- The time value of money. (Lecture 2)

Содержание

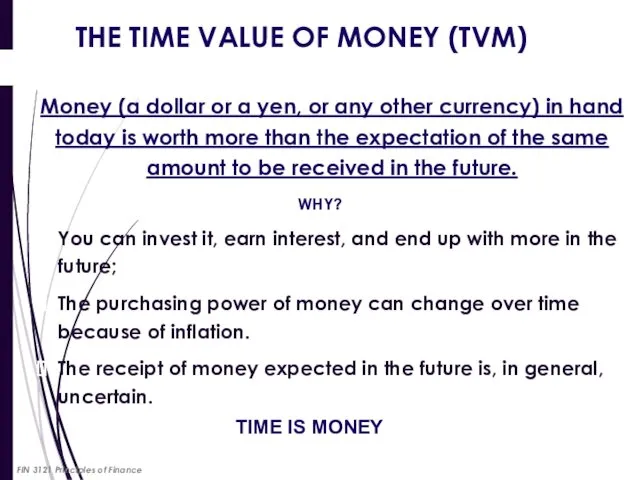

- 2. THE TIME VALUE OF MONEY (TVM) Money (a dollar or a yen, or any other currency)

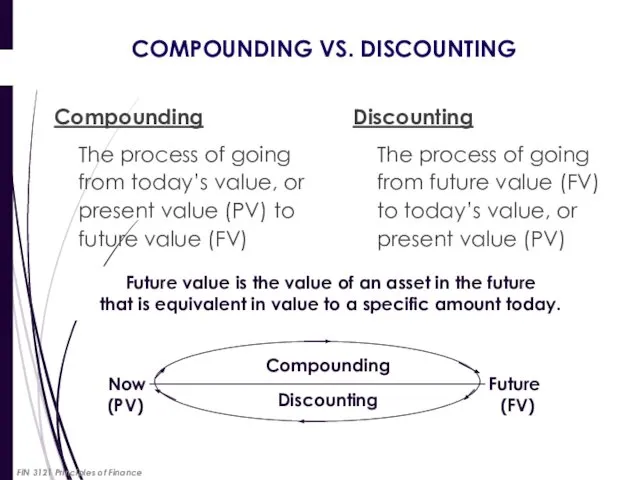

- 3. COMPOUNDING VS. DISCOUNTING Compounding The process of going from today’s value, or present value (PV) to

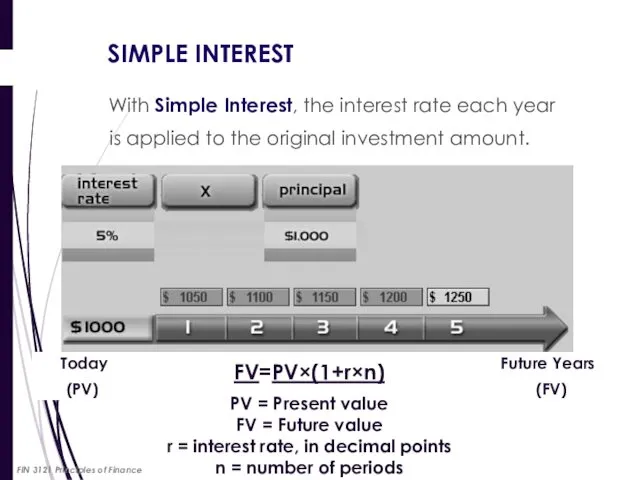

- 4. SIMPLE INTEREST With Simple Interest, the interest rate each year is applied to the original investment

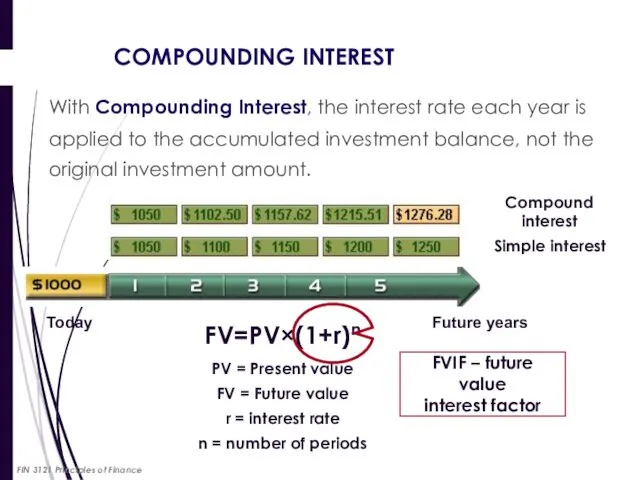

- 5. COMPOUNDING INTEREST With Compounding Interest, the interest rate each year is applied to the accumulated investment

- 6. COMPOUNDING INTEREST 1776 1800 1865 1929 1996 To see how much $2 investment would have grown,

- 7. THE TIMELINE A timeline is a linear representation of the timing of potential cash flows. Drawing

- 8. THE TIMELINE: EXAMPLE Problem Suppose you have a choice between receiving $5,000 today or $9,500 in

- 9. THE TIMELINE: EXAMPLE Solution The time line looks like this: In five years, the $5,000 will

- 10. COMPOUNDING INTEREST FV=PV×(1+r)n FIN 3121 Principles of Finance

- 11. FREQUENCY OF COMPOUNDING There are 12 compounding events in Bank B compared to 3 offered by

- 12. DISCOUNTING Discounting is a process of converting values to be received or paid in the future

- 13. DISCOUNTING If you can earn 5% interest compounded annually what do you need to put on

- 14. UNKNOWN VARIABLES Any time value problem involving lump sums -- i.e., a single outflow and a

- 15. EXAMPLE: UNKNOWN RATE Problem Bank A offers to pay you a lump sum of $20,000 after

- 16. EXAMPLE: UNKNOWN RATE Solution To answer this question, you have to calculate the rate of return

- 17. EXAMPLE: UNKNOWN № OF PERIODS You have decided that you will sell off your house, which

- 18. RULE OF 72 The number of years it takes for a sum of money to double

- 19. STREAM OF CASH FLOWS FIN 3121 Principles of Finance

- 20. ONLY VALUES AT THE SAME POINT IN TIME CAN BE COMPARED OR COMBINED FIN 3121 Principles

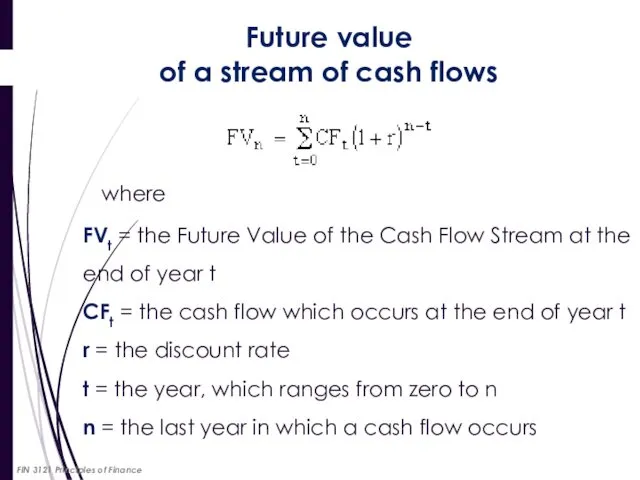

- 21. Valuing a Stream of Cash Flows General formula for valuing a stream of cash flows: if

