Productive system and Process Approach. Operations Management in Corporate Profitability and Competitiveness

- Productive system and Process Approach. Operations Management in Corporate Profitability and Competitiveness

Содержание

- 2. JAP LEARNING GOALS after these lessons you will be able to describe operations in terms of

- 3. JAP LEARNING GOALS after these lessons you will be able to 7. discuss trends in operations

- 4. JAP JAP What is a Productive system (Buffa), what is a Process (Krajewski& Ritzman)? Examples of

- 5. JAP EXAMPLES OF PRODUCTIVE SYSTEMS: Electronics assembly Airplane manufacturing Steel production Automobile assembly Oil refining Fast

- 6. JAP Why must a system has to be productive?

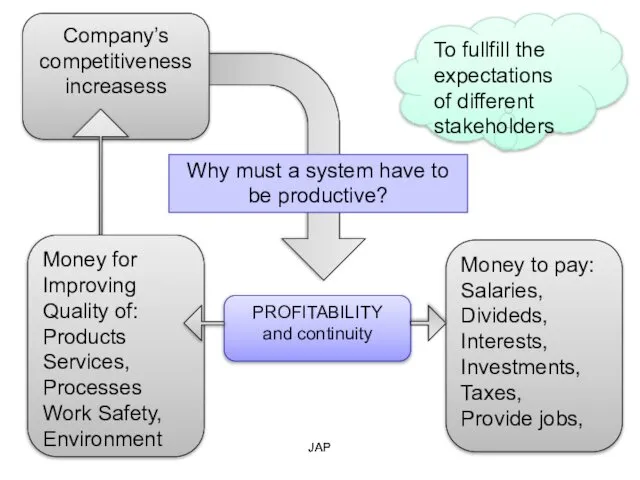

- 7. Company’s competitiveness increasess JAP JAP Why must a system have to be productive? PROFITABILITY and continuity

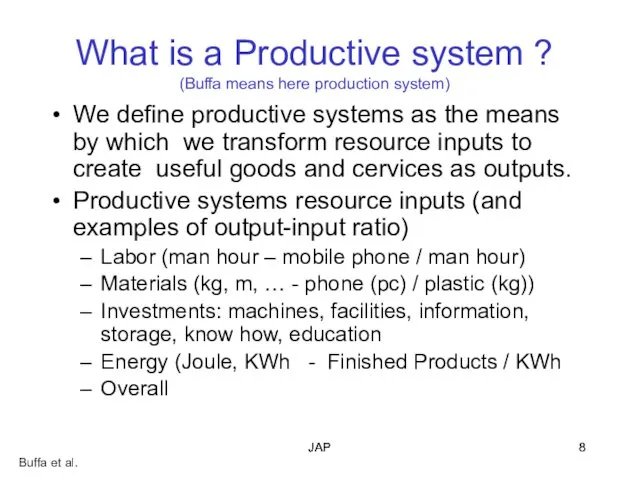

- 8. JAP JAP What is a Productive system ? (Buffa means here production system) We define productive

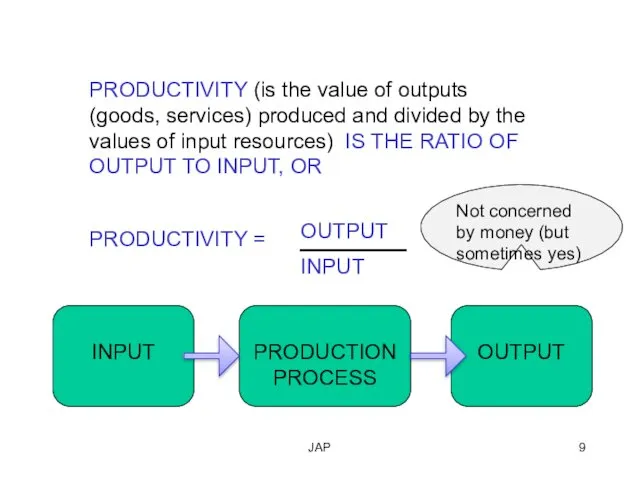

- 9. JAP PRODUCTIVITY (is the value of outputs (goods, services) produced and divided by the values of

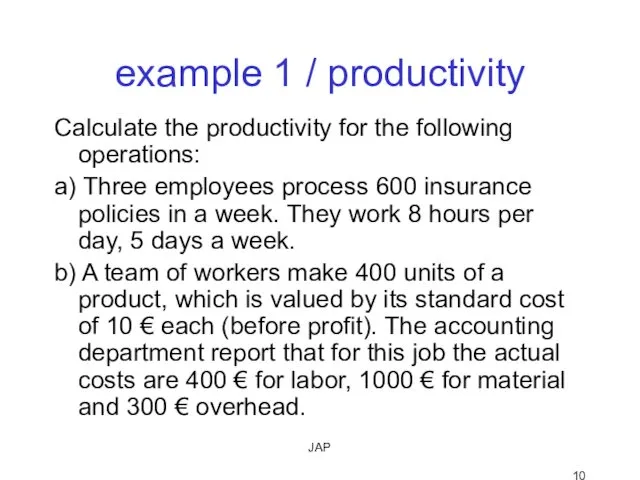

- 10. JAP example 1 / productivity Calculate the productivity for the following operations: a) Three employees process

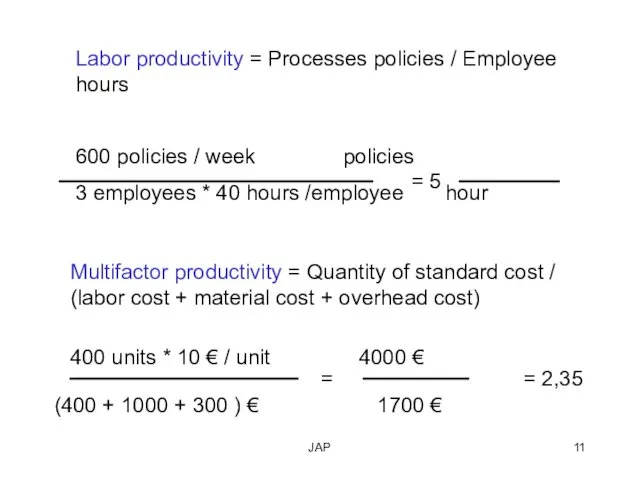

- 11. JAP Labor productivity = Processes policies / Employee hours 600 policies / week policies 3 employees

