- Tax and taxation. Corporate income tax

Содержание

- 2. What is the object of the corporate income tax? Taxable income Income taxed at source of

- 3. How is taxable income? Taxable income is defined as the difference between the adjusted gross annual

- 4. The costs of the taxpayer related to obtaining the total annual income are deductible in determining

- 5. Deductions made by the taxpayer in the presence of the documents confirming the expenses incurred in

- 6. What are the stakes? 10% - applies to the taxpayer's taxable income for which the land

- 7. What set the tax period? The period for which the calculated CPN - calendar year (from

- 8. What are the deadlines for the declaration? Declaration CIT consists of a Declaration and its annexes

- 9. What are the terms of payment of the tax? Taxpayers pay the corporate income tax by

- 10. for the calculation of the period before the submission of the declaration by the CPN from

- 12. Скачать презентацию

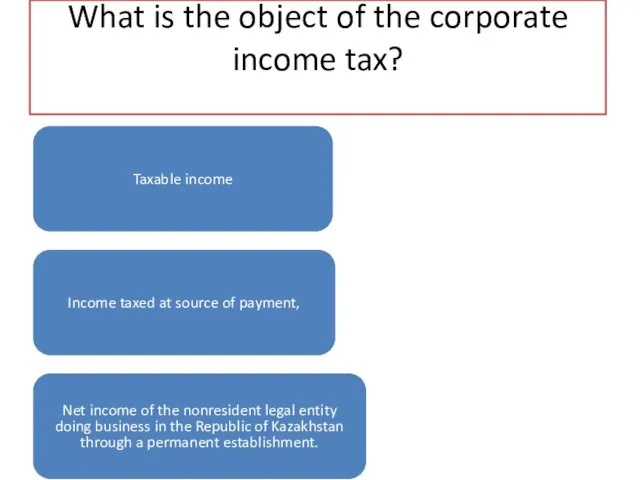

What is the object of the corporate income tax?

Taxable income

Income taxed

What is the object of the corporate income tax?

Taxable income

Income taxed

How is taxable income?

Taxable income is defined as the difference between

How is taxable income?

Taxable income is defined as the difference between

The costs of the taxpayer related to obtaining the total annual

The costs of the taxpayer related to obtaining the total annual

Deductions made by the taxpayer in the presence of the documents

Deductions made by the taxpayer in the presence of the documents

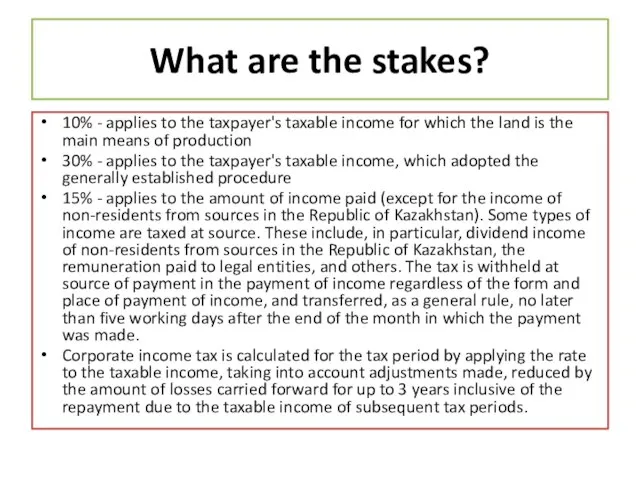

What are the stakes?

10% - applies to the taxpayer's taxable income

What are the stakes?

10% - applies to the taxpayer's taxable income

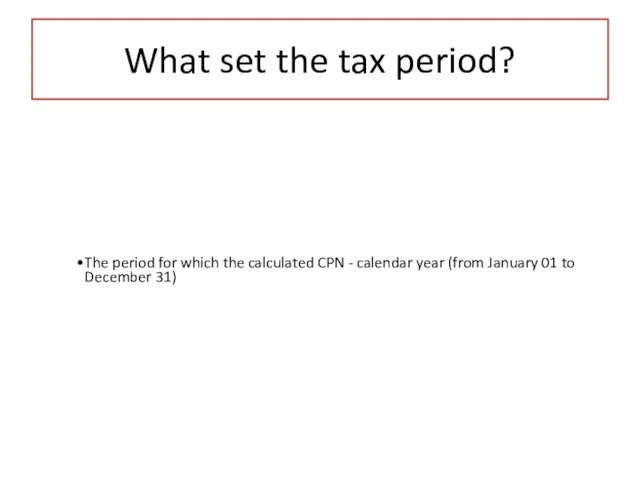

What set the tax period?

The period for which the calculated CPN

What set the tax period?

The period for which the calculated CPN

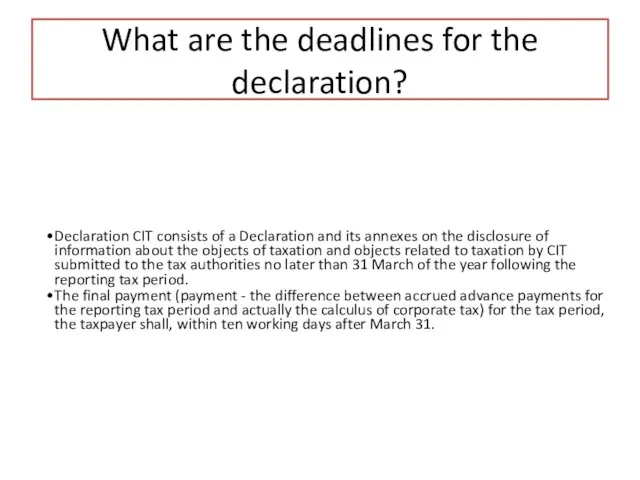

What are the deadlines for the declaration?

