- Ryanair & Aer Lingus

Содержание

- 2. SUMMARY BACKGROUND INFORMATION ON THE FIRMS AND MARKET BRIEF OVERVIEW OF THE ENTRY DETERRENCE AND EFFICIENCY

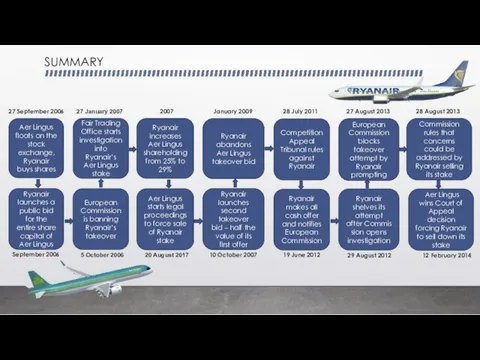

- 3. SUMMARY 27 September 2006 September 2006 5 October 2006 20 August 2017 Ryanair increases Aer Lingus

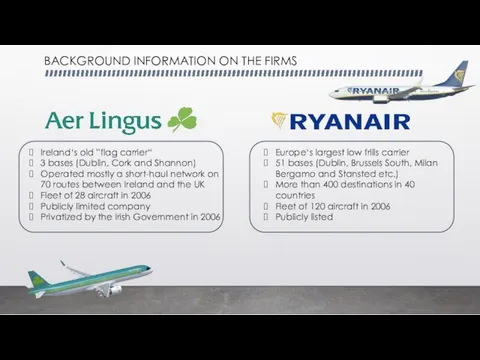

- 4. Europe‘s largest low frills carrier 51 bases (Dublin, Brussels South, Milan Bergamo and Stansted etc.) More

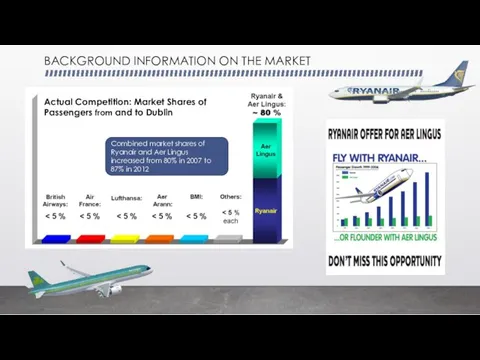

- 5. Actual Competition: Market Shares of Passengers from and to Dublin BACKGROUND INFORMATION ON THE MARKET Combined

- 6. BACKGROUND INFORMATION ON THE MARKET Irish airports are hard to penetrate for new competitors The Irish

- 7. BRIEF OVERVIEW OF THE RELEVANT THEORY Because the main arguments of Ryanair was about efficiency by

- 8. BRIEF OVERVIEW OF THE RELEVANT THEORY Model of entry deterrence from Fudenberg and Tirole (1984): The

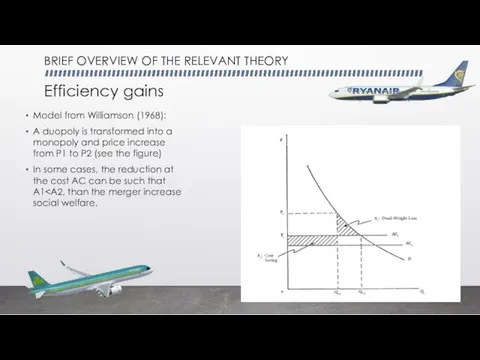

- 9. BRIEF OVERVIEW OF THE RELEVANT THEORY Efficiency gains Model from Williamson (1968): A duopoly is transformed

- 10. BRIEF OVERVIEW OF THE RELEVANT THEORY Competition and efficiency Model from Dusoet al. (2007): Main idea

- 11. THE FIRST MERGER ATTEMPT AND TRIAL PROCESS Ryanair arguments and commitments The effectivity would rise: Operational

- 12. THE FIRST MERGER ATTEMPT AND TRIAL PROCESS On the Ryanair’s post-merger cost reductions evaluation: Some efficiency

- 13. THE FIRST MERGER ATTEMPT AND TRIAL PROCESS Evaluations validity concerns: Cost reduction evaluations don’t measure any

- 14. Both companies appeal against Commission decisions in General Court Ryanair appeal the prohibition of the merger

- 15. The second attempt, result: withdrawing a bid Overview: The Raynair made a takeover bid to of

- 16. The third attempt of the takeover, result: prohibition 1) Overview: At 19.06.2012 the Raynair made another

- 17. THE EVOLUTION OF THE MARKET AFTER DECISION

- 18. THANKS FOR YOUR ATTENTION! ANY QUESTIONS?

