- World economics: microfinance

Содержание

- 2. INTRO MICROFINANCE Social impact of Banks; basic mechanism of capital accumulation; public and private investments; human

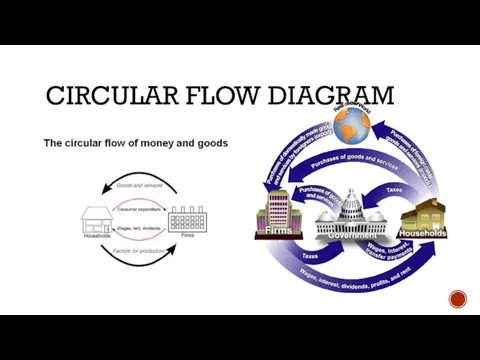

- 3. CIRCULAR FLOW DIAGRAM

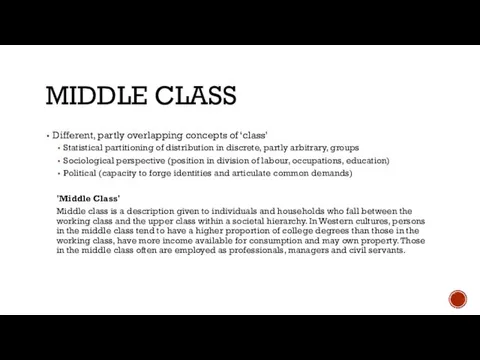

- 4. MIDDLE CLASS Different, partly overlapping concepts of ‘class’ Statistical partitioning of distribution in discrete, partly arbitrary,

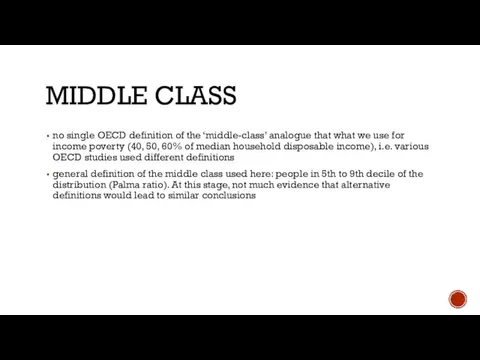

- 5. MIDDLE CLASS no single OECD definition of the ‘middle-class’ analogue that what we use for income

- 6. MIDDLE CLASS DEPENDS ON EARNINGS AS MAIN INCOME SOURCE

- 7. INCREASINGLY DUAL-EARNINGS HOUSEHOLDS

- 8. PREDOMINANTLY PRIME-AGED (WITH CHILDREN)

- 9. SIGNIFICANTLY CHANGES IN THE US (LOWER) AND SPAIN (HIGHER), SMALLER CHANGES ELSEWHERE

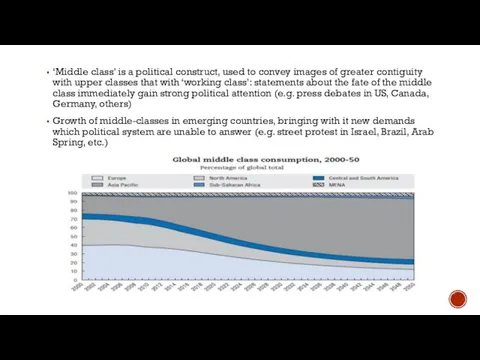

- 10. ‘Middle class’ is a political construct, used to convey images of greater contiguity with upper classes

- 11. CAPITAL ACCUMULATION Capital accumulation is a product of capital investment. Capital accumulation also increases with return

- 12. SOLOW MODEL Robert Solow developed the neo-classical theory of economic growth and Solow won the Nobel

- 13. WHAT ARE THE BASIC POINTS ABOUT THE SOLOW ECONOMIC GROWTH MODEL? The Solow model believes that

- 14. CATCH UP GROWTH / CUTTING EDGE GROWTH The Solow Model features the idea of catch-up growth

- 15. MICROFINANCE also called microcredit, is a type of banking service that is provided to unemployed or

- 16. HOW MICROFINANCE WORKS Microfinancing organizations support a wide range of activities, ranging from business start-up capital

- 17. MICROFINANCE LOAN TERMS Like conventional lenders, microfinanciers must charge interest on loans, and they institute specific

- 18. HISTORY OF MICROFINANCE Microfinance is not a new concept: Small operations have existed since the 18th

- 19. 1.0 We shall follow and advance the four principles of Grameen Bank – Discipline, Unity, Courage

- 20. documentary film directed and produced by Gayle Ferraro, exploring the impact of the Grameen Bank on

