- Financial econometrics

Содержание

- 2. Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD) Univariate time series models Univariate time series modelling

- 3. Quantitative Economic Analysis – 2016, Dr. Kashif Saleem (UOWD) Let ut (t=1,2,3,...) be a sequence of

- 4. Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD) An autoregressive model of order p, an AR(p)

- 5. Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD) By combining the AR(p) and MA(q) models, we

- 6. Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD) An autoregressive process has a geometrically decaying acf

- 7. Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD) The acf and pacf are not produced analytically

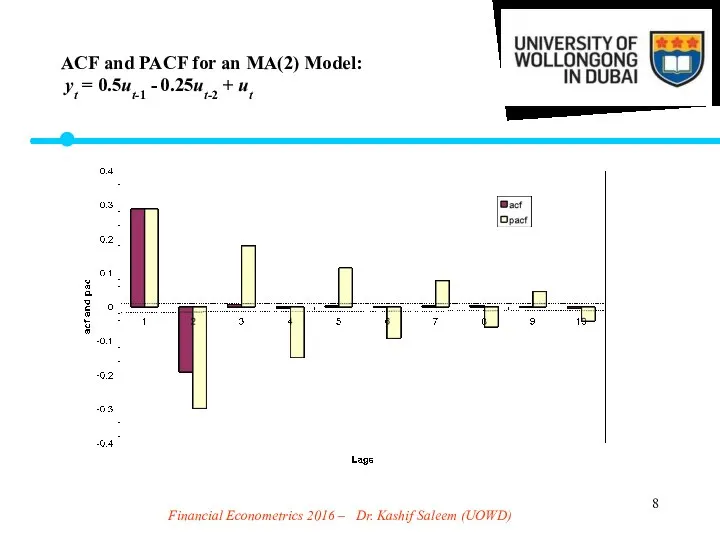

- 8. Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD) ACF and PACF for an MA(2) Model: yt

- 9. Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD) ACF and PACF for a slowly decaying AR(1)

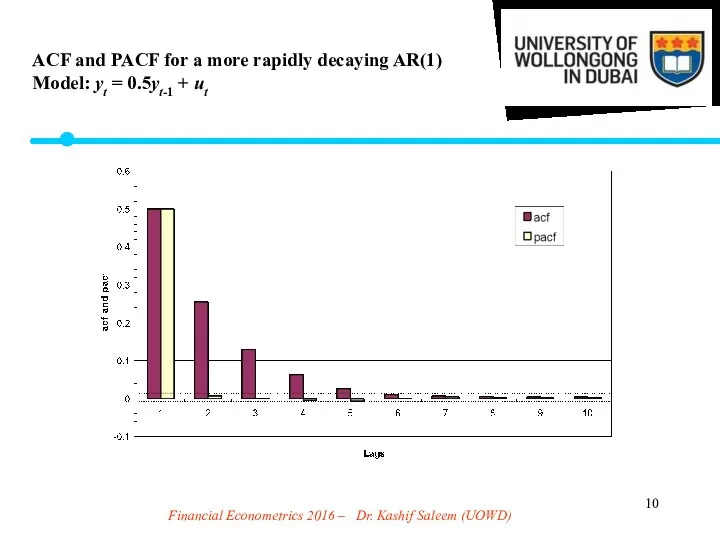

- 10. Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD) ACF and PACF for a more rapidly decaying

- 11. Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD) ACF and PACF for a more rapidly decaying

- 12. Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD) ACF and PACF for a Non-stationary Model (i.e.

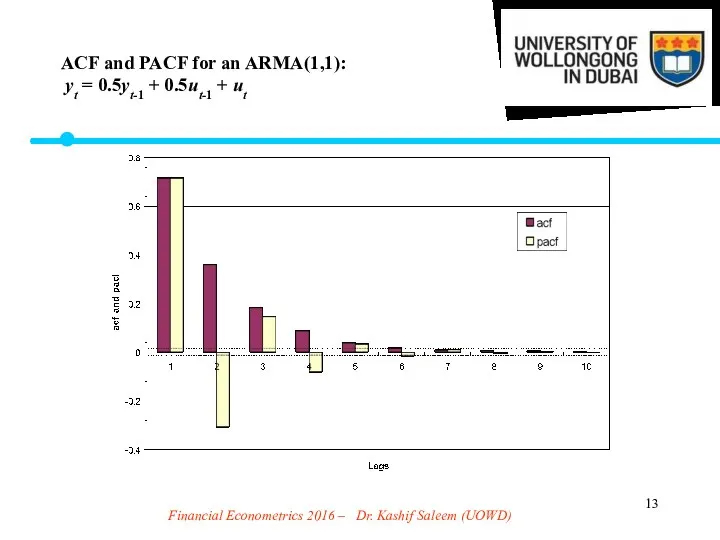

- 13. Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD) ACF and PACF for an ARMA(1,1): yt =

- 14. Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD) Box and Jenkins (1970) were the first to

- 15. Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD) Step 2: - Estimation of the parameters -

- 16. Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD) Identification would typically not be done using acf’s.

