- Overview of Working Capital Management

Содержание

- 2. After studying Chapter 8, you should be able to: Explain how the definition of "working capital"

- 3. Overview of Working Capital Management Working Capital Concepts Working Capital Issues Financing Current Assets: Short-Term and

- 4. Working Capital Concepts Net Working Capital Current Assets - Current Liabilities. Gross Working Capital The firm’s

- 5. Significance of Working Capital Management In a typical manufacturing firm, current assets exceed one-half of total

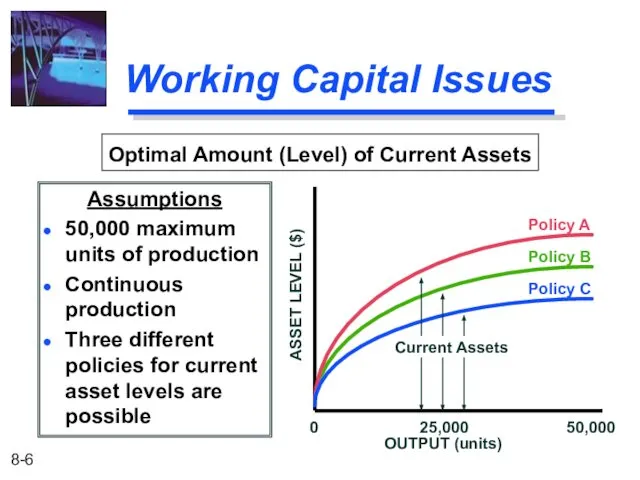

- 6. Working Capital Issues Assumptions 50,000 maximum units of production Continuous production Three different policies for current

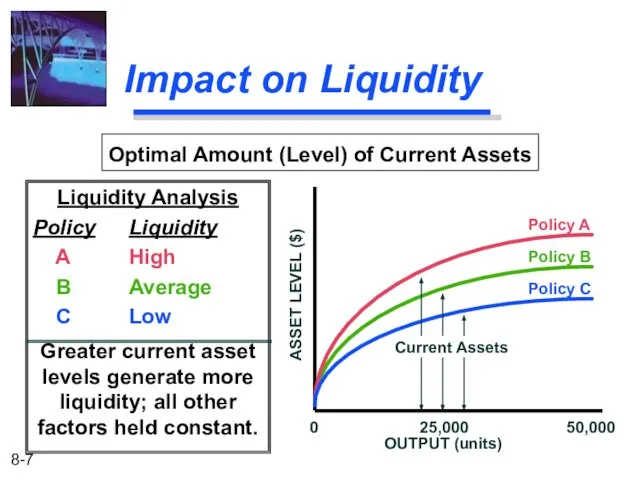

- 7. Impact on Liquidity Liquidity Analysis Policy Liquidity A High B Average C Low Greater current asset

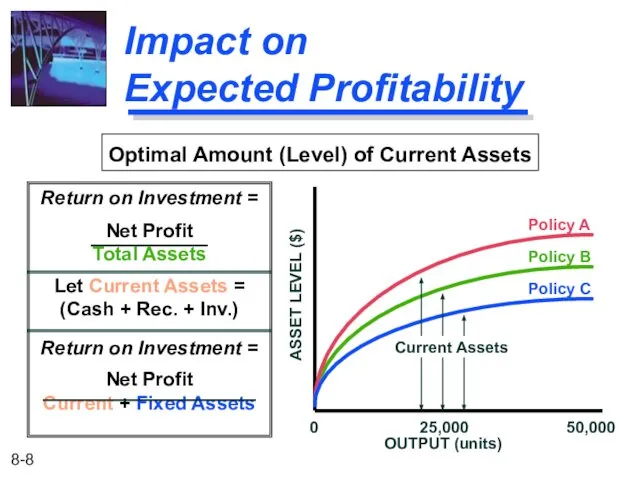

- 8. Impact on Expected Profitability Return on Investment = Net Profit Total Assets Let Current Assets =