- 22. where PV = the Present Value of the Cash Flow Stream, CFt = the cash flow

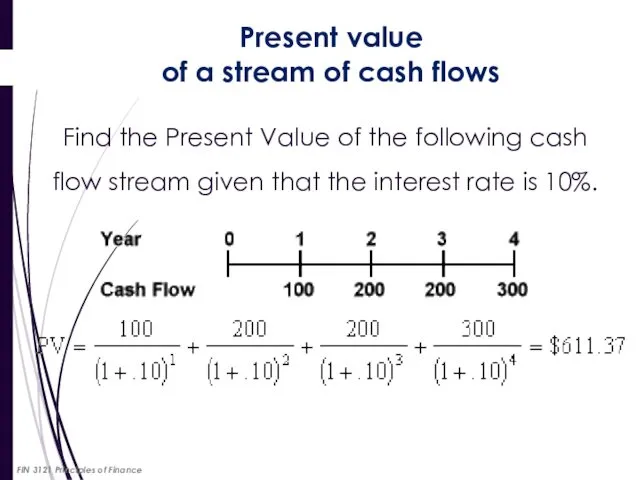

- 23. Find the Present Value of the following cash flow stream given that the interest rate is

- 24. Future value of a stream of cash flows where FVt = the Future Value of the

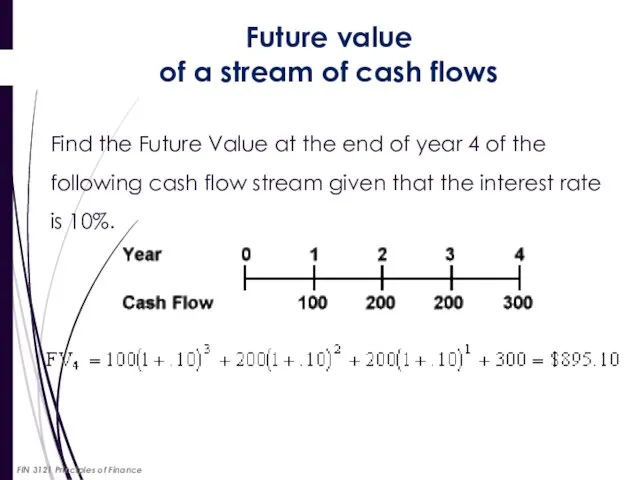

- 25. Find the Future Value at the end of year 4 of the following cash flow stream

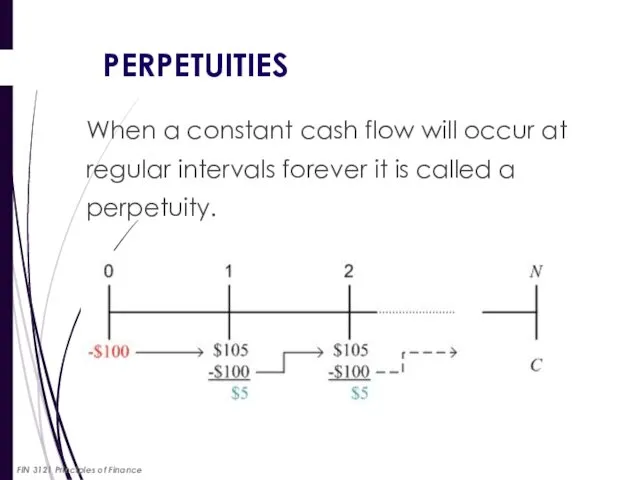

- 26. PERPETUITIES When a constant cash flow will occur at regular intervals forever it is called a

- 27. PERPETUITIES The value of a perpetuity is simply the cash flow divided by the interest rate.

- 28. PERPETUITIES: EXAMPLE Problem You want to donate to your University to endow an annual MBA graduation

- 29. PERPETUITIES: EXAMPLE FIN 3121 Principles of Finance

- 30. When a constant cash flow will occur at regular intervals for a finite number of N

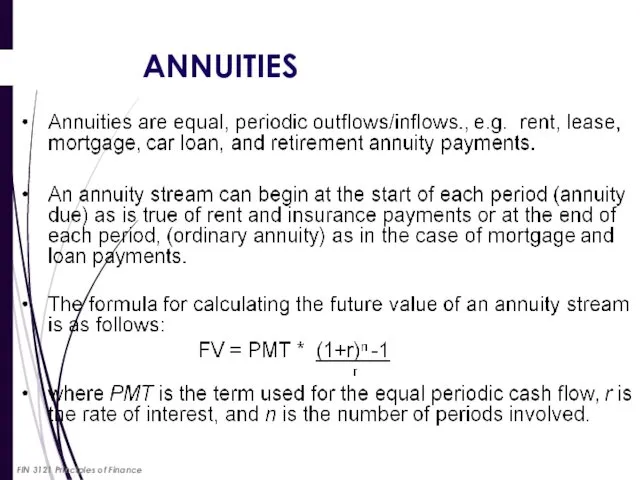

- 31. ANNUITIES FIN 3121 Principles of Finance

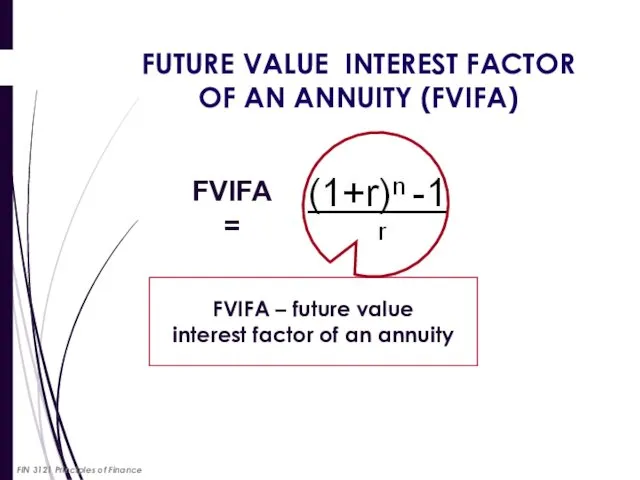

- 32. FUTURE VALUE INTEREST FACTOR OF AN ANNUITY (FVIFA) FVIFA = FVIFA – future value interest factor

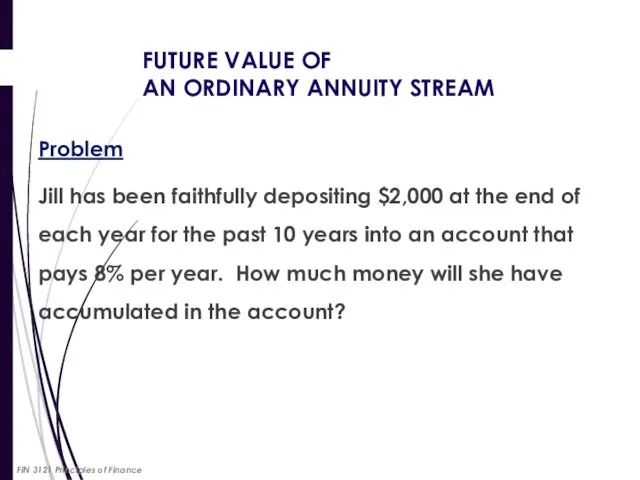

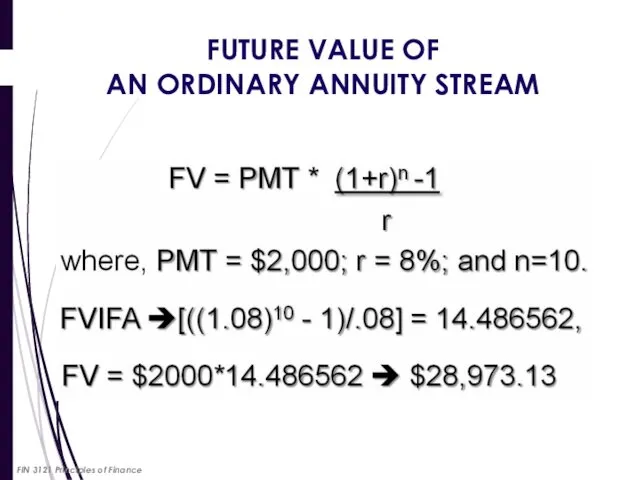

- 33. FUTURE VALUE OF AN ORDINARY ANNUITY STREAM Problem Jill has been faithfully depositing $2,000 at the

