- Inventories and the Cost of Goods Sold

Содержание

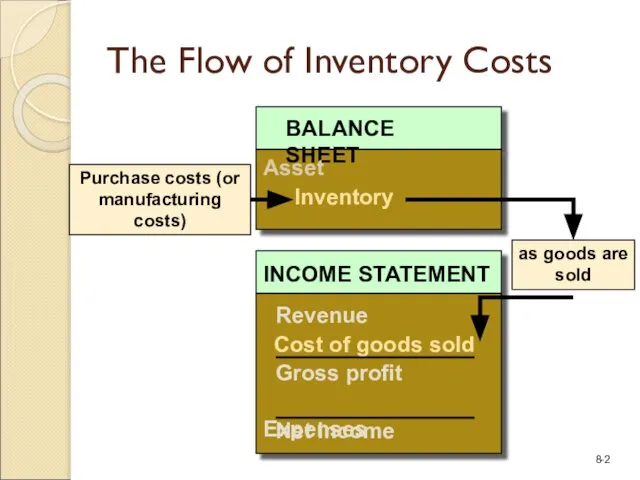

- 2. as goods are sold The Flow of Inventory Costs

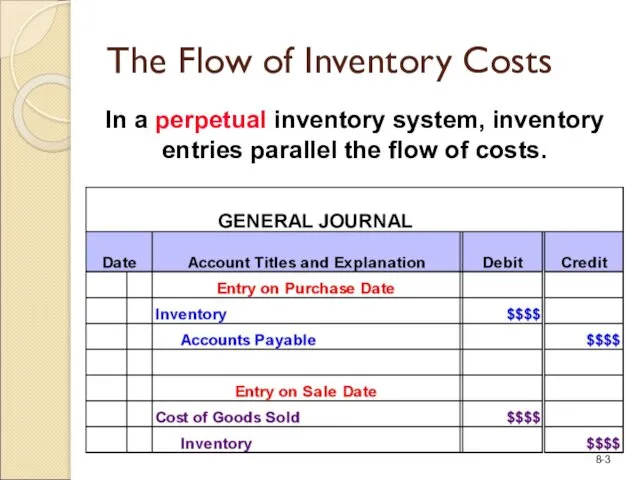

- 3. In a perpetual inventory system, inventory entries parallel the flow of costs. The Flow of Inventory

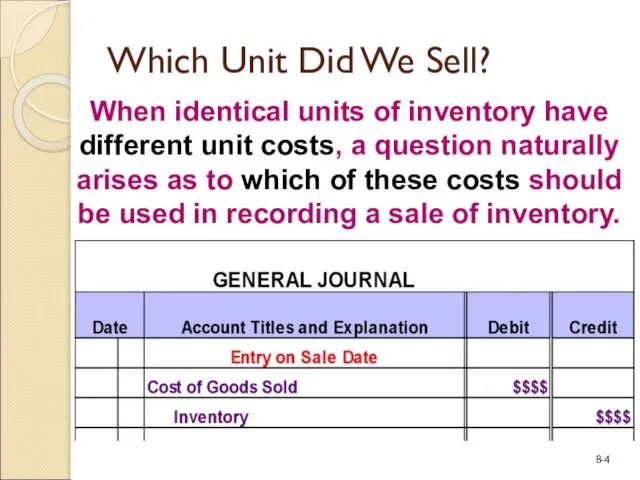

- 4. When identical units of inventory have different unit costs, a question naturally arises as to which

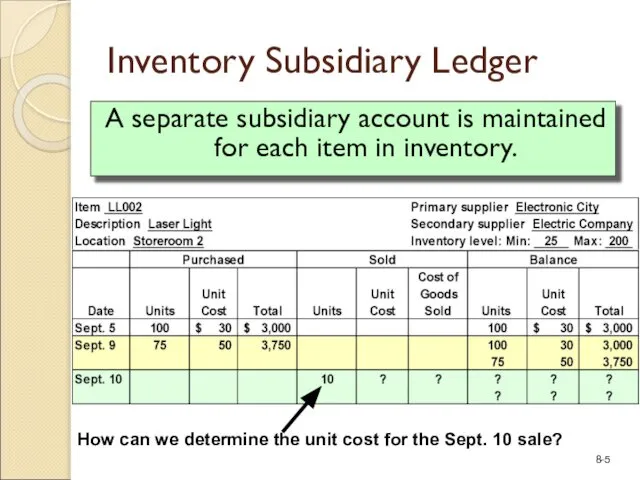

- 5. Inventory Subsidiary Ledger A separate subsidiary account is maintained for each item in inventory. How can

- 6. The Bike Company (TBC) Data for an Illustration

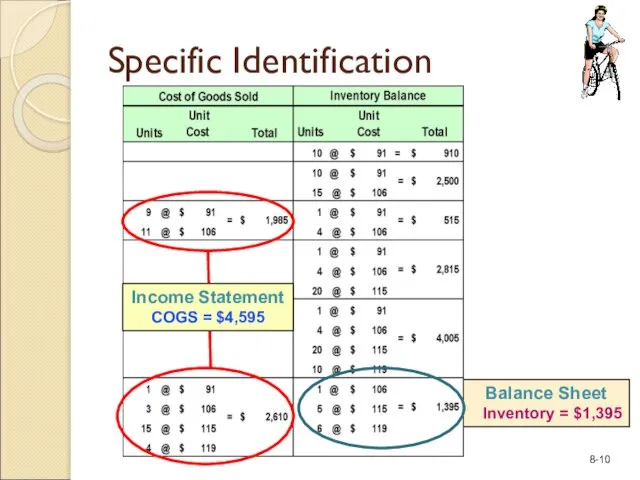

- 7. On August 14, TBC sold 20 bikes for $130 each. Of the bikes sold 9 originally

- 8. A similar entry is made after each sale. Specific Identification

- 9. Additional purchases were made on August 17 and 28. Specific Identification

- 10. Balance Sheet Inventory = $1,395 Specific Identification Income Statement COGS = $4,595

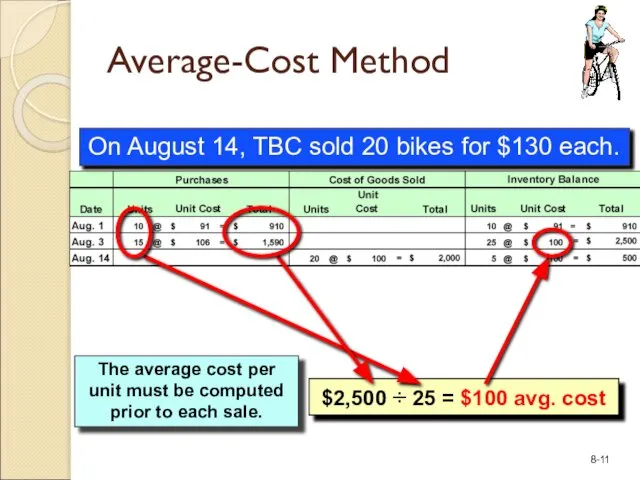

- 11. Average-Cost Method The average cost per unit must be computed prior to each sale. On August