- 17. Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD) The three most popular criteria are Akaike’s (1974)

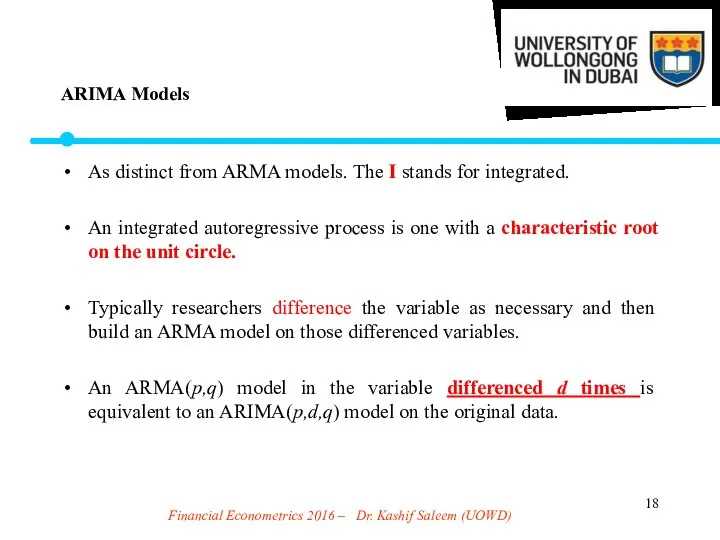

- 18. Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD) As distinct from ARMA models. The I stands

- 19. Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD) Another modelling and forecasting technique How much weight

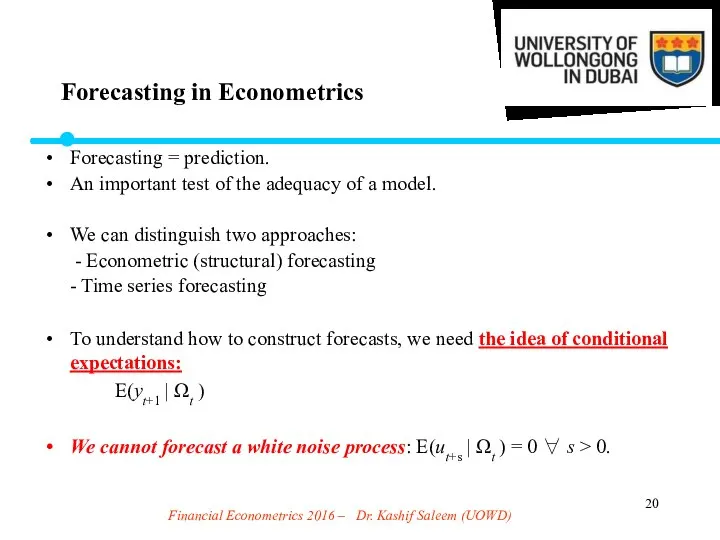

- 20. Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD) Forecasting = prediction. An important test of the

- 21. Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD) Expect the “forecast” of the model to be

- 22. Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD) Models for Forecasting Time Series Models The current

- 23. Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD) An MA(q) only has memory of q. e.g.

- 24. Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD) ft, 1 = E(yt+1 | t ) =

- 25. Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD) Say we have estimated an AR(2) yt =

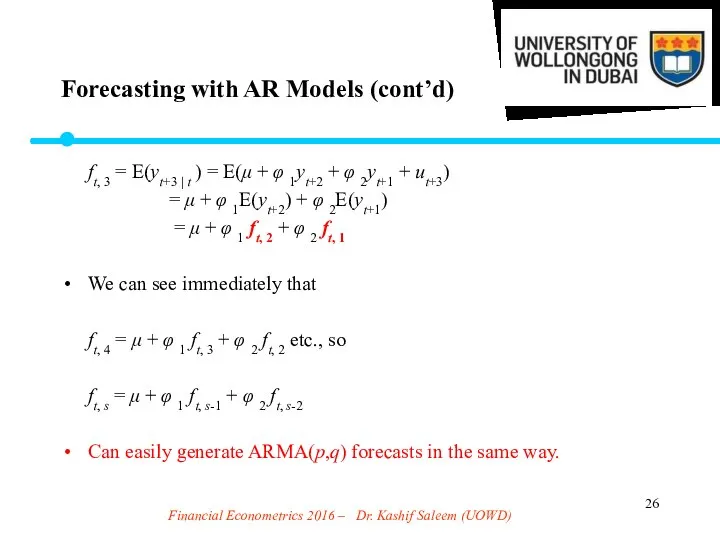

- 26. Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD) ft, 3 = E(yt+3 | t ) =