- 21. HISTORY OF MICROFINANCE India's SKS Microfinance also serves a large number of poor clients. Formed in

- 22. http://www.bfil.co.in/ SKS Microfinance renamed Bharat Financial Inclusion (June 13, 2016) Earlier in May, the company had

- 23. MICRO FINANCE FIRMS IN INDIA WITH BANKING LICENSE NEED TO BE CAREFUL AS TO NOT SERVICE

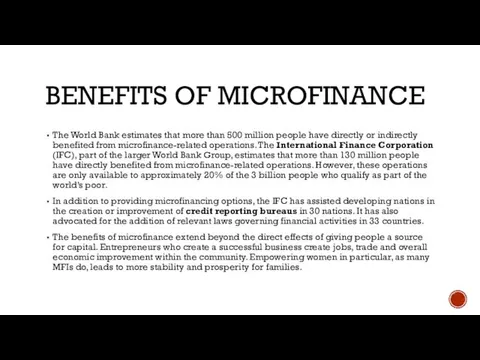

- 24. BENEFITS OF MICROFINANCE The World Bank estimates that more than 500 million people have directly or

- 25. The evolution of the industry has been driven by many factors which include the transformation of

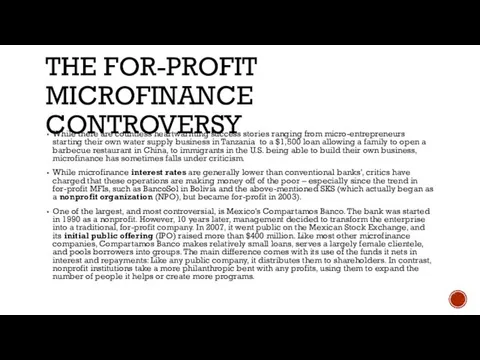

- 26. THE FOR-PROFIT MICROFINANCE CONTROVERSY While there are countless heartwarming success stories ranging from micro-entrepreneurs starting their

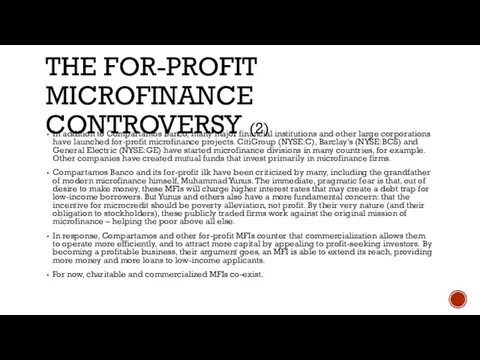

- 27. THE FOR-PROFIT MICROFINANCE CONTROVERSY (2) In addition to Compartamos Banco, many major financial institutions and other

- 28. THE MICROFINANCE DELUSION: WHO REALLY WINS?

- 29. CRISES POINTS Banks Monetary Financial Institutions (MFIs) Credit Culture Labour Slowdown Politics

- 30. HDI The HDI was created to emphasize that people and their capabilities should be the ultimate

- 32. HDI map

- 34. Скачать презентацию

INTRO

MICROFINANCE

Social impact of Banks;

basic mechanism of capital accumulation;

public and

INTRO

MICROFINANCE

Social impact of Banks;

basic mechanism of capital accumulation;

public and

CIRCULAR FLOW DIAGRAM

CIRCULAR FLOW DIAGRAM

MIDDLE CLASS

Different, partly overlapping concepts of ‘class’

Statistical partitioning of distribution

MIDDLE CLASS

Different, partly overlapping concepts of ‘class’