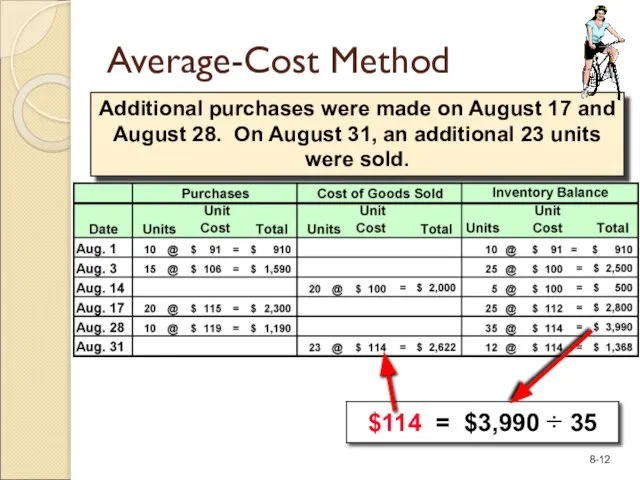

- 12. Average-Cost Method Additional purchases were made on August 17 and August 28. On August 31, an

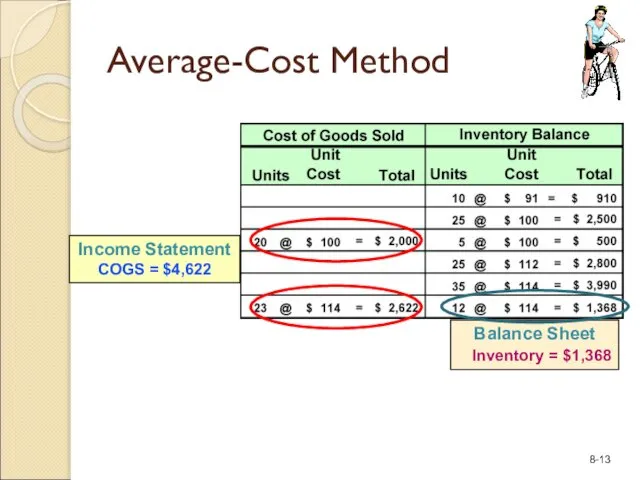

- 13. Income Statement COGS = $4,622 Balance Sheet Inventory = $1,368 Average-Cost Method

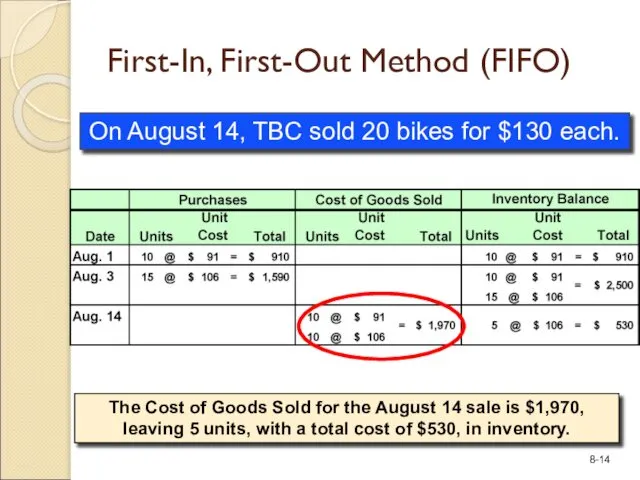

- 14. On August 14, TBC sold 20 bikes for $130 each. First-In, First-Out Method (FIFO)

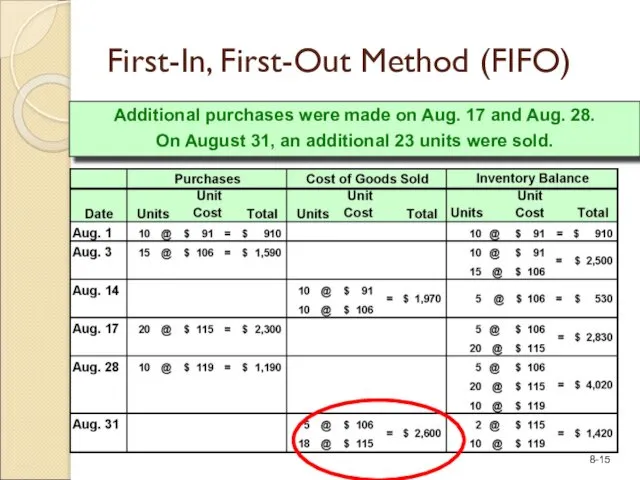

- 15. Additional purchases were made on Aug. 17 and Aug. 28. On August 31, an additional 23

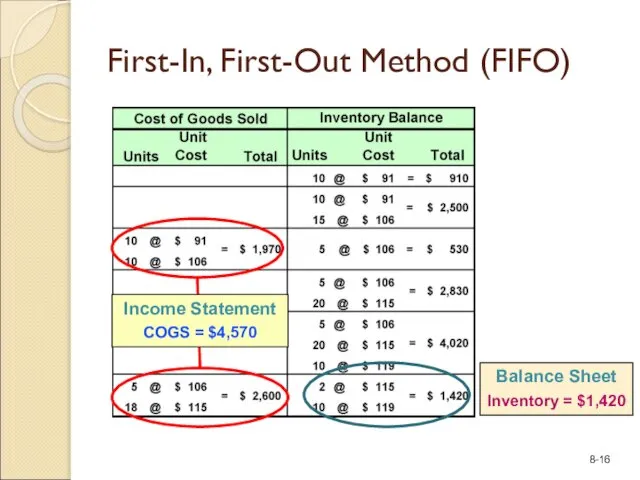

- 16. First-In, First-Out Method (FIFO) Balance Sheet Inventory = $1,420 Income Statement COGS = $4,570