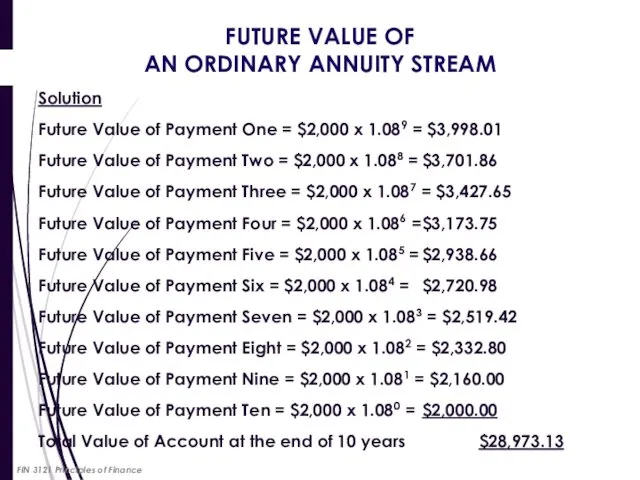

- 34. FUTURE VALUE OF AN ORDINARY ANNUITY STREAM Solution Future Value of Payment One = $2,000 x

- 35. FUTURE VALUE OF AN ORDINARY ANNUITY STREAM FIN 3121 Principles of Finance

- 36. PRESENT VALUE OF AN ANNUITY To calculate the value of a series of equal periodic cash

- 37. TIME LINE OF PRESENT VALUE OF ANNUITY STREAM FIN 3121 Principles of Finance

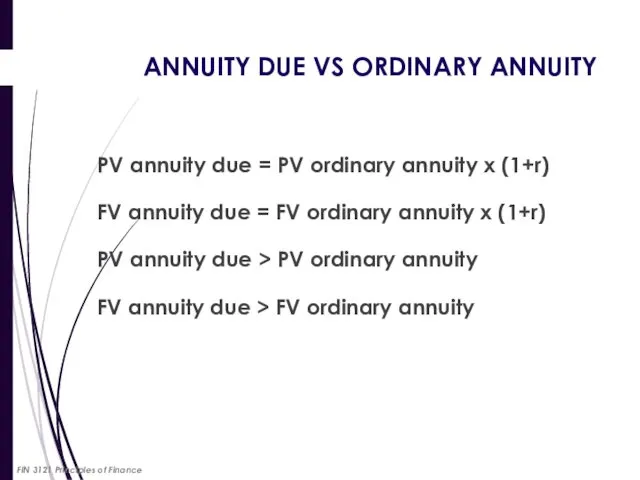

- 38. ANNUITY DUE VS ORDINARY ANNUITY A cash flow stream such as rent, lease, and insurance payments,

- 39. PV annuity due = PV ordinary annuity x (1+r) FV annuity due = FV ordinary annuity

- 40. ANNUITY DUE VS ORDINARY ANNUITY Problem: Let’s say that you are saving up for retirement and

- 41. ANNUITY DUE VS ORDINARY ANNUITY Given information: PMT = $3,000; n=20; i= 8%. FV of ordinary

- 42. TYPES OF LOAN REPAYMENTS There are 3 basic ways to repay a loan: Discount loans: pay

- 43. LOAN REPAYMENTS: EXAMPLE Problem: The Corner Bar & Grill is in the process of taking a

- 44. LOAN REPAYMENTS: EXAMPLE Solution: Under Option 1: Principal and Interest Due at the end. Payment at

- 45. LOAN REPAYMENTS: EXAMPLE Solution: Under Option 2: Interest-only Loan Annual Interest Payment (Years 1-4) = $50,000

- 46. LOAN REPAYMENTS: EXAMPLE Solution: Under Option 3: Amortized Loan To calculate the annual payment of principal

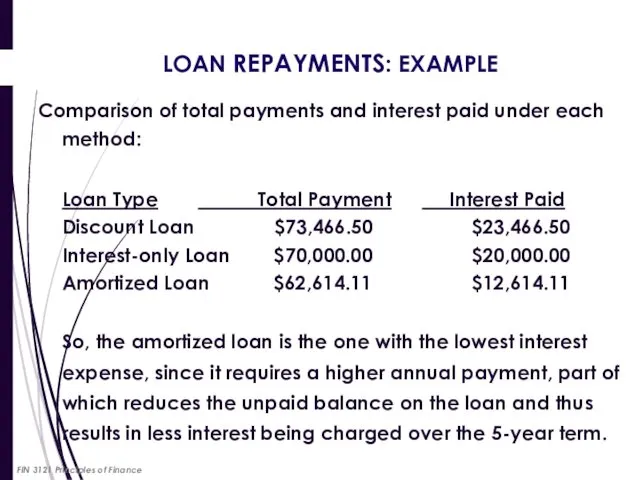

- 47. LOAN REPAYMENTS: EXAMPLE Comparison of total payments and interest paid under each method: Loan Type Total

- 48. AMORTIZATION SCHEDULES Amortization schedule contains the following information: Beginning principal; Total periodic payments; Periodic interest expense;

- 49. AMORTIZATION SCHEDULES Problem $ 25,000 loan being paid off at 8% annual interest rate within 6

- 50. AMORTIZATION SCHEDULES Solution For all consequent periods: 1. Apply step 3 to the principal amount remaining

- 51. AMORTIZATION SCHEDULES FIN 3121 Principles of Finance

- 53. Скачать презентацию

THE TIME VALUE OF MONEY (TVM)

Money (a dollar or a yen,

THE TIME VALUE OF MONEY (TVM)

