- Performance management. Target costing. (Topic 1)

Содержание

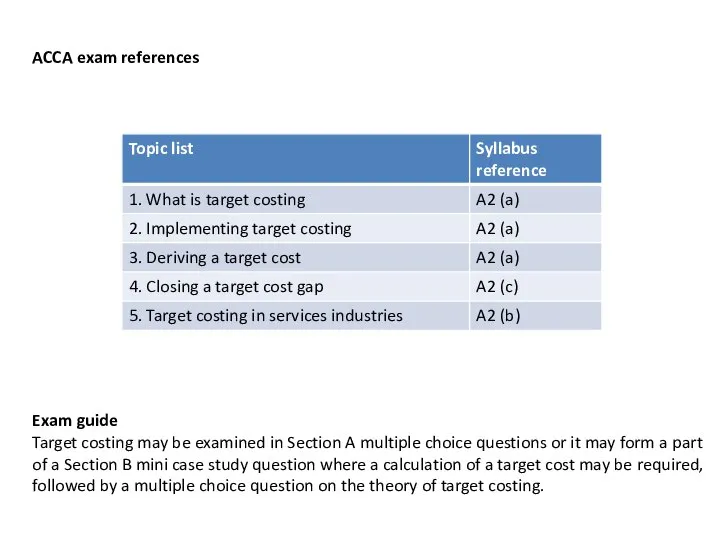

- 2. Exam guide Target costing may be examined in Section A multiple choice questions or it may

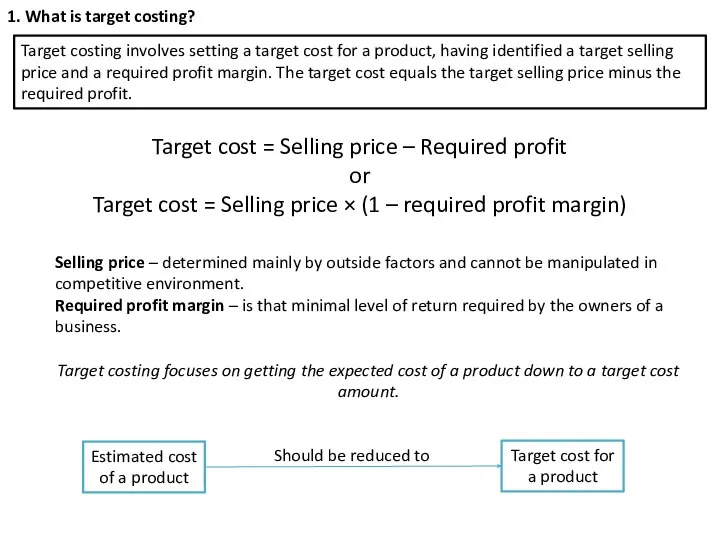

- 3. 1. What is target costing? Target costing involves setting a target cost for a product, having

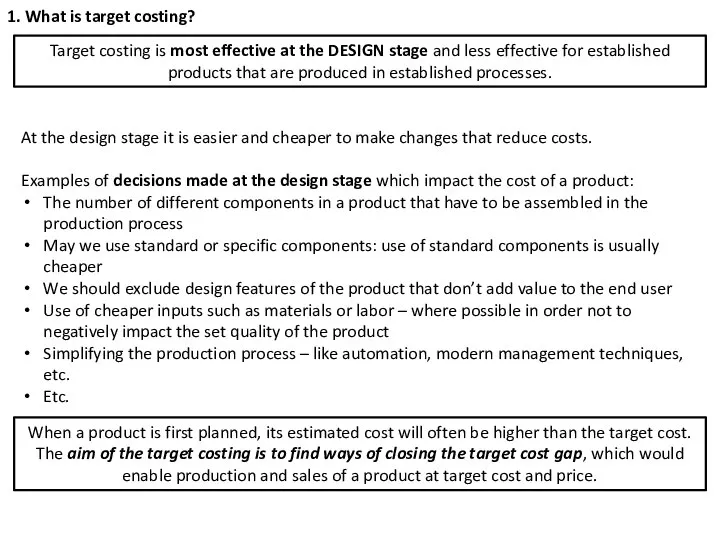

- 4. 1. What is target costing? Target costing is most effective at the DESIGN stage and less