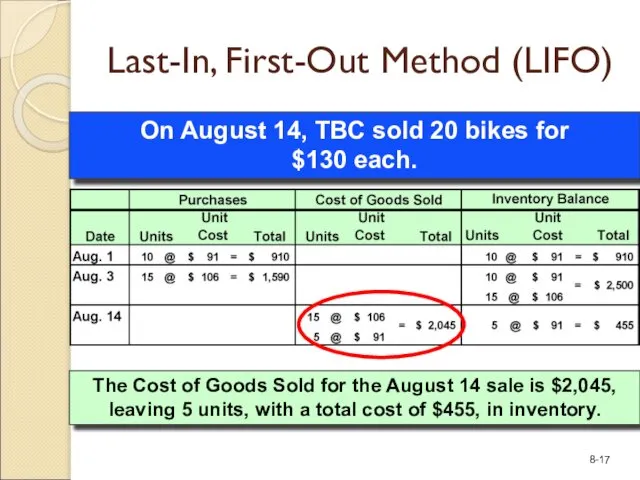

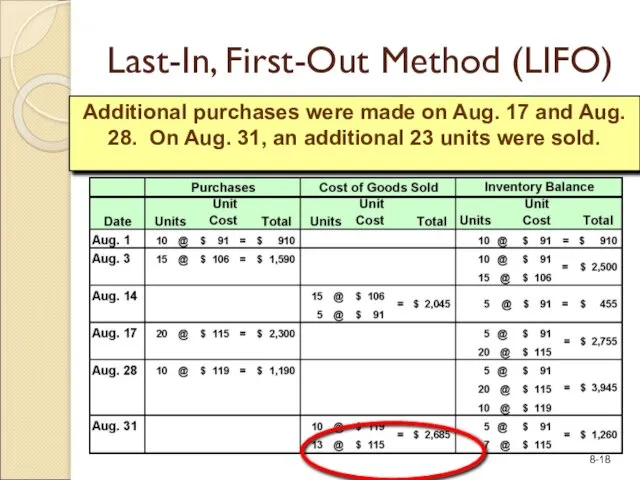

- 17. On August 14, TBC sold 20 bikes for $130 each. Last-In, First-Out Method (LIFO) The Cost

- 18. Last-In, First-Out Method (LIFO) Additional purchases were made on Aug. 17 and Aug. 28. On Aug.

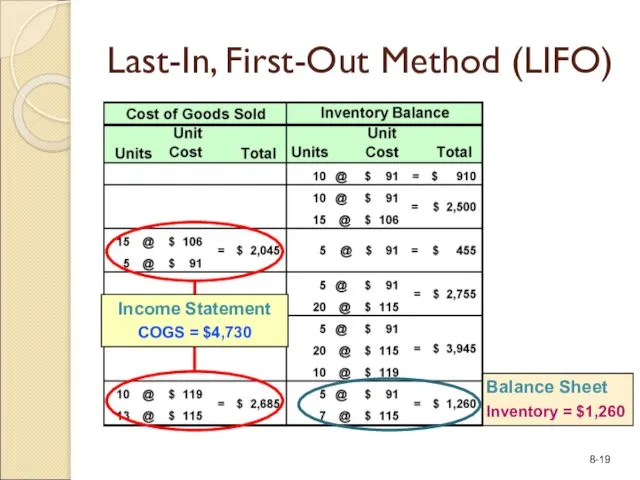

- 19. Balance Sheet Inventory = $1,260 Last-In, First-Out Method (LIFO) Income Statement COGS = $4,730

- 21. Once a company has adopted a particular accounting method, it should follow that method consistently rather

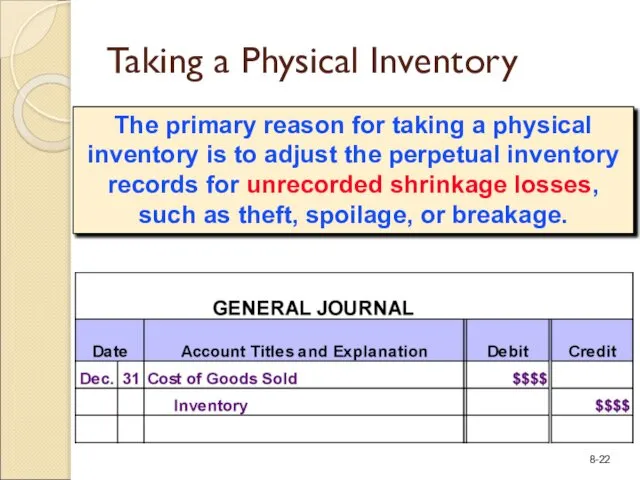

- 22. The primary reason for taking a physical inventory is to adjust the perpetual inventory records for

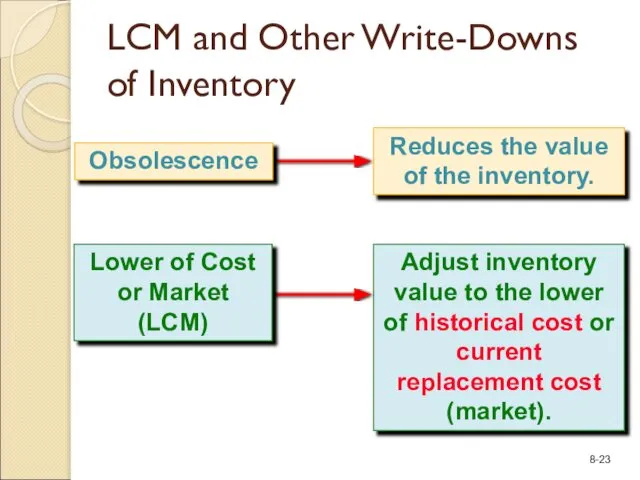

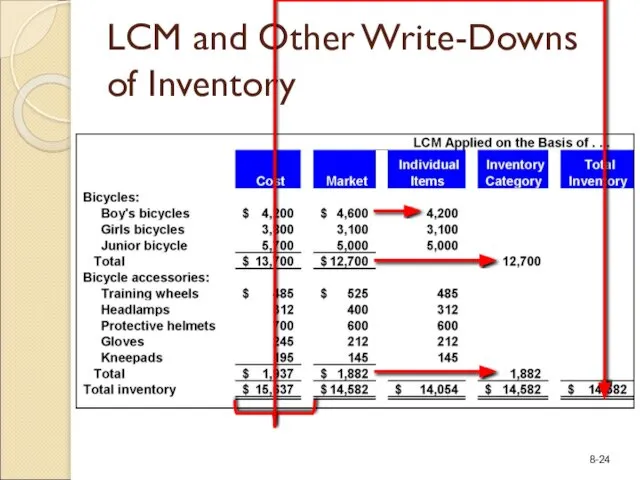

- 23. LCM and Other Write-Downs of Inventory

- 24. LCM and Other Write-Downs of Inventory

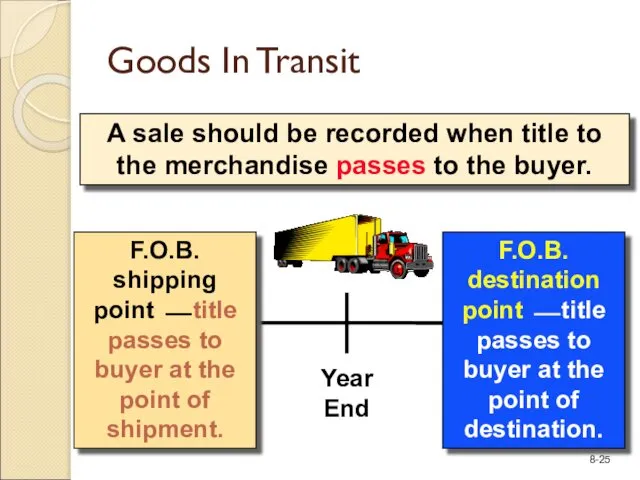

- 25. Year End A sale should be recorded when title to the merchandise passes to the buyer.