Money (a dollar or a yen,

COMPOUNDING VS. DISCOUNTING

Compounding

The process of going from today’s value, or

COMPOUNDING VS. DISCOUNTING

Compounding

The process of going from today’s value, or

SIMPLE INTEREST

With Simple Interest, the interest rate each year

is applied

SIMPLE INTEREST

With Simple Interest, the interest rate each year

is applied

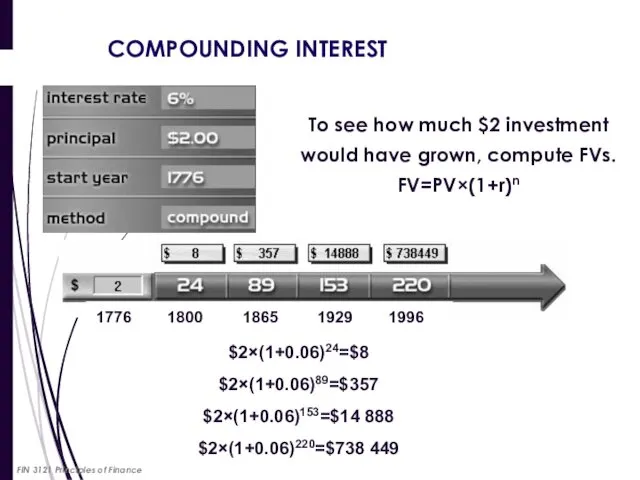

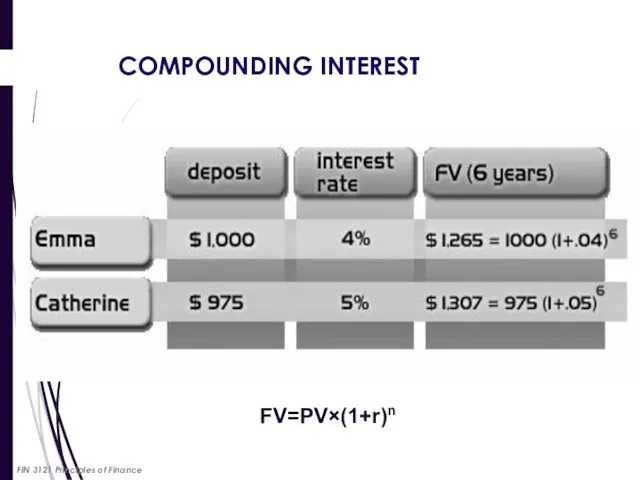

COMPOUNDING INTEREST

With Compounding Interest, the interest rate each year is applied

COMPOUNDING INTEREST

With Compounding Interest, the interest rate each year is applied

COMPOUNDING INTEREST

1776 1800 1865 1929 1996

To see how much $2

COMPOUNDING INTEREST

1776 1800 1865 1929 1996

To see how much $2

THE TIMELINE

A timeline is a linear representation of the timing of

THE TIMELINE

A timeline is a linear representation of the timing of

THE TIMELINE: EXAMPLE

Problem

Suppose you have a choice between receiving $5,000 today

THE TIMELINE: EXAMPLE

Problem

Suppose you have a choice between receiving $5,000 today

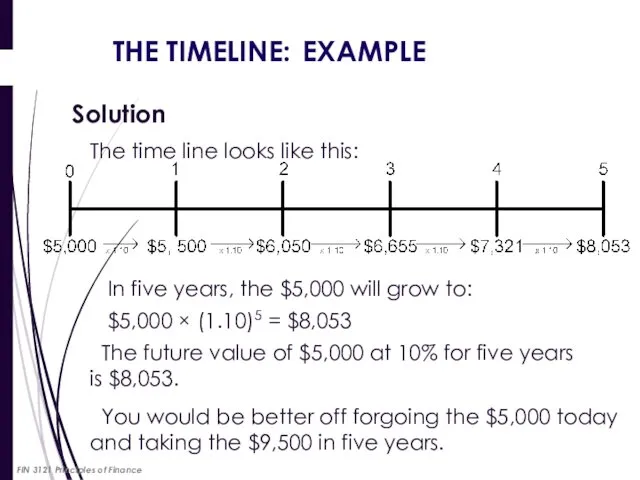

THE TIMELINE: EXAMPLE

Solution

The time line looks like this:

In five years,

THE TIMELINE: EXAMPLE

Solution

The time line looks like this:

In five years,

COMPOUNDING INTEREST

FV=PV×(1+r)n

FIN 3121 Principles of Finance

COMPOUNDING INTEREST

FV=PV×(1+r)n

FIN 3121 Principles of Finance

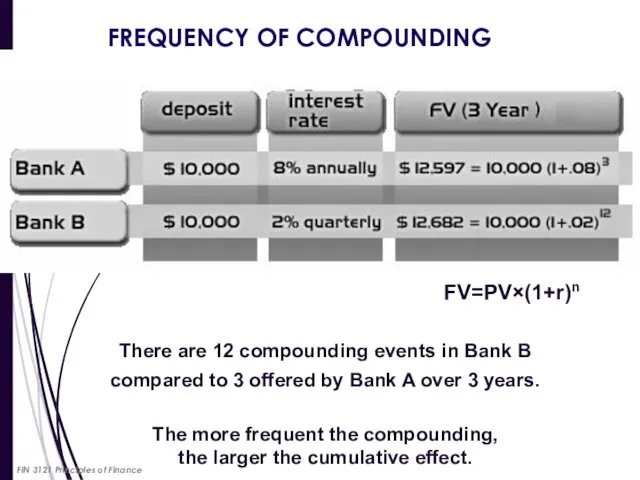

FREQUENCY OF COMPOUNDING

There are 12 compounding events in Bank B

compared

FREQUENCY OF COMPOUNDING

There are 12 compounding events in Bank B

compared

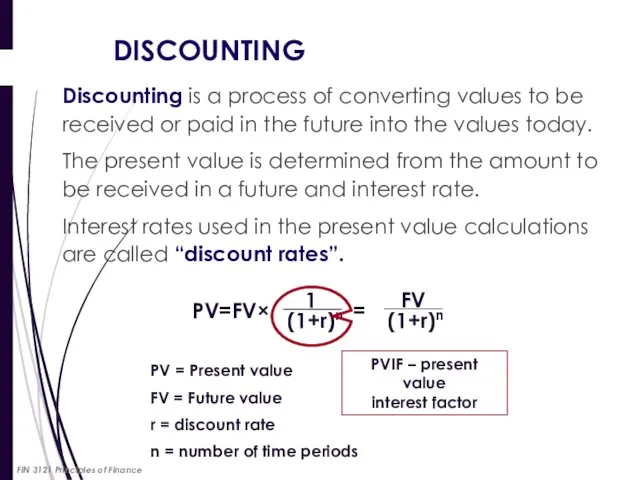

DISCOUNTING

Discounting is a process of converting values to be received or

DISCOUNTING

Discounting is a process of converting values to be received or

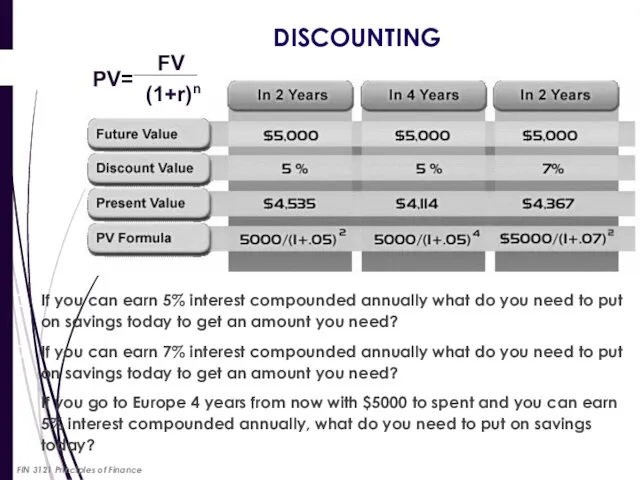

DISCOUNTING

If you can earn 5% interest compounded annually what do you

DISCOUNTING

If you can earn 5% interest compounded annually what do you

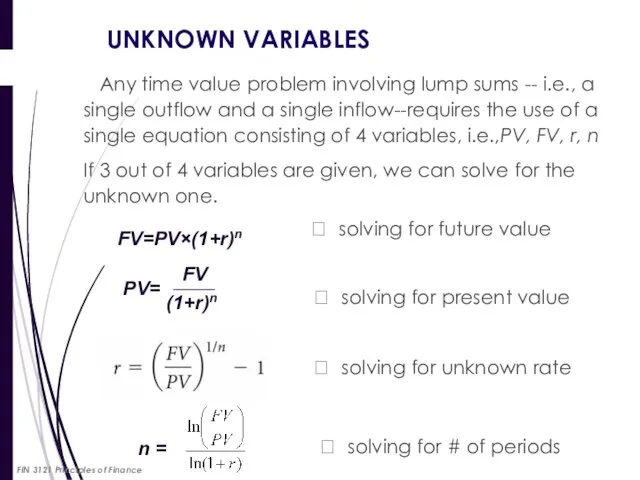

UNKNOWN VARIABLES

Any time value problem involving lump sums -- i.e.,

UNKNOWN VARIABLES

Any time value problem involving lump sums -- i.e.,

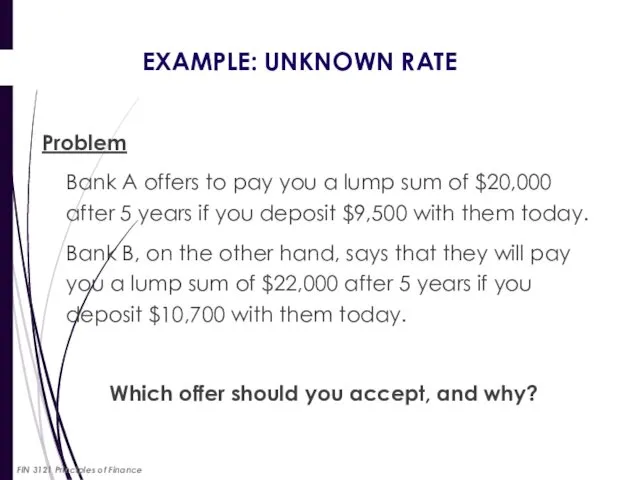

EXAMPLE: UNKNOWN RATE

Problem

Bank A offers to pay you a lump sum

EXAMPLE: UNKNOWN RATE

Problem

Bank A offers to pay you a lump sum

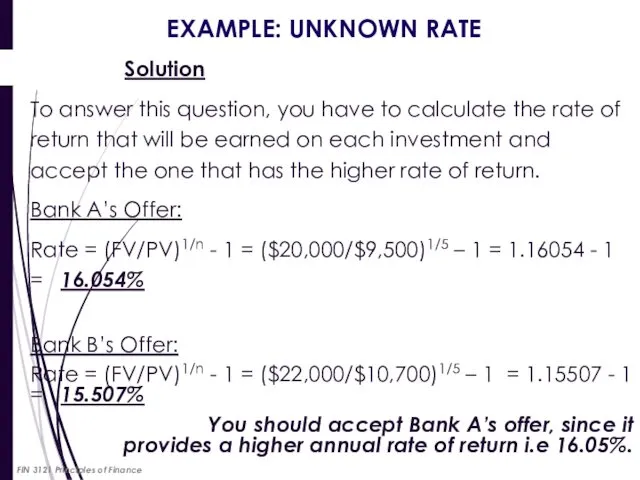

EXAMPLE: UNKNOWN RATE

Solution

To answer this question, you have to

EXAMPLE: UNKNOWN RATE

Solution

To answer this question, you have to

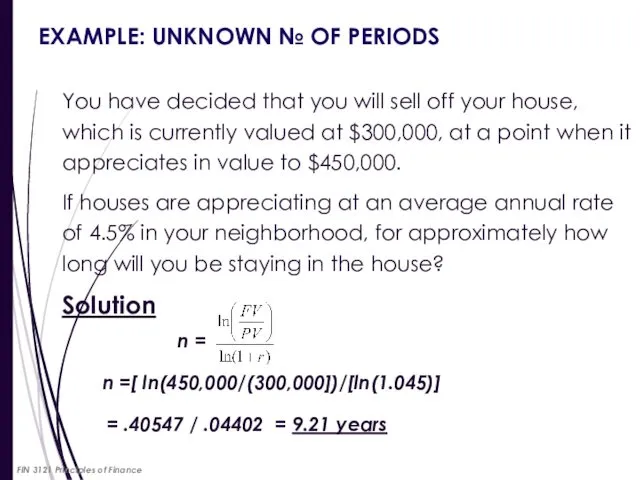

EXAMPLE: UNKNOWN № OF PERIODS

You have decided that you will sell

EXAMPLE: UNKNOWN № OF PERIODS

You have decided that you will sell

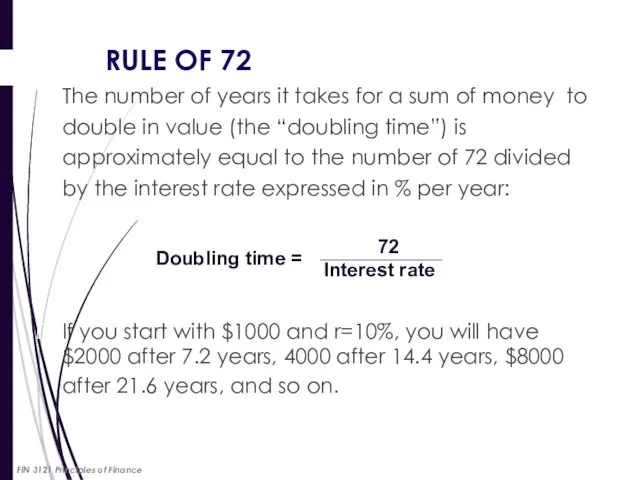

RULE OF 72

The number of years it takes for a sum

RULE OF 72

The number of years it takes for a sum

STREAM OF CASH FLOWS

FIN 3121 Principles of Finance

STREAM OF CASH FLOWS

FIN 3121 Principles of Finance

ONLY VALUES AT THE SAME POINT IN TIME

CAN BE COMPARED

ONLY VALUES AT THE SAME POINT IN TIME

CAN BE COMPARED

Valuing a Stream of Cash Flows

General formula for valuing a stream

Valuing a Stream of Cash Flows

General formula for valuing a stream

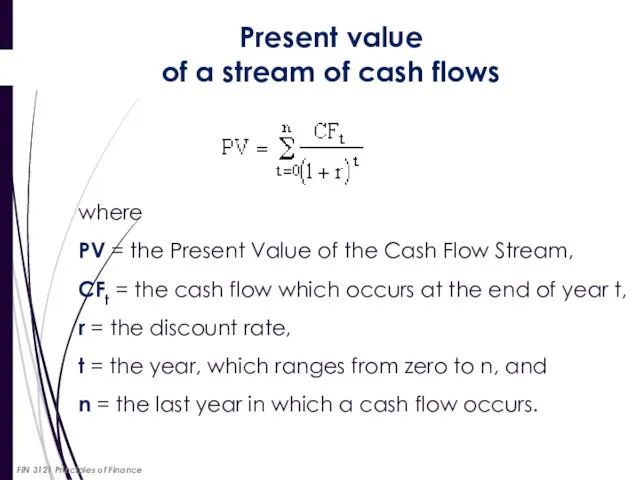

where

PV = the Present Value of the Cash Flow Stream,

where

PV = the Present Value of the Cash Flow Stream,

Find the Present Value of the following cash flow stream given

Find the Present Value of the following cash flow stream given

Future value

of a stream of cash flows

where

FVt =

Future value

of a stream of cash flows