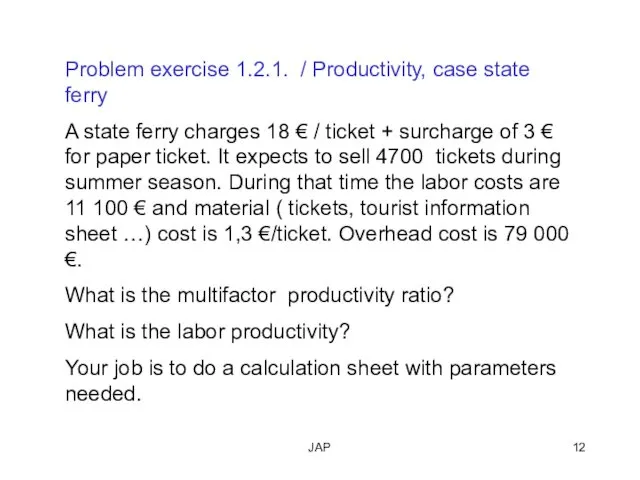

- 12. JAP Problem exercise 1.2.1. / Productivity, case state ferry A state ferry charges 18 € /

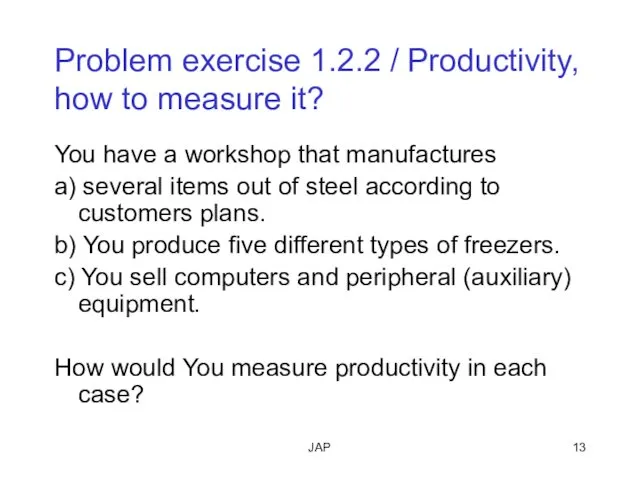

- 13. JAP Problem exercise 1.2.2 / Productivity, how to measure it? You have a workshop that manufactures

- 14. JAP Problem exercise 1.2.3. Productivity in University Student tuition at University in US is $100 per

- 15. JAP Problem exercise 1.2.4. Productivity, case garments Natalie Attired makes fashionable garments. During a particular week

- 16. JAP Exercise 1.2.5. Productivity, case uniform manufacturing The Big Black Bird Company (BBBC) has a large

- 17. JAP Profitable System versus Productive System cost of (money) labor materials machines facilities energy information capital

- 18. JAP THE DU PONT SYSTEM, RETURN ON ASSETS net sales variable costs contribution margin fixed costs

- 19. JAP Fixed Assets: Machinery Equipment Facilities Current Assets: Materials Work in Process Final Products Cash and

- 20. JAP THE DU PONT SYSTEM, REVENUE ON INVESTMENT (RETURN OF INVESTMENT, RETURN OF CAPITAL EMPLOYMENT) net

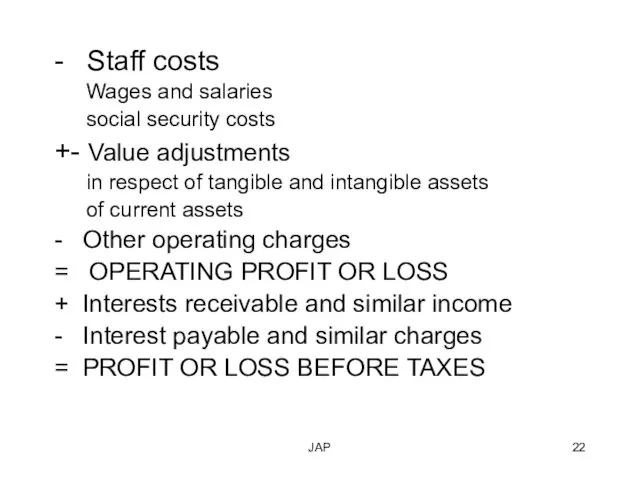

- 21. JAP INCOME STATEMENT NET TURNOVER - Variation in stock of finished goods and work in progress

- 22. JAP - Staff costs Wages and salaries social security costs +- Value adjustments in respect of

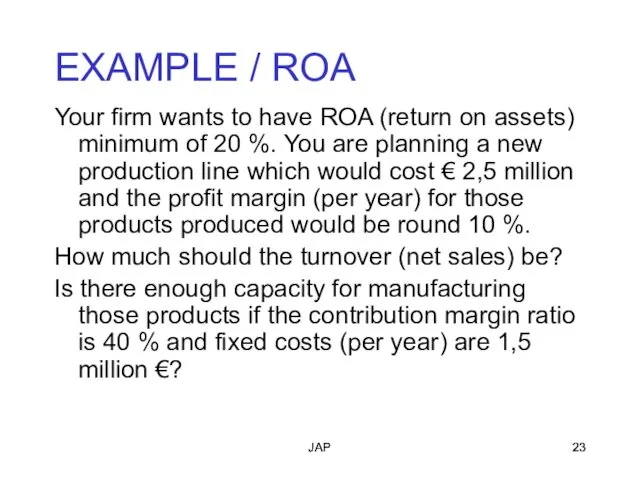

- 23. JAP JAP EXAMPLE / ROA Your firm wants to have ROA (return on assets) minimum of

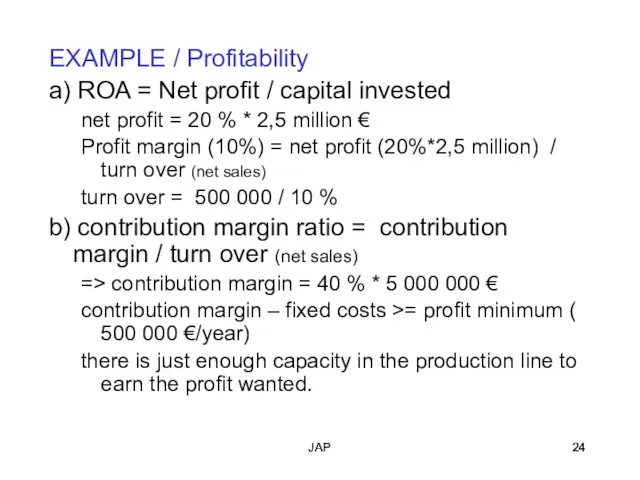

- 24. JAP JAP EXAMPLE / Profitability a) ROA = Net profit / capital invested net profit =