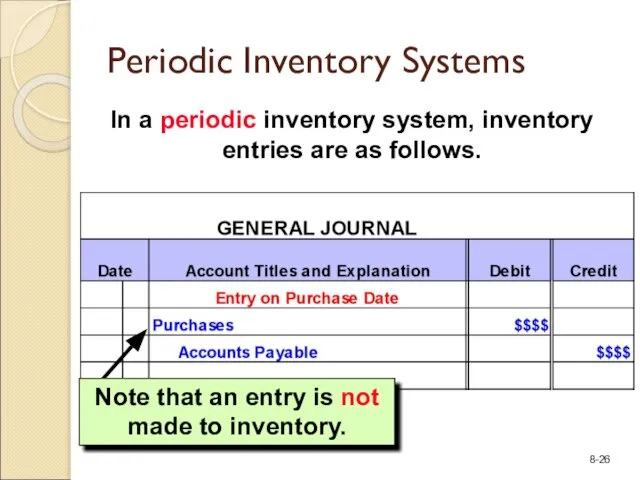

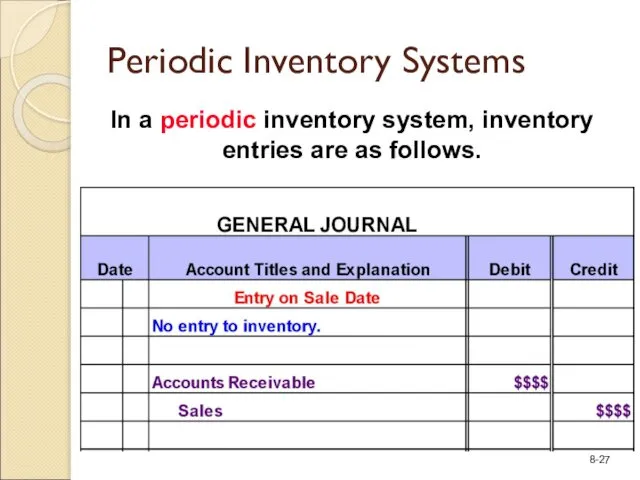

- 26. In a periodic inventory system, inventory entries are as follows. Note that an entry is not

- 27. In a periodic inventory system, inventory entries are as follows. Periodic Inventory Systems

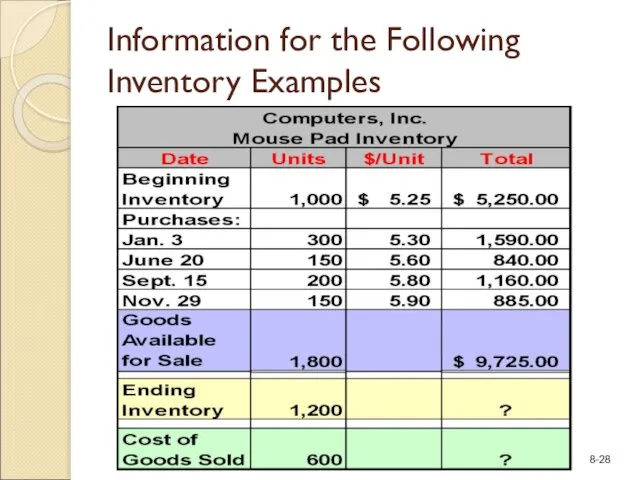

- 28. Information for the Following Inventory Examples

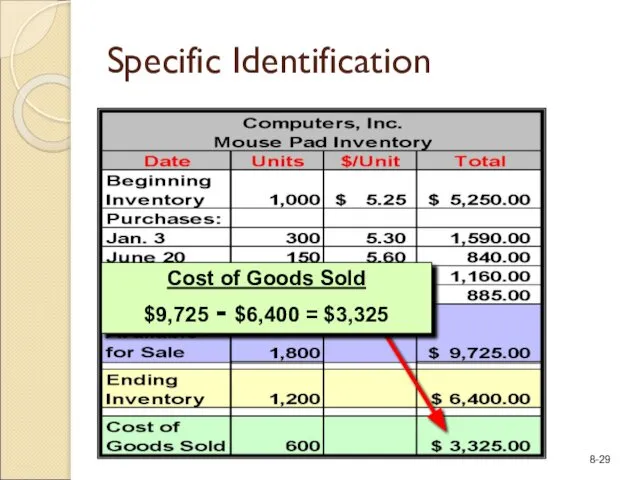

- 29. Specific Identification

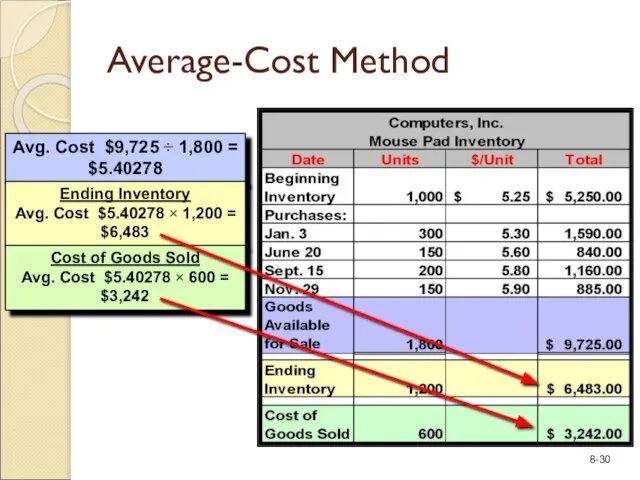

- 30. Avg. Cost $9,725 ÷ 1,800 = $5.40278 Average-Cost Method Ending Inventory Avg. Cost $5.40278 × 1,200

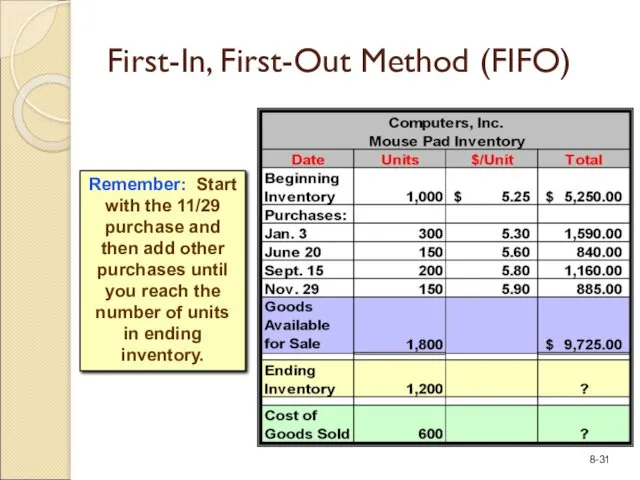

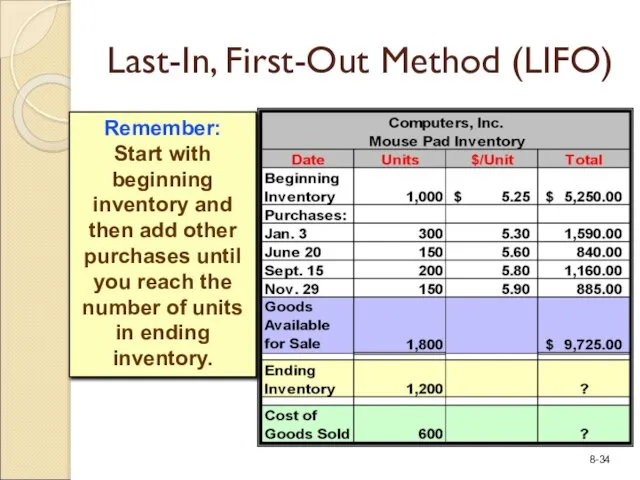

- 31. Remember: Start with the 11/29 purchase and then add other purchases until you reach the number