Statistical partitioning of distribution

MIDDLE CLASS

no single OECD definition of the ‘middle-class’ analogue that what

MIDDLE CLASS

no single OECD definition of the ‘middle-class’ analogue that what

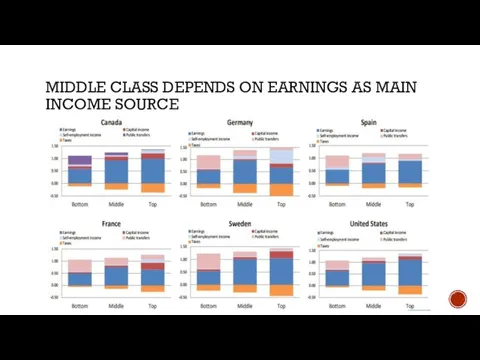

MIDDLE CLASS DEPENDS ON EARNINGS AS MAIN INCOME SOURCE

MIDDLE CLASS DEPENDS ON EARNINGS AS MAIN INCOME SOURCE

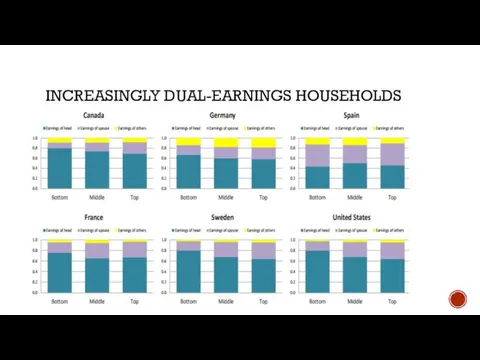

INCREASINGLY DUAL-EARNINGS HOUSEHOLDS

INCREASINGLY DUAL-EARNINGS HOUSEHOLDS

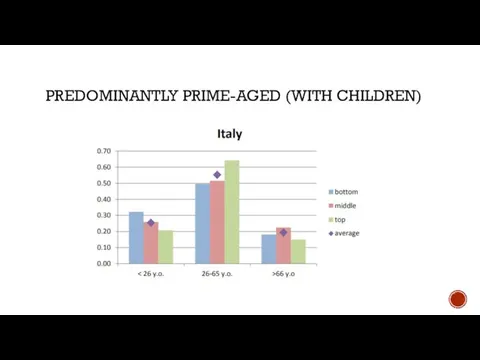

PREDOMINANTLY PRIME-AGED (WITH CHILDREN)

PREDOMINANTLY PRIME-AGED (WITH CHILDREN)

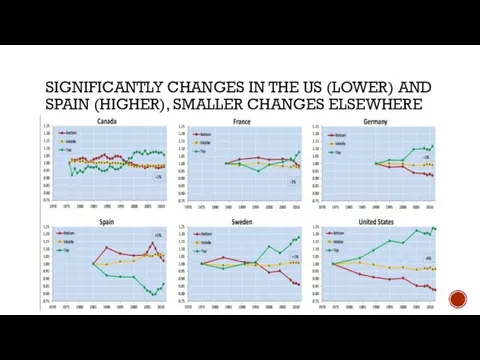

SIGNIFICANTLY CHANGES IN THE US (LOWER) AND SPAIN (HIGHER), SMALLER CHANGES

SIGNIFICANTLY CHANGES IN THE US (LOWER) AND SPAIN (HIGHER), SMALLER CHANGES

‘Middle class’ is a political construct, used to convey images of

‘Middle class’ is a political construct, used to convey images of

CAPITAL ACCUMULATION

Capital accumulation is a product of capital investment. Capital accumulation

CAPITAL ACCUMULATION

Capital accumulation is a product of capital investment. Capital accumulation

SOLOW MODEL

Robert Solow developed the neo-classical theory of economic growth and Solow won the

SOLOW MODEL

Robert Solow developed the neo-classical theory of economic growth and Solow won the

WHAT ARE THE BASIC POINTS ABOUT THE SOLOW ECONOMIC GROWTH MODEL?

The

WHAT ARE THE BASIC POINTS ABOUT THE SOLOW ECONOMIC GROWTH MODEL?

