- Investment Basics

Содержание

- 2. Learning Objectives Set your goals and be ready to invest. Understand how taxes affect your investments.

- 3. Investing Versus Speculating When you buy an investment, you put money in an asset that generates

- 4. Investing Versus Speculating With speculation, assets don’t generate an income return and their value depends entirely

- 5. Investing Versus Speculating Derivative securities derive their value from the value of another asset. Futures -

- 6. Investing Versus Speculating Futures contracts deal with commodities such as oil, soybeans, or corn. It requires

- 7. Investing Versus Speculating Options markets and futures markets are a “zero sum game.” If someone makes

- 8. Setting Investment Goals When you make a plan, you must: Write down your goals and prioritize

- 9. Setting Investment Goals Formalize goals into: Short-term – within 1 year Intermediate-term – 1-10 years Long-term

- 10. Setting Investment Goals Focus on which goals are important by asking: If I don’t accomplish this

- 11. Fitting Taxes into Investing Compare returns on an after-tax basis: Marginal tax is the rate you

- 12. Starting Your Investment Program Tips to Get Started Pay yourself first – set aside savings, so

- 13. Investment Choices Lending Investments Savings accounts and bonds. Debt instruments issued by corporations and the government.

- 14. Lending Investments A savings account pays interest on the balance held in the account. With a

- 15. Ownership Investments Real estate investments in income-producing properties are illiquid. Stocks, or equities, are the most

- 16. Market Interest Rates Interest rates affect the value of stocks, bonds, and real estate. Nominal rate

- 17. What Makes Up Interest Rate Risk? Real risk-free rate of return is what investors receive for

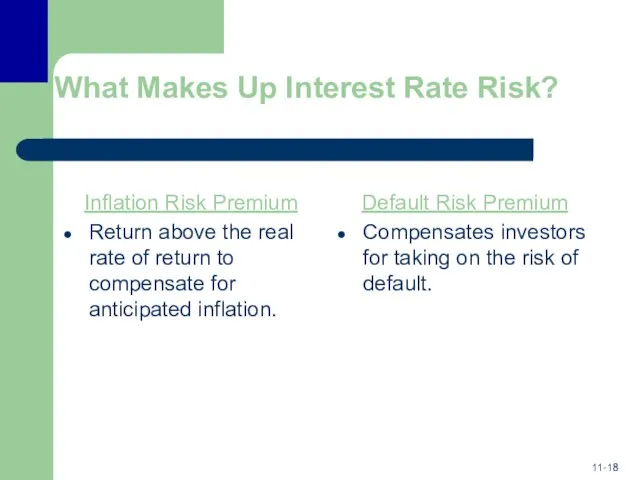

- 18. What Makes Up Interest Rate Risk? Inflation Risk Premium Return above the real rate of return

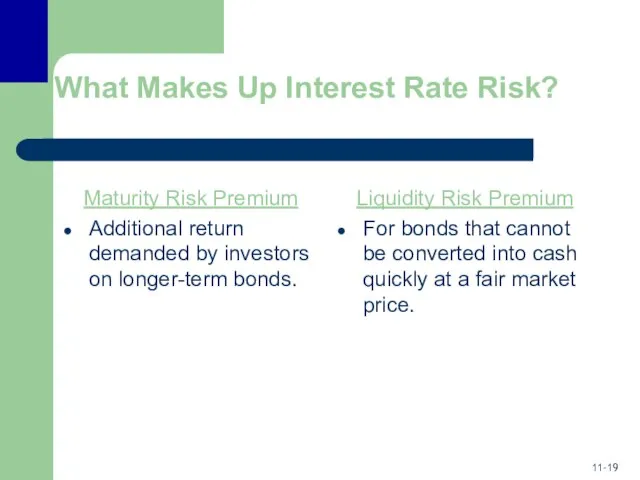

- 19. What Makes Up Interest Rate Risk? Maturity Risk Premium Additional return demanded by investors on longer-term

- 20. How Interest Rates Affect Returns on Other Investments Expected returns on all investments are related. What

- 21. Look at Risk-Return Trade-Offs Risk is related to potential return. The more risk you assume, the

- 22. Sources of Risk in the Risk-Return Trade-Off Interest Rate Risk – the higher the interest rate,

- 23. Sources of Risk in the Risk-Return Trade-Off Financial Risk – associated with the use of debt

- 24. Sources of Risk in the Risk-Return Trade-Off Market Rate Risk – associated with overall market movements.

- 25. Diversification “Don’t put all your eggs in one basket.” Extreme good and bad returns cancel out,

- 26. Systematic and Unsystematic Risk As you diversify, the variability or risk of the portfolio should decline.