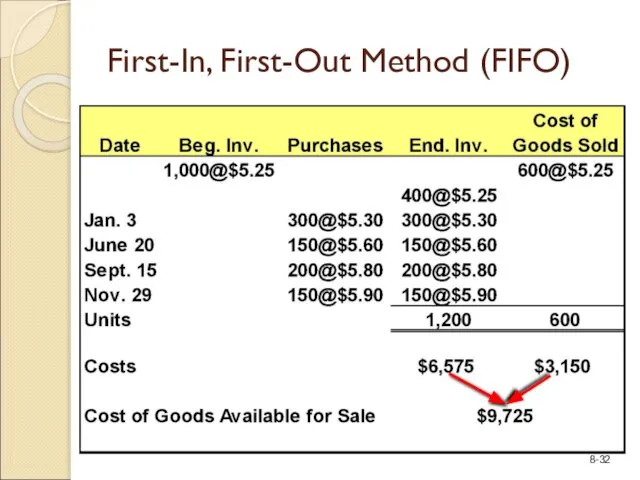

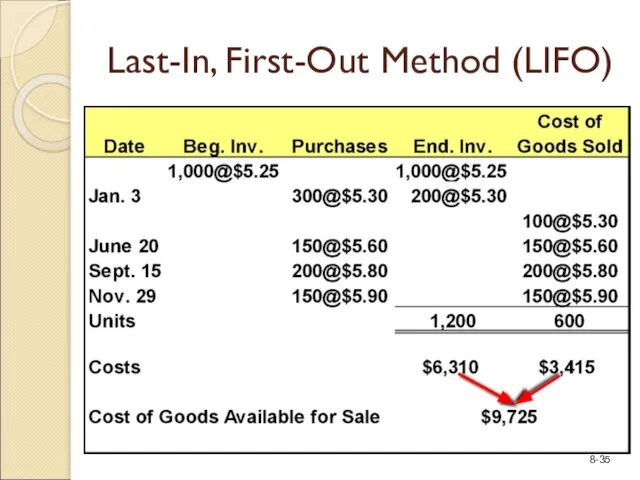

- 32. Now, let’s complete the table. First-In, First-Out Method (FIFO) Now, we have allocated the cost to

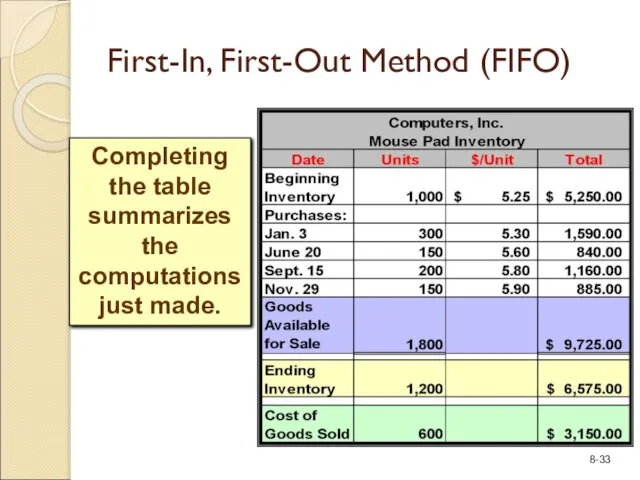

- 33. Completing the table summarizes the computations just made. First-In, First-Out Method (FIFO)

- 34. Remember: Start with beginning inventory and then add other purchases until you reach the number of

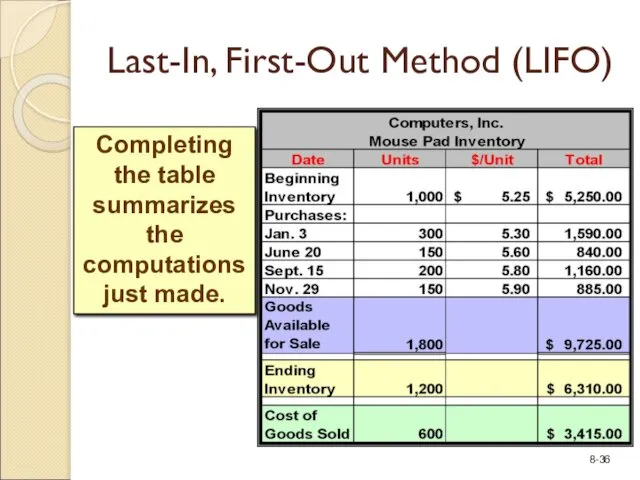

- 35. Last-In, First-Out Method (LIFO) Now, we have allocated the cost to all 1,200 units in ending

- 36. Completing the table summarizes the computations just made. Last-In, First-Out Method (LIFO)

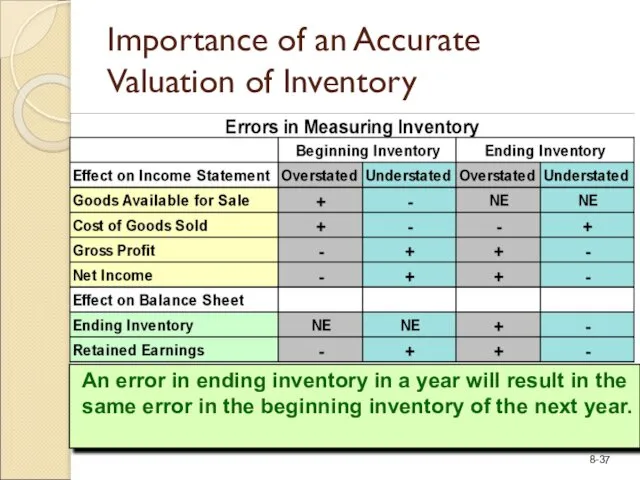

- 37. An error in ending inventory in a year will result in the same error in the

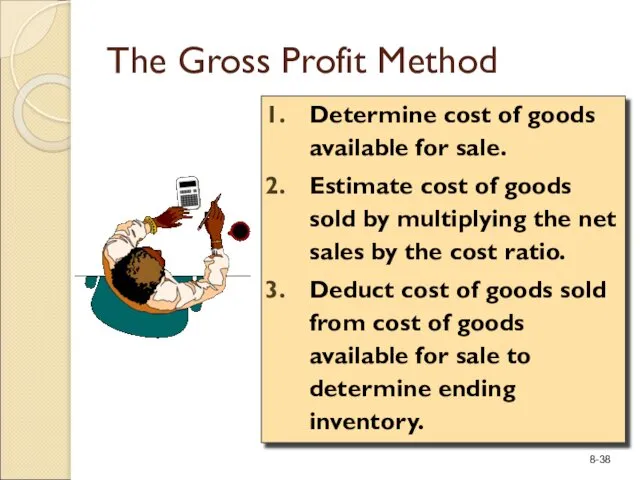

- 38. The Gross Profit Method Determine cost of goods available for sale. Estimate cost of goods sold