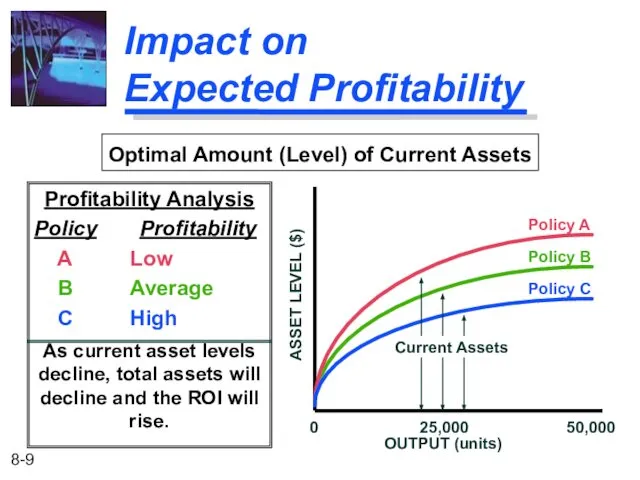

- 9. Impact on Expected Profitability Profitability Analysis Policy Profitability A Low B Average C High As current

- 10. Impact on Risk Decreasing cash reduces the firm’s ability to meet its financial obligations. More risk!

- 11. Impact on Risk Risk Analysis Policy Risk A Low B Average C High Risk increases as

- 12. Summary of the Optimal Amount of Current Assets SUMMARY OF OPTIMAL CURRENT ASSET ANALYSIS Policy Liquidity

- 13. Classifications of Working Capital Time Permanent Temporary Components Cash, marketable securities, receivables, and inventory

- 14. Permanent Working Capital The amount of current assets required to meet a firm’s long-term minimum needs.

- 15. Temporary Working Capital The amount of current assets that varies with seasonal requirements. Permanent current assets

- 16. Financing Current Assets: Short-Term and Long-Term Mix Spontaneous Financing: Trade credit, and other payables and accruals,

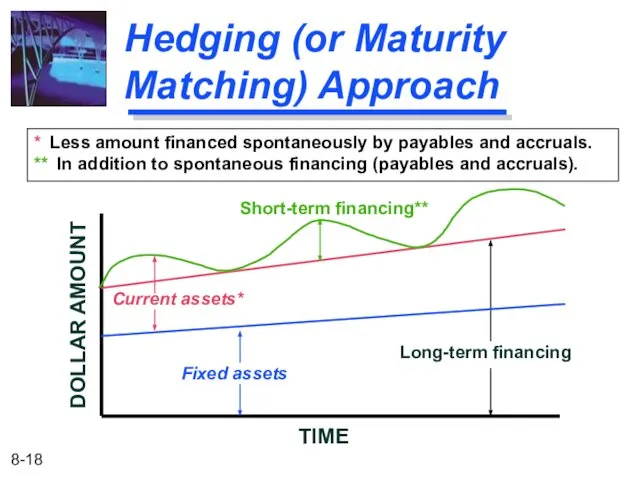

- 17. Hedging (or Maturity Matching) Approach A method of financing where each asset would be offset with

- 18. Hedging (or Maturity Matching) Approach * Less amount financed spontaneously by payables and accruals. ** In

- 19. Financing Needs and the Hedging Approach Fixed assets and the non-seasonal portion of current assets are

- 20. Self-Liquidating Nature of Short-Term Loans Seasonal orders require the purchase of inventory beyond current levels. Increased

- 21. Risks vs. Costs Trade-Off (Conservative Approach) Long-Term Financing Benefits Less worry in refinancing short-term obligations Less

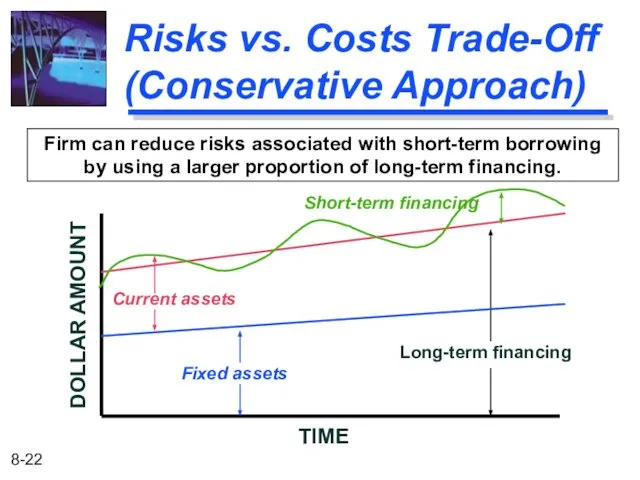

- 22. Risks vs. Costs Trade-Off (Conservative Approach) Firm can reduce risks associated with short-term borrowing by using

- 23. Comparison with an Aggressive Approach Short-Term Financing Benefits Financing long-term needs with a lower interest cost