The

CATCH UP GROWTH / CUTTING EDGE GROWTH

The Solow Model features the

CATCH UP GROWTH / CUTTING EDGE GROWTH

The Solow Model features the

MICROFINANCE

also called microcredit, is a type of banking service that is

MICROFINANCE

also called microcredit, is a type of banking service that is

HOW MICROFINANCE WORKS

Microfinancing organizations support a wide range of activities, ranging

HOW MICROFINANCE WORKS

Microfinancing organizations support a wide range of activities, ranging

MICROFINANCE LOAN TERMS

Like conventional lenders, microfinanciers must charge interest on loans,

MICROFINANCE LOAN TERMS

Like conventional lenders, microfinanciers must charge interest on loans,

HISTORY OF MICROFINANCE

Microfinance is not a new concept: Small operations have

HISTORY OF MICROFINANCE

Microfinance is not a new concept: Small operations have

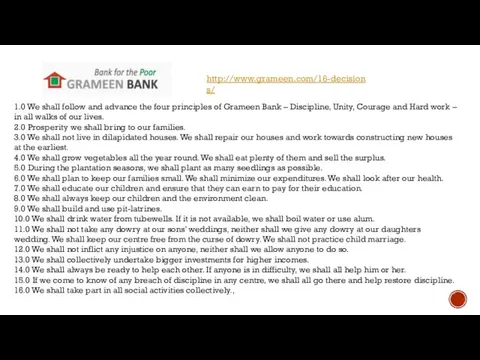

1.0 We shall follow and advance the four principles of Grameen

1.0 We shall follow and advance the four principles of Grameen

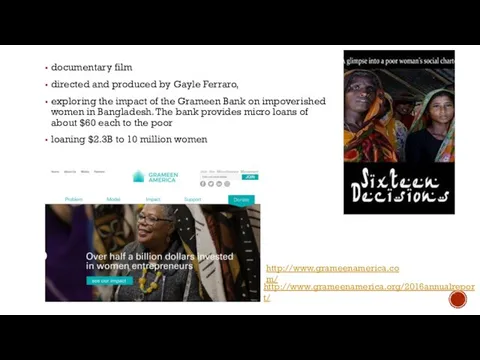

documentary film

directed and produced by Gayle Ferraro,

exploring the impact

documentary film

directed and produced by Gayle Ferraro,

exploring the impact

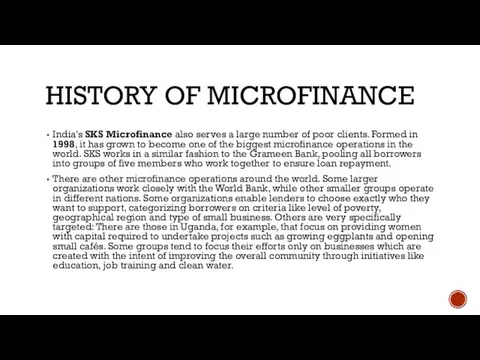

HISTORY OF MICROFINANCE

India's SKS Microfinance also serves a large number of

HISTORY OF MICROFINANCE

India's SKS Microfinance also serves a large number of

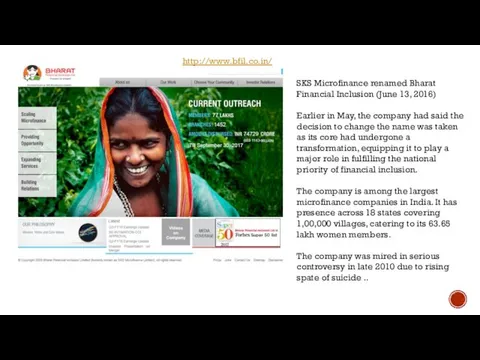

http://www.bfil.co.in/

SKS Microfinance renamed Bharat Financial Inclusion (June 13, 2016)

Earlier in

http://www.bfil.co.in/

SKS Microfinance renamed Bharat Financial Inclusion (June 13, 2016)

Earlier in

MICRO FINANCE FIRMS IN INDIA WITH BANKING LICENSE NEED TO BE

MICRO FINANCE FIRMS IN INDIA WITH BANKING LICENSE NEED TO BE

BENEFITS OF MICROFINANCE

The World Bank estimates that more than 500 million

BENEFITS OF MICROFINANCE

The World Bank estimates that more than 500 million

The evolution of the industry has been driven by many factors

The evolution of the industry has been driven by many factors

THE FOR-PROFIT MICROFINANCE CONTROVERSY

While there are countless heartwarming success stories ranging

THE FOR-PROFIT MICROFINANCE CONTROVERSY

While there are countless heartwarming success stories ranging

THE FOR-PROFIT MICROFINANCE CONTROVERSY (2)

In addition to Compartamos Banco, many major

THE FOR-PROFIT MICROFINANCE CONTROVERSY (2)

In addition to Compartamos Banco, many major

THE MICROFINANCE DELUSION: WHO REALLY WINS?

THE MICROFINANCE DELUSION: WHO REALLY WINS?

CRISES POINTS

Banks

Monetary Financial Institutions (MFIs)

Credit Culture

Labour Slowdown

Politics

CRISES POINTS

Banks

Monetary Financial Institutions (MFIs)