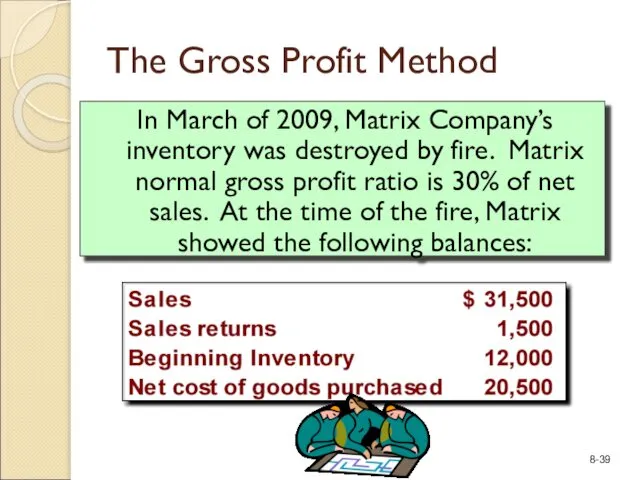

- 39. The Gross Profit Method In March of 2009, Matrix Company’s inventory was destroyed by fire. Matrix

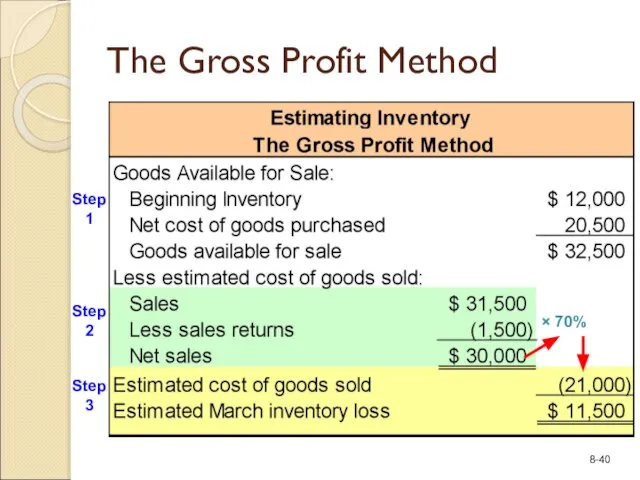

- 40. The Gross Profit Method Step 1 Step 2 Step 3

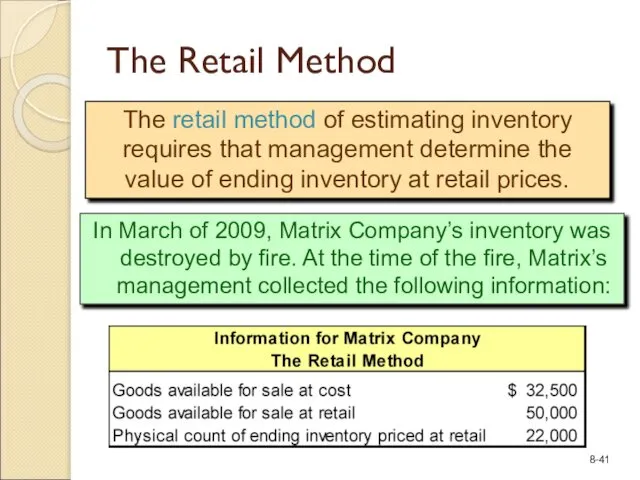

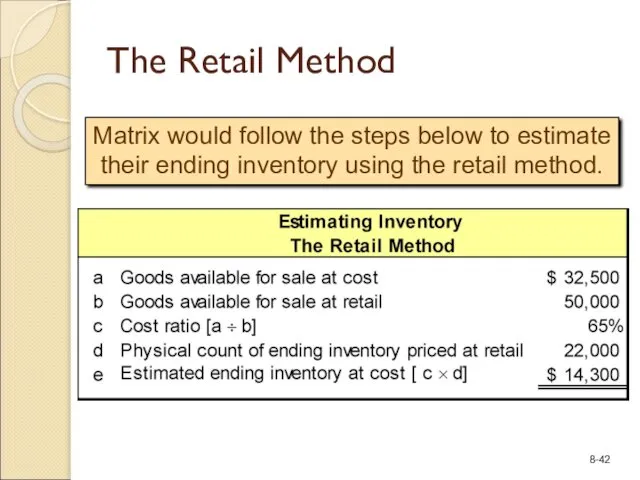

- 41. The Retail Method The retail method of estimating inventory requires that management determine the value of

- 42. The Retail Method Matrix would follow the steps below to estimate their ending inventory using the