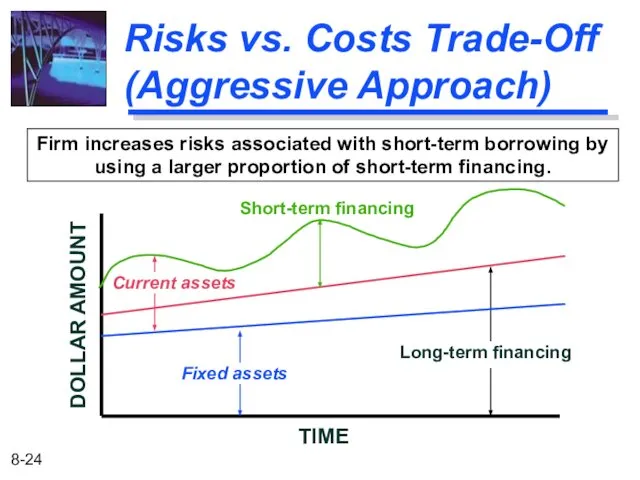

- 24. Firm increases risks associated with short-term borrowing by using a larger proportion of short-term financing. TIME

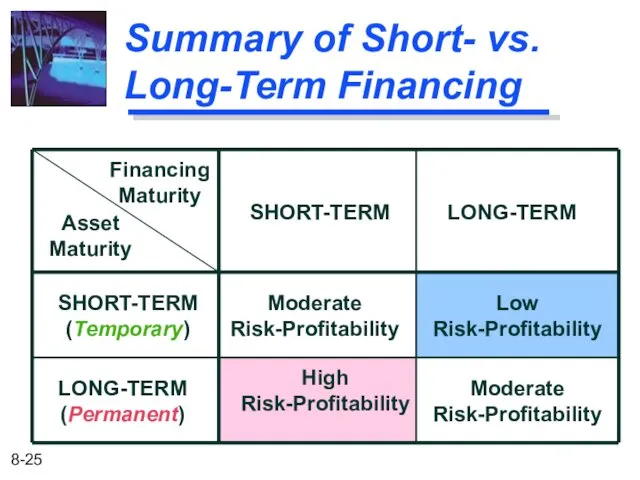

- 25. Summary of Short- vs. Long-Term Financing Financing Maturity Asset Maturity SHORT-TERM LONG-TERM Low Risk-Profitability Moderate Risk-Profitability

- 27. Скачать презентацию

After studying Chapter 8, you should be able to:

Explain how the

After studying Chapter 8, you should be able to:

Explain how the

Overview of Working Capital Management

Working Capital Concepts

Working Capital Issues

Financing Current Assets:

Overview of Working Capital Management

Working Capital Concepts

Working Capital Issues

Financing Current Assets:

Working Capital Concepts

Net Working Capital

Current Assets - Current Liabilities.

Gross Working Capital

The

Working Capital Concepts

Net Working Capital

Current Assets - Current Liabilities.

