prices

Not all resource price differences cause a

Summary

Temporary price differences spark the movement of resources away from lower-paid

Summary

Temporary price differences spark the movement of resources away from lower-paid

Opportunity Cost and Economic Rent

Recall that opportunity cost is what that

Opportunity Cost and Economic Rent

Recall that opportunity cost is what that

Opportunity Cost and Economic Rent

The division between these two categories depends

Opportunity Cost and Economic Rent

The division between these two categories depends

All Earnings are Economic Rent

If the supply of a resource to

All Earnings are Economic Rent

If the supply of a resource to

Exhibit 3: Opportunity Cost and Economic Rent

D

o

l

l

a

r

s

p

e

r

u

n

i

t

$1

0 10

Exhibit 3: Opportunity Cost and Economic Rent

D

o

l

l

a

r

s

p

e

r

u

n

i

t

$1

0 10

D

o

l

l

a

r

s

p

e

r

u

n

i

t

$10

0 1,000

S

D

Opportunity

costs

Hours of

labor per week

At the

D

o

l

l

a

r

s

p

e

r

u

n

i

t

$10

0 1,000

S

D

Opportunity

costs

Hours of

labor per week

At the

$10

5

0 5,000 10,000

Hours of labor

per week

Opportunity

costs

Economic

rent

S

D

D

o

l

l

a

r

s

p

e

r

$10

5

0 5,000 10,000

Hours of labor

per week

Opportunity

costs

Economic

rent

S

D

D

o

l

l

a

r

s

p

e

r

Summary

Note that specialized resources tend to earn a higher proportion of

Summary

Note that specialized resources tend to earn a higher proportion of

Closer Look at Resource Demand

In our discussion of a firm’s costs,

Closer Look at Resource Demand

In our discussion of a firm’s costs,

Exhibit 4: Marginal Revenue Product

Possible employment levels of the variable resource

Exhibit 4: Marginal Revenue Product

Possible employment levels of the variable resource

Marginal Revenue Product

The important question is what happens to the firm’s

Marginal Revenue Product

The important question is what happens to the firm’s

Marginal Revenue Product

A resource’s marginal revenue product depends on

How much additional

Marginal Revenue Product

A resource’s marginal revenue product depends on

How much additional

Selling Output as a Price Taker

The calculation of marginal revenue product

Selling Output as a Price Taker

The calculation of marginal revenue product

Exhibit 4: Marginal Revenue Product

Marginal revenue product is shown in the

Exhibit 4: Marginal Revenue Product

Marginal revenue product is shown in the

Selling Output as a Price Maker

If the firm has some market

Selling Output as a Price Maker

If the firm has some market

Exhibit 5: Marginal Revenue Product for a Price Maker

The marginal revenue

Exhibit 5: Marginal Revenue Product for a Price Maker

The marginal revenue

Marginal Resource Cost

Marginal resource cost is the additional cost to the

Marginal Resource Cost

Marginal resource cost is the additional cost to the

Exhibit 6: Market Equilibrium For a Resource

and the Firm’s Employment Decision

$200

Exhibit 6: Market Equilibrium For a Resource

and the Firm’s Employment Decision

$200

Resource Employment

For all resources employed, the firm should hire additional

Resource Employment

For all resources employed, the firm should hire additional

Summary

Maximum profit (or minimum loss) occurs where the marginal revenue from

Summary

Maximum profit (or minimum loss) occurs where the marginal revenue from

Shifts in the Demand for Resources

A resource’s marginal revenue product consists

Shifts in the Demand for Resources

A resource’s marginal revenue product consists

Change in the Price of Other Resources

The marginal product of any

Change in the Price of Other Resources

The marginal product of any

Change in the Price of Other Resources

Complements

A decrease in the price

Change in the Price of Other Resources

Complements

A decrease in the price

Changes in Technology

Technological improvements can boost the productivity of some resources

Changes in Technology

Technological improvements can boost the productivity of some resources

Change in the Demand for the Final Product

Because the demand is

Change in the Demand for the Final Product

Because the demand is

More than One Resource

As long as the marginal revenue product exceeds

More than One Resource

As long as the marginal revenue product exceeds

Презентация Категорический силлогизм

Презентация Категорический силлогизм Основополагающие принципы налогообложения

Основополагающие принципы налогообложения Введение в экономику. Проблемы экономической организации общества

Введение в экономику. Проблемы экономической организации общества Наука гнома Эконома

Наука гнома Эконома Понятие экономики

Понятие экономики Презентация урока по дисциплине «Основы менеджмента

Презентация урока по дисциплине «Основы менеджмента Человек и экономика

Человек и экономика Основания применения особого порядка принятия судебного решения Выполнили: Дамаева К., Мукебенова Л.

Основания применения особого порядка принятия судебного решения Выполнили: Дамаева К., Мукебенова Л. Экономический рост. Цикличность экономического развития

Экономический рост. Цикличность экономического развития Popyt turystyczny

Popyt turystyczny Просмотр накладных «в пути» и оприходование товара на свой склад. Просмотр остатков товара на складе.

Просмотр накладных «в пути» и оприходование товара на свой склад. Просмотр остатков товара на складе. Макроекономічне програмування та планування в системі державного регулювання економіки (Тема 3.2)

Макроекономічне програмування та планування в системі державного регулювання економіки (Тема 3.2) Современная конъюнктура мирового товарного рынка

Современная конъюнктура мирового товарного рынка Об экономном расходовании энергоресурсов

Об экономном расходовании энергоресурсов Консультационная деятельность МБУ ИКЦ «Янаул Информ» муниципального района Янаульский район РБ

Консультационная деятельность МБУ ИКЦ «Янаул Информ» муниципального района Янаульский район РБ Презентация Принципы международно-правового регулирования социального обеспечения

Презентация Принципы международно-правового регулирования социального обеспечения  Как работает рынок: спрос и предложение. Экономика для школьников. Главы №№ 3 - 4

Как работает рынок: спрос и предложение. Экономика для школьников. Главы №№ 3 - 4 Specificul determinării tarifelor la servicii

Specificul determinării tarifelor la servicii Корпоративные производственные системы. Развитие производственных систем. Факторы и концепции

Корпоративные производственные системы. Развитие производственных систем. Факторы и концепции Бюджет страны и бюджетно-налоговая политика. (Тема 7)

Бюджет страны и бюджетно-налоговая политика. (Тема 7) Продукция республиканских товаропроизводителей в ассортименте социально значимой группы товаров в округах Башкортостана

Продукция республиканских товаропроизводителей в ассортименте социально значимой группы товаров в округах Башкортостана Методы и функции экономической теории

Методы и функции экономической теории Социальный капитал. Характеристика и роль развития в экономических субъектах

Социальный капитал. Характеристика и роль развития в экономических субъектах Экономика. (10 класс, урок № 3)

Экономика. (10 класс, урок № 3) Экономические функции домохозяйства

Экономические функции домохозяйства Оценка коммерческого потенциала Технологии

Оценка коммерческого потенциала Технологии Механизмы совместного предпринимательства: структура и инструменты

Механизмы совместного предпринимательства: структура и инструменты Экономика родного края

Экономика родного края