where

FVt =

Find the Future Value at the end of year 4 of

Find the Future Value at the end of year 4 of

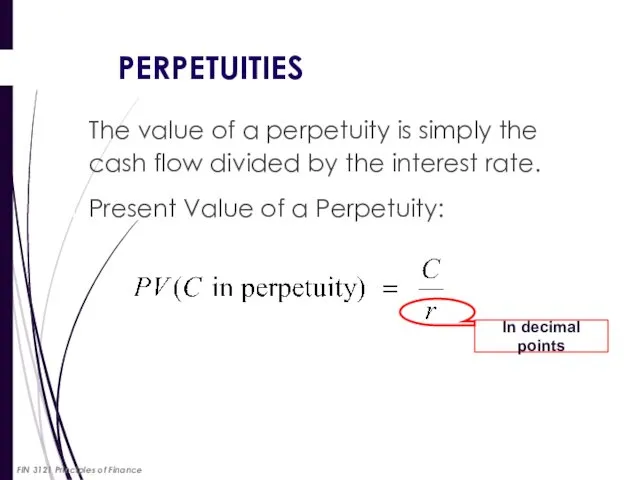

PERPETUITIES

When a constant cash flow will occur at regular intervals forever

PERPETUITIES

When a constant cash flow will occur at regular intervals forever

PERPETUITIES

The value of a perpetuity is simply the cash flow divided

PERPETUITIES

The value of a perpetuity is simply the cash flow divided

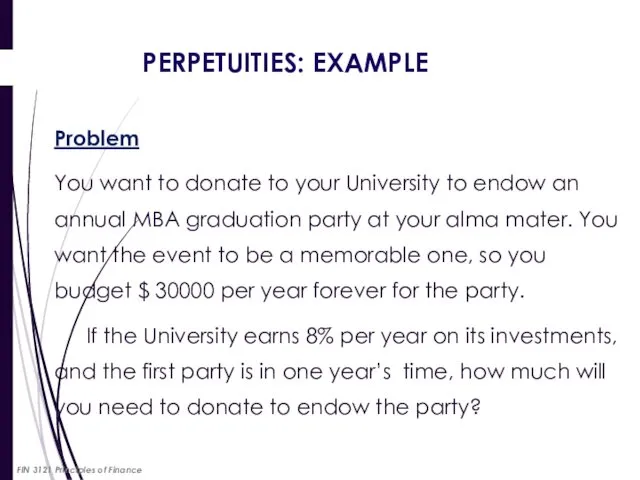

PERPETUITIES: EXAMPLE

Problem

You want to donate to your University to endow an

PERPETUITIES: EXAMPLE

Problem

You want to donate to your University to endow an

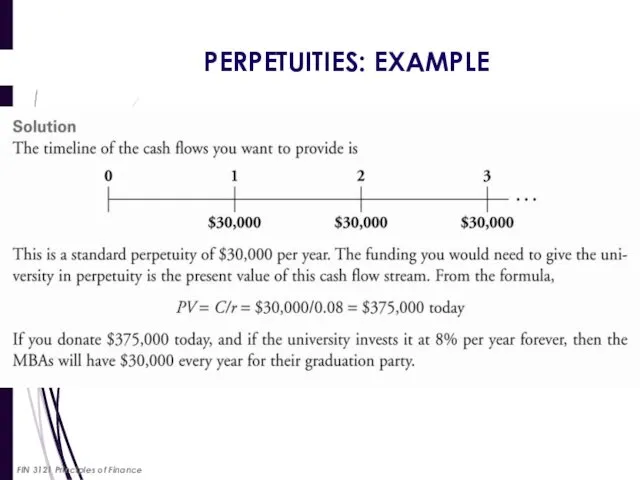

PERPETUITIES: EXAMPLE

FIN 3121 Principles of Finance

PERPETUITIES: EXAMPLE

FIN 3121 Principles of Finance

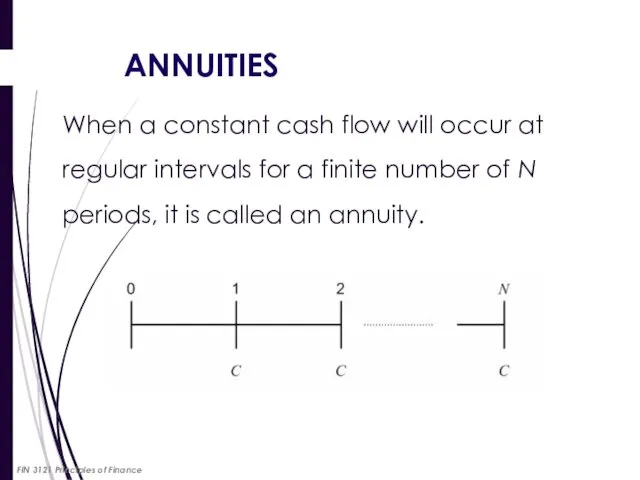

When a constant cash flow will occur at regular intervals for

When a constant cash flow will occur at regular intervals for

ANNUITIES

FIN 3121 Principles of Finance

ANNUITIES

FIN 3121 Principles of Finance

FUTURE VALUE INTEREST FACTOR

OF AN ANNUITY (FVIFA)

FVIFA =

FVIFA –

FUTURE VALUE INTEREST FACTOR

OF AN ANNUITY (FVIFA)

FVIFA =

FVIFA –

FUTURE VALUE OF

AN ORDINARY ANNUITY STREAM

Problem

Jill has been faithfully depositing

FUTURE VALUE OF

AN ORDINARY ANNUITY STREAM

Problem

Jill has been faithfully depositing

FUTURE VALUE OF

AN ORDINARY ANNUITY STREAM

Solution

Future Value of Payment One

FUTURE VALUE OF

AN ORDINARY ANNUITY STREAM

Solution

Future Value of Payment One

FUTURE VALUE OF

AN ORDINARY ANNUITY STREAM

FIN 3121 Principles of Finance

FUTURE VALUE OF

AN ORDINARY ANNUITY STREAM

FIN 3121 Principles of Finance

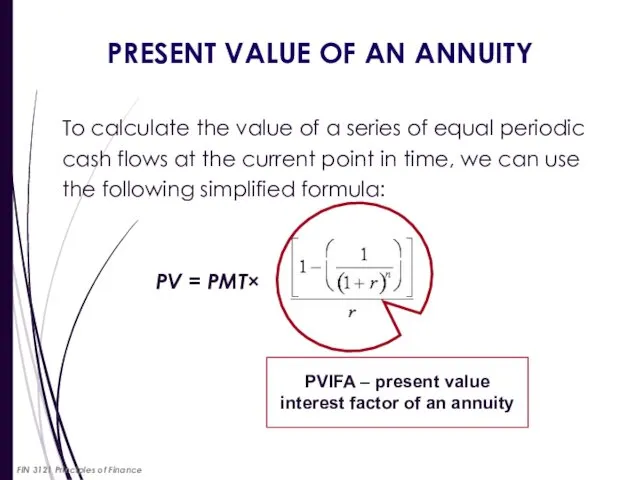

PRESENT VALUE OF AN ANNUITY

To calculate the value of a series

PRESENT VALUE OF AN ANNUITY

To calculate the value of a series

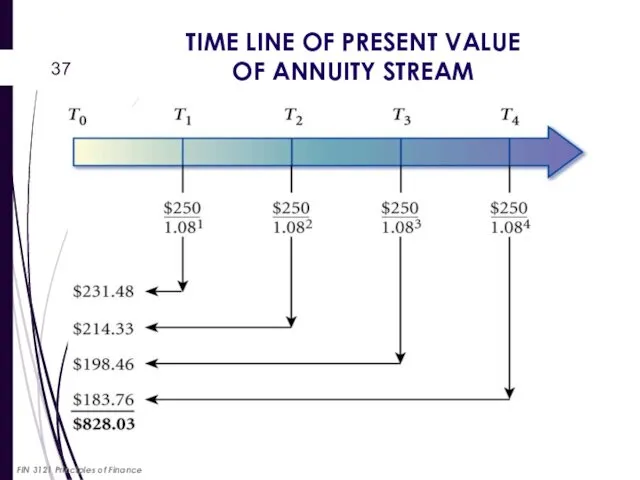

TIME LINE OF PRESENT VALUE

OF ANNUITY STREAM

FIN 3121 Principles of

TIME LINE OF PRESENT VALUE

OF ANNUITY STREAM

FIN 3121 Principles of

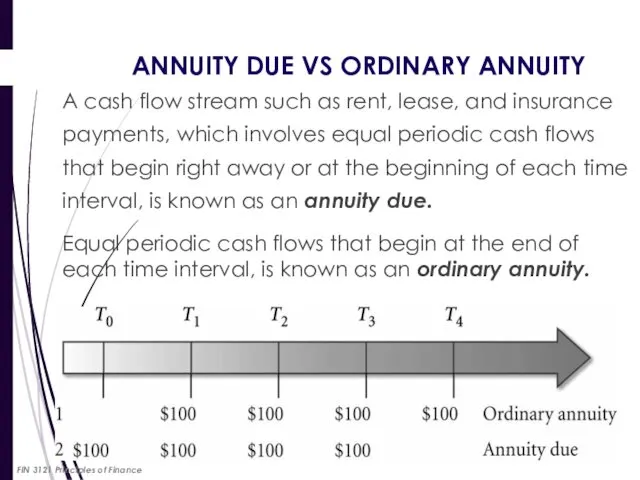

ANNUITY DUE VS ORDINARY ANNUITY

A cash flow stream such as rent,

ANNUITY DUE VS ORDINARY ANNUITY

A cash flow stream such as rent,

PV annuity due = PV ordinary annuity x (1+r)

FV annuity due

PV annuity due = PV ordinary annuity x (1+r)