Gross Working Capital

The

Significance of Working Capital Management

In a typical manufacturing firm, current assets

Significance of Working Capital Management

In a typical manufacturing firm, current assets

Working Capital Issues

Assumptions

50,000 maximum units of production

Continuous production

Three different policies for

Working Capital Issues

Assumptions

50,000 maximum units of production

Continuous production

Three different policies for

Impact on Liquidity

Liquidity Analysis

Policy Liquidity

A High

B Average

C Low

Greater current asset levels generate

Impact on Liquidity

Liquidity Analysis

Policy Liquidity

A High

B Average

C Low

Greater current asset levels generate

Impact on

Expected Profitability

Return on Investment =

Net Profit

Total Assets

Let Current Assets

Impact on

Expected Profitability

Return on Investment =

Net Profit

Total Assets

Let Current Assets

Impact on

Expected Profitability

Profitability Analysis

Policy Profitability

A Low

B Average

C High

As current asset

Impact on

Expected Profitability

Profitability Analysis

Policy Profitability

A Low

B Average

C High

As current asset

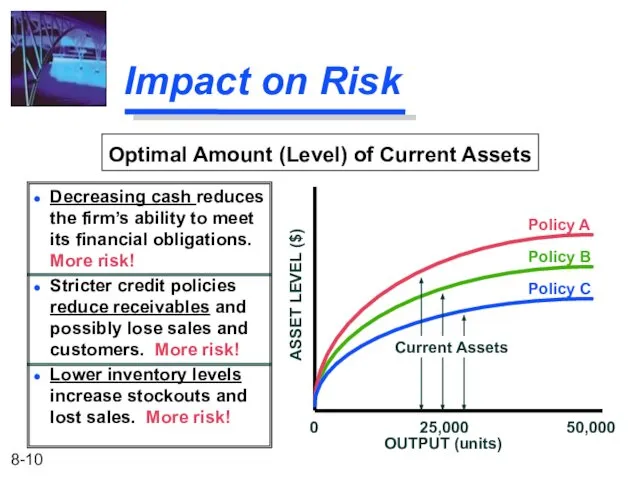

Impact on Risk

Decreasing cash reduces the firm’s ability to meet its

Impact on Risk

Decreasing cash reduces the firm’s ability to meet its

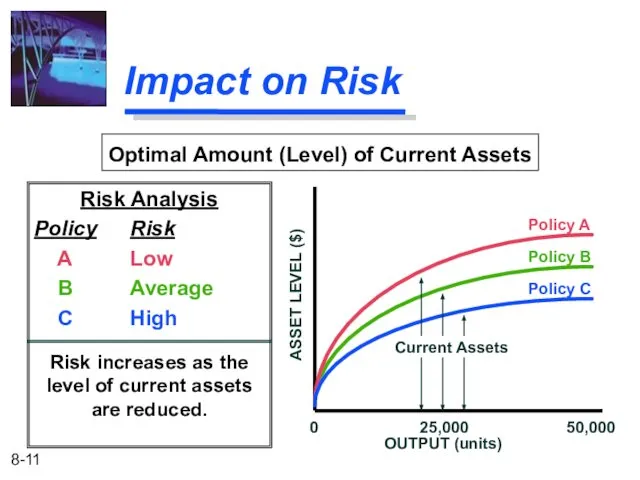

Impact on Risk

Risk Analysis

Policy Risk

A Low

B Average

C High

Risk increases as the level

Impact on Risk

Risk Analysis

Policy Risk

A Low

B Average

C High

Risk increases as the level

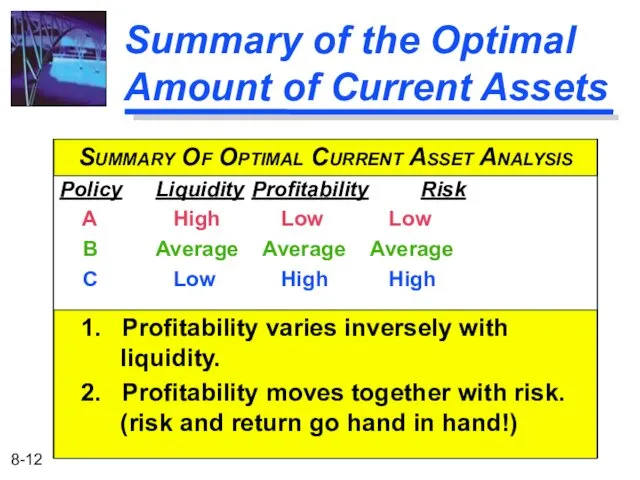

Summary of the Optimal Amount of Current Assets

SUMMARY OF OPTIMAL CURRENT

Summary of the Optimal Amount of Current Assets

SUMMARY OF OPTIMAL CURRENT

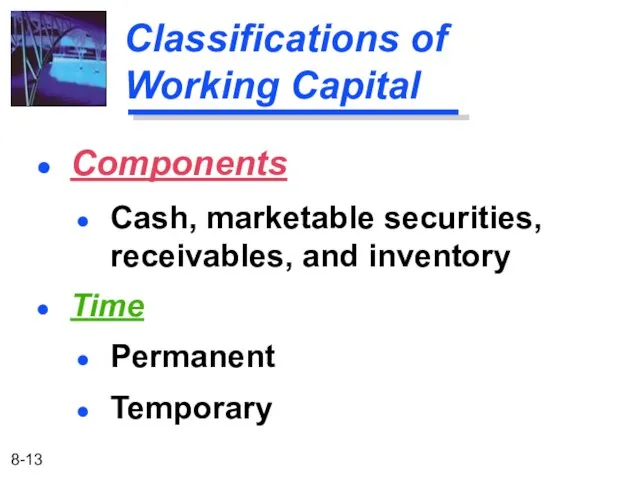

Classifications of Working Capital

Time

Permanent

Temporary

Components

Cash, marketable securities, receivables, and inventory

Classifications of Working Capital

Time

Permanent

Temporary

Components

Cash, marketable securities, receivables, and inventory

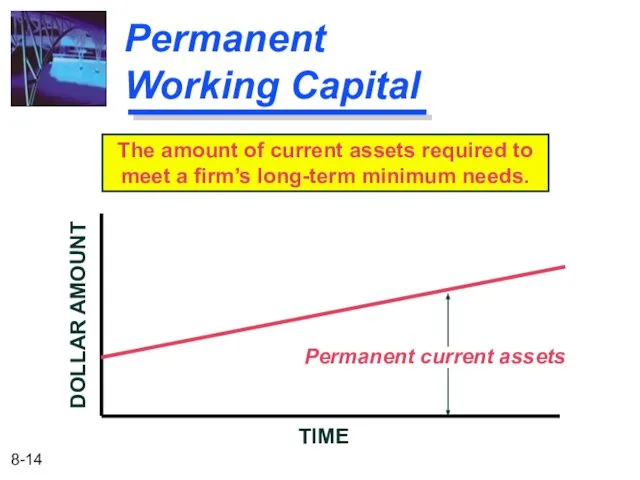

Permanent Working Capital

The amount of current assets required to meet a

Permanent Working Capital

The amount of current assets required to meet a

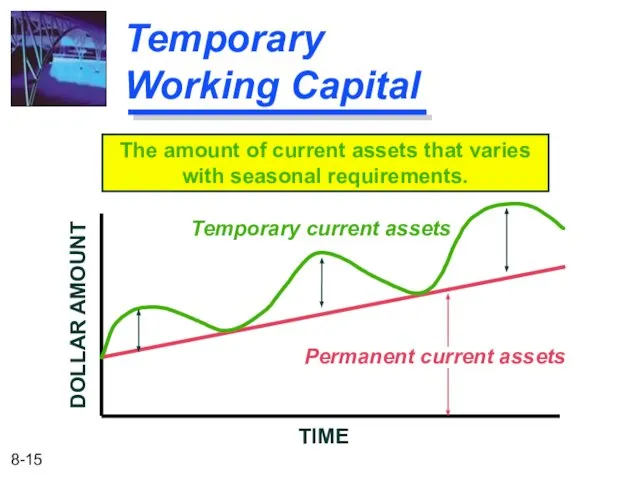

Temporary Working Capital

The amount of current assets that varies with seasonal