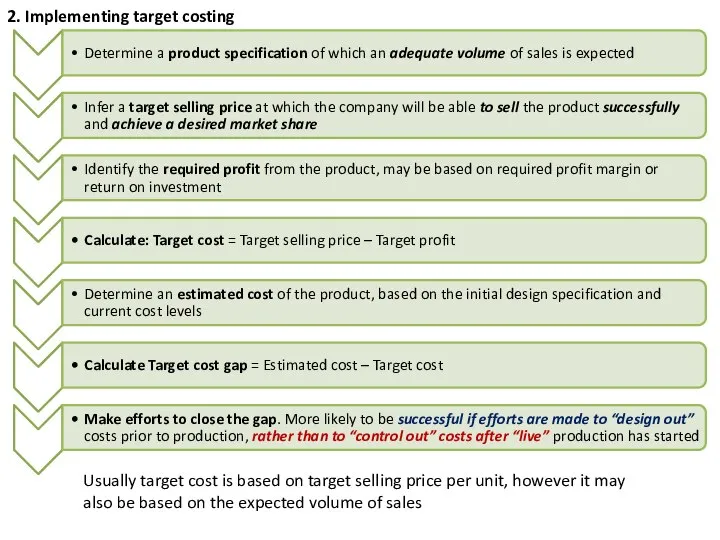

- 5. 2. Implementing target costing Usually target cost is based on target selling price per unit, however

- 6. 2. Implementing target costing – Case study Swedish retailer IKEA dominates the home furniture market in

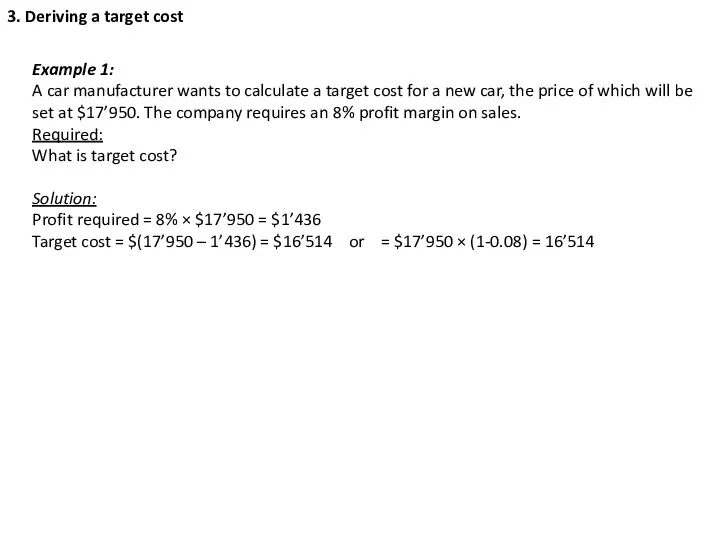

- 7. 3. Deriving a target cost Example 1: A car manufacturer wants to calculate a target cost

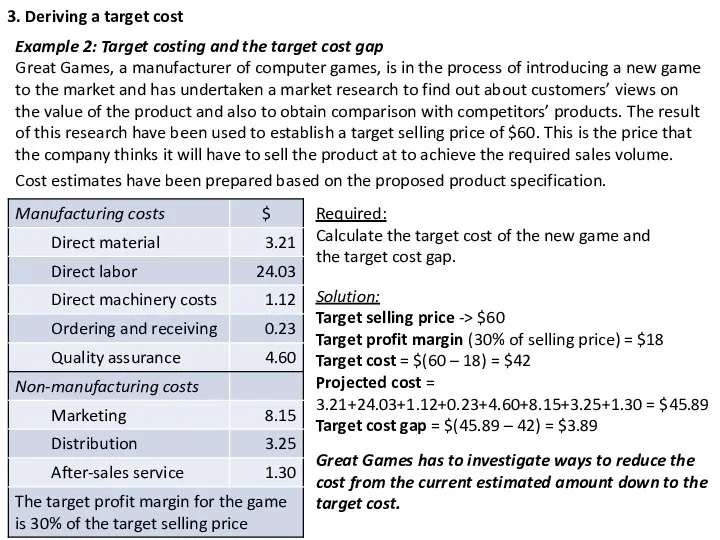

- 8. 3. Deriving a target cost Example 2: Target costing and the target cost gap Great Games,

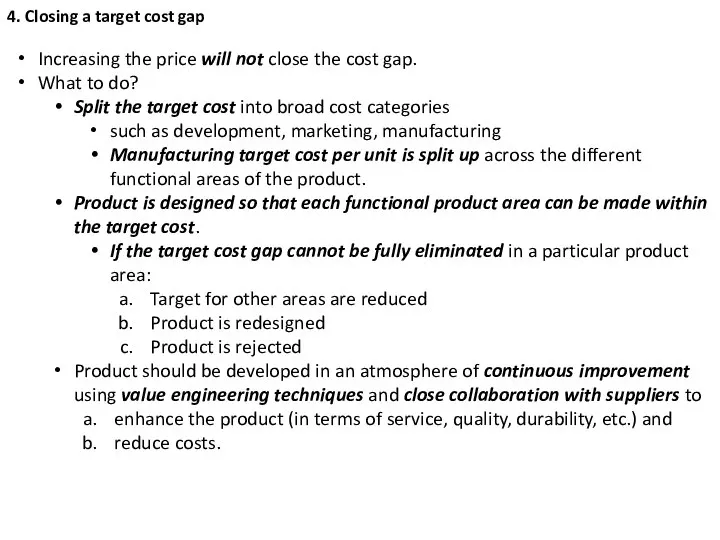

- 9. 4. Closing a target cost gap Increasing the price will not close the cost gap. What