- 27. Systematic and Unsystematic Risk Systematic Risk Market-related or non-diversifiable risk. That portion of a stock’s risk

- 28. How to Measure the Ultimate Risk on Your Portfolio For risk associated with investment returns, look

- 29. How to Measure the Ultimate Risk on Your Portfolio If investment time horizon is long and

- 30. Asset Allocation How your money should be divided among stocks, bonds and other investments. Investors should

- 31. Asset Allocation and Approaching Retirement The Golden Years (Age 55-64) Preserve level of wealth and allow

- 32. Asset Allocation and Approaching Retirement The Retirement Years (Over Age 65) Spending more than saving. Income

- 34. Скачать презентацию

Learning Objectives

Set your goals and be ready to invest.

Understand how taxes

Learning Objectives

Set your goals and be ready to invest.

Understand how taxes

Investing Versus Speculating

When you buy an investment, you put money in

Investing Versus Speculating

When you buy an investment, you put money in

Investing Versus Speculating

With speculation, assets don’t generate an income return and

Investing Versus Speculating

With speculation, assets don’t generate an income return and

Investing Versus Speculating

Derivative securities derive their value from the value of

Investing Versus Speculating

Derivative securities derive their value from the value of

Investing Versus Speculating

Futures contracts deal with commodities such as oil, soybeans,

Investing Versus Speculating

Futures contracts deal with commodities such as oil, soybeans,

Investing Versus Speculating

Options markets and futures markets are a “zero sum

Investing Versus Speculating

Options markets and futures markets are a “zero sum

Setting Investment Goals

When you make a plan, you must:

Write down your

Setting Investment Goals

When you make a plan, you must:

Write down your

Setting Investment Goals

Formalize goals into:

Short-term – within 1 year

Intermediate-term – 1-10

Setting Investment Goals

Formalize goals into:

Short-term – within 1 year

Intermediate-term – 1-10

Setting Investment Goals

Focus on which goals are important by asking:

If I

Setting Investment Goals

Focus on which goals are important by asking:

If I

Fitting Taxes into Investing

Compare returns on an after-tax basis:

Marginal tax

Fitting Taxes into Investing

Compare returns on an after-tax basis:

Marginal tax

Starting Your Investment Program

Tips to Get Started

Pay yourself first – set

Starting Your Investment Program

Tips to Get Started

Pay yourself first – set

Investment Choices

Lending Investments

Savings accounts and bonds.

Debt instruments issued by corporations

Investment Choices

Lending Investments

Savings accounts and bonds.

Debt instruments issued by corporations

Lending Investments

A savings account pays interest on the balance held in

Lending Investments

A savings account pays interest on the balance held in

Ownership Investments

Real estate investments in income-producing properties are illiquid.

Stocks, or equities,

Ownership Investments

Real estate investments in income-producing properties are illiquid.

Stocks, or equities,

Market Interest Rates

Interest rates affect the value of stocks, bonds, and

Market Interest Rates

Interest rates affect the value of stocks, bonds, and

What Makes Up Interest Rate Risk?

Real risk-free rate of return is

What Makes Up Interest Rate Risk?

Real risk-free rate of return is

What Makes Up Interest Rate Risk?

Inflation Risk Premium

Return above the

What Makes Up Interest Rate Risk?

Inflation Risk Premium

Return above the

What Makes Up Interest Rate Risk?

Maturity Risk Premium

Additional return demanded

What Makes Up Interest Rate Risk?

Maturity Risk Premium

Additional return demanded

How Interest Rates Affect Returns on Other Investments

Expected returns on all

How Interest Rates Affect Returns on Other Investments

Expected returns on all

Look at Risk-Return Trade-Offs

Risk is related to potential return.

The more risk

Look at Risk-Return Trade-Offs

Risk is related to potential return.

The more risk

Sources of Risk in the

Risk-Return Trade-Off

Interest Rate Risk – the higher

Sources of Risk in the

Risk-Return Trade-Off

Interest Rate Risk – the higher

Sources of Risk in the

Risk-Return Trade-Off

Financial Risk – associated with the

Sources of Risk in the

Risk-Return Trade-Off

Financial Risk – associated with the

Sources of Risk in the

Risk-Return Trade-Off

Market Rate Risk – associated with

Sources of Risk in the

Risk-Return Trade-Off

Market Rate Risk – associated with

Diversification

“Don’t put all your eggs in one basket.”

Extreme good and bad

Diversification

“Don’t put all your eggs in one basket.”