- 20. Скачать презентацию

SUMMARY

BACKGROUND INFORMATION ON THE FIRMS AND MARKET

BRIEF OVERVIEW OF THE

SUMMARY

BACKGROUND INFORMATION ON THE FIRMS AND MARKET

BRIEF OVERVIEW OF THE

SUMMARY

27 September 2006

September 2006

5 October 2006

20 August 2017

Ryanair increases Aer Lingus

SUMMARY

27 September 2006

September 2006

5 October 2006

20 August 2017

Ryanair increases Aer Lingus

Europe‘s largest low frills carrier

51 bases (Dublin, Brussels South, Milan

Europe‘s largest low frills carrier

51 bases (Dublin, Brussels South, Milan

Actual Competition: Market Shares of Passengers from and to Dublin

BACKGROUND INFORMATION

Actual Competition: Market Shares of Passengers from and to Dublin

BACKGROUND INFORMATION

BACKGROUND INFORMATION ON THE MARKET

Irish airports are hard to penetrate for

BACKGROUND INFORMATION ON THE MARKET

Irish airports are hard to penetrate for

BRIEF OVERVIEW OF THE RELEVANT THEORY

Because the main arguments of Ryanair

BRIEF OVERVIEW OF THE RELEVANT THEORY

Because the main arguments of Ryanair

BRIEF OVERVIEW OF THE RELEVANT THEORY

Model of entry deterrence from Fudenberg

BRIEF OVERVIEW OF THE RELEVANT THEORY

Model of entry deterrence from Fudenberg

BRIEF OVERVIEW OF THE RELEVANT THEORY

Efficiency gains

Model from Williamson (1968):

A duopoly

BRIEF OVERVIEW OF THE RELEVANT THEORY

Efficiency gains

Model from Williamson (1968):

A duopoly

BRIEF OVERVIEW OF THE RELEVANT THEORY

Competition and efficiency

Model from Dusoet al.

BRIEF OVERVIEW OF THE RELEVANT THEORY

Competition and efficiency

Model from Dusoet al.

THE FIRST MERGER ATTEMPT AND TRIAL PROCESS

Ryanair arguments and commitments

The effectivity

THE FIRST MERGER ATTEMPT AND TRIAL PROCESS

Ryanair arguments and commitments

The effectivity

THE FIRST MERGER ATTEMPT AND TRIAL PROCESS

On the Ryanair’s post-merger cost

THE FIRST MERGER ATTEMPT AND TRIAL PROCESS

On the Ryanair’s post-merger cost

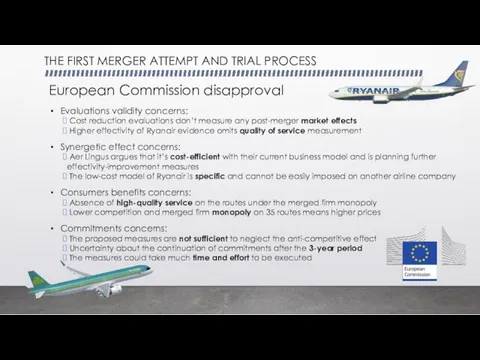

THE FIRST MERGER ATTEMPT AND TRIAL PROCESS

Evaluations validity concerns:

Cost reduction

THE FIRST MERGER ATTEMPT AND TRIAL PROCESS

Evaluations validity concerns:

Cost reduction

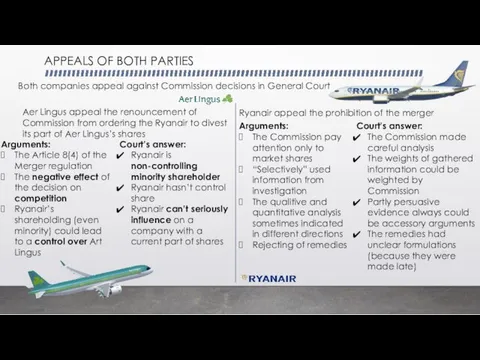

Both companies appeal against Commission decisions in General Court

Ryanair appeal the

Both companies appeal against Commission decisions in General Court

Ryanair appeal the

The second attempt, result: withdrawing a bid

Overview:

The Raynair made a takeover

The second attempt, result: withdrawing a bid

Overview:

The Raynair made a takeover

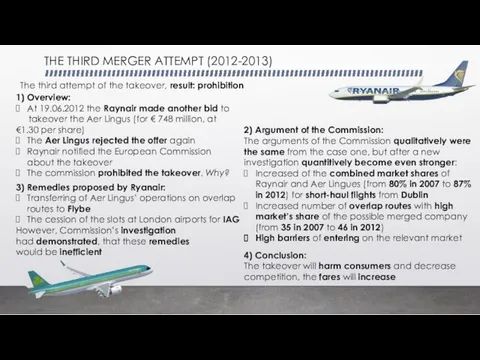

The third attempt of the takeover, result: prohibition

1) Overview:

At 19.06.2012

The third attempt of the takeover, result: prohibition

1) Overview:

At 19.06.2012

THE EVOLUTION OF THE MARKET AFTER DECISION

THE EVOLUTION OF THE MARKET AFTER DECISION

THANKS FOR YOUR ATTENTION!

ANY QUESTIONS?

THANKS FOR YOUR ATTENTION!

ANY QUESTIONS?