Declaration CIT consists of a

What are the deadlines for the declaration?

Declaration CIT consists of a

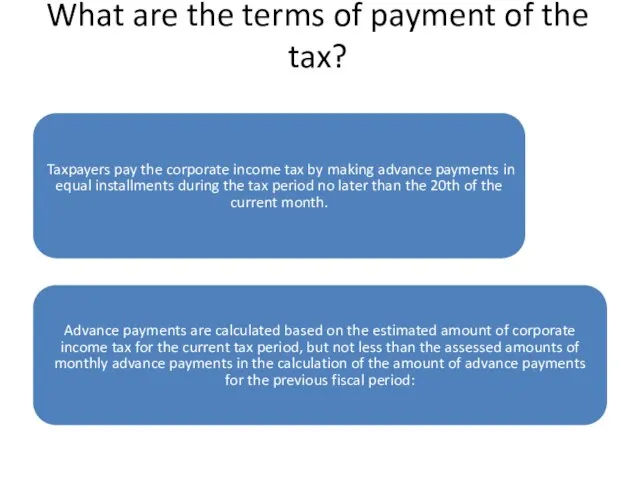

What are the terms of payment of the tax?

Taxpayers pay the

What are the terms of payment of the tax?

Taxpayers pay the

for the calculation of the period before the submission of the

for the calculation of the period before the submission of the

Роль Международного Валютного Фонда (МВФ) в международных денежных отношениях

Роль Международного Валютного Фонда (МВФ) в международных денежных отношениях ВКР: Анализ ликвидности и платежеспособности коммерческой организации

ВКР: Анализ ликвидности и платежеспособности коммерческой организации Сравнение налогов Республики Казахстан и Индии

Сравнение налогов Республики Казахстан и Индии Формы государственной поддержки инноваций в России

Формы государственной поддержки инноваций в России 1. Дополнительные меры финансовой поддержки работодателей Пермского края на 2021 год

1. Дополнительные меры финансовой поддержки работодателей Пермского края на 2021 год Income

Income Муниципальные ценные бумаги, их характеристика

Муниципальные ценные бумаги, их характеристика Бюджет для граждан исполнение местного бюджета за 2020 год

Бюджет для граждан исполнение местного бюджета за 2020 год Грантовая поддержка, как современный механизм развития территорий

Грантовая поддержка, как современный механизм развития территорий Постоянные и переменные затраты. Издержки производства

Постоянные и переменные затраты. Издержки производства Аналіз стану фінансового забезпечення судів

Аналіз стану фінансового забезпечення судів Внебюджетные фонды

Внебюджетные фонды Совершенствование системы ценообразования в строительстве

Совершенствование системы ценообразования в строительстве Бюджет государства и семьи

Бюджет государства и семьи Страховые взносы в ПФР, ФСС, ФФОМС и налог на доходы. Практическое занятие 4

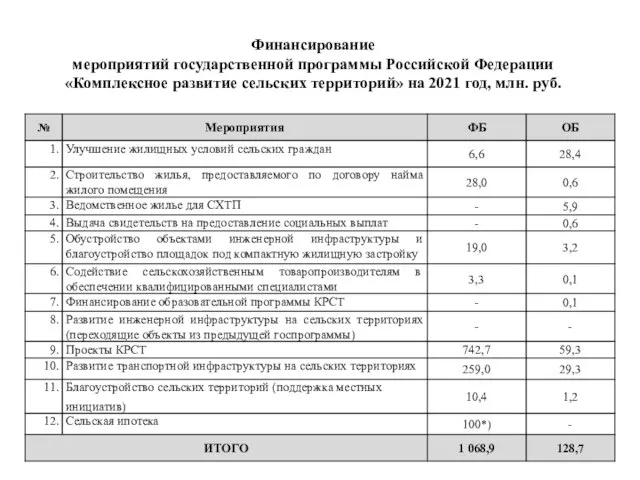

Страховые взносы в ПФР, ФСС, ФФОМС и налог на доходы. Практическое занятие 4 Финансирование мероприятий государственной программы Российской Федерации Комплексное развитие сельских территорий на 2021

Финансирование мероприятий государственной программы Российской Федерации Комплексное развитие сельских территорий на 2021 Ямайская валютная система

Ямайская валютная система Организация процедуры оценки ресурсного потенциала предприятия

Организация процедуры оценки ресурсного потенциала предприятия Типы организации и построения финансовых структур российских компаний

Типы организации и построения финансовых структур российских компаний Олимпиады и конкурсы как эффективный способ формирования финансовой грамотности школьников

Олимпиады и конкурсы как эффективный способ формирования финансовой грамотности школьников Поняття та функції податкового механізму

Поняття та функції податкового механізму Эндогенные и экзогенные деньги

Эндогенные и экзогенные деньги Организация оплаты труда в сельском хозяйстве

Организация оплаты труда в сельском хозяйстве Технологии передачи данных. Реестр ККТ: новые и старые модели

Технологии передачи данных. Реестр ККТ: новые и старые модели Риск банкротства организации и методы его предотвращения предприятия ОАО Дорисс

Риск банкротства организации и методы его предотвращения предприятия ОАО Дорисс Рентна плата

Рентна плата Концепция планирования выездных налоговых проверок

Концепция планирования выездных налоговых проверок Қазақстан Республткасының аудиториялық қызметін нормативті реттейтін жүйе

Қазақстан Республткасының аудиториялық қызметін нормативті реттейтін жүйе