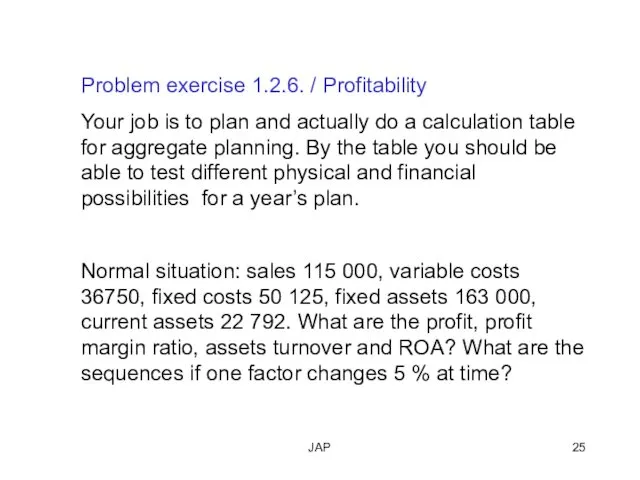

- 25. JAP Problem exercise 1.2.6. / Profitability Your job is to plan and actually do a calculation

- 26. JAP Exercise 7 / Profitability As a president of Mölkky Oy you find that one of

- 27. JAP help for exercises 1.2.6 and 1.2.7

- 28. JAP Problem exercise 1.2.8. /Profitability How can You reach a 100% increase in profit when the

- 29. JAP Target Costing Market Price (an estimate or real price of a product a company is

- 30. JAP Euros Target Cost Production Cost Money we can use for development Throughput time Cost This

- 31. JAP Example of New Production Method development project at planning at half phase way Estimated Output

- 32. JAP What is a Process? We define process to be any activity or group of activities

- 33. JAP PROCESSES AND OPERATIONS Inputs: Workers Managers Equipment Facilities Materials Services Land Energy Outputs: services goods

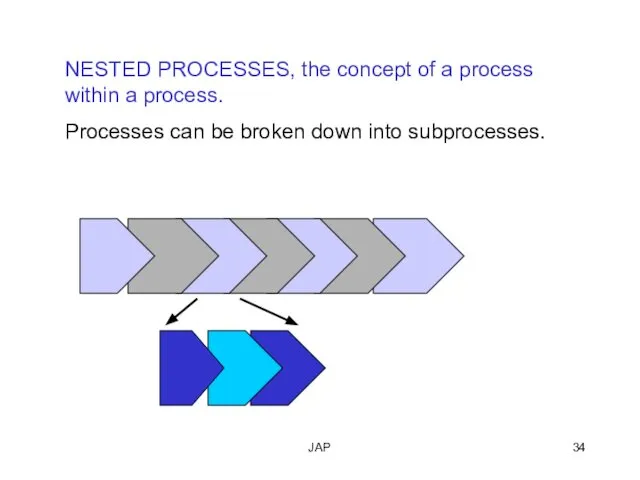

- 34. JAP NESTED PROCESSES, the concept of a process within a process. Processes can be broken down

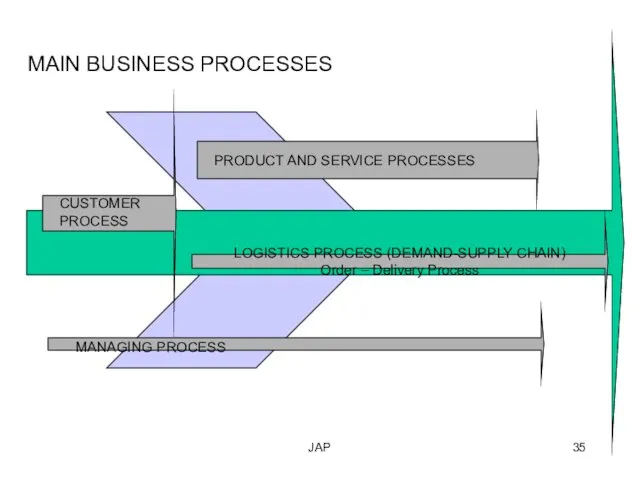

- 35. JAP LOGISTICS PROCESS (DEMAND-SUPPLY CHAIN) Order – Delivery Process PRODUCT AND SERVICE PROCESSES CUSTOMER PROCESS MAIN

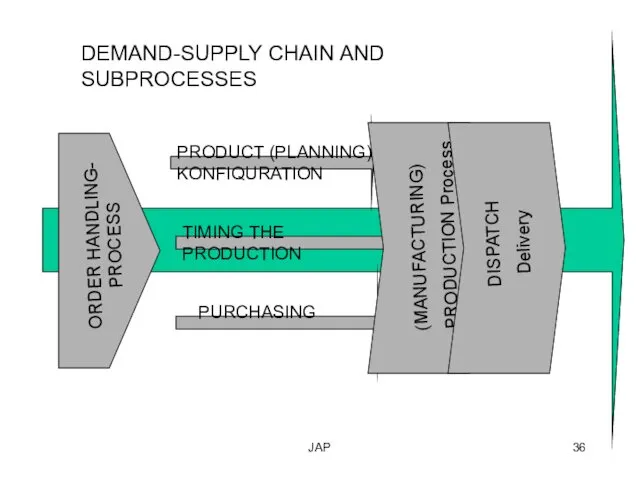

- 36. JAP DEMAND-SUPPLY CHAIN AND SUBPROCESSES PRODUCT (PLANNING) KONFIQURATION PURCHASING TIMING THE PRODUCTION (MANUFACTURING) PRODUCTION Process DISPATCH

- 37. JAP CASE NOKIA: CUSTOMER SATISFACTION PROCESS is a process for systematic customer satisfaction and competition/competitor evaluations.

- 38. JAP What is Operations Management / Process Management (Krajewski & Ritzman)? Operations Management term refers to

- 39. JAP Major Process for manufacturing/production process decisions: Process choice: A process decision that determines whether resources

- 40. JAP Logistics (vertical) Integration SUPPLIERS SUPPLIERS SUPPLIERS CUSTOMERS CUSTOMERS CUSTOMERS OPERATIONS OPERATIONS OPERATIONS LOGISTICS ACTIVITIES A)

- 41. JAP Enterprise Competitiveness and Operations Function There are four (five) dimensions of competitiveness that measure the