Равновесие потребителя

Равновесие потребителя Сбалансированность развития экономики

Сбалансированность развития экономики Классический этап экономической теории. Жан Батист Сэи

Классический этап экономической теории. Жан Батист Сэи Развитие экономики. (Тема 1)

Развитие экономики. (Тема 1) Презентация Валютный курс: понятие, виды, методы регулирования

Презентация Валютный курс: понятие, виды, методы регулирования Структура производственного процесса

Структура производственного процесса Планирование себестоимости продукции

Планирование себестоимости продукции Акт постановки на баланс остатков алкогольной продукции в ЕГАИС

Акт постановки на баланс остатков алкогольной продукции в ЕГАИС Рынки, близкие к совершенной конкуренции. Природа и виды монополии

Рынки, близкие к совершенной конкуренции. Природа и виды монополии Ресурсы мировой экономики

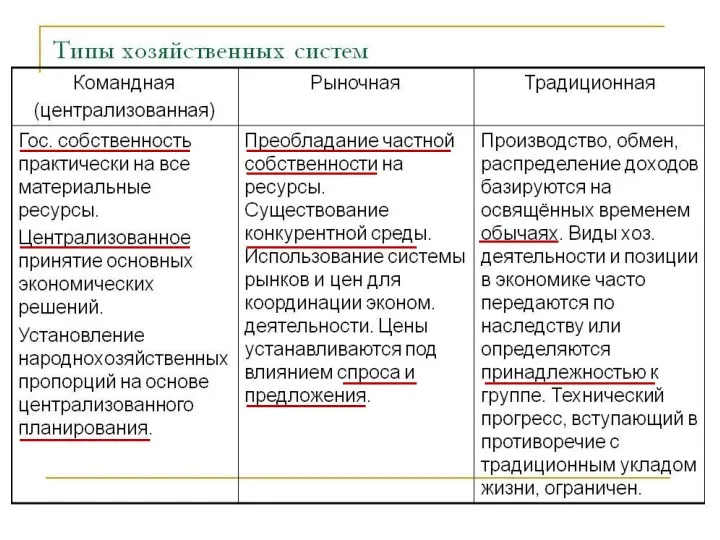

Ресурсы мировой экономики Типы хозяйственных систем. Правомочия собственника

Типы хозяйственных систем. Правомочия собственника Экономика кооперационно-сетевых взаимодействий. М к лекц 2 ФПКП

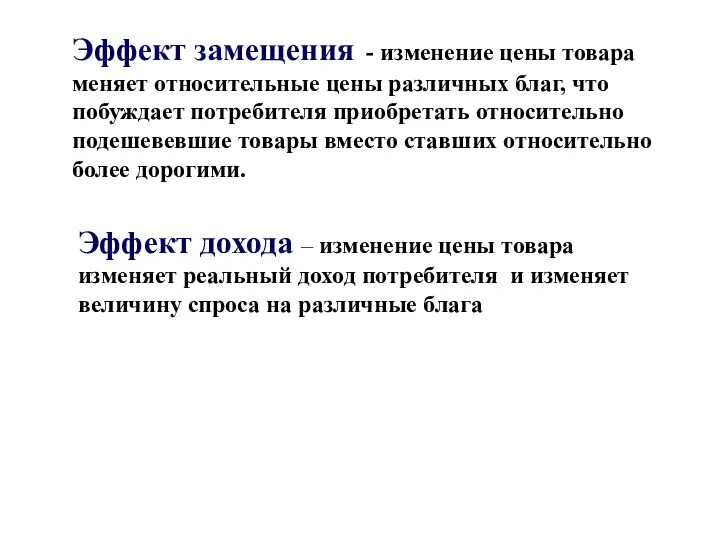

Экономика кооперационно-сетевых взаимодействий. М к лекц 2 ФПКП Эффект замещения. Эффект дохода

Эффект замещения. Эффект дохода Эффективность предпринимательской деятельности. Формирование собственных финансовых ресурсов

Эффективность предпринимательской деятельности. Формирование собственных финансовых ресурсов Максимизация прибыли. Виды рыночных структур. Тема 7

Максимизация прибыли. Виды рыночных структур. Тема 7 Классическая экономическая школа

Классическая экономическая школа Бюджетный процесс в РФ

Бюджетный процесс в РФ Налоги на прибыль

Налоги на прибыль Контролирующие иностранные компании и контролирующие лица

Контролирующие иностранные компании и контролирующие лица Региональные интеграционные блоки. Ирландия

Региональные интеграционные блоки. Ирландия Экономические вопросы в ЕГЭ по обществознанию

Экономические вопросы в ЕГЭ по обществознанию Обеспечение транспортной интеграции экономики Республики Тыва с глобальными рынками (российскими и мировыми)

Обеспечение транспортной интеграции экономики Республики Тыва с глобальными рынками (российскими и мировыми) Проблемы фискальной и монетарной политики. Макроэкономическая политика и инфляция. (Лекция 4)

Проблемы фискальной и монетарной политики. Макроэкономическая политика и инфляция. (Лекция 4) Основы предпринимательской деятельности

Основы предпринимательской деятельности ІДЗ регіональна економіка. Київська область

ІДЗ регіональна економіка. Київська область Презентация Организация и оплата труда на предприятии

Презентация Организация и оплата труда на предприятии налоги

налоги Рынок и рыночные структуры

Рынок и рыночные структуры