Extreme good and bad

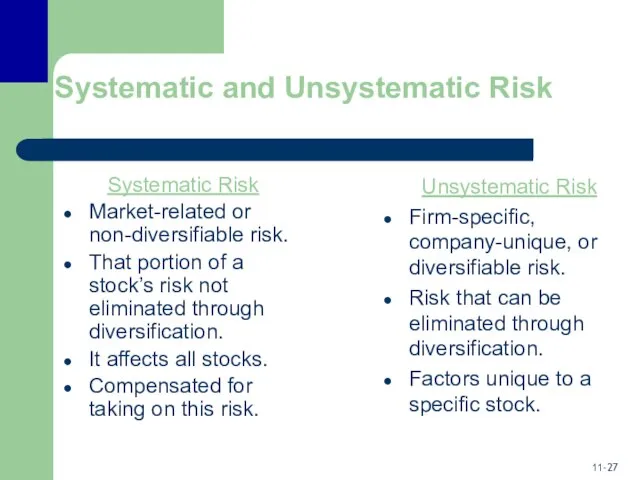

Systematic and Unsystematic Risk

As you diversify, the variability or risk of

Systematic and Unsystematic Risk

As you diversify, the variability or risk of

Systematic and Unsystematic Risk

Systematic Risk

Market-related or non-diversifiable risk.

That portion of a

Systematic and Unsystematic Risk

Systematic Risk

Market-related or non-diversifiable risk.

That portion of a

How to Measure the Ultimate Risk on Your Portfolio

For risk associated

How to Measure the Ultimate Risk on Your Portfolio

For risk associated

How to Measure the Ultimate Risk on Your Portfolio

If investment time

How to Measure the Ultimate Risk on Your Portfolio

If investment time

Asset Allocation

How your money should be divided among stocks, bonds and

Asset Allocation

How your money should be divided among stocks, bonds and

Asset Allocation and Approaching Retirement

The Golden Years (Age 55-64)

Preserve level of

Asset Allocation and Approaching Retirement

The Golden Years (Age 55-64)

Preserve level of

Asset Allocation and Approaching Retirement

The Retirement Years (Over Age 65)

Spending more

Asset Allocation and Approaching Retirement

The Retirement Years (Over Age 65)

Spending more

Новые положения по бухгалтерскому учету. Учет фактов хозяйственной деятельности (часть1)

Новые положения по бухгалтерскому учету. Учет фактов хозяйственной деятельности (часть1) Осторожно, финансовые мошенники

Осторожно, финансовые мошенники Трансформация платежных систем на основе Block-Chain технологий

Трансформация платежных систем на основе Block-Chain технологий Стационарное социальное обслуживание

Стационарное социальное обслуживание Классическое брокерское обслуживание. ВТБ 24

Классическое брокерское обслуживание. ВТБ 24 Программа Universal Life. Страховая защита, сохранение и накопление капитала

Программа Universal Life. Страховая защита, сохранение и накопление капитала Рискогенная сила бухгалтерской финансовой отчётности: опыт Великой депрессии

Рискогенная сила бухгалтерской финансовой отчётности: опыт Великой депрессии Оценка точности прогноза

Оценка точности прогноза ГБУЗ Успенская ЦРБ МЗ КК

ГБУЗ Успенская ЦРБ МЗ КК Обслуживание пассажиров при нерегулярности полетов

Обслуживание пассажиров при нерегулярности полетов Мой выбор – профессия бухгалтера

Мой выбор – профессия бухгалтера Национальная сертификация. Профессиональный бухгалтер Казахстана

Национальная сертификация. Профессиональный бухгалтер Казахстана Introduction to Project Finance. Project Appraisal, Financing and Management

Introduction to Project Finance. Project Appraisal, Financing and Management Разворотные свечи и свечные формации разворота

Разворотные свечи и свечные формации разворота Помощник бухгалтера

Помощник бухгалтера Банкротство Физических лиц

Банкротство Физических лиц Рабочий отчет департамента аналитики компании IPO

Рабочий отчет департамента аналитики компании IPO Самые странные налоги, которые пока не ввели в России

Самые странные налоги, которые пока не ввели в России Инвестор. Цена

Инвестор. Цена Проект Open Budget - Mykolayiv

Проект Open Budget - Mykolayiv Історія виникнення грошей

Історія виникнення грошей Мультивалютный робот-советник Kyber Sova. Инструмент торговли на рынке FOREX

Мультивалютный робот-советник Kyber Sova. Инструмент торговли на рынке FOREX Actual problems of commercial banks deposit policy

Actual problems of commercial banks deposit policy Самозанятость

Самозанятость Кредит на исполнение контракта от ООО Экспобанк. Умный банк для умного бизнеса

Кредит на исполнение контракта от ООО Экспобанк. Умный банк для умного бизнеса Инвестиционное планирование

Инвестиционное планирование Опорные схемы. Теоретические основы банковского менеджмента

Опорные схемы. Теоретические основы банковского менеджмента Зарплатный проект в рамках Пакетов решений Alfa Smart

Зарплатный проект в рамках Пакетов решений Alfa Smart