- 27. Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD) Some of the most popular criteria for assessing

- 28. Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD) A natural generalisation of autoregressive models popularised by

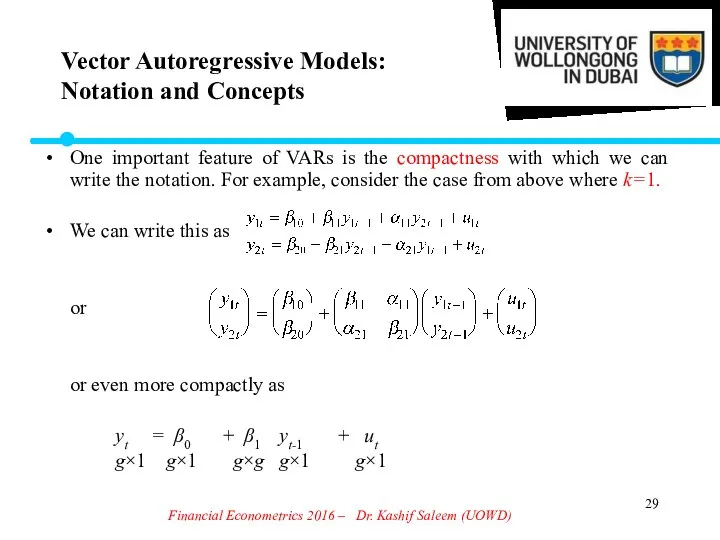

- 29. Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD) One important feature of VARs is the compactness

- 30. Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD) This model can be extended to the case

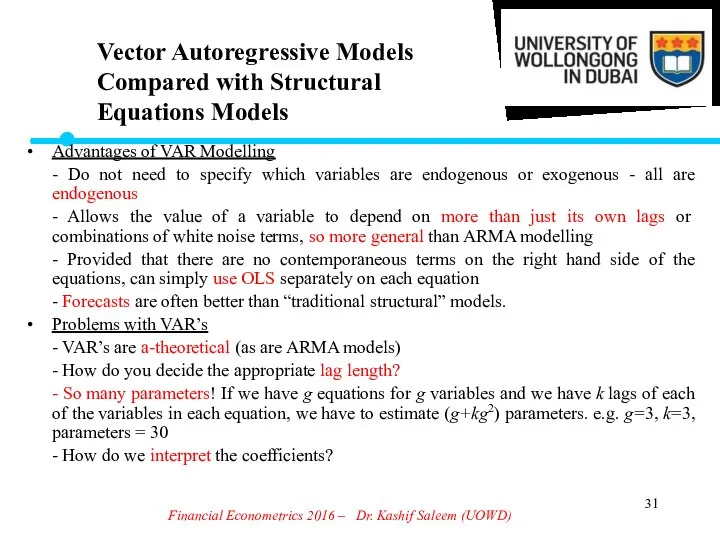

- 31. Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD) Advantages of VAR Modelling - Do not need

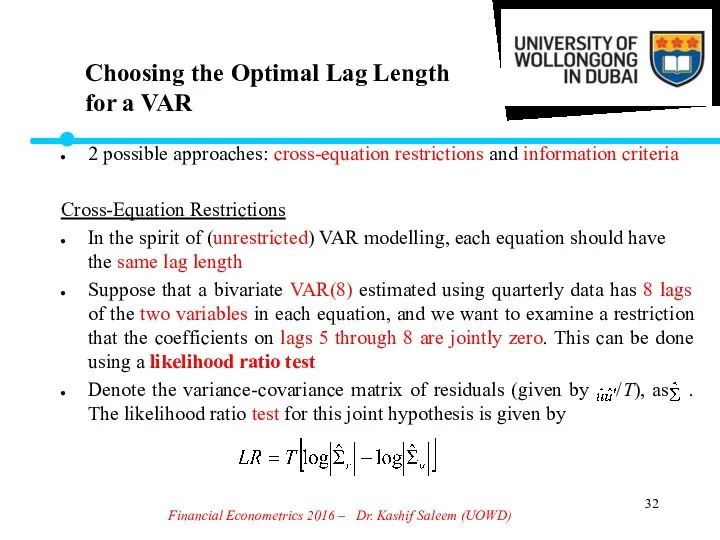

- 32. Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD) Choosing the Optimal Lag Length for a VAR