FV annuity due

ANNUITY DUE VS ORDINARY ANNUITY

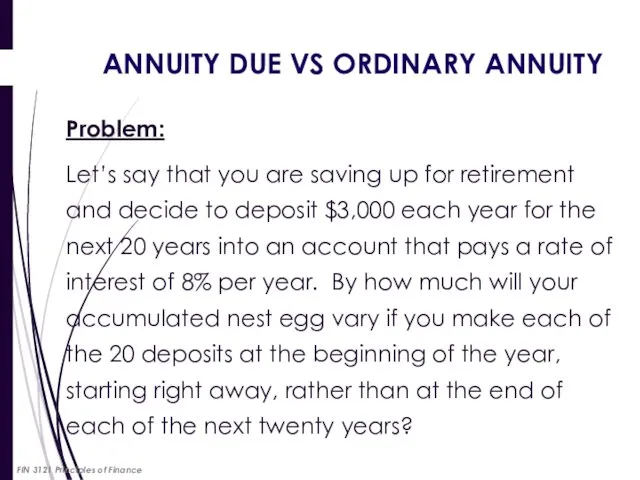

Problem:

Let’s say that you are saving up

ANNUITY DUE VS ORDINARY ANNUITY

Problem:

Let’s say that you are saving up

ANNUITY DUE VS ORDINARY ANNUITY

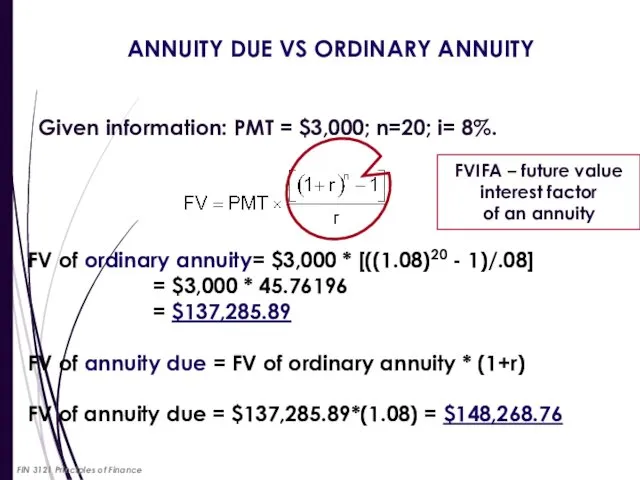

Given information: PMT = $3,000; n=20; i=

ANNUITY DUE VS ORDINARY ANNUITY

Given information: PMT = $3,000; n=20; i=

TYPES OF LOAN REPAYMENTS

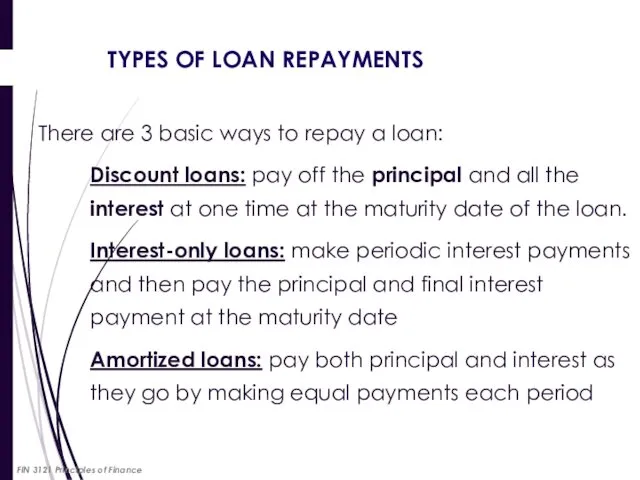

There are 3 basic ways to repay a

TYPES OF LOAN REPAYMENTS

There are 3 basic ways to repay a

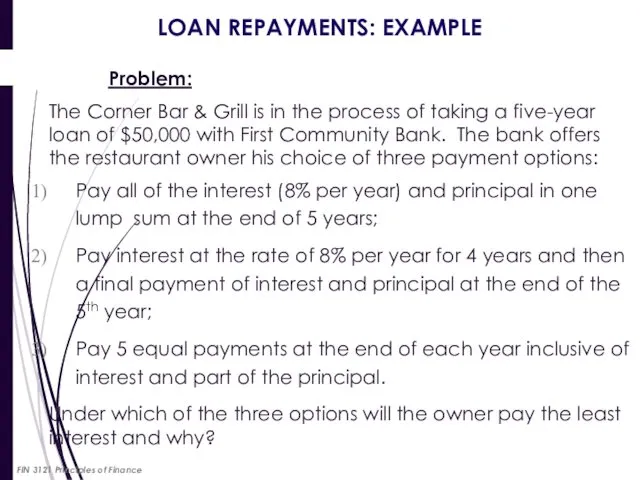

LOAN REPAYMENTS: EXAMPLE

Problem:

The Corner Bar & Grill is in the

LOAN REPAYMENTS: EXAMPLE

Problem:

The Corner Bar & Grill is in the

LOAN REPAYMENTS: EXAMPLE

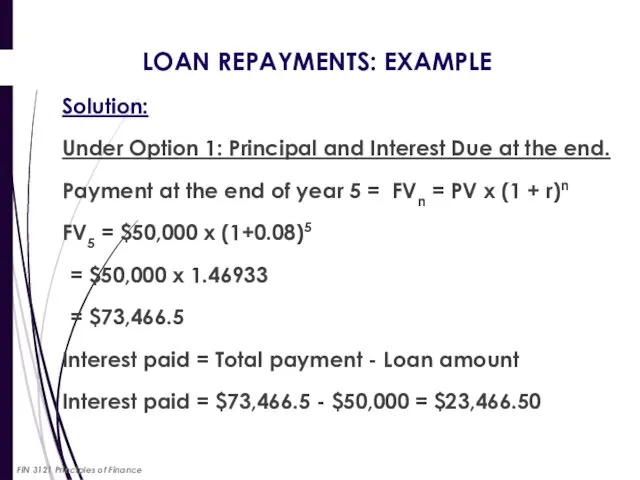

Solution:

Under Option 1: Principal and Interest Due at the

LOAN REPAYMENTS: EXAMPLE

Solution:

Under Option 1: Principal and Interest Due at the

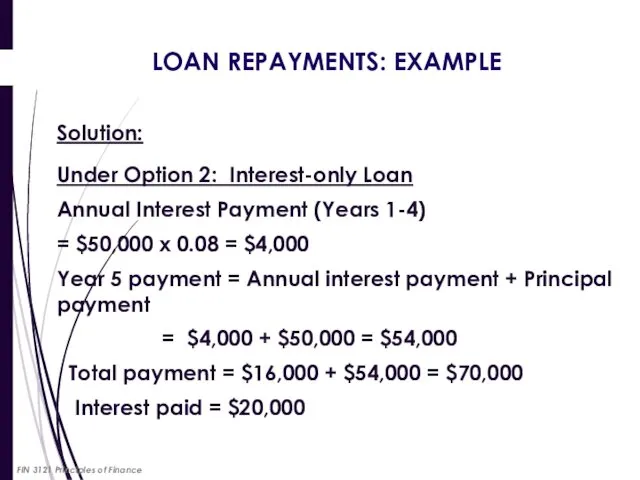

LOAN REPAYMENTS: EXAMPLE

Solution:

Under Option 2: Interest-only Loan

Annual Interest Payment (Years 1-4)

LOAN REPAYMENTS: EXAMPLE

Solution:

Under Option 2: Interest-only Loan

Annual Interest Payment (Years 1-4)

