- Purpose of the capital market (lecture 11)

Содержание

- 2. Lecture 11. Capital Markets Murodullo Bazarov m.bazarov@wiut.uz ATB205 office hours: Tues 11:00-13:00

- 3. MEQ & RYL

- 4. Lecture Outline Purpose of the Capital Market Capital Market Participants Capital Market Trading Types of Bonds

- 5. Purpose of the Capital Market Original maturity is greater than one year, typically for long-term financing

- 6. Capital Market Participants Primary issuers of securities: Federal and local governments: debt issuers Corporations: equity and

- 7. Capital Market Trading 1. Primary market for initial sale (IPO) 2. Secondary market Over-the-counter Organized exchanges

- 8. Types of Bonds Bonds are securities that represent debt owed by the issuer to the investor,

- 9. Treasury Notes and Bonds The U.S. Treasury issues notes and bonds to finance its operations. The

- 10. Treasury Bond Interest Rates No default risk since the Treasury can print money to payoff the

- 11. Money Market Instruments: Treasury Bills

- 12. Municipal Bonds Issued by local, county, and state governments Used to finance public interest projects Tax-free

- 13. Municipal Bonds Suppose the rate on a corporate bond is 5% and the rate on a

- 14. Municipal Bonds Two types General obligation bonds Revenue bonds NOT default-free (e.g., Orange County California) Defaults

- 15. Municipal Bonds: Comparing Revenue and General Obligation Bonds Issuance of Revenue and General Obligation Bonds, 1984–2012

- 16. Corporate Bonds Typically have a face value of $1,000, although some have a face value of

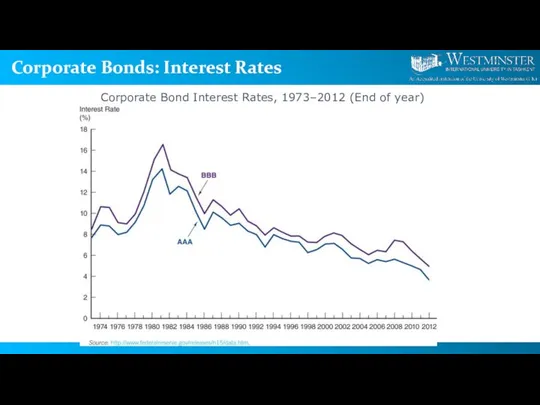

- 17. Corporate Bonds: Interest Rates Corporate Bond Interest Rates, 1973–2012 (End of year)

- 18. Characteristics of Corporate Bonds Registered Bonds Replaced “bearer” bonds Internal revenue service (IRS) can track interest

- 19. Characteristics of Corporate Bonds Secured Bonds Mortgage bonds Equipment trust certificates Unsecured Bonds Debentures Subordinated debentures

- 20. Financial Guarantees for Bonds Some debt issuers purchase financial guarantees to lower the risk of their

- 21. Investing in Bonds Bonds are the most popular alternative to stocks for long-term investing. Even though

- 22. Investing in Bonds Bonds and Stocks Issued, 1983–2012

- 23. Investing in Stocks Represents ownership in a firm Earn a return in two ways Price of

- 24. Investing in Stocks: How Stocks are Sold Organized exchanges NYSE is best known, with daily volume

- 25. Investing in Stocks: Organized vs. OTC Organized exchanges (e.g., NYSE) Auction markets with floor specialists 25%

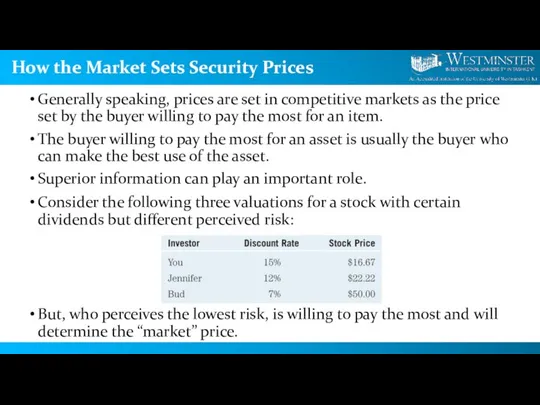

- 26. How the Market Sets Security Prices Generally speaking, prices are set in competitive markets as the