- 33. Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD) Choosing the Optimal Lag Length for a VAR

- 34. Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD) Information Criteria for VAR Lag Length Selection Multivariate

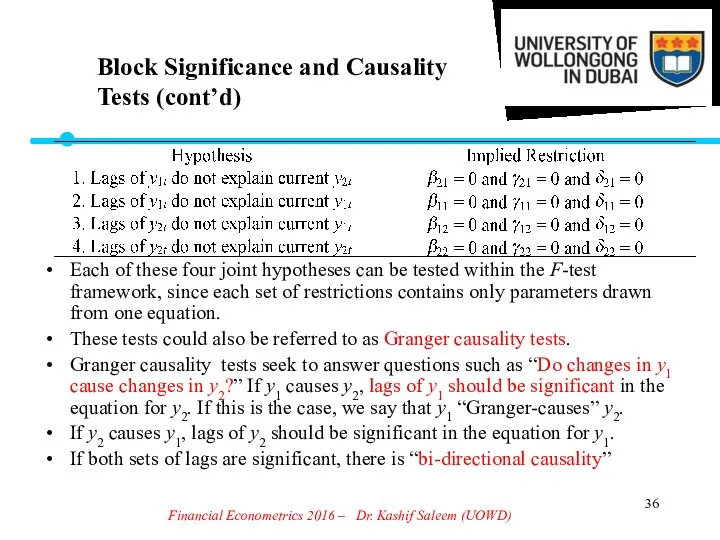

- 35. Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD) Block Significance and Causality Tests It is likely

- 36. Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD) Block Significance and Causality Tests (cont’d) Each of

- 37. Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD) Impulse Responses VAR models are often difficult to

- 38. Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD) Variance Decompositions Variance decompositions offer a slightly different

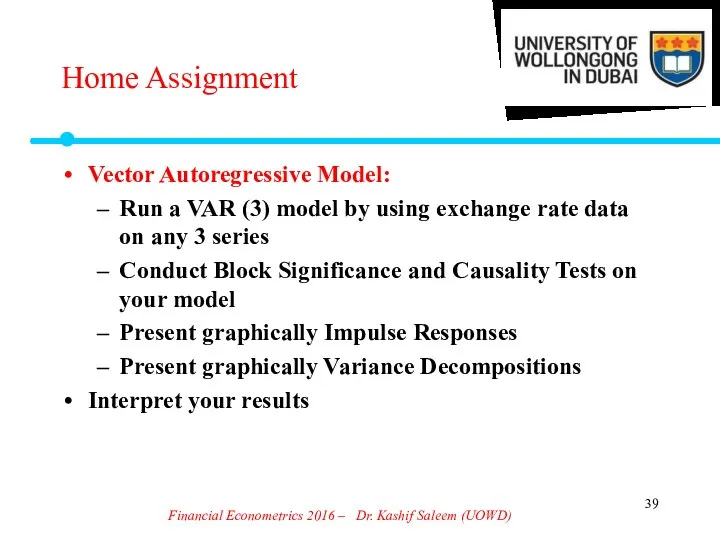

- 39. Home Assignment Vector Autoregressive Model: Run a VAR (3) model by using exchange rate data on

- 41. Скачать презентацию

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

Univariate time series models

Univariate

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

Univariate time series models

Univariate

Quantitative Economic Analysis – 2016, Dr. Kashif Saleem (UOWD)

Let ut (t=1,2,3,...)

Quantitative Economic Analysis – 2016, Dr. Kashif Saleem (UOWD)

Let ut (t=1,2,3,...)

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

An autoregressive model of

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

An autoregressive model of

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

By combining the AR(p)

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

By combining the AR(p)

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

An autoregressive process has

a

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

An autoregressive process has

a

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

The acf and pacf

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

The acf and pacf

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

ACF and PACF for

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

ACF and PACF for

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

ACF and PACF for

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

ACF and PACF for

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

ACF and PACF for

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

ACF and PACF for

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

ACF and PACF for

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

ACF and PACF for

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

ACF and PACF for

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

ACF and PACF for

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

ACF and PACF for

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

ACF and PACF for

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

Box and Jenkins (1970)

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

Box and Jenkins (1970)

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

Step 2:

- Estimation of

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

Step 2:

- Estimation of

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

Identification would typically not

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

Identification would typically not

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

The three most popular

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

The three most popular

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

As distinct from ARMA

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

As distinct from ARMA

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

Another modelling and forecasting

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

Another modelling and forecasting

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

Forecasting = prediction.