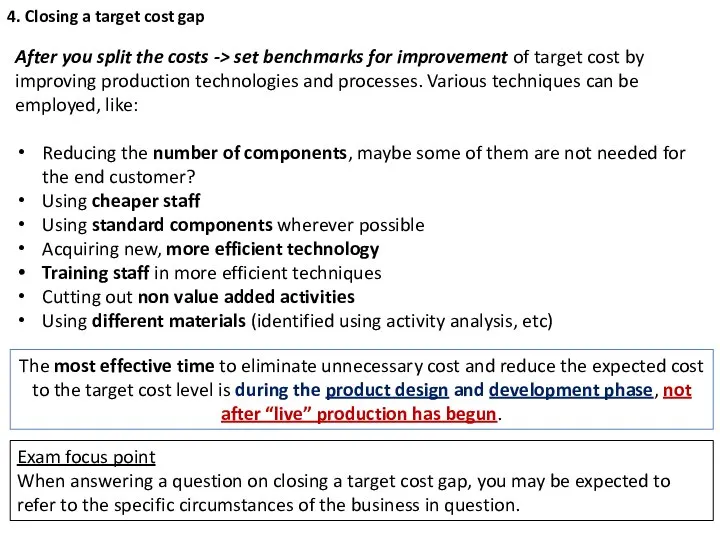

- 10. 4. Closing a target cost gap After you split the costs -> set benchmarks for improvement

- 11. 5. Target costing in service industries Examples of service businesses: Mass service eg banking, transportation (rail,

- 12. 5. Target costing in service industries Remind that: a target cost for a product is a

- 14. Скачать презентацию

Exam guide

Target costing may be examined in Section A multiple choice

Exam guide

Target costing may be examined in Section A multiple choice

1. What is target costing?

Target costing involves setting a target cost

1. What is target costing?

Target costing involves setting a target cost

1. What is target costing?

Target costing is most effective at the

1. What is target costing?

Target costing is most effective at the

2. Implementing target costing

Usually target cost is based on target selling

2. Implementing target costing

Usually target cost is based on target selling

2. Implementing target costing – Case study

Swedish retailer IKEA dominates the

2. Implementing target costing – Case study

Swedish retailer IKEA dominates the

3. Deriving a target cost

Example 1:

A car manufacturer wants to calculate

3. Deriving a target cost

Example 1:

A car manufacturer wants to calculate

3. Deriving a target cost

Example 2: Target costing and the target

3. Deriving a target cost

Example 2: Target costing and the target

4. Closing a target cost gap

Increasing the price will not close

4. Closing a target cost gap

Increasing the price will not close

4. Closing a target cost gap

After you split the costs ->

4. Closing a target cost gap

After you split the costs ->

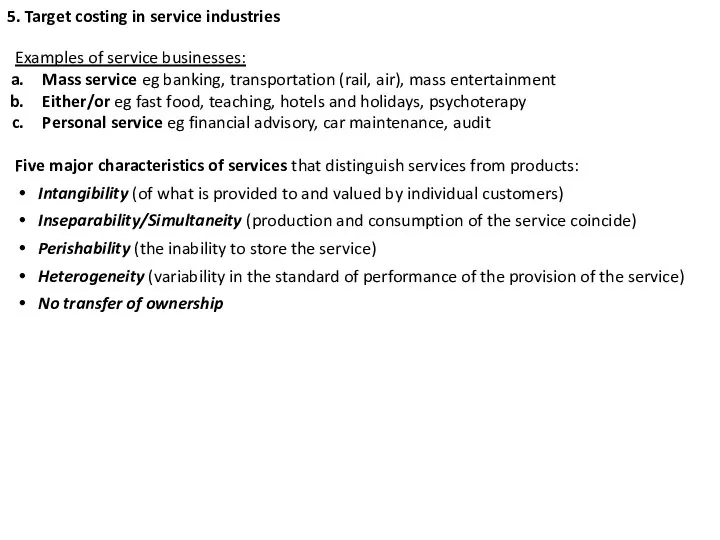

5. Target costing in service industries

Examples of service businesses:

Mass service eg

5. Target costing in service industries

Examples of service businesses:

Mass service eg

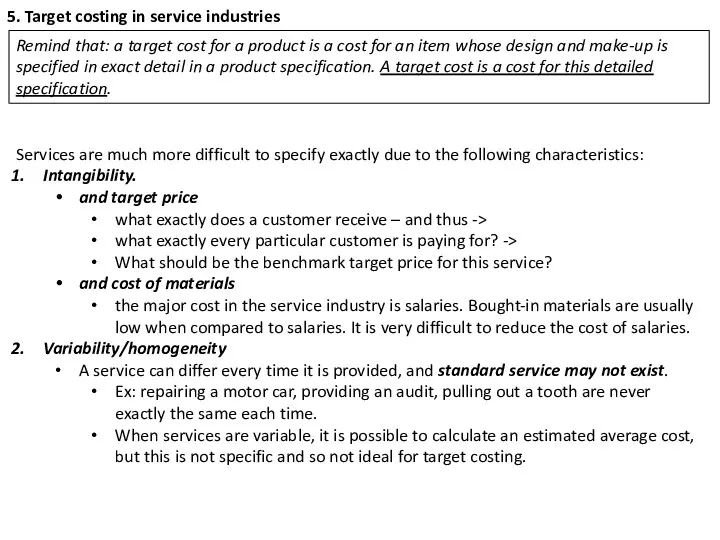

5. Target costing in service industries

Remind that: a target cost for

5. Target costing in service industries

Remind that: a target cost for

Религия, как одна из форм культуры

Религия, как одна из форм культуры История возникновения языка программирования Паскаль (Pascal)

История возникновения языка программирования Паскаль (Pascal) Гимн Герб Флаг

Гимн Герб Флаг Лекция 7 Уравнение множественной регрессии Теорема Гаусса-Маркова Автор: Костюнин Владимир Ильич, доцент кафедры: «Математ

Лекция 7 Уравнение множественной регрессии Теорема Гаусса-Маркова Автор: Костюнин Владимир Ильич, доцент кафедры: «Математ Коста Леванович Хетагуров (биография)

Коста Леванович Хетагуров (биография) Расчет экспортной, импортной и внешнеторговой квоты за период с 2000 по 2012 года на примере Новой Зеландии и ЮАР

Расчет экспортной, импортной и внешнеторговой квоты за период с 2000 по 2012 года на примере Новой Зеландии и ЮАР Понятие МФ материал

Понятие МФ материал Соединения разъёмные

Соединения разъёмные «Луч» ДО жұйесініњ орталыќ постындаѓы ТБ арнасыныњ аппаратуралары (Дәріс 9)

«Луч» ДО жұйесініњ орталыќ постындаѓы ТБ арнасыныњ аппаратуралары (Дәріс 9) Розробка рекламної поліграфічної продукції для студентського міні-кафе

Розробка рекламної поліграфічної продукції для студентського міні-кафе Прямолінійний рівноприскорений рух

Прямолінійний рівноприскорений рух Шаблон презентации проекта

Шаблон презентации проекта Презентация Отказ в выпуске товаров

Презентация Отказ в выпуске товаров Образовательная программа дошкольного образования «Рябинушка» муниципального бюджетного дошкольного образовательного учрежде

Образовательная программа дошкольного образования «Рябинушка» муниципального бюджетного дошкольного образовательного учрежде Химия элементов s-элементы

Химия элементов s-элементы  История болезни по фтизиатрии

История болезни по фтизиатрии Московская региональная программа ландшафтно-усадебной урбанизации на 2016-2025 гг

Московская региональная программа ландшафтно-усадебной урбанизации на 2016-2025 гг Система каротажа при бурении. Занятие 9

Система каротажа при бурении. Занятие 9 Анализ общемировых политических и экономических тенденций

Анализ общемировых политических и экономических тенденций Одарченко Марина Анатольевна учитель математики Муниципальное общеобразовательное учреждение «Средняя общеобразовательная шк

Одарченко Марина Анатольевна учитель математики Муниципальное общеобразовательное учреждение «Средняя общеобразовательная шк Применение метода Ченгси-Ванга для обфускации функциональных языков

Применение метода Ченгси-Ванга для обфускации функциональных языков Презентация Налоговая система РФ

Презентация Налоговая система РФ Чертежи сборочных единиц

Чертежи сборочных единиц Nikolay Vasilievich Sklifosovsky

Nikolay Vasilievich Sklifosovsky Теория и методика физической культуры. Лекция «Введение в теорию физической культуры»

Теория и методика физической культуры. Лекция «Введение в теорию физической культуры» Импрессионизм 60-90 г.г. XIX в.

Импрессионизм 60-90 г.г. XIX в. Дисциплина начертательная геометрия

Дисциплина начертательная геометрия Отчеты в Visual Studio

Отчеты в Visual Studio