Credit Culture

Labour Slowdown

Politics

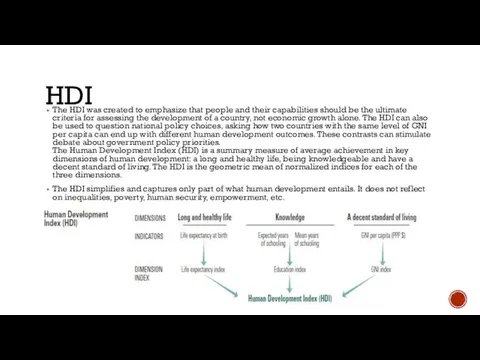

HDI

The HDI was created to emphasize that people and their capabilities

HDI

The HDI was created to emphasize that people and their capabilities

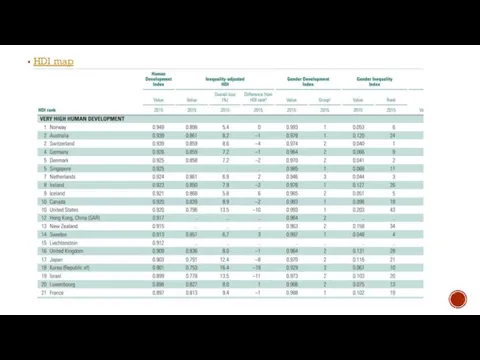

HDI map

HDI map

Внешенэкономическая деятельность: право и управление

Внешенэкономическая деятельность: право и управление AliExpress

AliExpress Особенности неравновесной конъюнктуры агропродовольственного рынка на первом и втором этапах его эволюции. (Тема 6)

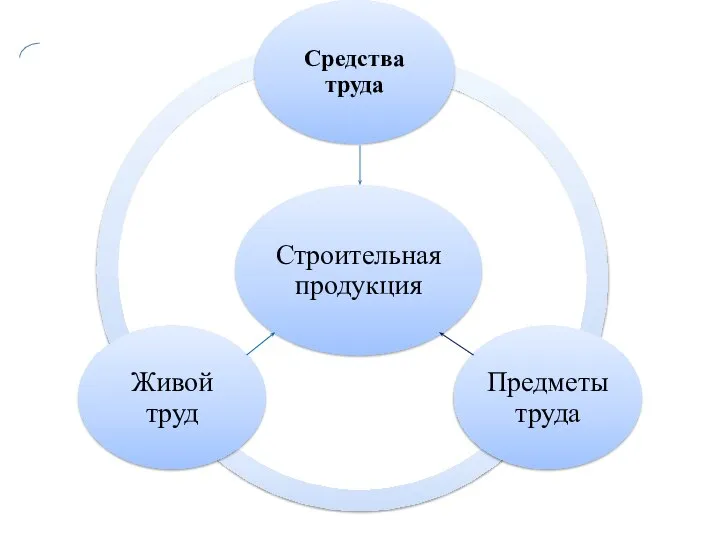

Особенности неравновесной конъюнктуры агропродовольственного рынка на первом и втором этапах его эволюции. (Тема 6) Основные фонды

Основные фонды Демографическая проблема

Демографическая проблема Анализ производственных результатов деятельности

Анализ производственных результатов деятельности Интеллектуальный капитал

Интеллектуальный капитал Три министра финансов

Три министра финансов Управление рисками иностранных инвестиций

Управление рисками иностранных инвестиций Факторы производства

Факторы производства Шымкент каласының жер ресурстарын тиімді пайдалану мәселері

Шымкент каласының жер ресурстарын тиімді пайдалану мәселері Організація і шляхи вдосконалення обліку, аудиту нерозподіленого прибутку, аналіз ефективності його використання

Організація і шляхи вдосконалення обліку, аудиту нерозподіленого прибутку, аналіз ефективності його використання Процес створення суб’єкта підприємницької діяльності та його основні етапи

Процес створення суб’єкта підприємницької діяльності та його основні етапи Стратегическое видение развития группы

Стратегическое видение развития группы Место и роль международных корпораций в международной мировой экономике на примере Johnson&Johnson

Место и роль международных корпораций в международной мировой экономике на примере Johnson&Johnson Президентская программа. Экономика для менеджеров (Управленческая экономика)

Президентская программа. Экономика для менеджеров (Управленческая экономика) Региональные союзы

Региональные союзы Инфляция (виды, причины и последствия)

Инфляция (виды, причины и последствия) Сукупний попит і сукупна пропозиція. (Тема 3)

Сукупний попит і сукупна пропозиція. (Тема 3) Восприятие торговой марки Северная долина

Восприятие торговой марки Северная долина Институциональные основы функционирования рыночной экономики

Институциональные основы функционирования рыночной экономики Экономическая безопасность Швейцарии

Экономическая безопасность Швейцарии Зарождение и этапы мирового хозяйства

Зарождение и этапы мирового хозяйства Цена, прибыль, рентабельность

Цена, прибыль, рентабельность Разработка программного обеспечения структурного анализа экономики региона

Разработка программного обеспечения структурного анализа экономики региона Рынки факторов производства

Рынки факторов производства Эффективность, Легитимность, легальность политической власти Подготовили: студентки группы Э-102, Шунайлова Жанна, Епифанова Евге

Эффективность, Легитимность, легальность политической власти Подготовили: студентки группы Э-102, Шунайлова Жанна, Епифанова Евге Модели организационной эффективности

Модели организационной эффективности