An important

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

Forecasting = prediction.

An important

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

Expect the “forecast” of

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

Expect the “forecast” of

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

Models for Forecasting

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

Models for Forecasting

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

An MA(q) only has

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

An MA(q) only has

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

ft, 1 = E(yt+1

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

ft, 1 = E(yt+1

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

Say we have estimated

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

Say we have estimated

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

ft, 3 = E(yt+3

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

ft, 3 = E(yt+3

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

Some of the most

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

Some of the most

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

A natural generalisation of

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

A natural generalisation of

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

One important feature of

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

One important feature of

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

This model can be

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

This model can be

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

Advantages of VAR Modelling

-

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

Advantages of VAR Modelling

-

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

Choosing the Optimal Lag

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

Choosing the Optimal Lag

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

Choosing the Optimal Lag

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

Choosing the Optimal Lag

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

Information Criteria for VAR

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

Information Criteria for VAR

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

Block Significance and Causality

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

Block Significance and Causality

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

Block Significance and Causality

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

Block Significance and Causality

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

Impulse Responses

VAR models are

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

Impulse Responses

VAR models are

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

Variance Decompositions

Variance decompositions

Financial Econometrics 2016 – Dr. Kashif Saleem (UOWD)

Variance Decompositions

Variance decompositions

Home Assignment

Vector Autoregressive Model:

Run a VAR (3) model by using

Home Assignment

Vector Autoregressive Model:

Run a VAR (3) model by using

Презентация Категорический силлогизм

Презентация Категорический силлогизм Основополагающие принципы налогообложения

Основополагающие принципы налогообложения Введение в экономику. Проблемы экономической организации общества

Введение в экономику. Проблемы экономической организации общества Наука гнома Эконома

Наука гнома Эконома Понятие экономики

Понятие экономики Презентация урока по дисциплине «Основы менеджмента

Презентация урока по дисциплине «Основы менеджмента Человек и экономика

Человек и экономика Основания применения особого порядка принятия судебного решения Выполнили: Дамаева К., Мукебенова Л.

Основания применения особого порядка принятия судебного решения Выполнили: Дамаева К., Мукебенова Л. Экономический рост. Цикличность экономического развития

Экономический рост. Цикличность экономического развития Popyt turystyczny

Popyt turystyczny Просмотр накладных «в пути» и оприходование товара на свой склад. Просмотр остатков товара на складе.

Просмотр накладных «в пути» и оприходование товара на свой склад. Просмотр остатков товара на складе. Макроекономічне програмування та планування в системі державного регулювання економіки (Тема 3.2)

Макроекономічне програмування та планування в системі державного регулювання економіки (Тема 3.2) Современная конъюнктура мирового товарного рынка

Современная конъюнктура мирового товарного рынка Об экономном расходовании энергоресурсов

Об экономном расходовании энергоресурсов Консультационная деятельность МБУ ИКЦ «Янаул Информ» муниципального района Янаульский район РБ

Консультационная деятельность МБУ ИКЦ «Янаул Информ» муниципального района Янаульский район РБ Презентация Принципы международно-правового регулирования социального обеспечения

Презентация Принципы международно-правового регулирования социального обеспечения  Как работает рынок: спрос и предложение. Экономика для школьников. Главы №№ 3 - 4

Как работает рынок: спрос и предложение. Экономика для школьников. Главы №№ 3 - 4 Specificul determinării tarifelor la servicii

Specificul determinării tarifelor la servicii Корпоративные производственные системы. Развитие производственных систем. Факторы и концепции

Корпоративные производственные системы. Развитие производственных систем. Факторы и концепции Бюджет страны и бюджетно-налоговая политика. (Тема 7)

Бюджет страны и бюджетно-налоговая политика. (Тема 7) Продукция республиканских товаропроизводителей в ассортименте социально значимой группы товаров в округах Башкортостана

Продукция республиканских товаропроизводителей в ассортименте социально значимой группы товаров в округах Башкортостана Методы и функции экономической теории

Методы и функции экономической теории Социальный капитал. Характеристика и роль развития в экономических субъектах

Социальный капитал. Характеристика и роль развития в экономических субъектах Экономика. (10 класс, урок № 3)

Экономика. (10 класс, урок № 3) Экономические функции домохозяйства

Экономические функции домохозяйства Оценка коммерческого потенциала Технологии

Оценка коммерческого потенциала Технологии Механизмы совместного предпринимательства: структура и инструменты

Механизмы совместного предпринимательства: структура и инструменты Экономика родного края

Экономика родного края