Temporary Working Capital

The amount of current assets that varies with seasonal

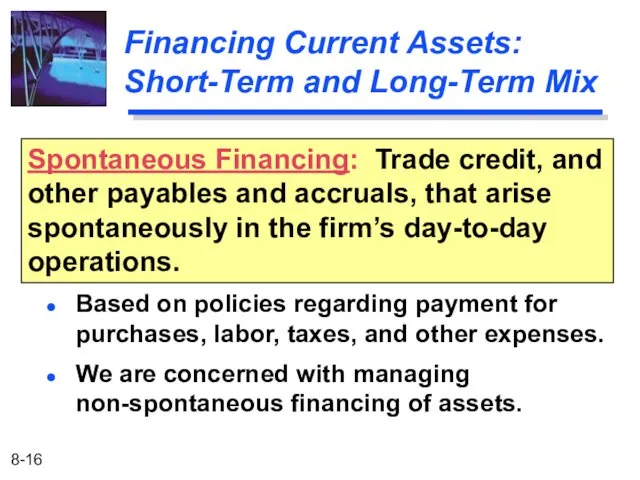

Financing Current Assets: Short-Term and Long-Term Mix

Spontaneous Financing: Trade credit, and

Financing Current Assets: Short-Term and Long-Term Mix

Spontaneous Financing: Trade credit, and

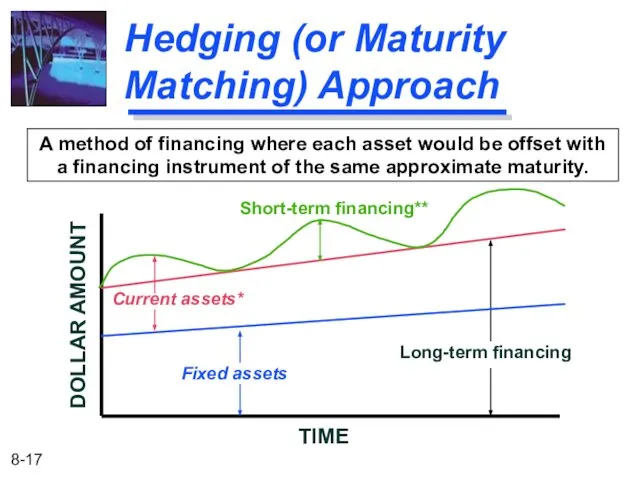

Hedging (or Maturity Matching) Approach

A method of financing where each asset

Hedging (or Maturity Matching) Approach

A method of financing where each asset

Hedging (or Maturity Matching) Approach

* Less amount financed spontaneously by payables

Hedging (or Maturity Matching) Approach

* Less amount financed spontaneously by payables

Financing Needs and

the Hedging Approach

Fixed assets and the non-seasonal portion

Financing Needs and

the Hedging Approach

Fixed assets and the non-seasonal portion

Self-Liquidating Nature of Short-Term Loans

Seasonal orders require the purchase of inventory

Self-Liquidating Nature of Short-Term Loans

Seasonal orders require the purchase of inventory

Risks vs. Costs Trade-Off (Conservative Approach)

Long-Term Financing Benefits

Less worry in refinancing

Risks vs. Costs Trade-Off (Conservative Approach)

Long-Term Financing Benefits

Less worry in refinancing

Risks vs. Costs Trade-Off (Conservative Approach)

Firm can reduce risks associated with

Risks vs. Costs Trade-Off (Conservative Approach)

Firm can reduce risks associated with

Comparison with an Aggressive Approach

Short-Term Financing Benefits

Financing long-term needs with a

Comparison with an Aggressive Approach

Short-Term Financing Benefits

Financing long-term needs with a

Firm increases risks associated with short-term borrowing by using a larger

Firm increases risks associated with short-term borrowing by using a larger

Summary of Short- vs. Long-Term Financing

Financing

Maturity

Asset

Maturity

SHORT-TERM

LONG-TERM

Low

Risk-Profitability

Moderate

Risk-Profitability

Moderate

Risk-Profitability

High

Risk-Profitability

SHORT-TERM

(Temporary)

LONG-TERM

(Permanent)

Summary of Short- vs. Long-Term Financing

Financing

Maturity

Asset

Maturity

SHORT-TERM

LONG-TERM

Low

Risk-Profitability

Moderate

Risk-Profitability

Moderate

Risk-Profitability

High

Risk-Profitability

SHORT-TERM

(Temporary)

LONG-TERM

(Permanent)