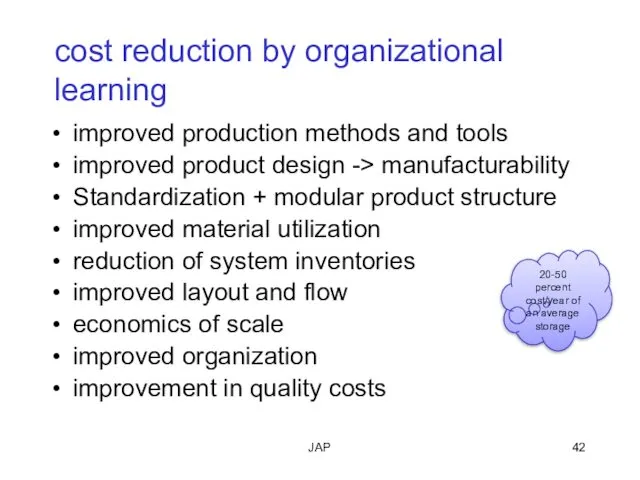

- 42. JAP cost reduction by organizational learning improved production methods and tools improved product design -> manufacturability

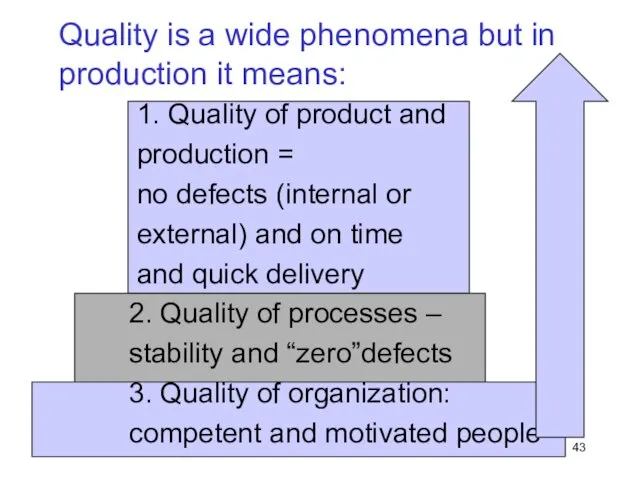

- 43. JAP Quality is a wide phenomena but in production it means: 1. Quality of product and

- 44. JAP High-performance design: Determination of the level of operations performance required in making a product or

- 45. JAP “Time is money”: Short delivery time: The elapsed time between receiving a customer’s order and

- 46. JAP Time based competition: The process by which managers define the steps and time needed to

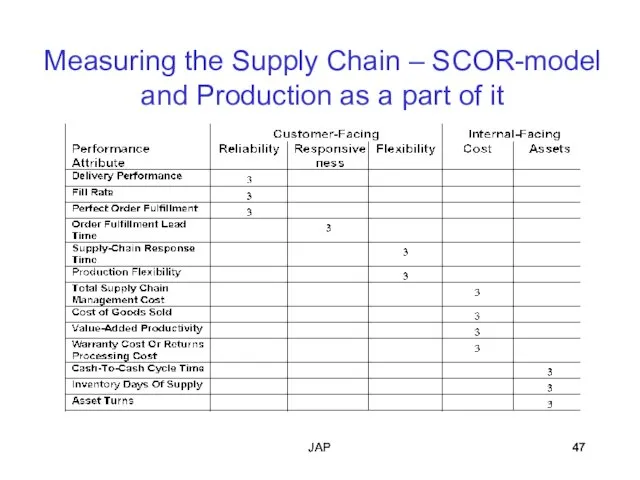

- 47. JAP JAP Measuring the Supply Chain – SCOR-model and Production as a part of it

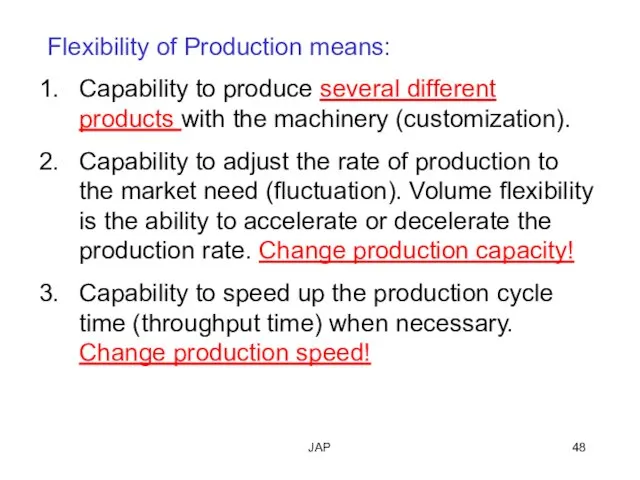

- 48. JAP Flexibility of Production means: Capability to produce several different products with the machinery (customization). Capability

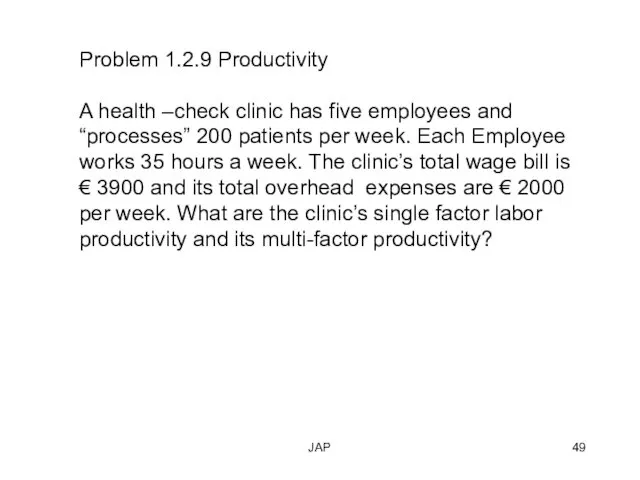

- 49. JAP Problem 1.2.9 Productivity A health –check clinic has five employees and “processes” 200 patients per

- 51. Скачать презентацию

JAP

LEARNING GOALS after these lessons you will be able to

describe

JAP

LEARNING GOALS after these lessons you will be able to

describe

JAP

LEARNING GOALS after these lessons you will be able to

7. discuss

JAP

LEARNING GOALS after these lessons you will be able to

7. discuss

JAP

JAP

What is a Productive system (Buffa), what is a Process (Krajewski&

JAP

JAP

What is a Productive system (Buffa), what is a Process (Krajewski&

JAP

EXAMPLES OF PRODUCTIVE SYSTEMS:

Electronics assembly

Airplane manufacturing

Steel production

Automobile assembly

Oil refining

Fast food

JAP

EXAMPLES OF PRODUCTIVE SYSTEMS:

Electronics assembly

Airplane manufacturing

Steel production

Automobile assembly

Oil refining

Fast food

JAP

Why must a system has to be productive?

JAP

Why must a system has to be productive?

Company’s competitiveness increasess

JAP

JAP

Why must a system have to be productive?

PROFITABILITY

and

Company’s competitiveness increasess

JAP

JAP

Why must a system have to be productive?

PROFITABILITY

and

JAP

JAP

What is a Productive system ?