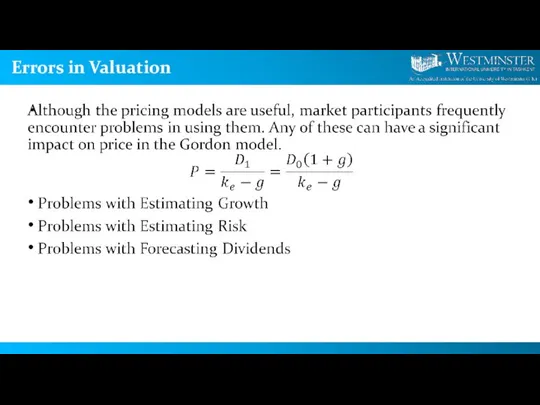

- 27. Errors in Valuation

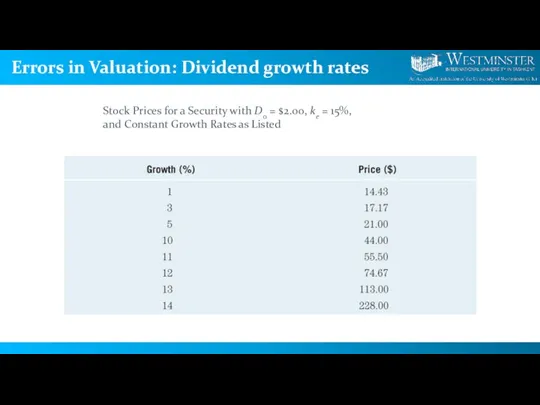

- 28. Errors in Valuation: Dividend growth rates Stock Prices for a Security with D0 = $2.00, ke

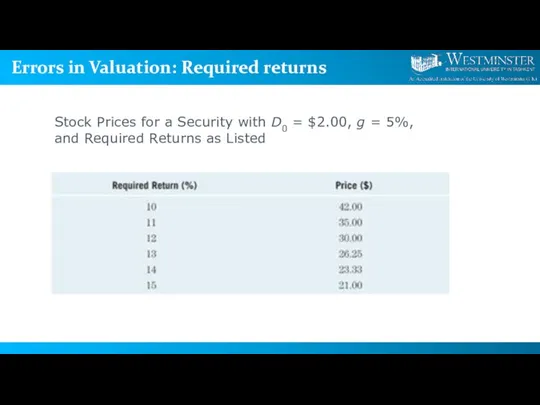

- 29. Errors in Valuation: Required returns Stock Prices for a Security with D0 = $2.00, g =

- 30. Errors in Valuation Security valuation is not an exact science! Considering different growth rates, required rates,

- 31. Case: The 2007–2009 Financial Crisis and the Stock Market The financial crisis, which started in August

- 32. Case: 9/11, Enron and the Market Both 9/11 and the Enron scandal were events in 2001.

- 34. Скачать презентацию

Lecture 11. Capital Markets

Murodullo Bazarov

m.bazarov@wiut.uz

ATB205

office hours: Tues 11:00-13:00

Lecture 11. Capital Markets

Murodullo Bazarov

m.bazarov@wiut.uz

ATB205

office hours: Tues 11:00-13:00

MEQ & RYL

MEQ & RYL

Lecture Outline

Purpose of the Capital Market

Capital Market Participants

Capital Market Trading

Types

Lecture Outline

Purpose of the Capital Market

Capital Market Participants

Capital Market Trading

Types

Purpose of the Capital Market

Original maturity is greater than one year,

Purpose of the Capital Market

Original maturity is greater than one year,

Capital Market Participants

Primary issuers of securities:

Federal and local governments: debt issuers

Corporations:

Capital Market Participants

Primary issuers of securities:

Federal and local governments: debt issuers

Corporations:

Capital Market Trading

1. Primary market for initial sale (IPO)

2. Secondary market

Over-the-counter

Organized

Capital Market Trading

1. Primary market for initial sale (IPO)

2. Secondary market

Over-the-counter

Organized

Types of Bonds

Bonds are securities that represent debt owed by the

Types of Bonds

Bonds are securities that represent debt owed by the

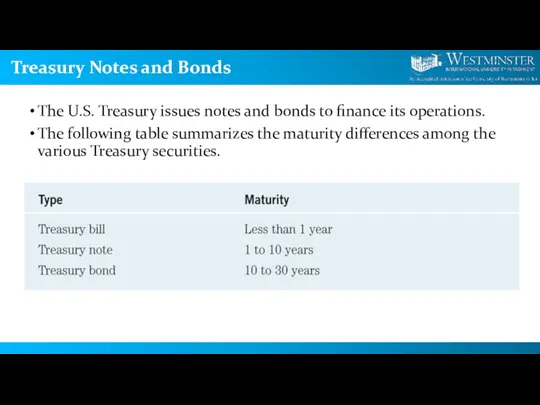

Treasury Notes and Bonds

The U.S. Treasury issues notes and bonds to

Treasury Notes and Bonds

The U.S. Treasury issues notes and bonds to

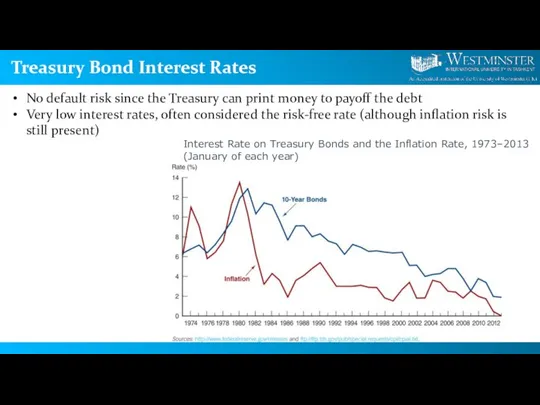

Treasury Bond Interest Rates

No default risk since the Treasury can print

Treasury Bond Interest Rates

No default risk since the Treasury can print

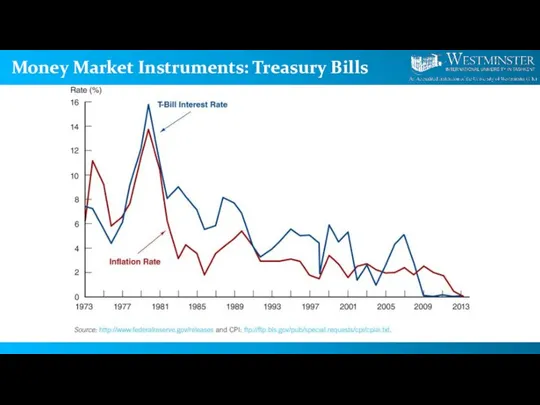

Money Market Instruments: Treasury Bills

Money Market Instruments: Treasury Bills

Municipal Bonds

Issued by local, county, and state governments

Used to finance public

Municipal Bonds

Issued by local, county, and state governments

Used to finance public

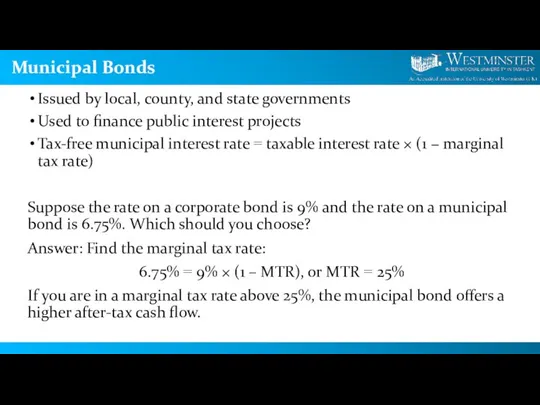

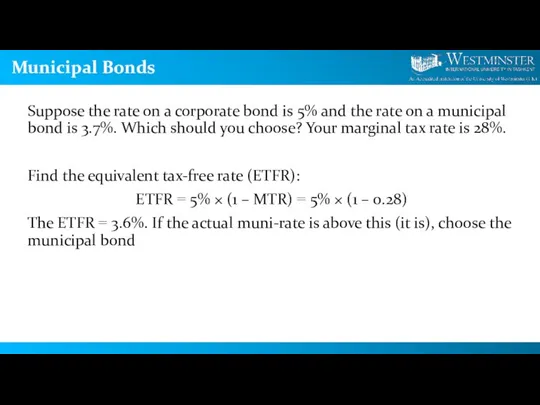

Municipal Bonds

Suppose the rate on a corporate bond is 5% and

Municipal Bonds

Suppose the rate on a corporate bond is 5% and

Municipal Bonds

Two types

General obligation bonds

Revenue bonds

NOT default-free (e.g., Orange County California)

Defaults

Municipal Bonds

Two types

General obligation bonds

Revenue bonds

NOT default-free (e.g., Orange County California)

Defaults

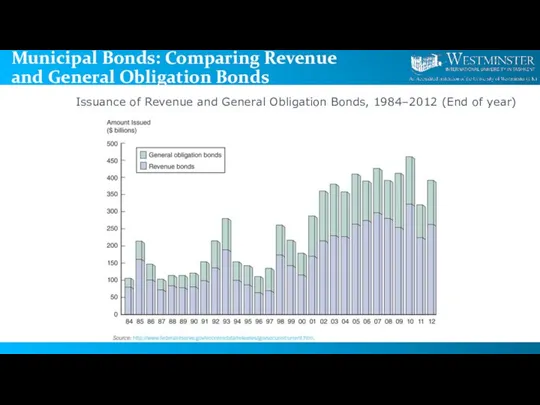

Municipal Bonds: Comparing Revenue and General Obligation Bonds

Issuance of Revenue and

Municipal Bonds: Comparing Revenue and General Obligation Bonds