Проектная деятельность в образовании. Управление проектами

Проектная деятельность в образовании. Управление проектами Второй этап работы над проектом: организация групп, роли в команде

Второй этап работы над проектом: организация групп, роли в команде Реструктуризация управления компанией

Реструктуризация управления компанией Трудовая адаптация персонала

Трудовая адаптация персонала Глобальные системы резервирования как эффективные рекламные технологии

Глобальные системы резервирования как эффективные рекламные технологии Организационная культура

Организационная культура Мотивация СМЗ 2.0

Мотивация СМЗ 2.0 Manager`s proffesional skils and personality traids

Manager`s proffesional skils and personality traids Тәуекел менеджментінің базалық тұжырымдамалыры және көрсеткіштері

Тәуекел менеджментінің базалық тұжырымдамалыры және көрсеткіштері Мотивация как функция управления

Мотивация как функция управления Форматы мероприятий

Форматы мероприятий Сутність туристичних формальностей

Сутність туристичних формальностей Мотивация

Мотивация Внедрение автоматизированной подсистемы управления персоналом

Внедрение автоматизированной подсистемы управления персоналом Работа менеджера в организации

Работа менеджера в организации Сущность управленческих отношений в организации

Сущность управленческих отношений в организации Гостиница Базилика

Гостиница Базилика Бизнес процессы. Отдел продаж. Производство

Бизнес процессы. Отдел продаж. Производство Стратегический подход к управлению изменениями

Стратегический подход к управлению изменениями Понятие и характеристика затрат в логистической деятельности

Понятие и характеристика затрат в логистической деятельности Административная (классическая) школа менеджмента

Административная (классическая) школа менеджмента Использование информационных технологий на предприятии оптовой торговли

Использование информационных технологий на предприятии оптовой торговли Задача принятия управленческого решения

Задача принятия управленческого решения Оценка сложных систем в условиях стохастической неопределенности. (Лекция 10)

Оценка сложных систем в условиях стохастической неопределенности. (Лекция 10) Метрологическое обеспечение АЗС

Метрологическое обеспечение АЗС Стили работы лидера

Стили работы лидера Финансовый менеджмент

Финансовый менеджмент 2. Международная Ассоциация Управления Проектами

2. Международная Ассоциация Управления Проектами