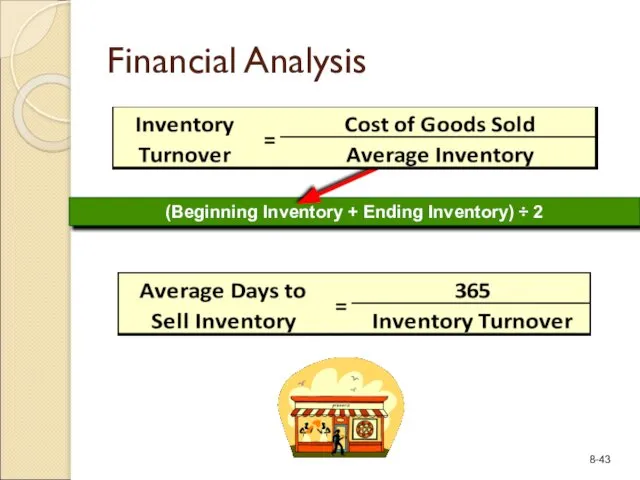

- 43. (Beginning Inventory + Ending Inventory) ÷ 2 Financial Analysis

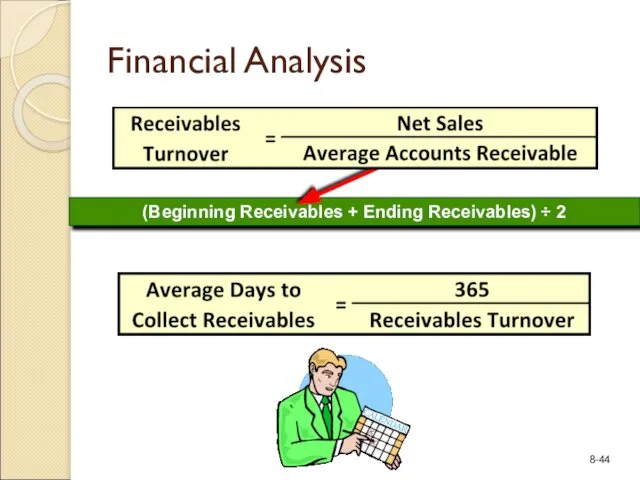

- 44. Financial Analysis (Beginning Receivables + Ending Receivables) ÷ 2

- 46. Скачать презентацию

as goods are sold

The Flow of Inventory Costs

as goods are sold

The Flow of Inventory Costs

In a perpetual inventory system, inventory entries parallel the flow of

In a perpetual inventory system, inventory entries parallel the flow of

When identical units of inventory have different unit costs, a question

When identical units of inventory have different unit costs, a question

Inventory Subsidiary Ledger

A separate subsidiary account is maintained for each item

Inventory Subsidiary Ledger

A separate subsidiary account is maintained for each item

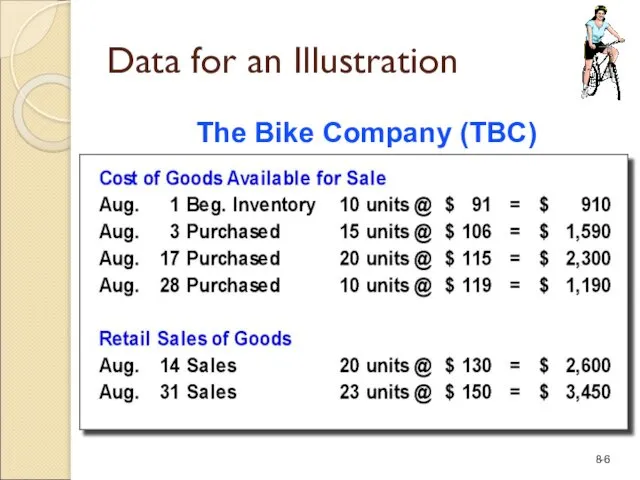

The Bike Company (TBC)

Data for an Illustration

The Bike Company (TBC)

Data for an Illustration

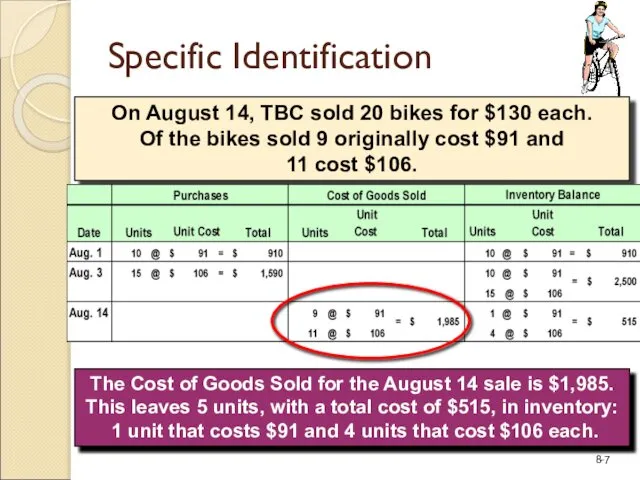

On August 14, TBC sold 20 bikes for $130 each.

Of

On August 14, TBC sold 20 bikes for $130 each.

Of

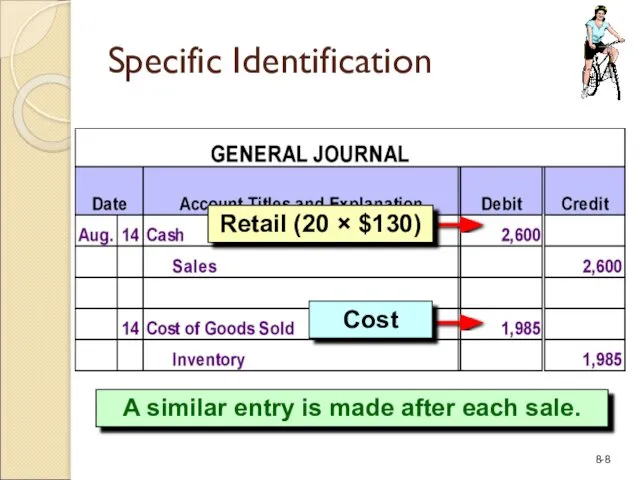

A similar entry is made after each sale.

Specific Identification

A similar entry is made after each sale.

Specific Identification

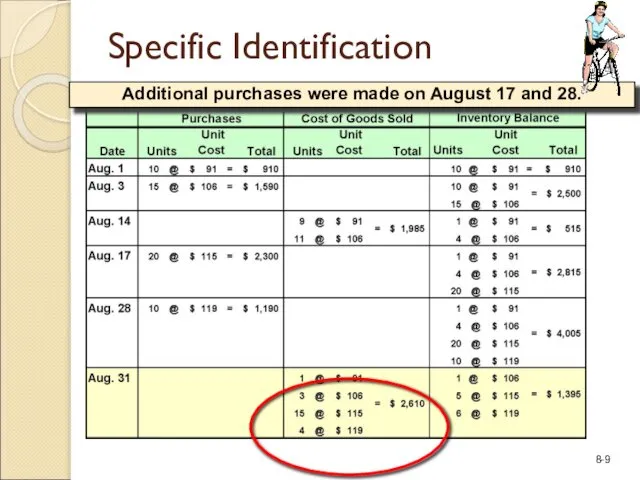

Additional purchases were made on August 17 and 28.

Specific

Additional purchases were made on August 17 and 28.

Specific

Balance Sheet

Inventory = $1,395

Specific Identification

Income Statement

COGS = $4,595

Balance Sheet

Inventory = $1,395

Specific Identification

Income Statement

COGS = $4,595

Average-Cost Method

The average cost per unit must be computed prior to

Average-Cost Method

The average cost per unit must be computed prior to

Average-Cost Method

Additional purchases were made on August 17 and August 28.

Average-Cost Method

Additional purchases were made on August 17 and August 28.

Income Statement

COGS = $4,622

Balance Sheet

Inventory = $1,368

Average-Cost Method

Income Statement

COGS = $4,622

Balance Sheet

Inventory = $1,368

Average-Cost Method

On August 14, TBC sold 20 bikes for $130 each.

First-In,

On August 14, TBC sold 20 bikes for $130 each.

First-In,

Additional purchases were made on Aug. 17 and Aug. 28.

On August

Additional purchases were made on Aug. 17 and Aug. 28.

On August

First-In, First-Out Method (FIFO)

Balance Sheet

Inventory = $1,420

Income Statement

COGS = $4,570

First-In, First-Out Method (FIFO)

Balance Sheet

Inventory = $1,420

Income Statement

COGS = $4,570

On August 14, TBC sold 20 bikes for

$130 each.

Last-In,

On August 14, TBC sold 20 bikes for

$130 each.