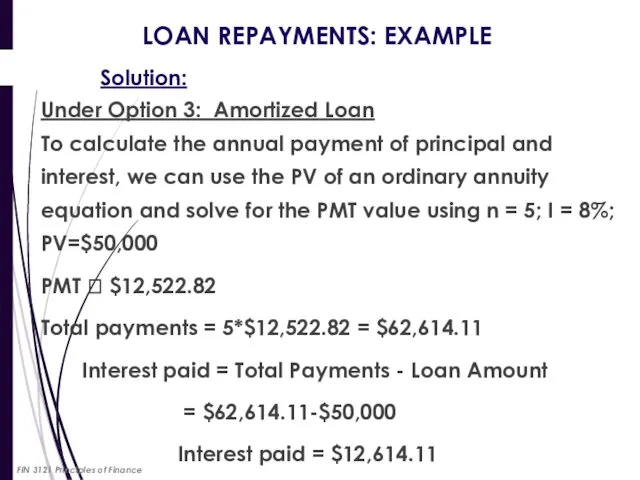

LOAN REPAYMENTS: EXAMPLE

Solution:

Under Option 3: Amortized Loan

To calculate the

LOAN REPAYMENTS: EXAMPLE

Solution:

Under Option 3: Amortized Loan

To calculate the

LOAN REPAYMENTS: EXAMPLE

Comparison of total payments and interest paid under each

LOAN REPAYMENTS: EXAMPLE

Comparison of total payments and interest paid under each

AMORTIZATION SCHEDULES

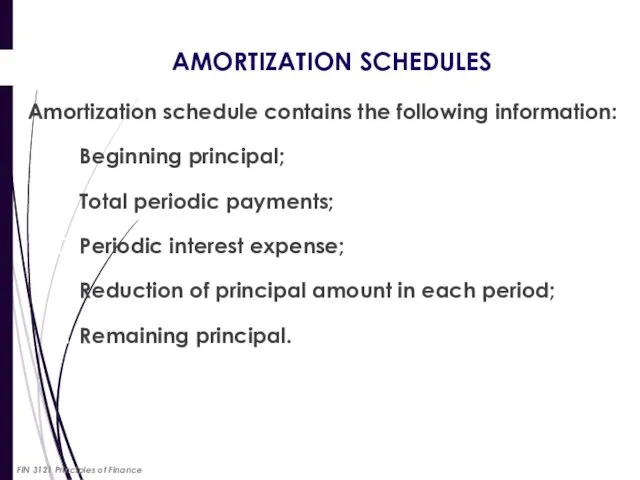

Amortization schedule contains the following information:

Beginning principal;

Total periodic payments;

AMORTIZATION SCHEDULES

Amortization schedule contains the following information:

Beginning principal;

Total periodic payments;

AMORTIZATION SCHEDULES

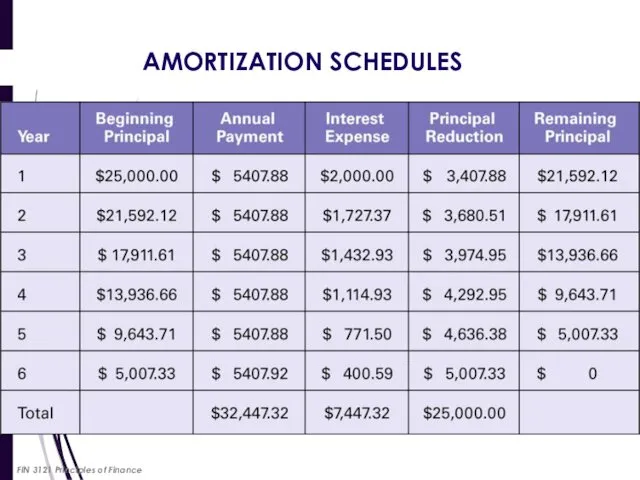

Problem

$ 25,000 loan being paid off at 8%

AMORTIZATION SCHEDULES

Problem

$ 25,000 loan being paid off at 8%

AMORTIZATION SCHEDULES

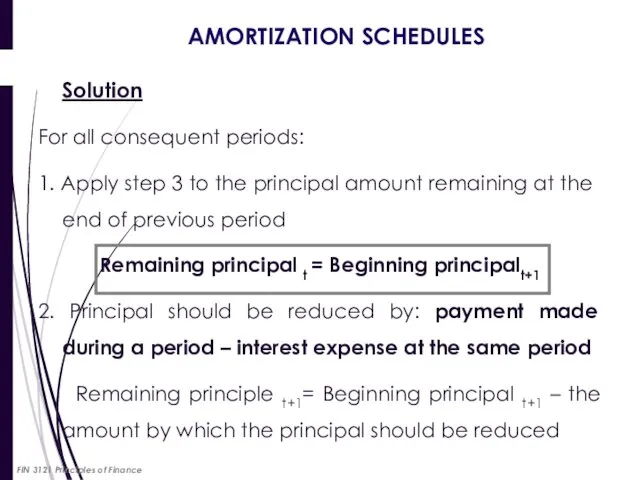

Solution

For all consequent periods:

1. Apply step 3 to the

AMORTIZATION SCHEDULES

Solution

For all consequent periods:

1. Apply step 3 to the

AMORTIZATION SCHEDULES

FIN 3121 Principles of Finance

AMORTIZATION SCHEDULES

FIN 3121 Principles of Finance

Фінансовий облік основних засобів. (Тема 2)

Фінансовий облік основних засобів. (Тема 2) Юный финансист. Доходы молодых граждан до восемнадцати лет и особенности их получения

Юный финансист. Доходы молодых граждан до восемнадцати лет и особенности их получения Основные теоретические концепции корпоративных финансов

Основные теоретические концепции корпоративных финансов Международная компания КриптоБанк

Международная компания КриптоБанк Концепция межбюджетных отношений и организации бюджетного процесса в субъектах РФ и муниципальных образованиях

Концепция межбюджетных отношений и организации бюджетного процесса в субъектах РФ и муниципальных образованиях Особенности конкурсного финансирования инновационных проектов

Особенности конкурсного финансирования инновационных проектов Фондовая биржа. Часть 1

Фондовая биржа. Часть 1 Бюджет семьи

Бюджет семьи Тема 2.1. Налог на добавленную стоимость

Тема 2.1. Налог на добавленную стоимость Деятельность коммерческого банка на рынке межбанковского кредитования на примере Сбербанка России

Деятельность коммерческого банка на рынке межбанковского кредитования на примере Сбербанка России Як виник фінансовий облік. Фінансова звітність компанії

Як виник фінансовий облік. Фінансова звітність компанії Услуги аутсорсинга бухгалтерии

Услуги аутсорсинга бухгалтерии Совершенствоание организации сбытовой деятельности предприятия ОАО Агрокомбинат Южный

Совершенствоание организации сбытовой деятельности предприятия ОАО Агрокомбинат Южный Себестоимость гостиничного предприятия

Себестоимость гостиничного предприятия ВКР: Учет расчетных отношений с поставщиками и подрядчиками

ВКР: Учет расчетных отношений с поставщиками и подрядчиками Тариф инвестиционный

Тариф инвестиционный Машина в кредит. Программа Ethtrade

Машина в кредит. Программа Ethtrade Необычные налоги Соединённых Штатов Америки

Необычные налоги Соединённых Штатов Америки Разработка технического предложения локально - вычислительной сети центра тестирования ГИБДД

Разработка технического предложения локально - вычислительной сети центра тестирования ГИБДД Соглашение о ценообразовании в отношении консультационных услуг

Соглашение о ценообразовании в отношении консультационных услуг Бизнес под ключ

Бизнес под ключ Счета бухгалтерского учета по структуре и назначению

Счета бухгалтерского учета по структуре и назначению Основы финансирования проектов. Способы и источники финансирования

Основы финансирования проектов. Способы и источники финансирования Центробанк выпустил посвященные медикам монеты

Центробанк выпустил посвященные медикам монеты Оценка аудиторского риска

Оценка аудиторского риска Кредитная и банковская системы

Кредитная и банковская системы Открытие и ведение расчетного счета

Открытие и ведение расчетного счета Основные новации Бюджетного кодекса Российской Федерации по казначейскому сопровождению и бюджетному мониторингу

Основные новации Бюджетного кодекса Российской Федерации по казначейскому сопровождению и бюджетному мониторингу