(Buffa means here production system)

We define

JAP

JAP

What is a Productive system ?

(Buffa means here production system)

We define

JAP

PRODUCTIVITY (is the value of outputs (goods, services) produced and divided

JAP

PRODUCTIVITY (is the value of outputs (goods, services) produced and divided

JAP

example 1 / productivity

Calculate the productivity for the following operations:

a) Three

JAP

example 1 / productivity

Calculate the productivity for the following operations:

a) Three

JAP

Labor productivity = Processes policies / Employee hours

600 policies / week

JAP

Labor productivity = Processes policies / Employee hours

600 policies / week

JAP

Problem exercise 1.2.1. / Productivity, case state ferry

A state ferry charges

JAP

Problem exercise 1.2.1. / Productivity, case state ferry

A state ferry charges

JAP

Problem exercise 1.2.2 / Productivity, how to measure it?

You have a

JAP

Problem exercise 1.2.2 / Productivity, how to measure it?

You have a

JAP

Problem exercise 1.2.3. Productivity in University

Student tuition at University in US

JAP

Problem exercise 1.2.3. Productivity in University

Student tuition at University in US

JAP

Problem exercise 1.2.4. Productivity, case garments

Natalie Attired makes fashionable garments. During

JAP

Problem exercise 1.2.4. Productivity, case garments

Natalie Attired makes fashionable garments. During

JAP

Exercise 1.2.5. Productivity, case uniform manufacturing

The Big Black Bird Company (BBBC)

JAP

Exercise 1.2.5. Productivity, case uniform manufacturing

The Big Black Bird Company (BBBC)

JAP

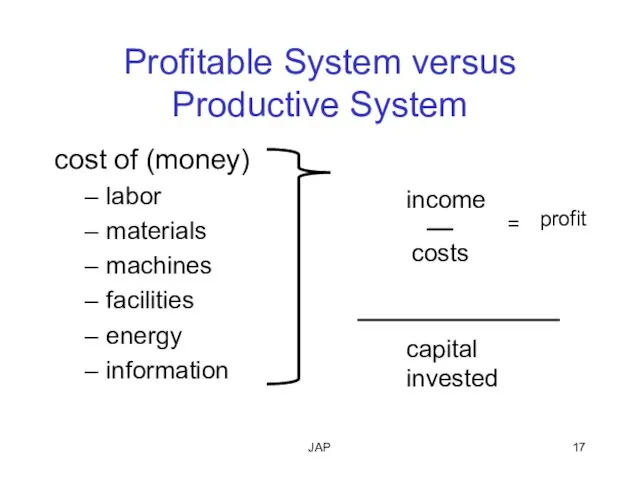

Profitable System versus Productive System

cost of (money)

labor

materials

machines

facilities

energy

information

capital invested

income

costs

=

profit

JAP

Profitable System versus Productive System

cost of (money)

labor

materials

machines

facilities

energy

information

capital invested

income

costs

=

profit

JAP

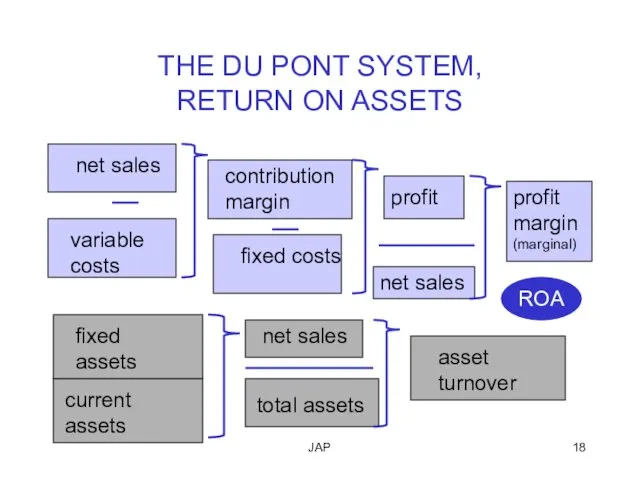

THE DU PONT SYSTEM,

RETURN ON ASSETS

net sales

variable costs

contribution margin

fixed costs

profit

net

JAP

THE DU PONT SYSTEM,

RETURN ON ASSETS

net sales

variable costs

contribution margin

fixed costs

profit

net

JAP

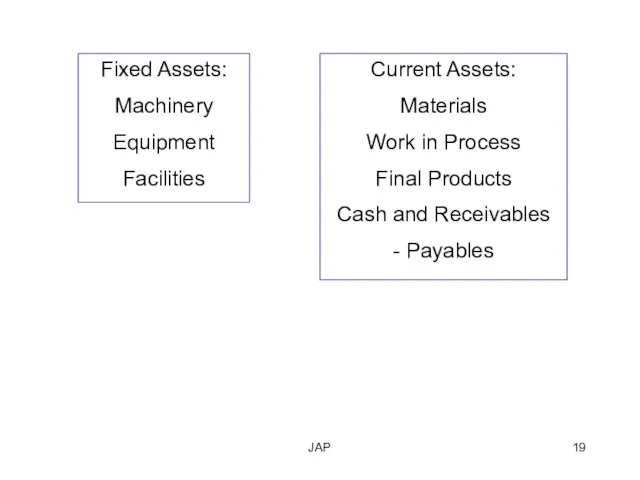

Fixed Assets:

Machinery

Equipment

Facilities

Current Assets:

Materials

Work in Process

Final Products

Cash and Receivables

- Payables

JAP

Fixed Assets:

Machinery

Equipment

Facilities

Current Assets:

Materials

Work in Process

Final Products

Cash and Receivables

- Payables

JAP

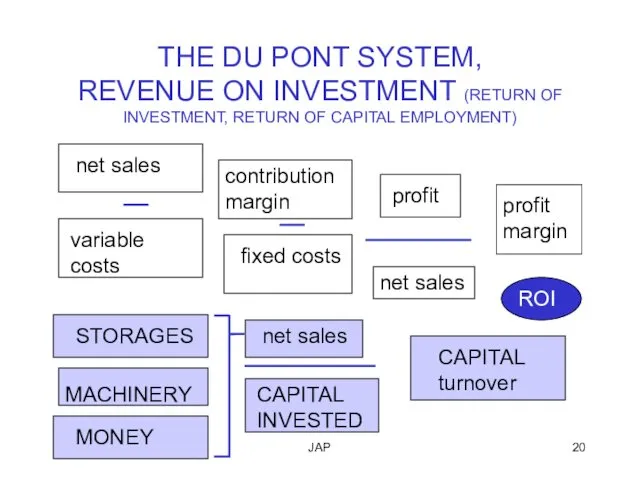

THE DU PONT SYSTEM,

REVENUE ON INVESTMENT (RETURN OF INVESTMENT, RETURN OF

JAP

THE DU PONT SYSTEM, REVENUE ON INVESTMENT (RETURN OF INVESTMENT, RETURN OF

JAP

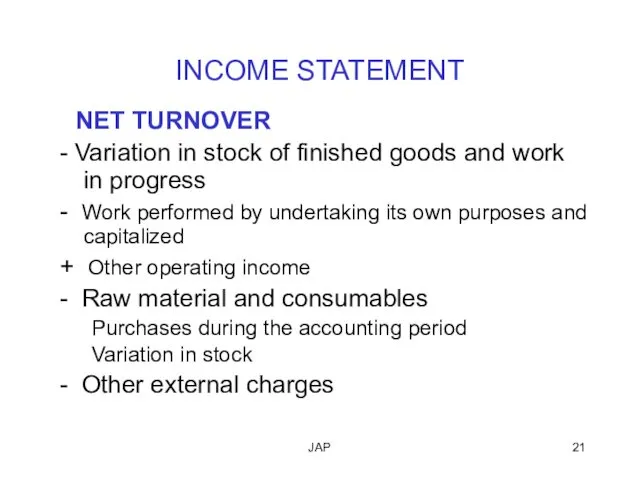

INCOME STATEMENT

NET TURNOVER

- Variation in stock of finished goods and

JAP

INCOME STATEMENT

NET TURNOVER

- Variation in stock of finished goods and

JAP

- Staff costs

Wages and salaries

social security costs

+- Value adjustments

in respect of

JAP

- Staff costs

Wages and salaries

social security costs

+- Value adjustments

in respect of

JAP

JAP

EXAMPLE / ROA

Your firm wants to have ROA (return on assets)

JAP

JAP

EXAMPLE / ROA

Your firm wants to have ROA (return on assets)