Last-In,

Last-In, First-Out Method (LIFO)

Additional purchases were made on Aug. 17 and

Last-In, First-Out Method (LIFO)

Additional purchases were made on Aug. 17 and

Balance Sheet

Inventory = $1,260

Last-In, First-Out Method (LIFO)

Income Statement

COGS = $4,730

Balance Sheet

Inventory = $1,260

Last-In, First-Out Method (LIFO)

Income Statement

COGS = $4,730

Once a company has adopted a particular accounting method, it should

Once a company has adopted a particular accounting method, it should

The primary reason for taking a physical inventory is to adjust

The primary reason for taking a physical inventory is to adjust

LCM and Other Write-Downs

of Inventory

LCM and Other Write-Downs

of Inventory

LCM and Other Write-Downs

of Inventory

LCM and Other Write-Downs

of Inventory

Year End

A sale should be recorded when title to the merchandise

Year End

A sale should be recorded when title to the merchandise

In a periodic inventory system, inventory entries are as follows.

Note that

In a periodic inventory system, inventory entries are as follows.

Note that

In a periodic inventory system, inventory entries are as follows.

Periodic Inventory

In a periodic inventory system, inventory entries are as follows.

Periodic Inventory

Information for the Following Inventory Examples

Information for the Following Inventory Examples

Specific Identification

Specific Identification

Avg. Cost $9,725 ÷ 1,800 = $5.40278

Average-Cost Method

Ending Inventory

Avg. Cost

Avg. Cost $9,725 ÷ 1,800 = $5.40278

Average-Cost Method

Ending Inventory

Avg. Cost

Remember: Start with the 11/29 purchase and then add other purchases

Remember: Start with the 11/29 purchase and then add other purchases

Now, let’s complete the table.

First-In, First-Out Method (FIFO)

Now, we have allocated

Now, let’s complete the table.

First-In, First-Out Method (FIFO)

Now, we have allocated

Completing the table summarizes the computations just made.

First-In, First-Out Method (FIFO)

Completing the table summarizes the computations just made.

First-In, First-Out Method (FIFO)

Remember: Start with beginning inventory and then add other purchases until

Remember: Start with beginning inventory and then add other purchases until

Last-In, First-Out Method (LIFO)

Now, we have allocated the cost to all

Last-In, First-Out Method (LIFO)

Now, we have allocated the cost to all

Completing the table summarizes the computations just made.

Last-In, First-Out Method (LIFO)

Completing the table summarizes the computations just made.

Last-In, First-Out Method (LIFO)

An error in ending inventory in a year will result in

An error in ending inventory in a year will result in

The Gross Profit Method

Determine cost of goods available for sale.

Estimate cost

The Gross Profit Method

Determine cost of goods available for sale.

Estimate cost

The Gross Profit Method

In March of 2009, Matrix Company’s inventory was

The Gross Profit Method

In March of 2009, Matrix Company’s inventory was

The Gross Profit Method

Step

1

Step

2

Step

3

The Gross Profit Method

Step

1

Step

2

Step

3

The Retail Method

The retail method of estimating inventory requires that management

The Retail Method

The retail method of estimating inventory requires that management

The Retail Method

Matrix would follow the steps below to estimate their

The Retail Method

Matrix would follow the steps below to estimate their

(Beginning Inventory + Ending Inventory) ÷ 2

Financial Analysis

(Beginning Inventory + Ending Inventory) ÷ 2

Financial Analysis

Financial Analysis

(Beginning Receivables + Ending Receivables) ÷ 2

Financial Analysis

(Beginning Receivables + Ending Receivables) ÷ 2

Фінансова стратегія: поняття, еволюція, концепції

Фінансова стратегія: поняття, еволюція, концепції Коррупция как болезнь современной России

Коррупция как болезнь современной России Венчурный фонд

Венчурный фонд Оплата труда в организации. Формы и системы оплаты труда

Оплата труда в организации. Формы и системы оплаты труда Финансовые результаты предприятия

Финансовые результаты предприятия Проценты по вкладу: большие и маленькие. Финансовая грамотность, 10 класс

Проценты по вкладу: большие и маленькие. Финансовая грамотность, 10 класс Счета бухгалтерского учета

Счета бухгалтерского учета О мерах по повышению заработной платы учителей

О мерах по повышению заработной платы учителей Основы построения страховых тарифов (Тема 2)

Основы построения страховых тарифов (Тема 2) Организация учета готовой продукции и расчетов с покупателями и заказчиками. ООО Омский завод плавленых сыров

Организация учета готовой продукции и расчетов с покупателями и заказчиками. ООО Омский завод плавленых сыров Подготовка информации, необходимой для оценки бизнеса

Подготовка информации, необходимой для оценки бизнеса Финансы и деньги

Финансы и деньги Современные проблемы мировой финансовой системы. Четвертая промышленная революция и проблема труда

Современные проблемы мировой финансовой системы. Четвертая промышленная революция и проблема труда Конференция попечительского совета

Конференция попечительского совета Сущность и состав финансовых ресурсов: новые реалии

Сущность и состав финансовых ресурсов: новые реалии Предмет и метод бухгалтерского учета

Предмет и метод бухгалтерского учета Органы финансово-экономического контроля

Органы финансово-экономического контроля Упрощённая система налогообложения

Упрощённая система налогообложения Аудит магазина, анализ конкурентов. Точки масштабирования бренда

Аудит магазина, анализ конкурентов. Точки масштабирования бренда 20171007_o7-15

20171007_o7-15 Налоговый вычет в 2020 году

Налоговый вычет в 2020 году Frendex - закрытый инвестиционный клуб

Frendex - закрытый инвестиционный клуб Финансы, банки, ценные бумаги (подготовка к ГИА по обществознанию)

Финансы, банки, ценные бумаги (подготовка к ГИА по обществознанию) Инфляция. Причины инфляции

Инфляция. Причины инфляции Вкладывай средства в своё будущее

Вкладывай средства в своё будущее Стоп-коронавирус

Стоп-коронавирус Анализ платежеспособности и ликвидности предприятия. (Тема 3)

Анализ платежеспособности и ликвидности предприятия. (Тема 3) Функции финансового менеджмента

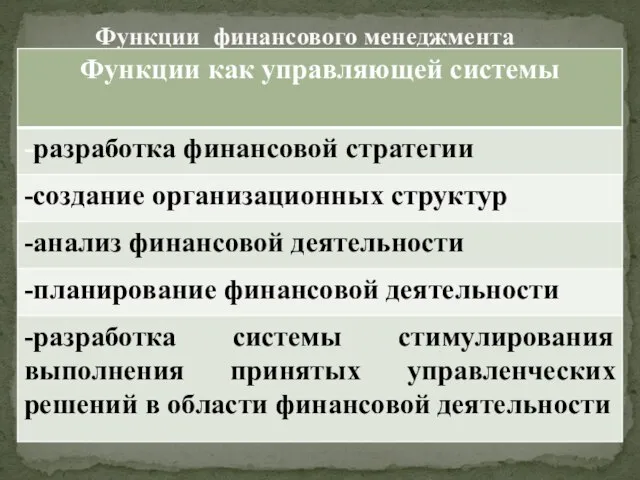

Функции финансового менеджмента