Issuance of Revenue and

Corporate Bonds

Typically have a face value of $1,000, although some have

Corporate Bonds

Typically have a face value of $1,000, although some have

Corporate Bonds: Interest Rates

Corporate Bond Interest Rates, 1973–2012 (End of year)

Corporate Bonds: Interest Rates

Corporate Bond Interest Rates, 1973–2012 (End of year)

Characteristics of Corporate Bonds

Registered Bonds

Replaced “bearer” bonds

Internal revenue service (IRS) can

Characteristics of Corporate Bonds

Registered Bonds

Replaced “bearer” bonds

Internal revenue service (IRS) can

Characteristics of Corporate Bonds

Secured Bonds

Mortgage bonds

Equipment trust certificates

Unsecured Bonds

Debentures

Subordinated debentures

Variable-rate bonds

Junk

Characteristics of Corporate Bonds

Secured Bonds

Mortgage bonds

Equipment trust certificates

Unsecured Bonds

Debentures

Subordinated debentures

Variable-rate bonds

Junk

Financial Guarantees for Bonds

Some debt issuers purchase financial guarantees to lower

Financial Guarantees for Bonds

Some debt issuers purchase financial guarantees to lower

Investing in Bonds

Bonds are the most popular alternative to stocks for

Investing in Bonds

Bonds are the most popular alternative to stocks for

Investing in Bonds

Bonds and Stocks Issued, 1983–2012

Investing in Bonds

Bonds and Stocks Issued, 1983–2012

Investing in Stocks

Represents ownership

in a firm

Earn a return in

Investing in Stocks

Represents ownership

in a firm

Earn a return in

Investing in Stocks: How Stocks are Sold

Organized exchanges

NYSE is best

Investing in Stocks: How Stocks are Sold

Organized exchanges

NYSE is best

Investing in Stocks: Organized vs. OTC

Organized exchanges (e.g., NYSE)