JAP

JAP

EXAMPLE / Profitability

a) ROA = Net profit / capital invested

net profit

JAP

JAP

EXAMPLE / Profitability

a) ROA = Net profit / capital invested

net profit

JAP

Problem exercise 1.2.6. / Profitability

Your job is to plan and actually

JAP

Problem exercise 1.2.6. / Profitability

Your job is to plan and actually

JAP

Exercise 7 / Profitability

As a president of Mölkky Oy you find

JAP

Exercise 7 / Profitability

As a president of Mölkky Oy you find

JAP

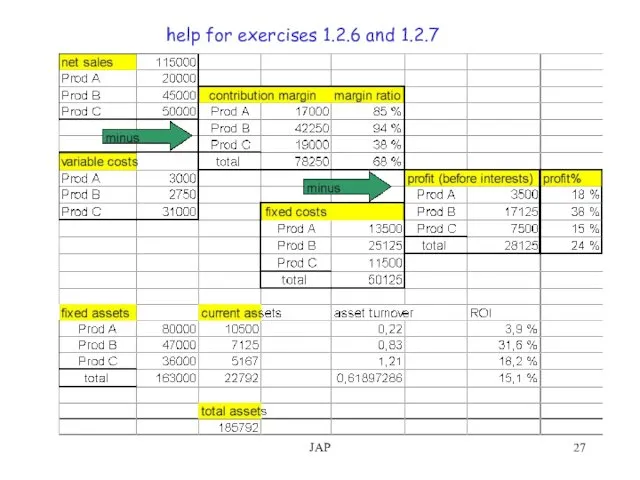

help for exercises 1.2.6 and 1.2.7

JAP

help for exercises 1.2.6 and 1.2.7

JAP

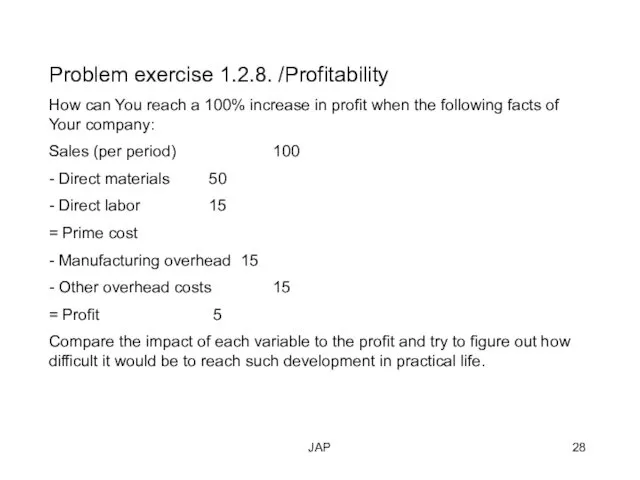

Problem exercise 1.2.8. /Profitability

How can You reach a 100% increase in

JAP

Problem exercise 1.2.8. /Profitability

How can You reach a 100% increase in

JAP

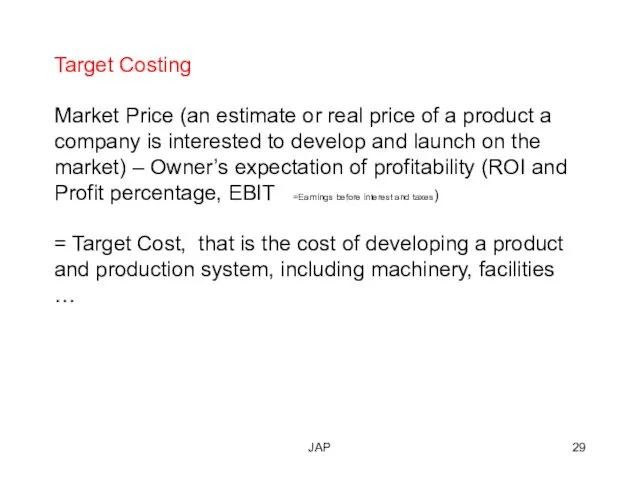

Target Costing

Market Price (an estimate or real price of a product

JAP

Target Costing

Market Price (an estimate or real price of a product

JAP

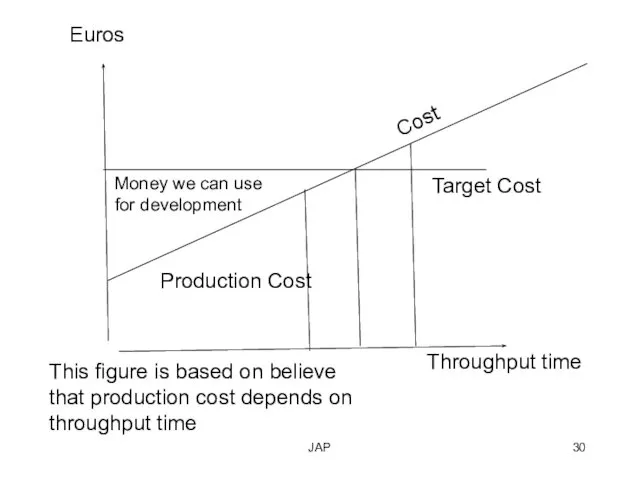

Euros

Target Cost

Production Cost

Money we can use for development

Throughput time

Cost

This figure is

JAP

Euros

Target Cost

Production Cost

Money we can use for development

Throughput time

Cost

This figure is

JAP

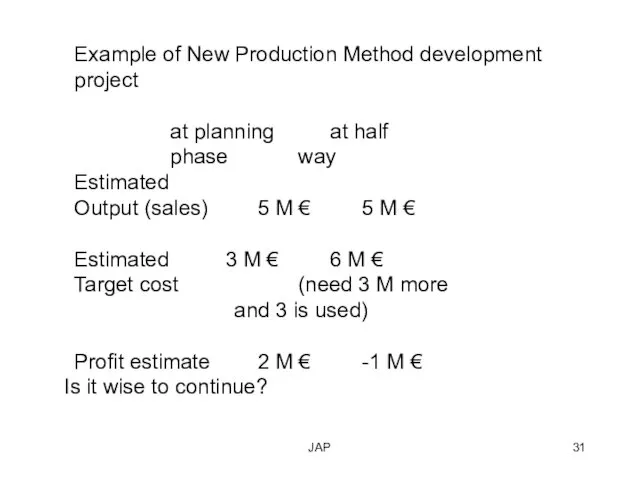

Example of New Production Method development project

at planning at half

phase way

Estimated

Output (sales) 5

JAP

Example of New Production Method development project

at planning at half

phase way

Estimated

Output (sales) 5

JAP

What is a Process?

We define process to be any activity or

JAP

What is a Process?

We define process to be any activity or

JAP

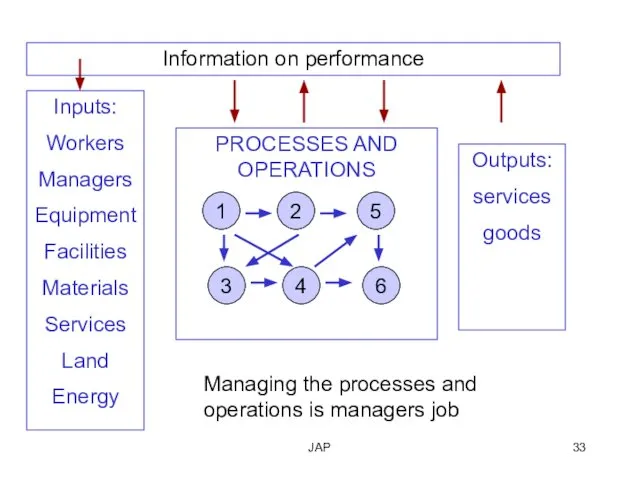

PROCESSES AND OPERATIONS

Inputs:

Workers

Managers

Equipment

Facilities

Materials

Services

Land

Energy

Outputs:

services

goods

1

3

6

5

2

4

Information on performance

Managing the processes and operations is managers

JAP

PROCESSES AND OPERATIONS

Inputs:

Workers

Managers

Equipment

Facilities

Materials

Services

Land

Energy

Outputs:

services

goods

1

3

6

5

2

4

Information on performance

Managing the processes and operations is managers

JAP

NESTED PROCESSES, the concept of a process within a process.

Processes can

JAP

NESTED PROCESSES, the concept of a process within a process.

Processes can

JAP

LOGISTICS PROCESS (DEMAND-SUPPLY CHAIN)

Order – Delivery Process

PRODUCT AND SERVICE PROCESSES

CUSTOMER PROCESS

MAIN

JAP

LOGISTICS PROCESS (DEMAND-SUPPLY CHAIN)

Order – Delivery Process

PRODUCT AND SERVICE PROCESSES

CUSTOMER PROCESS

MAIN

JAP

DEMAND-SUPPLY CHAIN AND SUBPROCESSES

PRODUCT (PLANNING) KONFIQURATION

PURCHASING

TIMING THE PRODUCTION

(MANUFACTURING)

PRODUCTION Process

DISPATCH

Delivery

ORDER HANDLING- PROCESS

JAP

DEMAND-SUPPLY CHAIN AND SUBPROCESSES

PRODUCT (PLANNING) KONFIQURATION

PURCHASING

TIMING THE PRODUCTION

(MANUFACTURING)

PRODUCTION Process

DISPATCH

Delivery

ORDER HANDLING- PROCESS

JAP

CASE NOKIA:

CUSTOMER SATISFACTION PROCESS is a process for systematic customer satisfaction

JAP

CASE NOKIA:

CUSTOMER SATISFACTION PROCESS is a process for systematic customer satisfaction

JAP

What is Operations Management / Process Management (Krajewski & Ritzman)?

Operations Management

JAP

What is Operations Management / Process Management (Krajewski & Ritzman)?

Operations Management

JAP

Major Process for manufacturing/production process decisions:

Process choice: A process decision that

JAP

Major Process for manufacturing/production process decisions:

Process choice: A process decision that

JAP

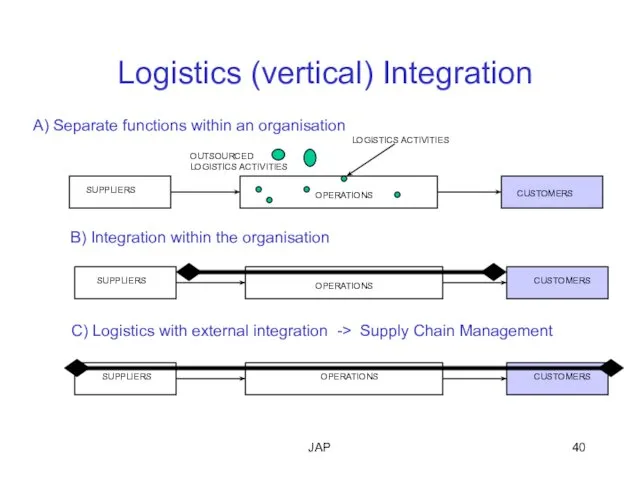

Logistics (vertical) Integration

SUPPLIERS

SUPPLIERS

SUPPLIERS

CUSTOMERS

CUSTOMERS

CUSTOMERS

OPERATIONS

OPERATIONS

OPERATIONS

LOGISTICS ACTIVITIES

A) Separate functions within an organisation

B) Integration within

JAP

Logistics (vertical) Integration

SUPPLIERS

SUPPLIERS

SUPPLIERS

CUSTOMERS

CUSTOMERS

CUSTOMERS

OPERATIONS

OPERATIONS

OPERATIONS

LOGISTICS ACTIVITIES

A) Separate functions within an organisation

B) Integration within

JAP

Enterprise Competitiveness and Operations Function

There are four (five) dimensions of competitiveness

JAP

Enterprise Competitiveness and Operations Function

There are four (five) dimensions of competitiveness

JAP

cost reduction by organizational learning

improved production methods and tools

improved product design

JAP

cost reduction by organizational learning

improved production methods and tools

improved product design

JAP

Quality is a wide phenomena but in production it means:

JAP

Quality is a wide phenomena but in production it means:

JAP

High-performance design: Determination of the level of operations performance required in

JAP

High-performance design: Determination of the level of operations performance required in

JAP

“Time is money”:

Short delivery time: The elapsed time between receiving a

JAP

“Time is money”:

Short delivery time: The elapsed time between receiving a

JAP

Time based competition: The process by which managers define the steps

JAP

Time based competition: The process by which managers define the steps

JAP

JAP

Measuring the Supply Chain – SCOR-model and Production as a part

JAP

JAP

Measuring the Supply Chain – SCOR-model and Production as a part

JAP

Flexibility of Production means:

Capability to produce several different products with the

JAP

Flexibility of Production means:

Capability to produce several different products with the

JAP

Problem 1.2.9 Productivity

A health –check clinic has five employees and “processes”

JAP

Problem 1.2.9 Productivity

A health –check clinic has five employees and “processes”

Организационная культура

Организационная культура Повышение эффективности оптовых продаж с помощью автоматизации отдела сбыта

Повышение эффективности оптовых продаж с помощью автоматизации отдела сбыта Транспортная логистика

Транспортная логистика Модель управления в Индии

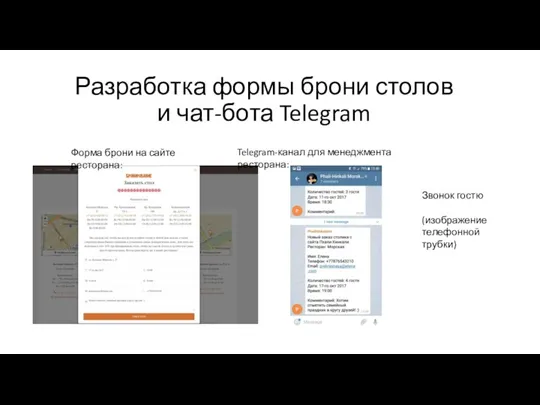

Модель управления в Индии Разработка формы брони столов и чат-бота Telegram

Разработка формы брони столов и чат-бота Telegram Управление инновационными проектами

Управление инновационными проектами Корпоративная культура

Корпоративная культура Организация и управление

Организация и управление Научные основы управления

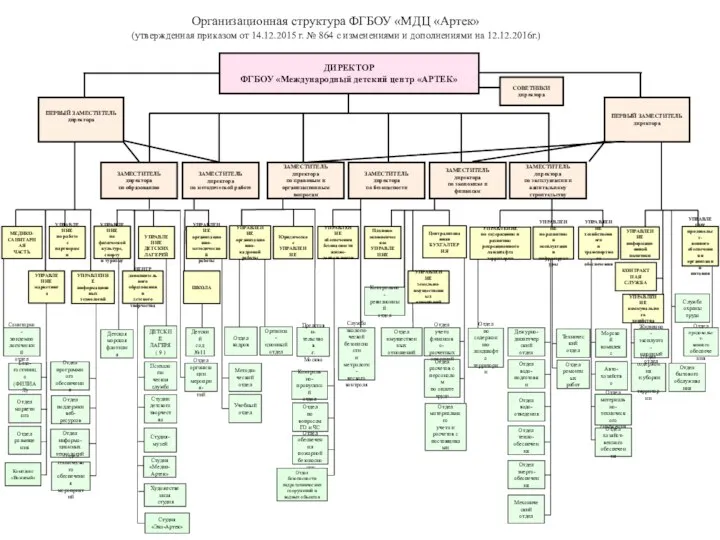

Научные основы управления Организационная структура ФГБОУ МДЦ Артек

Организационная структура ФГБОУ МДЦ Артек Коммуникационный менеджмент

Коммуникационный менеджмент Кто такой лидер

Кто такой лидер Трудовая адаптация персонала на предприятии

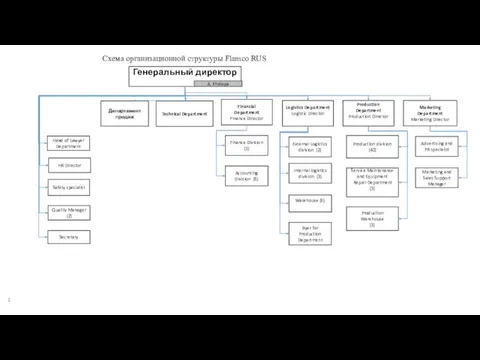

Трудовая адаптация персонала на предприятии Схема организационной структуры Flamco RUS

Схема организационной структуры Flamco RUS Определение деловых коммуникаций

Определение деловых коммуникаций Совершенствование системы логистики снабжения. ОАО Нижнекамский хлебокомбинат

Совершенствование системы логистики снабжения. ОАО Нижнекамский хлебокомбинат Планирование, контроль, учет в управленческом цикле

Планирование, контроль, учет в управленческом цикле Проектирование эффективных региональных моделей управления образовательными организациями

Проектирование эффективных региональных моделей управления образовательными организациями Дисфункциональность и несостоятельность государственного и муниципального управления. Лекция 7

Дисфункциональность и несостоятельность государственного и муниципального управления. Лекция 7 Стэйкхолдерская модель корпорации

Стэйкхолдерская модель корпорации Матрица MCC: Mission and Core Competencies (МКК: Миссия и Ключевые компетенции)

Матрица MCC: Mission and Core Competencies (МКК: Миссия и Ключевые компетенции) Построение системы управления персоналом

Построение системы управления персоналом Организационное развитие. Общий взгляд на проблему

Организационное развитие. Общий взгляд на проблему Разработка рекламного модуля для сувенирной продукции для кафе-бара Корейской кухни Kannam Chicken

Разработка рекламного модуля для сувенирной продукции для кафе-бара Корейской кухни Kannam Chicken Системы менеджмента качества

Системы менеджмента качества Классификация информации. Управленческая информация

Классификация информации. Управленческая информация Планирование – как функция менеджмента

Планирование – как функция менеджмента Советник, которому доверяют

Советник, которому доверяют