Auction markets with

Investing in Stocks: Organized vs. OTC

Organized exchanges (e.g., NYSE)

Auction markets with

How the Market Sets Security Prices

Generally speaking, prices are set in

How the Market Sets Security Prices

Generally speaking, prices are set in

Errors in Valuation

Errors in Valuation

Errors in Valuation: Dividend growth rates

Stock Prices for a Security with

Errors in Valuation: Dividend growth rates

Stock Prices for a Security with

Errors in Valuation: Required returns

Stock Prices for a Security with D0

Errors in Valuation: Required returns

Stock Prices for a Security with D0

Errors in Valuation

Security valuation is not an exact science!

Considering different growth

Errors in Valuation

Security valuation is not an exact science!

Considering different growth

Case: The 2007–2009 Financial Crisis and the Stock Market

The financial crisis,

Case: The 2007–2009 Financial Crisis and the Stock Market

The financial crisis,

Case: 9/11, Enron and the Market

Both 9/11 and the Enron scandal

Case: 9/11, Enron and the Market

Both 9/11 and the Enron scandal

Оплата праці

Оплата праці Виды банковских счетов

Виды банковских счетов Производственные ресурсы: основной капитал

Производственные ресурсы: основной капитал Рынок труда и социально-трудовые отношения

Рынок труда и социально-трудовые отношения Оборотные средства предприятия

Оборотные средства предприятия Основы финансовых вычислений. Сложные проценты

Основы финансовых вычислений. Сложные проценты VIII Уральский инвестиционный форум г. Челябинск

VIII Уральский инвестиционный форум г. Челябинск Семестровая работа по дисциплине Основы экономики и финансовой грамотности

Семестровая работа по дисциплине Основы экономики и финансовой грамотности Стохастические модели динамического программирования

Стохастические модели динамического программирования Prosperity club. Живи и процветай

Prosperity club. Живи и процветай Перший Український Міжнародний Банк (ПУМБ)

Перший Український Міжнародний Банк (ПУМБ) Предпринимательская деятельность и управление финансами

Предпринимательская деятельность и управление финансами Income

Income Бюджет абинского городского поселения на 2021 год и плановый период 2022-2023 годов

Бюджет абинского городского поселения на 2021 год и плановый период 2022-2023 годов Otvety na chastye voprosy po razdelu zarabotnoj platy v programme 1SBuhgalteriya 8 dlya Kazahstana. IPN, vychety po IPN i mnogoe drugoe

Otvety na chastye voprosy po razdelu zarabotnoj platy v programme 1SBuhgalteriya 8 dlya Kazahstana. IPN, vychety po IPN i mnogoe drugoe Промышленность и инвестиции

Промышленность и инвестиции Финансовый контроль

Финансовый контроль Особенности правового регулирования труда самозанятых граждан

Особенности правового регулирования труда самозанятых граждан Налоговый вычет в 2020 году

Налоговый вычет в 2020 году Домовой классический : описание продукта, основные понятия, тарифы. Лекция 3

Домовой классический : описание продукта, основные понятия, тарифы. Лекция 3 Лекция 21 Модуль 5

Лекция 21 Модуль 5 Теоретические концепции корпоративных финансов

Теоретические концепции корпоративных финансов Лекция 3-4. Бухгалтерские информационные системы (БУИС)

Лекция 3-4. Бухгалтерские информационные системы (БУИС) Деньги и банки

Деньги и банки Ценные бумаги: как и где их покупать и продавать. Фондовый рынок как источник финансовых ресурсов для предприятий (IPO, SPO)

Ценные бумаги: как и где их покупать и продавать. Фондовый рынок как источник финансовых ресурсов для предприятий (IPO, SPO) Самые необычные денежные купюры

Самые необычные денежные купюры Облік в оподаткуванні, його зміст та організація на підприємстві

Облік в оподаткуванні, його зміст та організація на підприємстві Экономические основы производства. Прикладные понятия экономики

Экономические основы производства. Прикладные понятия экономики